finance

financeSimilar presentations:

Corporate Finance

1. Corporate Finance

CORPORATE FINANCEElena Rogova, professor, e.rogova@gsom.spbu.ru

Fall semester, 2025-2026

2. Capital Structure - Definition

• Capital Structure refers to the mix of long-term sources of funds usedby the firm.

• Capital structure should be well planned generally keeping in view the

interest of the equity shareholders and the financial requirements of a

company.

Value of the Firm:

V=D+E

Debt

Equity

01.12.2025

2

3. The Choices in Financing

There are only two ways in which a business can make moneyDebt:

The essence of debt is that you

promise to make fixed payments in

the future (interest payments and

repaying principal). If you

fail to make those payments, you lose

control of your business.

01.12.2025

OR

Equity:

With equity, you do get

whatever cash flows are

left over after you have

made debt payments

3

4. Debt: Summarizing the Trade Off

Advantages of BorrowingTax Shield

Added Discipline

Disadvantages of Borrowing

Bankruptcy costs

Agency costs

Loss of Future Flexibility

01.12.2025

4

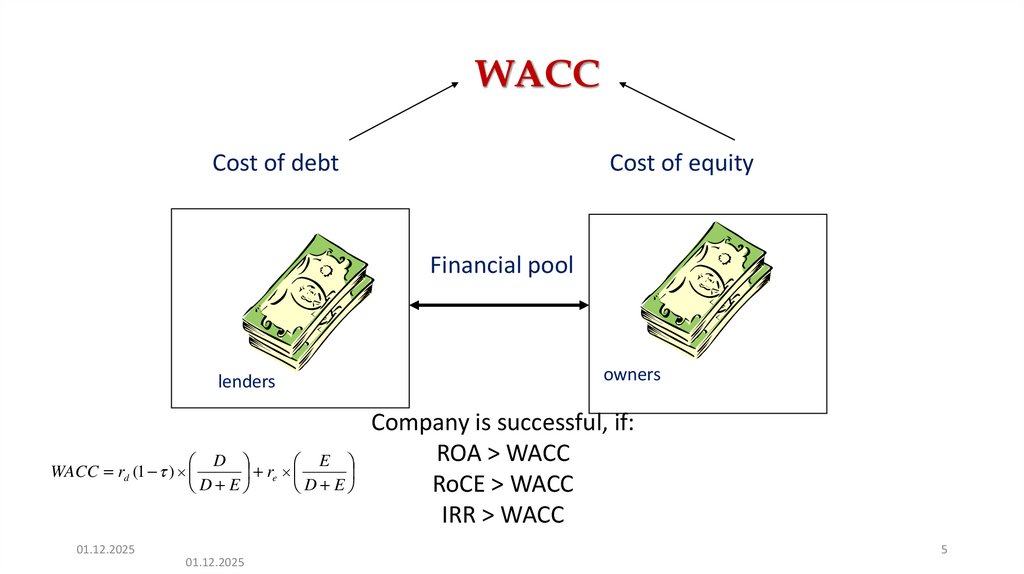

5.

WACCCost of debt

Cost of equity

Financial pool

lenders

owners

Company is successful, if:

ROA > WACC

D

E

WACC r (1 )

r

RoCE > WACC

D E

D E

IRR > WACC

d

01.12.2025

e

01.12.2025

5

6. Capital Structure Theories

• The total capital structure theories can be categorised into two relevantand irrelevant theories.

The following are the main theories/Approaches of capital structure:

1. Net Income Approach

2. Modigliani and Miller Approach

3. Traditional Approach

4. Comparables Approach

01.12.2025

6

7.

Topic 5. CapitalStructure

Optimisation

01.12.2025

Topic 4. Capital

Structure

Theories

7

8. A Framework for Getting to the Optimal

01.12.20258

9. Approaches to the Optimal Capital Structure

1. The Cost of Capital Approach: The optimal debt ratio is the one thatminimizes the cost of capital for a firm.

2. The Adjusted Present Value Approach: The optimal debt ratio is the

one that maximizes the overall value of the firm.

3. The Sector Approach: The optimal debt ratio is the one that brings

the firm closes to its peer group in terms of financing mix.

4. The Life Cycle Approach: The optimal debt ratio is the one that best

suits where the firm is in its life cycle.

01.12.2025

9

10. The Cost of Capital Approach

• Value of a Firm = Present Value of Cash Flows to the Firm, discountedback at the cost of capital.

• If the cash flows to the firm are held constant, and the cost of capital

is minimized, the value of the firm will be maximized.

01.12.2025

10

11. Measuring Cost of Capital

• The cost of debt is the market interest rate that the firm has to pay on its longterm borrowing today, net of tax benefits. It will be a function of:The long-term risk-free rate

The default spread for the company, reflecting its credit risk

The firm’s marginal tax rate

• The cost of equity reflects the expected return demanded by marginal equity

investors. If they are diversified, only the portion of the equity risk that cannot be

diversified away (beta or betas) will be priced into the cost of equity.

• The cost of capital is the cost of each component weighted by its relative market

value.

Cost of capital (WACC) = Cost of equity (E/(D+E)) + After-tax cost of debt (D/(D+E))

01.12.2025

11

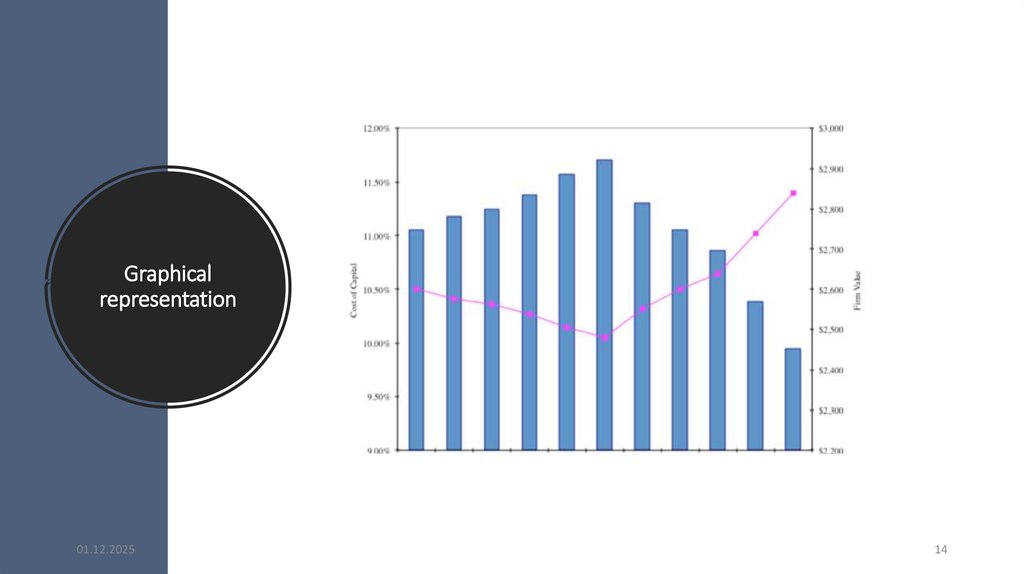

12. Applying Cost of Capital Approach: The Example

Assume the firm has $200 million in cash flows, expected to grow 3% a year forever.01.12.2025

12

13. Applying Cost of Capital Approach: The Example

Assume the firm has $200 million in cash flows, expected to grow 3% a year forever.01.12.2025

13

14.

Graphicalrepresentation

01.12.2025

14

15. Current Cost of Capital: Norilsk Nickel

• The beta for NN’s stock in December 2021 was 0.99. The T. bond rate at that time was2.80%. Using an estimated equity risk premium for Russia of 8.60%, we estimated the

cost of equity for NN:

Cost of Equity = 2.80% + 0.99(8.60%) = 11.31%

• NN’s bond rating in December 2021 was BBB, and based on this rating, the spread is

1.99% and estimated pretax cost of debt for NN is 2.80+1.99 = 4.79%. Using a tax rate of

20%, the after-tax cost of debt for NN:

After-Tax Cost of Debt =4.79% (1 – 0.20) =3.832%

• The cost of capital was calculated using these costs and the weights based on market

values of equity (3,505) and debt (759.7):

Cost of capital = 3.832%*(759.7/(3,505+759.7))+11.31%*(3,505/(3,505+759.7))=9.98%

• Average D/E for 5 years = 0.2329

01.12.2025

15

16. Mechanics of Cost of Capital Estimation

1. Estimate the Cost of Equity at different levels of debt:Equity will become riskier -> Beta will increase -> Cost of Equity will increase.

Estimation will use levered beta calculation

2. Estimate the Cost of Debt at different levels of debt:

Default risk will go up, and bond ratings will go down as debt goes up -> Cost

of Debt will increase.

To estimating bond ratings, we may use the TIE ratio (EBIT/Interest expense)

3. Estimate the Cost of Capital at different levels of debt

4. Calculate the effect on Firm Value and Stock Price.

01.12.2025

16

17. Cost of equity: estimate the unlevered beta for the firm

• The Regression Beta: One approach is to use the regression beta (0.99) and thenunlever, using the average debt to equity ratio (23.29%) during the period of the

regression.

Unlevered beta = 0.99 / (1 + 0.2329(1 - 0.20))= 0.8345

• The Bottom-up Beta: Alternatively, we can back to the source and estimate it from

the betas of the businesses.

• If the company has several businesses, we calculate the proportion of each business

in the value of the company (using EV/Sales ratio), find unlevered betas for each

business and then weight them

• Simplified approach for NN: use only mining and metals: unlevered beta is 1.19

• 2/3 of the final estimate comes from the regression beta and 1/3 from the bottomup beta

• The final estimate: beta = 0.8325*2/3+1.19*1/3 = 0.952

01.12.2025

17

18. NN’s financials

20212020

Revenues, bn rub

EBITDA, bn

Depreciation and amortization

1117

751

290

878

543

87

EBIT

Interest expenses

TIE (Interest Coverage Ratio)

461

63.1

7.31

456

19.7

23.1

CAPEX

FCF

242.9

415.9

103.7

348.1

01.12.2025

18

19. Cost of Equity

Debt ratio D/ELevered ß

Risk-free

rate

MRP

Cost pf

equity

0%

0%

0.952

2.80%

8.60%

10.99%

10%

11.11%

1.037

2.80%

8.60%

11.72%

20%

25%

1.143

2.80%

8.60%

12.63%

30%

42.86%

1.279

2.80%

8.60%

13.80%

40%

66.67%

1.461

2.80%

8.60%

15.36%

50%

100%

1.715

2.80%

8.60%

17.55%

60%

150%

2.096

2.80%

8.60%

20.83%

70%

233.33%

2.731

2.80%

8.60%

26.29%

80%

400%

4.002

2.80%

8.60%

37.21%

90%

900%

7.813

2.80%

8.60%

69.99%

D

(1 tax rate))

E

CoE rf L MRP

L U (1

01.12.2025

19

20. Assumptions

• In calculating the levered beta in this table, we assumed that all market risk isborne by the equity investors; this may be unrealistic especially at higher levels of

debt.

• We can also consider an alternative estimate of levered betas that apportions

some of the market risk to the debt:

• levered = u [1+(1-t)D/E] - debt (1-t) D/E

• The beta of debt is based upon the rating of the bond and is estimated by

regressing past returns on bonds in each rating class against returns on a market

index. The levered betas estimated using this approach will generally be lower

than those estimated with the conventional model

01.12.2025

20

21. The Ratings Table

Interest coverage ratio is> 8.50

6.5 – 8.5

5.5 – 6.5

4.25 – 5.5

3 – 4.25

2.5 -3

2.25 –2.5

2 – 2.25

1.75 -2

1.5 – 1.75

1.25 -1.5

0.8 -1.25

0.65 – 0.8

0.2 – 0.65

<0.2

01.12.2025

Rating is

Aaa/AAA

Aa2/AA

A1/A+

A2/A

A3/ABaa2/BBB

Ba1/BB+

Ba2/BB

B1/B+

B2/B

B3/BCaa/CCC

Ca2/CC

C2/C

D2/D

Spread is

0.40%

0.70%

0.85%

1.00%

1.30%

2.00%

3.00%

4.00%

5.50%

6.50%

7.25%

8.75%

9.50%

10.50%

12.00%

Interest rate

3.20%

3.50%

3.65%

3.80%

4.10%

4.80%

5.80%

6.80%

8.30%

9.30%

10.05%

11.55%

12.30%

13.30%

14.80%

T.Bond rate =2.80%

21

22. Estimating Cost of Debt

Start with the market value of the firm = 3,505.0+759.7 = 4,264.7 bn rublesD/(D+E)

0.00% 10.00% (Debt to capital)

D/E

0.00% 11.11% (D/E = 10/90 = 0.1111)

Debt

0

426.5 (10% of 4,264.7)

EBITDA

EBIT

Interest

751

461

$0

751

461

14

(Same as 0% debt)

(Same as 0% debt)

(Pre-tax cost of debt * Debt)

Pre-tax TIE

∞

31.3

(EBIT/ Interest Expenses)

Likely Rating

AAA

AA

(From Ratings table)

Pre-tax cost of debt 3.20% 3.50% (Riskless Rate + Spread)

01.12.2025

22

23. Test: Can you do the 30% level?

D/(D + E)20.00%

D/E

25.00%

Debt

852,9

EBIT

461

Interest expense

41

Interest coverage ratio

11.4

Likely rating

BBB

Pretax cost of debt

4.80%

01.12.2025

Iteration 1

(Debt @BBB rate)

30.00%

Iteration 2

(Debt @BB rate)

30.00%

23

24. Bond Ratings, Cost of Debt and Debt Ratios

DebtRatio

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

$ Debt

0

426.5

852,9

1279.4

1705.9

2132.35

2558.9

2985.3

3411.8

3838.2

01.12.2025

Interest

Expense

0

14.71

40.51

60.77

115.15

143.93

255.9

298.5

417.95

508.56

Interest

Coverage

Ratio

∞

31.3

11.4

7.58

4.00

3.2

1.80

1.54

1.1

0.90

Bond Rating

AAA

AA

A

BBB

BB

BB

BBCC

C

Pre-tax

cost of

debt

3.20%

3.50%

3.80%

4.80%

6.80%

6.80%

10.05%

10.05%

12.30%

13.30%

Tax rate

20%

20%

20%

20%

20%

20%

20%

20%

20%

20%

After-tax

cost of debt

2.56%

2.80%

3.04%

3.84%

5.44%

5.44%

8.04%

8.04%

9.84%

10.64%

24

25. NN’s cost of capital schedule…

…NN’s cost of capital schedule

Debt ratio

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Beta

0,952

1,037

1,143

1,279

1,461

1,715

2,096

2,731

4,002

7,813

Cost of Equity

0,1099

0,1172

0,1263

0,138

0,1536

0,1755

0,2083

0,2629

0,3721

0,6999

Cost of Debt (after tax)

0,0256

0,0280

0,0304

0,0384

0,0544

0,0544

0,0804

0,0804

0,0984

0,1064

WACC

0,1099

0,10828

0,10712

0,10812

0,11392

0,11495

0,13156

0,13515

0,15434

0,16575

Nornikel has capital structure close to optimal

01.12.2025

25

26. Effect on Firm Value – Full Valuation

Step 1: Estimate the cash flows to firmStep 2: Back out the implied growth rate in the current market value

Growth rate = (Firm Value * Cost of Capital – CF to Firm)/(Firm Value + CF to Firm)

Step 3: Revalue the firm with the new cost of capital

FCFF0 (1 g)

Firm Value

(Cost of Capital -g)

01.12.2025

26

27. What if something goes wrong? The Downside Risk

• Sensitivity to AssumptionsA. “What if” analysis

The optimal debt ratio is a function of our inputs on operating income, tax rates and macro

variables. We could focus on one or two key variables – operating income is an obvious choice –

and look at history for guidance on volatility in that number and ask what if questions.

B. “Economic Scenario” Approach

We can develop possible scenarios, based upon macro variables, and examine the optimal

debt ratio under each one. For instance, we could look at the optimal debt ratio for a cyclical firm

under a boom economy, a regular economy and an economy in recession.

• Constraint on Bond Ratings/ Book Debt Ratios

Alternatively, we can put constraints on the optimal debt ratio to reduce exposure to downside

risk. Thus, we could require the firm to have a minimum rating, at the optimal debt ratio or to

have a book debt ratio that is less than a “specified” value.

01.12.2025

27

28. Limitations of the Cost of Capital approach

• It is static: The most critical number in the entire analysis is theoperating income. If that changes, the optimal debt ratio will

change.

• It ignores indirect bankruptcy costs: The operating income is

assumed to stay fixed as the debt ratio and the rating changes.

• Beta and Ratings: It is based upon rigid assumptions of how

market risk and default risk get borne as the firm borrows

more money and the resulting costs.

01.12.2025

28

29. The APV Approach to Optimal Capital Structure

• In the adjusted present value approach, the value of the firm is written asthe sum of the value of the firm without debt (the unlevered firm) and the

effect of debt on firm value

Firm Value = Unlevered Firm Value + (Tax Benefits of Debt - Expected Bankruptcy Cost

from the Debt)

• The optimal debt level is the one that maximizes firm value

01.12.2025

29

30. Implementing the APV Approach

• Step 1: Estimate the unlevered firm value. This can be done in one of two ways:• Estimating the unlevered beta, a cost of equity based upon the unlevered beta and valuing the

firm using this cost of equity (which will also be the cost of capital, with an unlevered firm)

• Alternatively, Unlevered Firm Value = Current Market Value of Firm - Tax Benefits of Debt

(Current) + Expected Bankruptcy cost from Debt

• Step 2: Estimate the tax benefits at different levels of debt. The simplest assumption

to make is that the savings are perpetual, in which case

• Tax benefits = Debt * Tax Rate

• Step 3: Estimate a probability of bankruptcy at each debt level, and multiply by the

cost of bankruptcy (including both direct and indirect costs) to estimate the

expected bankruptcy cost.

01.12.2025

30

31. Estimating Expected Bankruptcy Cost

• Probability of BankruptcyEstimate the synthetic rating that the firm will have at each level of debt

Estimate the probability that the firm will go bankrupt over time, at that

level of debt (Use studies that have estimated the empirical

probabilities of this occurring over time - Altman does an update every

year)

• Cost of Bankruptcy

The direct bankruptcy cost is the easier component. It is generally

between 5-10% of firm value, based upon empirical studies

The indirect bankruptcy cost is much tougher. It should be higher for

sectors where operating income is affected significantly by default risk

(like airlines) and lower for sectors where it is not (like groceries)

For simplicity, let’s assume that this cost is 25% of company’s value

01.12.2025

31

32. Ratings and Default Probabilities: Results from Altman study of bonds

RatingAAA

AA

A+

A

ABBB

BB

B+

B

BCCC

CC

C

D

01.12.2025

Likelihood of Default

0.07%

0.51%

0.60%

0.66%

2.50%

7.54%

16.63%

25.00%

36.80%

45.00%

59.01%

70.00%

85.00%

100.00%

Altman estimated these probabilities by

looking at bonds in each ratings class ten

years prior and then examining the

proportion of these bonds that defaulted

over the ten years.

32

33. NN: Estimating Unlevered Firm Value

Current Value of firm = 3,505+759.7 =4264,7 billion rubles

- Tax Benefit on Current Debt = 759.7 * 0.20

= 151.94

+ Expected Bankruptcy Cost = 0.66% * (0.25 * 4264.7) = 7.04

Unlevered Value of Firm =

4119.79 billion rubles

• Cost of Bankruptcy for NN = 25% of firm value

• Probability of Bankruptcy = 0.66%, based on firm’s current rating of A

• Tax Rate = 20%

01.12.2025

33

34. NN: APV at Debt Ratios

DebtRatio

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

01.12.2025

Tax

Debt

Rate

0

20%

426.5 20%

852.9 20%

1279.4 20%

1705.9 20%

2132.35 20%

2558.9 20%

2985.3 20%

3411.8 20%

3838.2 20%

Unlevered

Firm

Tax

Value

Benefits

4119.79

0

4119.79

85.2

4119.79

170.58

4119.79

255.88

4119.79

341.18

4119.79

426.47

4119.79

511.78

4119.79

597.06

4119.79

682.36

4119.79

767.64

Bond

Rating

AAA

AA

A

BBB

BB

B+

BBCC

C

34

Probability

of Default

0.07%

0.51%

0.66%

7.54%

16.63%

25%

45.00%

45.00%

70.00%

85.00%

Expected

Bankruptcy

Cost

0

5.44

7.04

80.39

177.30

266.54

479.78

479.78

746.32

906.25

Value of

Levered

Firm

4119.79

4199.55

4259.55

4295.28

4283.67

4279.72

4152.79

4237.07

4055.83

3981.18

35. Relative Analysis

• The “safest” place for any firm to be is close to the industry average• Subjective adjustments can be made to these averages to arrive at the

right debt ratio.

• Higher tax rates -> Higher debt ratios (Tax benefits)

• Lower insider ownership -> Higher debt ratios (Greater discipline)

• More stable income -> Higher debt ratios (Lower bankruptcy costs)

• More intangible assets -> Lower debt ratios (More agency problems)

01.12.2025

35

36. Getting past simple averages

Step 1: Run a regression of debt ratios on the variables that you believedetermine debt ratios in the sector. For example,

Debt Ratio = a + b (Tax rate) + c (Earnings Variability) + d (EBITDA/Firm Value)

Check this regression for statistical significance (t statistics) and

predictive ability (R squared)

Step 2: Estimate the values of the proxies for the firm under

consideration. Plugging into the cross-sectional regression, we can

obtain an estimate of predicted debt ratio.

Step 3: Compare the actual debt ratio to the predicted debt ratio.

01.12.2025

36

37. The Mechanics of Changing Debt Ratio quickly…

01.12.202537