mathematics

mathematicsSimilar presentations:

")

")

")

")

")

Jointly distributed discrete random variables (lecture 7)

1.

LECTURE 7JOINTLY DISTRIBUTED DISCRETE

RANDOM VARIABLES

2.

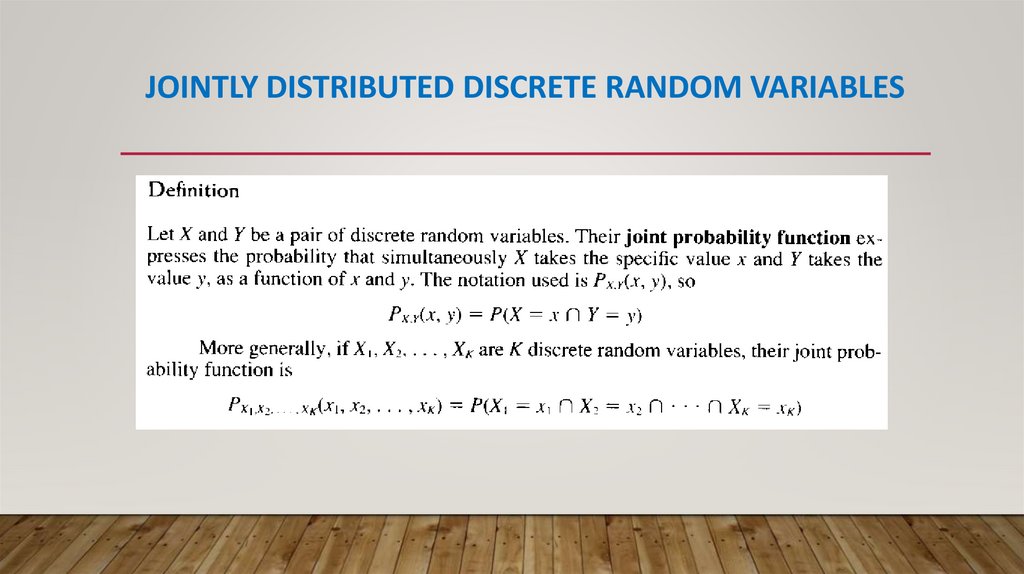

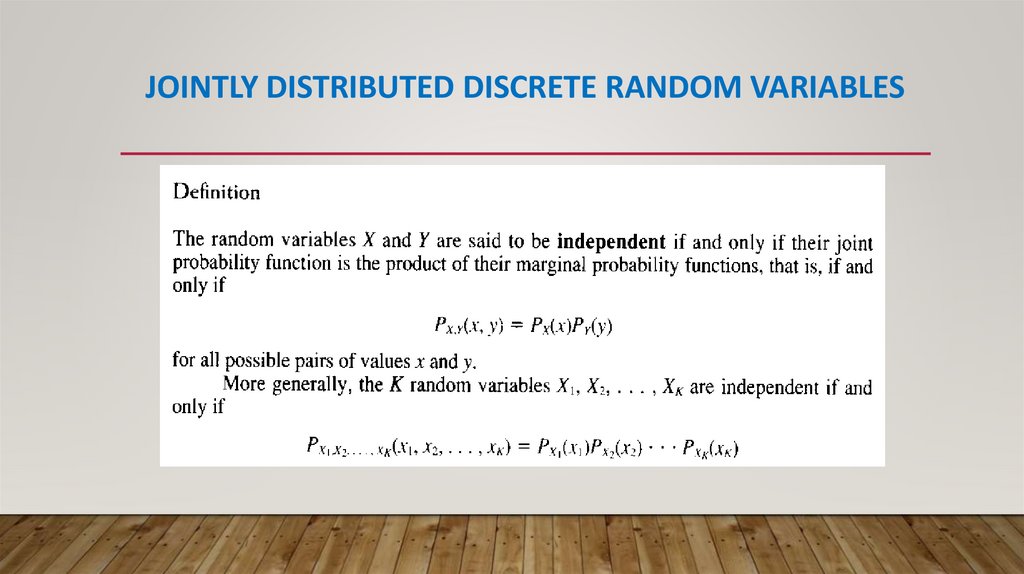

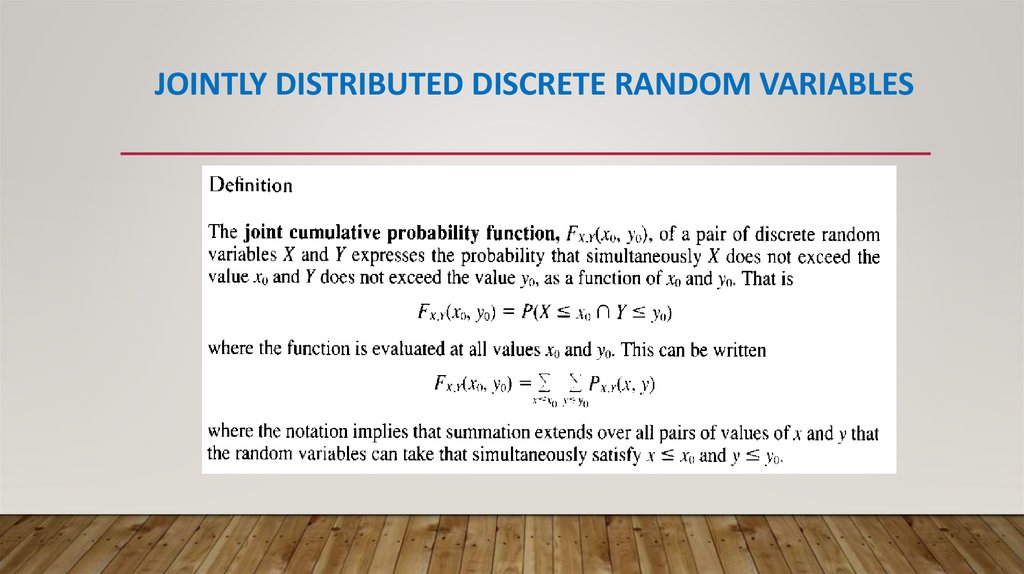

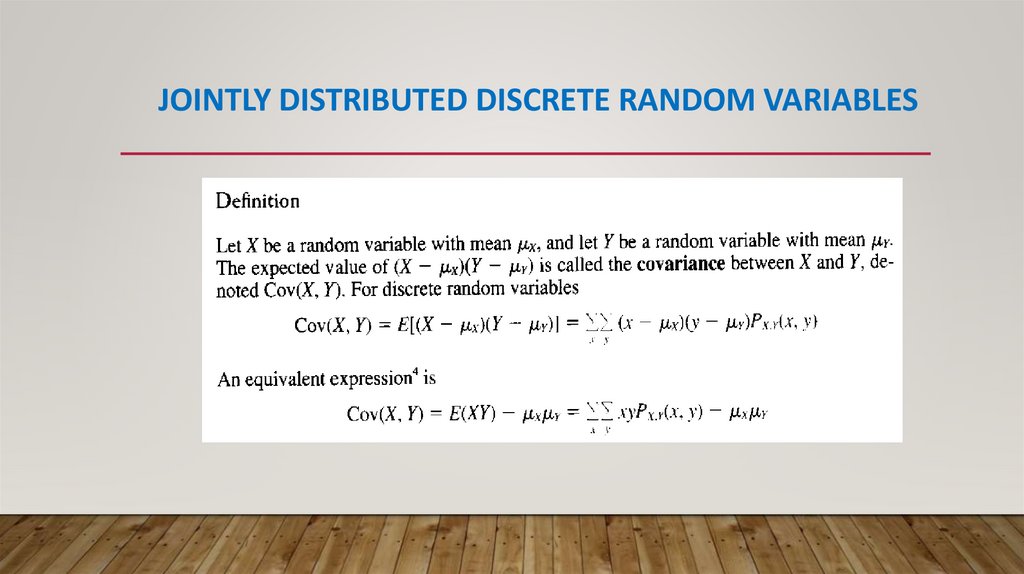

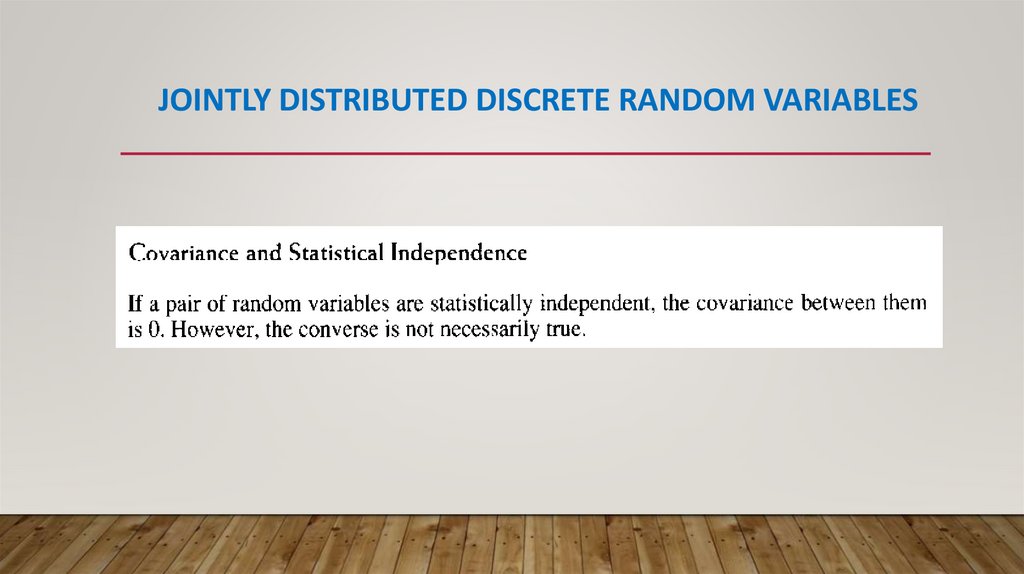

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES3.

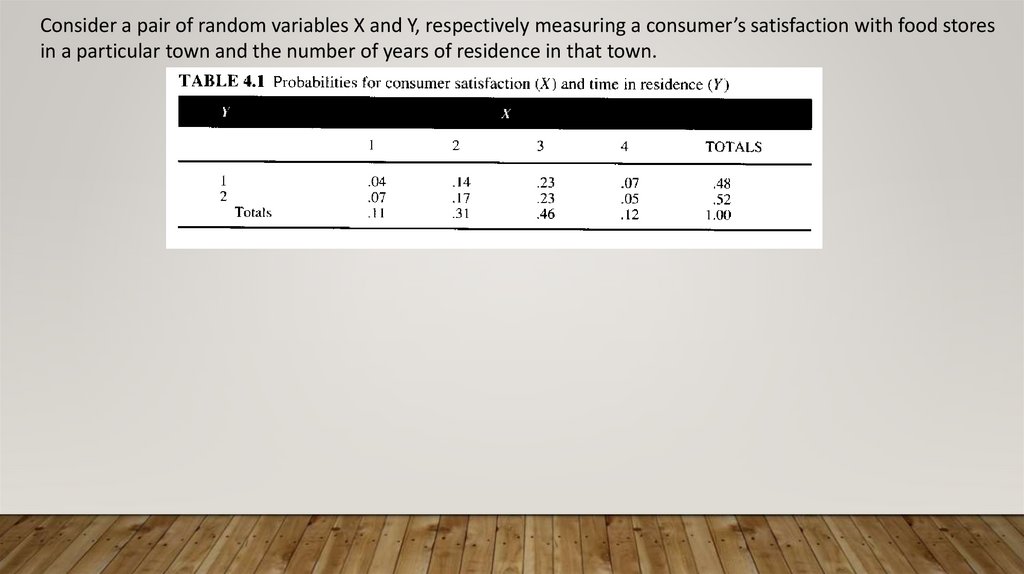

Consider a pair of random variables X and Y, respectively measuring a consumer’s satisfaction with food storesin a particular town and the number of years of residence in that town.

4.

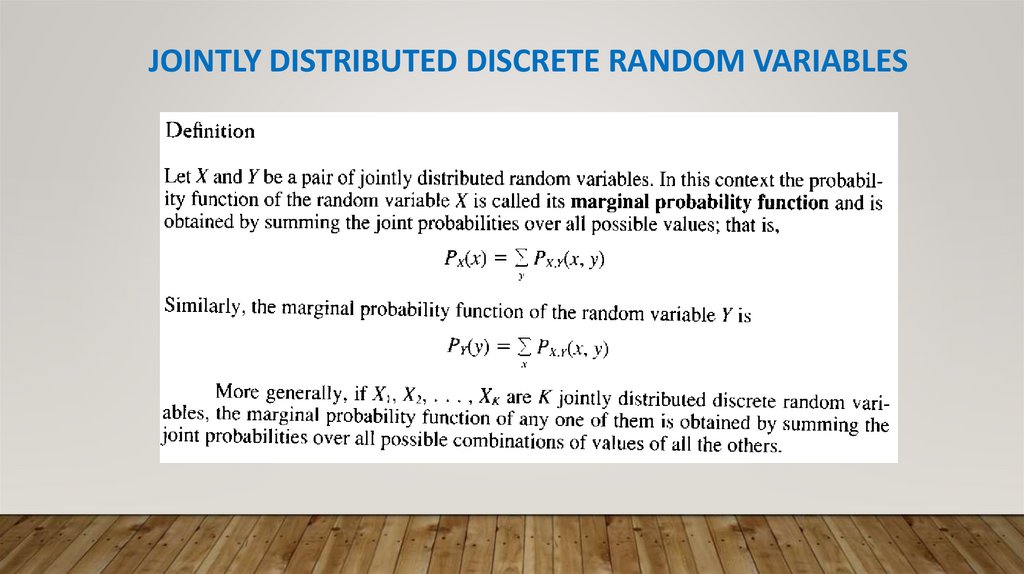

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES5.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES6.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES7.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES8.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES9.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES10.

JOINTLY DISTRIBUTED DISCRETE RANDOM VARIABLES11.

12.

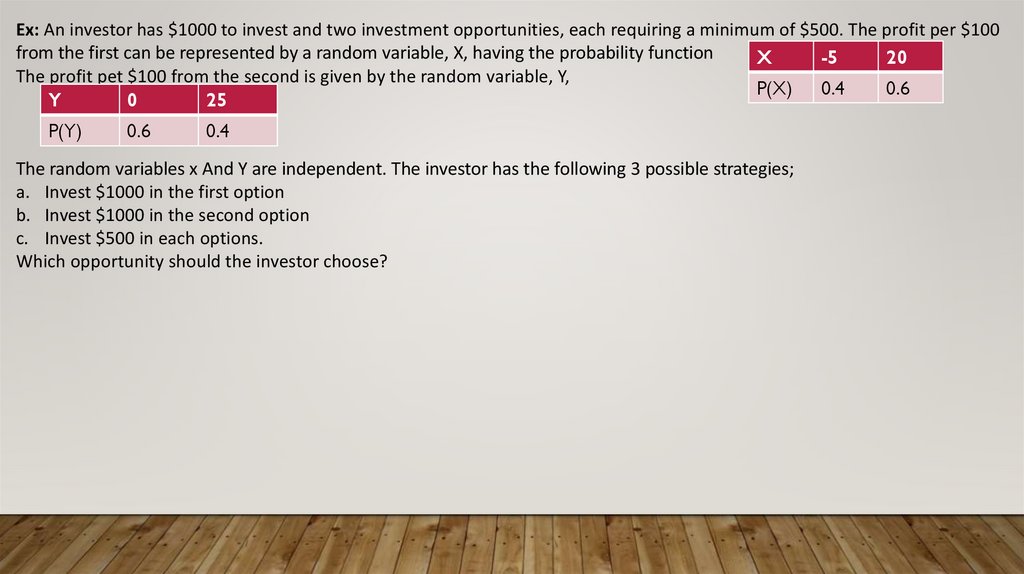

Ex: An investor has $1000 to invest and two investment opportunities, each requiring a minimum of $500. The profit per $100from the first can be represented by a random variable, X, having the probability function

X

-5

20

The profit pet $100 from the second is given by the random variable, Y,

P(X)

0.4

0.6

Y

0

25

P(Y)

0.6

0.4

The random variables x And Y are independent. The investor has the following 3 possible strategies;

a. Invest $1000 in the first option

b. Invest $1000 in the second option

c. Invest $500 in each options.

Which opportunity should the investor choose?