")

")

finance

financeSimilar presentations:

Financial Accounting 4ACCN008C-n Semester 1, 2024/2025

1. Financial Accounting 4ACCN008C-n Semester 1, 2024/2025

Revision2. Final exam

Section A – 60 marks:20 multiple choice questions(3 marks per 1 question)

Section B –40 marks:

2 open ended questions

All questions are compulsory

They cover all topics

Duration 2 hours 30 minutes

3. Final exam

The students are permitted to bring into the examination room:Non-Programmable Calculator

Black or blue pen

Ruler

All answers must be written in the answer book provided.

Black or Blue pen only must be used for written answers and for all

drawings and sketches.

The use of pencils or erasable pens is not permitted.

4.

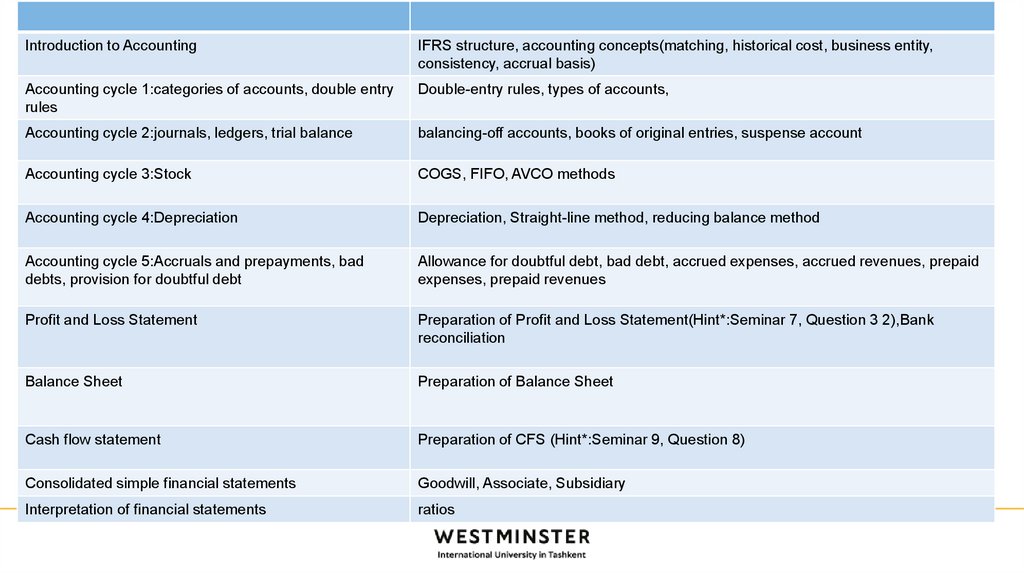

Introduction to AccountingIFRS structure, accounting concepts(matching, historical cost, business entity,

consistency, accrual basis)

Accounting cycle 1:categories of accounts, double entry

rules

Double-entry rules, types of accounts,

Accounting cycle 2:journals, ledgers, trial balance

balancing-off accounts, books of original entries, suspense account

Accounting cycle 3:Stock

COGS, FIFO, AVCO methods

Accounting cycle 4:Depreciation

Depreciation, Straight-line method, reducing balance method

Accounting cycle 5:Accruals and prepayments, bad

debts, provision for doubtful debt

Allowance for doubtful debt, bad debt, accrued expenses, accrued revenues, prepaid

expenses, prepaid revenues

Profit and Loss Statement

Preparation of Profit and Loss Statement(Hint*:Seminar 7, Question 3 2),Bank

reconciliation

Balance Sheet

Preparation of Balance Sheet

Cash flow statement

Preparation of CFS (Hint*:Seminar 9, Question 8)

Consolidated simple financial statements

Goodwill, Associate, Subsidiary

Interpretation of financial statements

ratios

5. The Scope of FA

Collect informationregarding financial

transactions

Stage 1

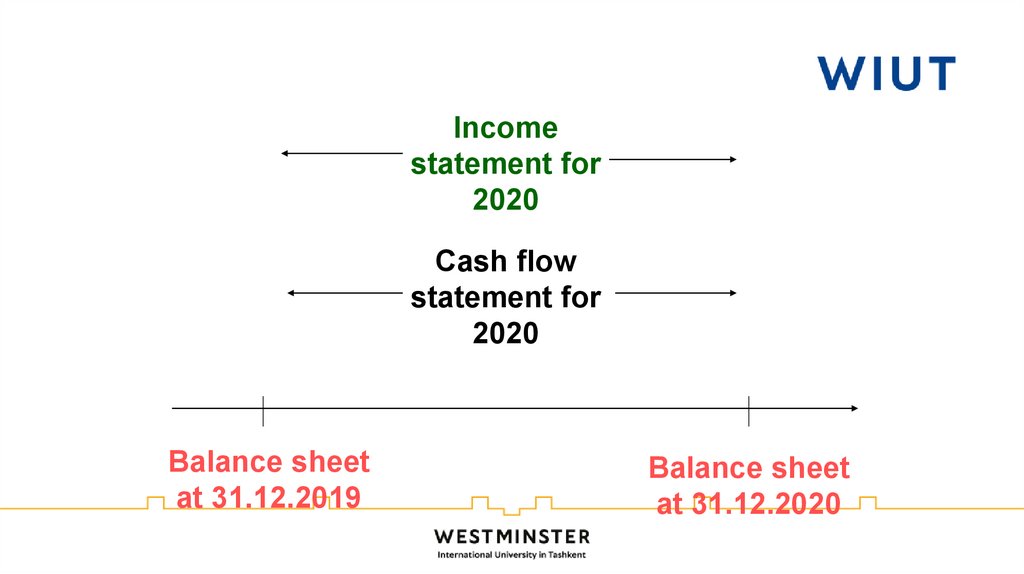

Express in monetary

terms

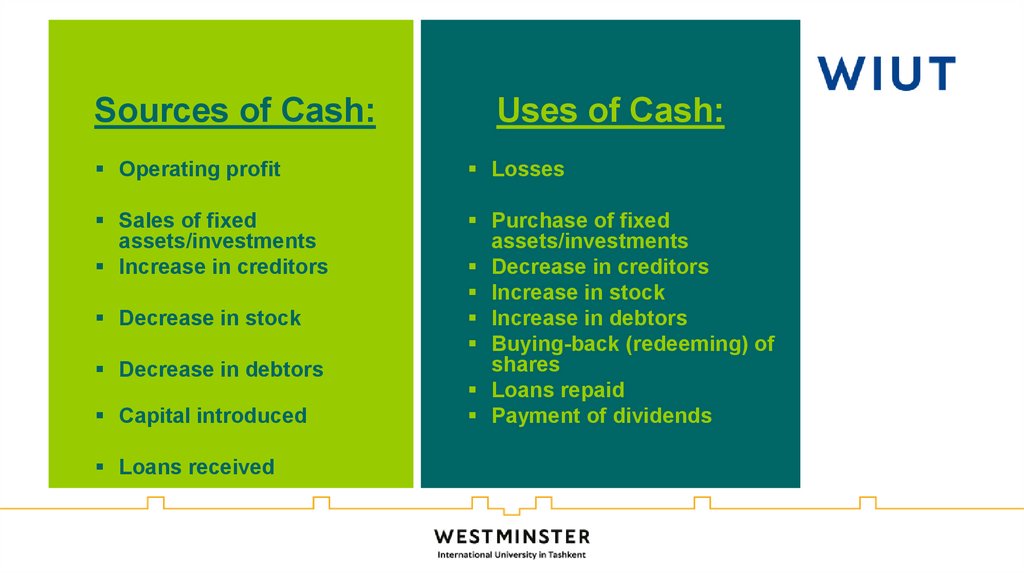

Record in accounting

journals

Summarize and present such

financial information in

financial statements

Stage 2

Balance

Sheet

Stage 3

Profit and

Loss Account

Cash flow

statement

Analyze and interpret

financial statements

6. 1.The body to which the International Accounting Standards Board is responsible is:

A IFRS Advisory CouncilB IFRS Interpretations Committee

C IFRS Foundation

D All of the above

6

7. Accounting standards

•The FA syllabus isconcerned

with

International

Financial

Reporting

Standards

(IFRSs).

•IFRSs are produced by

the

International

Accounting Standards

Board (IASB).

•The IASB operates under

the oversight of the IFRS

Foundation.

https://www.ifrs.org/

8. 2.Which accounting concept states that the expenses incurred during a period are recorded in the same period in which the

related revenues are earned?A The materiality concept

B The matching concept

C The duality concept

D The business entity concept

A

9. 3.A business sells $300 worth of goods to a customer; the customer pays $200 in cash immediately and will pay the remaining

$100 in 15 days' time.What is the double entry to record the purchase in the customer's accounting

records?

A Debit purchases $300, credit cash $300

B Debit purchases $300, credit payables $100, credit cash $200

C Debit payables $100, debit cash $200, credit purchases $300

D Debit cash $300, credit payables $100, credit purchases $200

10.

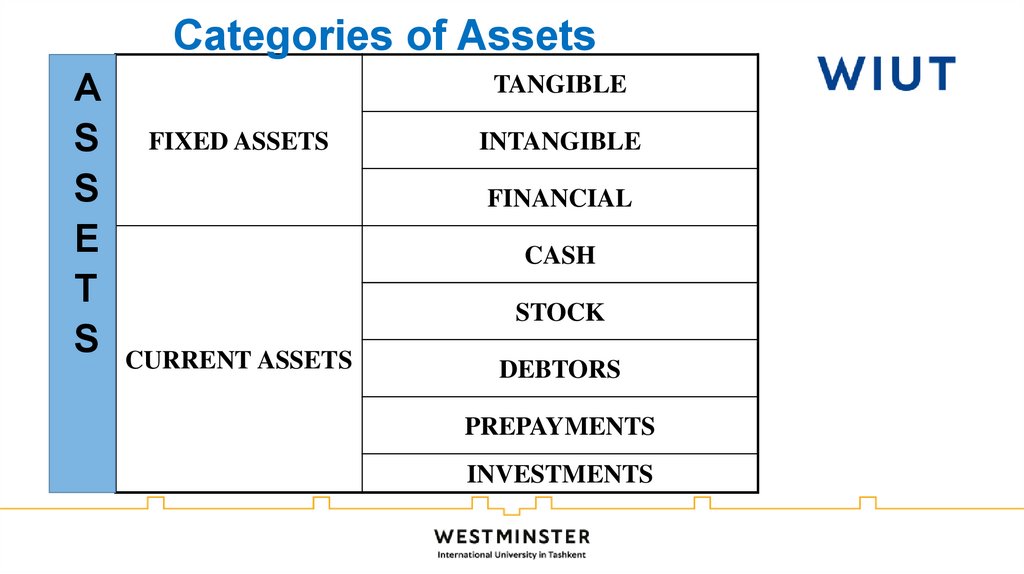

Categories of AssetsA

S FIXED ASSETS

S

E

T

S CURRENT ASSETS

TANGIBLE

INTANGIBLE

FINANCIAL

CASH

STOCK

DEBTORS

PREPAYMENTS

INVESTMENTS

11.

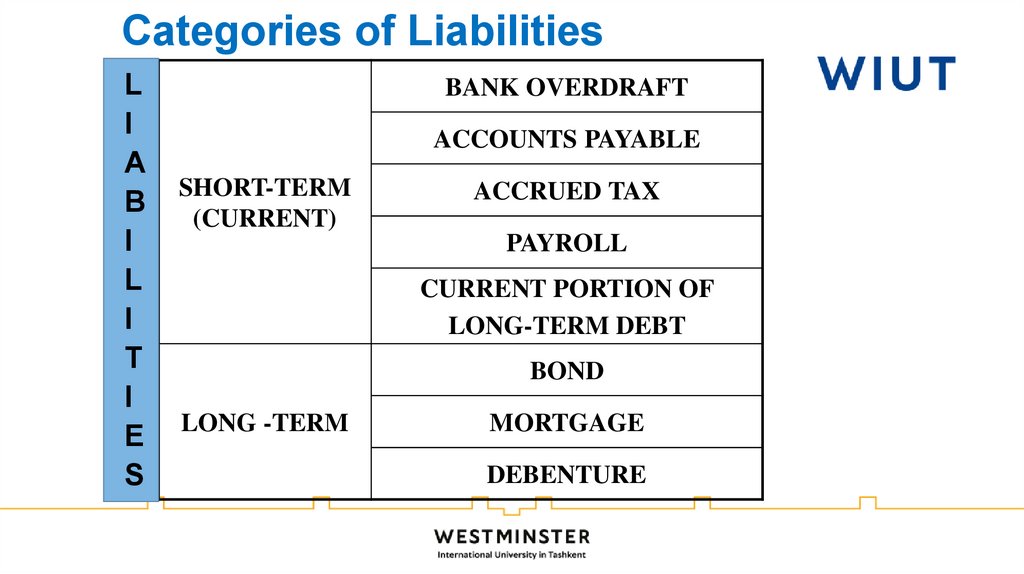

Categories of LiabilitiesL

I

A

B

I

L

I

T

I

E

S

BANK OVERDRAFT

ACCOUNTS PAYABLE

SHORT-TERM

(CURRENT)

ACCRUED TAX

PAYROLL

CURRENT PORTION OF

LONG-TERM DEBT

BOND

LONG -TERM

MORTGAGE

DEBENTURE

12.

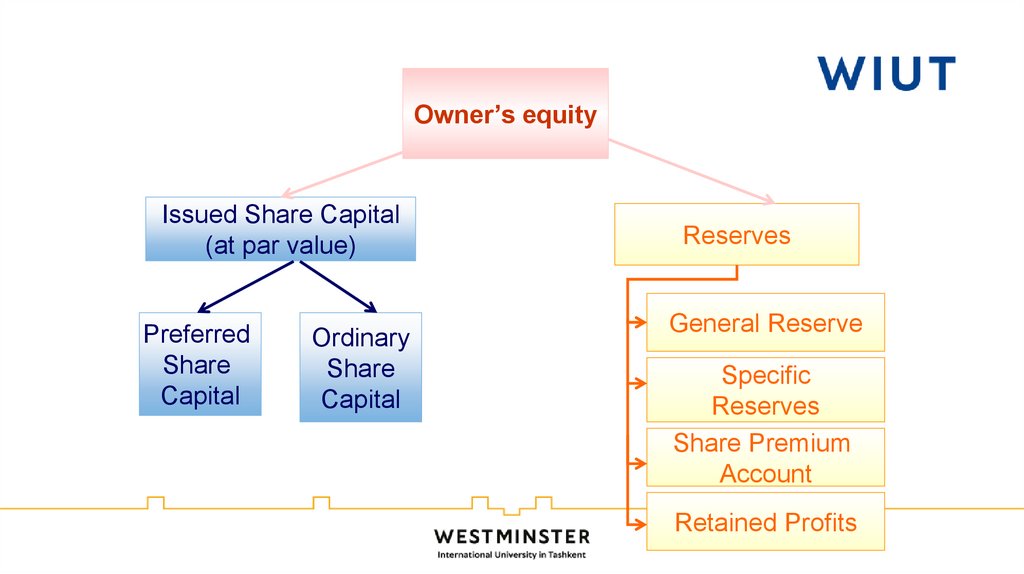

Owner’s equityIssued Share Capital

(at par value)

Preferred

Share

Capital

Ordinary

Share

Capital

Reserves

General Reserve

Specific

Reserves

Share Premium

Account

Retained Profits

13. Revenues

Turnover (sales)Profits on sale of fixed assets

Interest receivable

Investment income

Discounts received

Share of profit from associated companies

14. Expenses

Expenses are usually seen as being the costs incurred in earningthe revenues that are recognized during that period

Cost of Sales (COGS)

Depreciation

Losses from the sale of fixed assets

Discounts allowed

Increase in provision

15. Rules of Accounting

Rules of AccountingDEBIT

CREDIT

ASSETS

+

-

LIABILITIES

-

+

CAPITAL

-

+

REVENUES

-

+

EXPENSES

+

-

A+E =L+C+R

16. Rules of Debit and Credit

Capital (Owner’s equity)Liabilities

Assets

Debit

Credit

Debit

Credit

Debit

Credit

+

Increase

Left

Normal bal.

Decrease

Right

Decrease

Left

+

Increase

Right

Normal bal.

Decrease

Left

+

Increase

Right

Normal bal.

Revenues

Expenses

Debit

Credit

Debit

Credit

Decrease

Left

+

Increase

Right

Normal bal.

+

Increase

Left

Normal bal.

Decrease

Right

16

17. Example of Trial Balance

PP DESIGNTrial Balance

February 28, 2010

Name of Accounts

Debit

Bank

13,550

Cash

5,550

Equipment

8,000

Office Supplies

500

Artsy Co

3,000

Prompt Supplier

Credit

0

Capital

25,000

Sales

9,000

Discount received

50

Rent expenses

1,200

Salary expenses

2,000

Utilities expenses

250

Total

34,050

34,050

18. 4.Where a transaction is entered into the correct ledger accounts, but the wrong amount is used, what is the error known as?

A An error of omissionB An error of original entry

C An error of commission

D An error of principle

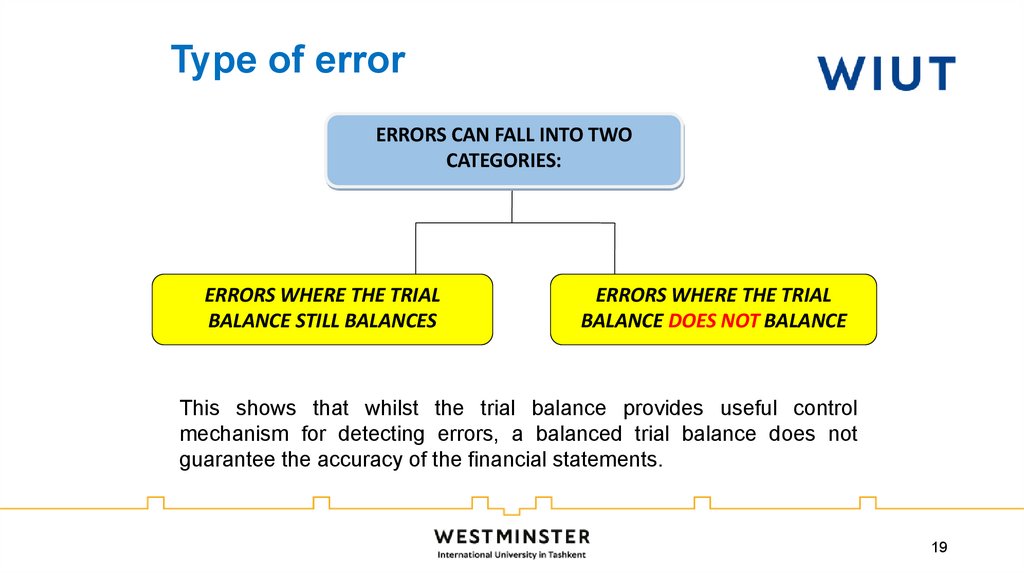

19.

Type of errorERRORS CAN FALL INTO TWO

CATEGORIES:

ERRORS WHERE THE TRIAL

BALANCE STILL BALANCES

ERRORS WHERE THE TRIAL

BALANCE DOES NOT BALANCE

This shows that whilst the trial balance provides useful control

mechanism for detecting errors, a balanced trial balance does not

guarantee the accuracy of the financial statements.

19

20.

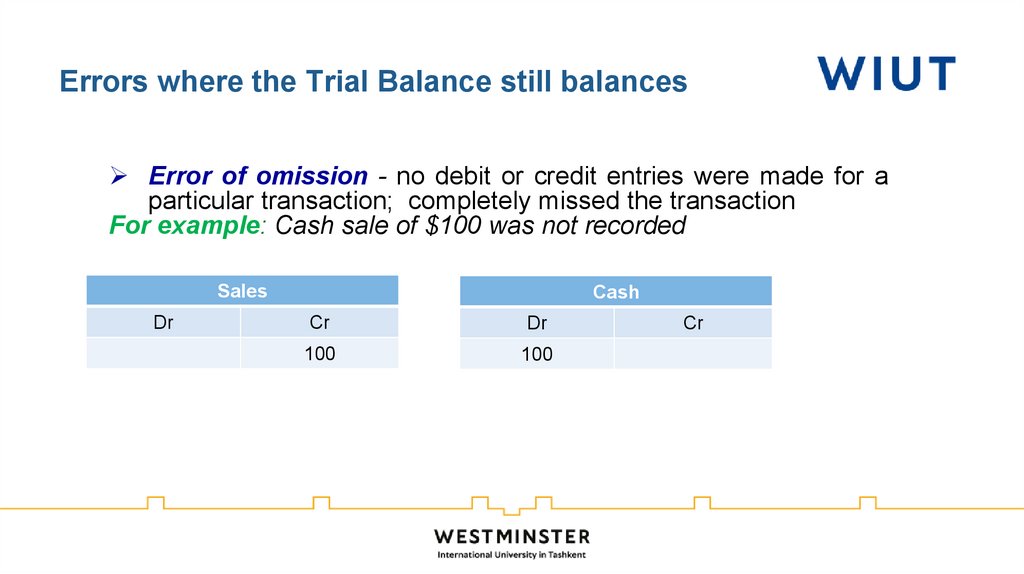

Errors where the Trial Balance still balancesError of omission - no debit or credit entries were made for a

particular transaction; completely missed the transaction

For example: Cash sale of $100 was not recorded

Sales

Dr

Cash

Cr

Dr

100

100

Cr

21.

Errors where the Trial Balance still balancesComplete reversal of entries – entries were made in the wrong side of

the accounts; a transaction requires a debit entry in account A and a

credit entry in account B but account A was credited and account B was

debited instead

For example: cash sale of $200 has been debited to sales and credited to

bank.

Cash

Sales

Dr

Cr

Dr

Cr

200

400

400

200

Bal.c/f 200

Bal. c/f 200

400

400

400

Bal. b/f 200

Bal. b/f 200

400

22.

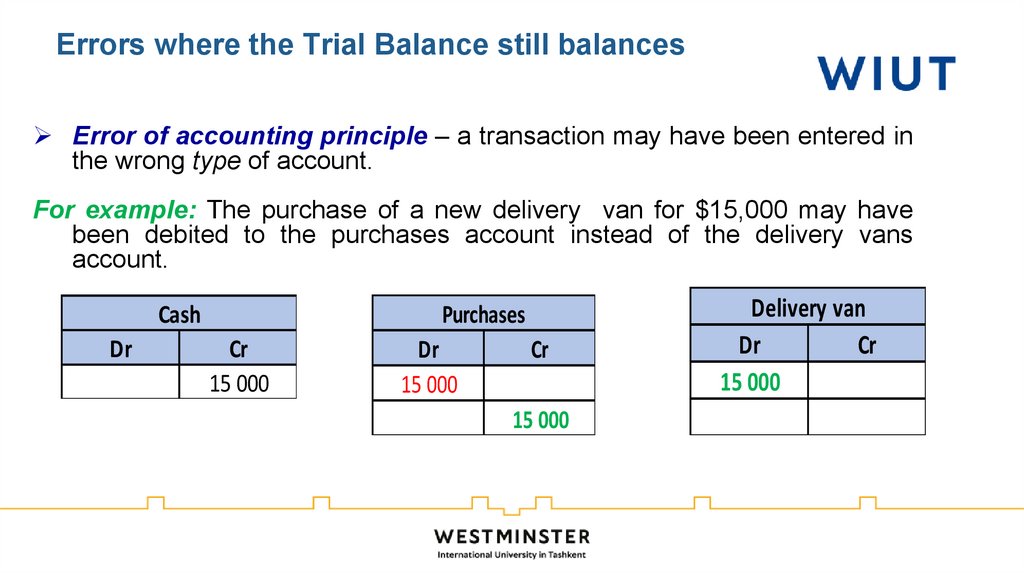

Errors where the Trial Balance still balancesError of accounting principle – a transaction may have been entered in

the wrong type of account.

For example: The purchase of a new delivery van for $15,000 may have

been debited to the purchases account instead of the delivery vans

account.

Purchases

Cash

Dr

Cr

15 000

Dr

15 000

Cr

15 000

Delivery van

Dr

Cr

15 000

23.

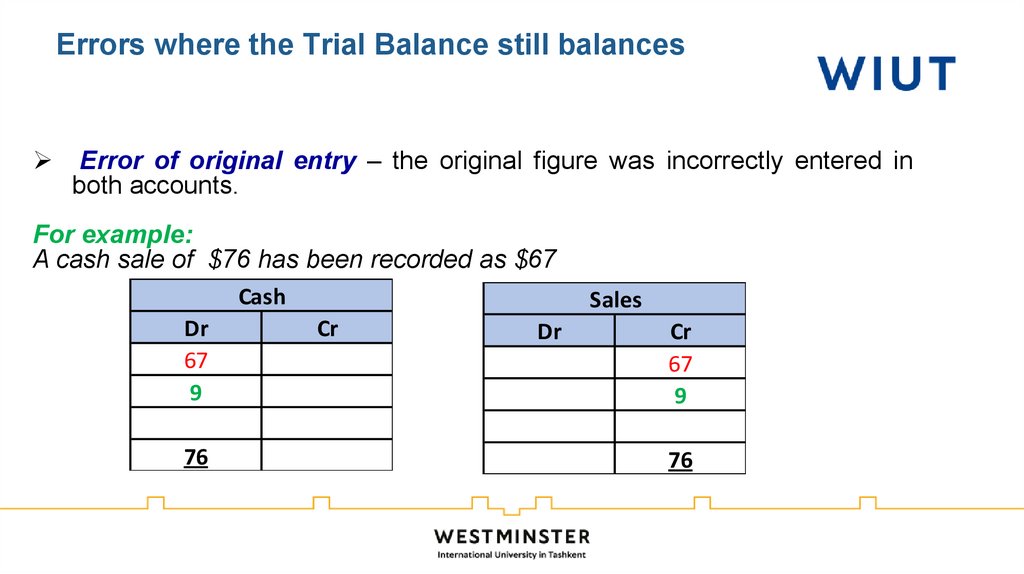

Errors where the Trial Balance still balancesError of original entry – the original figure was incorrectly entered in

both accounts.

For example:

A cash sale of $76 has been recorded as $67

Cash

Dr

67

9

76

Sales

Cr

Dr

Cr

67

9

76

24. Errors where the Trial Balance still balances

Error of commission – entries were made on the correctsides of the accounts but to the wrong personal account.

For example: credit sales for $10,000 to C Green were

incorrectly recorded in the accounts of K Green.

Sales

Dr

K Green

Cr

10 000

Dr

10 000

Cr

10 000

C Green

Dr

10 000

Cr

24

25. 5.What journals are required to correct the error and eliminate the suspense account?

A credit balance of $81 in the rent income account had been incorrectlyextracted on the list of balances as a debit balance.

* They have posted Dr rent income 81, Dr bank 81, Cr suspense a/c 162

25

26. Suspense accounts

A suspense account is an account in which debits or credits are held temporarily untilsufficient information is available for them to be posted to the correct accounts.

There are two main reasons why suspense accounts may be created.

1. On the extraction of trial balance the debits are not equal to the credits and the difference

is put to the suspense account.

2. When a bookkeeper performing double entry is not sure where to post one side of an entry

they may debit or credit a suspense account and leave the entry there until its ultimate

destination is clarified.

For example: A cash payment might be made and must obviously be credited to cash. But the

bookkeeper may not know what the payment is for, and so will not know which account to

debit.

The balance on the suspense account must be cleared before final accounts can be prepared

27. 6.What should be the correct balance per the cash book?

The following bank reconciliation statement has been prepared by a traineeaccountant:

$

Overdraft per bank statement

5,340

Less: Unpresented cheques

10,550

5,210

Add: Outstanding lodgements

25,600

Cash at bank

30,810

A $20,390 balance at bank

B $30,810 balance at bank as stated

C $9,710 balance at bank

D $9,710 overdrawn

28. Bank reconciliations

In theory, the entries appearing on a business's bank statement should beexactly the same as those in the business cash book. The balance shown by

the bank statement should be the same as the cash book balance on the

same date.

Our Company

Bank

( Business)

(e.g.OFB,Kapitalbank, etc.)

Cash Book

Bank statement

A bank reconciliation is a comparison of a bank statement (sent monthly,

weekly or even daily by the bank) with the cash book. Differences between

the balance on the bank statement and the balance in the cash book will be

errors or timing differences, and they should be identified and satisfactorily

explained.

28

29. Why might your own estimate of your bank balance be different from the amount shown on your bank statement?

There are three common explanations:Error. Errors in calculation, or recording income and payments, are more likely to have been

made by you than by the bank, but it is conceivable that the bank has made a mistake too.

Bank charges or bank interest. The bank might deduct charges for interest on an overdraft

or for its services, which you are not informed about until you receive the bank statement.

Timing differences These items have been recorded in the cash book , but due to the bank

clearing process have not yet been recorded in the bank statement

Outstanding/ unpresented cheques- cheques sent to suppliers but not yet cleared by the bank.

Outstanding/uncleared lodgements- cheques received by the business but not yet cleared by

the bank

29

30. 7.What is the value of the company's closing inventory of TV sets on 31 December 2020?

7.What is the value of the company's closing inventory of TV sets on31 December 2020?

A company values its inventory using the FIFO method. On 1 January 2020

the company had 550 TV sets in inventory, valued at $350 each. During the

year ended 31 December 2020 the following transactions took place:

1 March

Purchased 300 TV sets at $370 each

1 June

Sold 570 TV sets for $228,000

1 August

Purchased 480 TV sets at $400 each

15 December

Sold 115 TV sets for $48,300

A $227,650

B $253,050

C $242,450

D $267,850

31. Cost of goods sold (COGS)

COGS is the cost of acquiring ormanufacturing the products that a

company sells during a period, so

the only costs included in the

measure are those that are directly

tied to the production of the

products, including the cost of labor,

materials, and manufacturing

overhead.

32. Cost of Goods Sold (COGS)

COGS == Opening Stock

Add Purchases

Less Return Outwards (purchase returns)

Add Carriage Inwards

Cost of the goods available for sale

Less Closing Stock

33. Valuation of stock - FIFO

• InFIFO(first-in-first-out),

the

assumption is made for costing

purposes that the first items of

inventory received are the first

items to be sold.

• Thus every time a sale is made,

the COGS is identified as

representing the cost of the oldest

goods remaining in inventory.

34. Valuation: Average cost

• Under the weighted average cost formula, the cost of each item isdetermined from the weighted average of the cost similar items at the

beginning of the period and the cost of similar items purchased or produced

during the period.

Average cost per unit = Total

cost of inventory / No. of units

in inventory

35. 8.The amount of accumulated depreciation on December 31, 2020, if the straight-line method of depreciation is used is:

Saga Innovations Company purchased agricultural equipment on January 1, 2017, for$500,000. The equipment has an estimated residual value of $50,000 and an estimated

useful life of 10 years.

A $180,000

B $45,000

C $90,000

D $200,000

35

36. Calculating Depreciation

(i) straight-line method - the depreciation charge is constant over the life ofthe asset.

Historical Cost Residual Value

Useful Economic Life

*The residual value, also known as

salvage value, is the estimated value of a fixed

asset at the end of its useful life.

37.

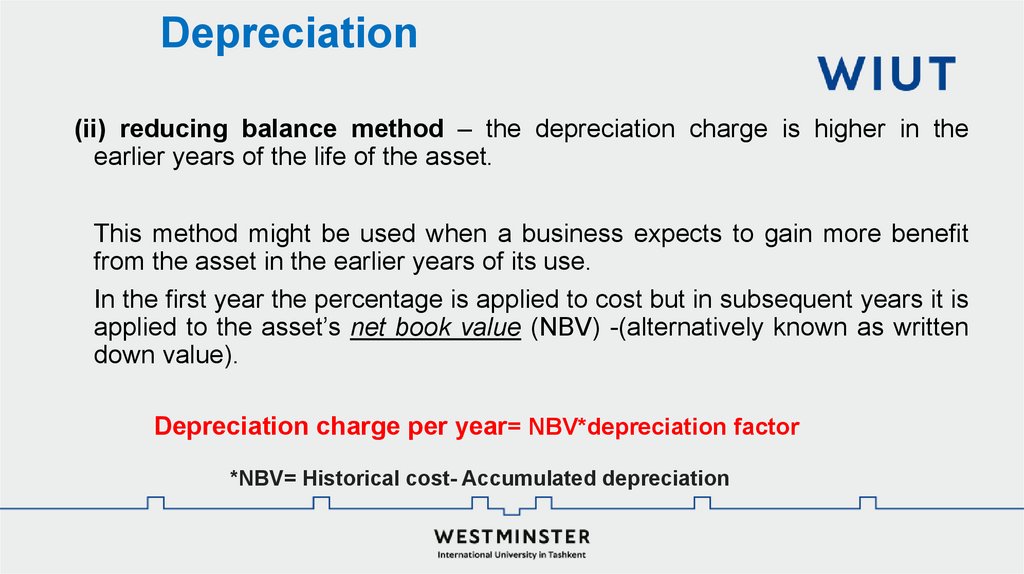

Depreciation(ii) reducing balance method – the depreciation charge is higher in the

earlier years of the life of the asset.

This method might be used when a business expects to gain more benefit

from the asset in the earlier years of its use.

In the first year the percentage is applied to cost but in subsequent years it is

applied to the asset’s net book value (NBV) -(alternatively known as written

down value).

Depreciation charge per year= NBV*depreciation factor

*NBV= Historical cost- Accumulated depreciation

38. 9.What figure should appear in the statement of profit or loss for the year ended 31 December 2020 for these items?

On 31 December 2019 a company's allowance for receivables was $15,000.On 31 December 2020 trade receivables totaled $653,000. It was decided to

write off debts totaling $43,000. The receivables allowance was to be

adjusted to an amount equivalent to 7% of the trade receivables based on

past events.

A $45,710

B $27,700

C $70,700

D $88,710

39. Bad & doubtful debts

Bad & doubtful debts• Bad debt – highly unlikely it will be paid/recovered; long-time owing and

proven to be bad.

• Doubtful debts – are the debt that are likely to be bad but have not yet

been proven to be so.

40. Bad & doubtful debts

Bad & doubtful debtsWriting off a bad debt completely removes the debt from the accounting

books

And the double entry will be:

Dr Bad debt (it is an expense account)

Cr Debtors (reduce the debtor figure by the amount of the bad debt)

The balance of Bad Debts account is then transferred to Profit and Loss

account at the end of accounting period.

41. Bad & doubtful debts

Bad & doubtful debtsOn 5 January, we sold $200 and $50 of pens to Chumi and Chiki

respectively. However, at the year end, Chumi only managed to pay $120

and Chiki business already went bankrupt.

Debtor Chumi

Sales

Dr

Cr

05-Jan

05-Jan

Cr

200

31-Dec

31-Dec

120

80

Bad debt

Cash

Dr

31-Dec 120

200

50

Dr

05-Jan

Debtor Chiki

Cr

Dr

31-Dec

31-Dec

Cr

50

80

Dr

05-Jan

50

Cr

31-Dec

50

42. Bad & doubtful debts

Bad & doubtful debtsWriting off a bad debt completely removes the debt from the accounting books

And the double entry will be:

Dr Bad debts (it is an expense account)

Cr Debtors (reduce the debtor figure by the amount of the bad debt)

The balance of Bad Debts account is then transferred to Profit and Loss

account at the end of accounting period.

Balance Sheet

Dr

Fixed assets

xxx

Current Assets

Debtors

Cr

250

130

PROFIT & LOSS ACCOUNT

Revenue:

Expenses:

Bad debts

130

xxx

43. Provision for doubtful debts

Why do we need provision?How do you decide how much to provide?

The estimated figure can be made:

i) By looking at each debt, and deciding to what extent it will be bad;

ii) By estimating, on the basis of experience, what percentages(%) of the total amount due

from the remaining debtors will ultimately prove to be bad debts.

Ageing Schedule for Doubtful Debts

Period debt owing

Amount ($)

Estimated % doubtful

Provision for doubtful

debts ($)

Less than 1 mth

5,000

1

50

1 – 2 months

3,000

3

90

2 – 3 months

800

4

32

3 months – 1 year

200

5

10

Over 1 year

160

20

32

9,160

214

44. Provision for doubtful debts

SalesDr

Cr

9160

Accounts receivable

Dr

Cr

9160

Represented in balance sheet as:

Current assets:

Bad and doubtful debt expenses

Dr

Cr

214

Provision for doubtful debt

Dr

Cr

214

Accounts receivable

Provision for doubtful debt

Net accounts receivable

Dr

$ 9,160

Cr

$ 214

$8,946

45.

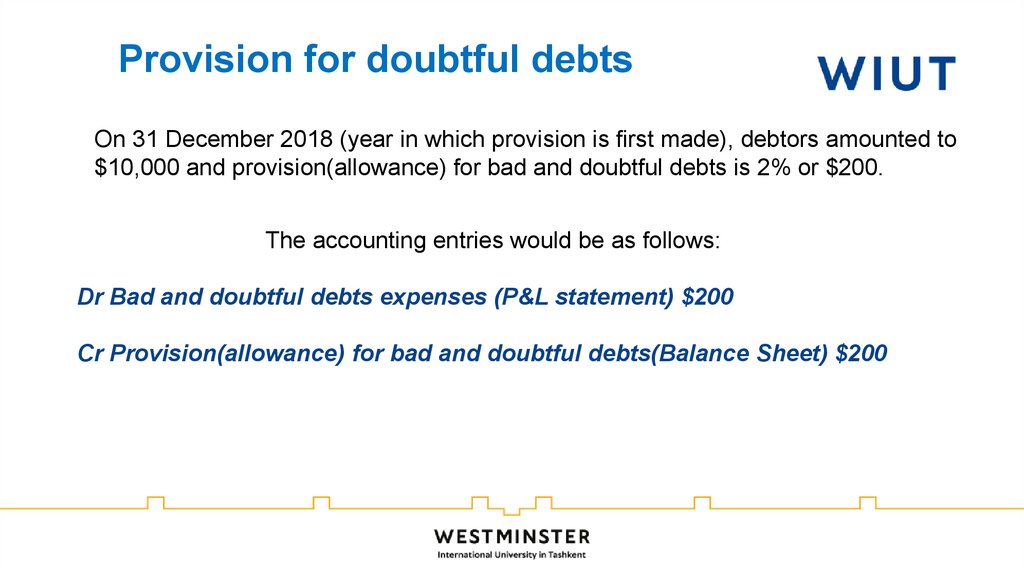

Provision for doubtful debtsOn 31 December 2018 (year in which provision is first made), debtors amounted to

$10,000 and provision(allowance) for bad and doubtful debts is 2% or $200.

The accounting entries would be as follows:

Dr Bad and doubtful debts expenses (P&L statement) $200

Cr Provision(allowance) for bad and doubtful debts(Balance Sheet) $200

46. Provision for d. debts

Increasing the provision: suppose that at the end of the following year, 31December 2019, debtors had risen to $12,000 but the provision is still kept at

2%, or $240. Since a provision of $200 had been brought forward from 2018, in

2019 a provision for the additional $40 only should be made.

The accounting entries on 31 December 2019 would be as follows:

Dr Change(Increase) in Provision for doubtful debt (P and L

Statement) $40

Cr Provision for bad and doubtful debts(Balance Sheet) $40

47. Provision for d. debts

Reducing the provision: suppose that at the end of the following year, 31December 2020, debtors fell to $10,500 but the provision remained at 2%, or $210.

Since a provision of $240 had been brought forward from 2019, the provision in

2020 needs to be reduced by $30 .

The accounting entries on 31 December 2020 would be as follows:

Dr Provision for bad and doubtful debts (Balance Sheet) $30

Cr Change(Decrease) in Provision for doubtful debt (P and L Statement) $30

48. Profit & Loss Account

Profit & Loss AccountTrading account section – to calculate the gross profit

(excess of sales over the cost of goods sold).

Sales

Less: Returns Inwards (Sales Returns)

(Net sales)

X

Add: Opening stock

Add: Purchases

Less: Returns outwards (purchases returns)

Add: Carriage inwards

Less: Closing stock

Add: Wages (warehouse and workshop)

Cost of sales/Cost of goods sold

GROSS PROFIT

X

49. Profit & Loss Account

Profit & Loss AccountHelps to calculate the net profit (excess of gross profit and other revenues over all other

expenses)

Wages and salaries

Advertising and sales promotion

Depreciation

Bad debts

Provision for bad and doubtful debts (increase/decrease)

Discounts allowed

Directors’ remuneration

OPERATING PROFIT

Dividends receivable..

Income from other fixed assets investments **

PROFIT BEFORE INTEREST AND TAX (PBIT/ EBIT)

Debenture Interest payable

Loan interest payable

PROFIT BEFORE TAX (PBT)

Taxation …

PROFIT AFTER TAX (PAT)

50.

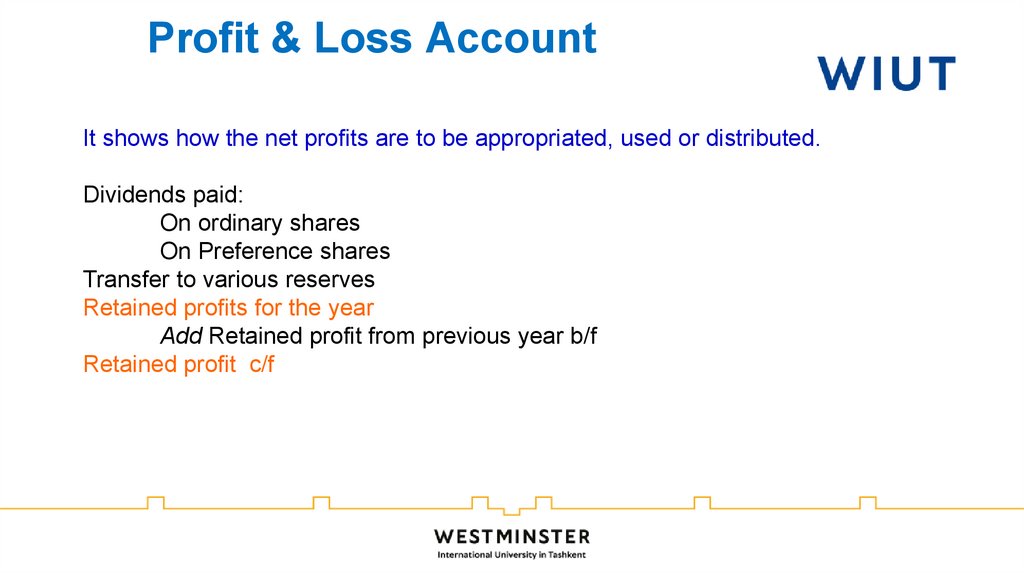

Profit & Loss AccountIt shows how the net profits are to be appropriated, used or distributed.

Dividends paid:

On ordinary shares

On Preference shares

Transfer to various reserves

Retained profits for the year

Add Retained profit from previous year b/f

Retained profit c/f

51. 10.Which of the following corrections need to be made to the calculation?

10.Which of the following corrections need tobe made to the calculation?

A draft statement of cash flows contains the following calculation of cash flows from operating activities:

$000

Profit before tax

12,358

Depreciation

335

Increase in inventories

528

Increase in trade and other receivables

445

Decrease in trade payables

(388)

Net cash inflow from operating activities

13,278

1Depreciation should be deducted, not added

2 Increase in inventories should be deducted, not added

3 Increase in receivables should be deducted, not added

4 Decrease in payables should be added, not deducted

A 2 and 4

B 1 and 3

C 2 and 3

D 1 and 4

52. Cash Flow Statement

Financial statement provides a reconciliation between the amount of profitgenerated during a period, and the amount by which cash balances have

increased or decreased during that period

53.

Incomestatement for

2020

Cash flow

statement for

2020

Balance sheet

at 31.12.2019

Balance sheet

at 31.12.2020

54.

Sources of Cash:Uses of Cash:

Operating profit

Losses

Sales of fixed

assets/investments

Increase in creditors

Purchase of fixed

assets/investments

Decrease in creditors

Increase in stock

Increase in debtors

Buying-back (redeeming) of

shares

Loans repaid

Payment of dividends

Decrease in stock

Decrease in debtors

Capital introduced

Loans received

55. Cash Flow Statement

56. Reconciliation of Operating Profit

Operating ProfitDepreciation charges

Loss/(profit) on sale of tangible fixed assets

(Increase)/decrease in stock

(Increase)/decrease in debtors

Increase/(decrease) in creditors

Increase/(decrease) in provision for bad and doubtful debt

1. Net cash inflow/outflow from operating activities

57. 11.Which of the following companies are subsidiaries of Pineapple Co?

Orange Co: Pineapple Co owns 83% of the non-voting preference shares of OrangeMelon Co: Pineapple Co owns 67% of the ordinary share capital of Melon Co;

however Melon Co is located overseas and is subject to tax in that country.

Banana Co: Pineapple Co has four representatives on the board of directors of

Banana Co. Each director can cast 11 votes each out of the total of 50 votes at

board meetings.

A Melon Co, Banana Co

B Orange Co, Melon Co, Banana Co

C Orange Co, Banana Co

D Orange Co, Melon Co

58. Group and Consolidation

Consolidation means presenting the results, assets and liabilities of a group of companiesas if they were one company.

You will probably know that many large companies actually consist of several companies

controlled by one central or administrative company. Together, these companies are called a

group

59. How does a group arise?

The central company, called a parent, generally owns most (>50%) or all ofthe shares in the other companies, which are called subsidiaries (A

subsidiary is an entity controlled by another entity).

The parent company usually controls the subsidiary by owning most of the

shares in that company, but share ownership is not always the same as

control, which can arise in other ways.

Example: Pizza Hut, Taco Bell & KFC –subsidiaries, Yum! Brand Inc. – parent

company of these subsidiaries

60.

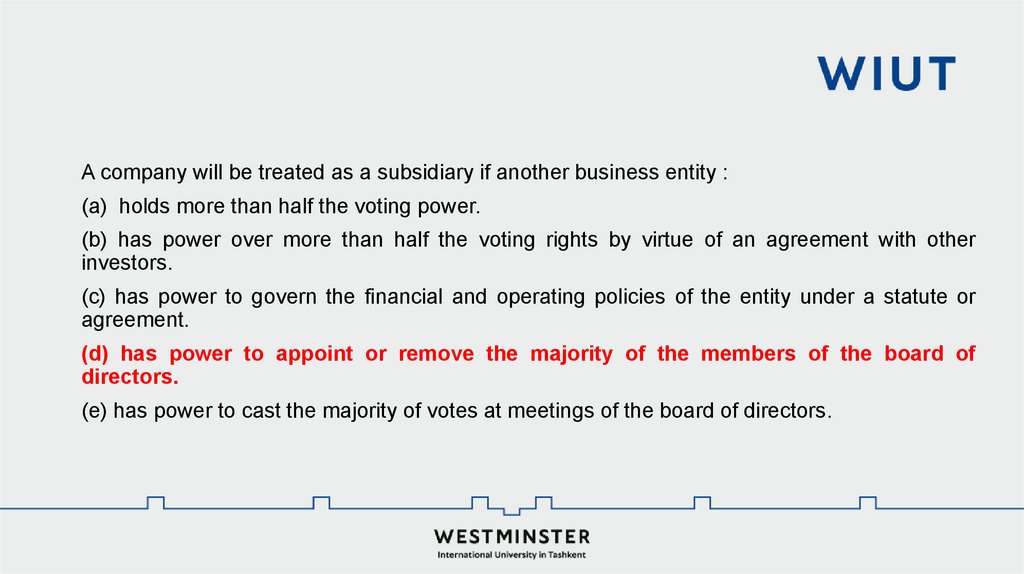

A company will be treated as a subsidiary if another business entity :(a) holds more than half the voting power.

(b) has power over more than half the voting rights by virtue of an agreement with other

investors.

(c) has power to govern the financial and operating policies of the entity under a statute or

agreement.

(d) has power to appoint or remove the majority of the members of the board of

directors.

(e) has power to cast the majority of votes at meetings of the board of directors.

61. Associates

An associate is an entity over which another entity exerts significant influence. Associatesare accounted for in the consolidated statements of a group using the equity method.

The key criterion here is significant influence. This is the 'power to participate in the financial

and operating policy decisions of the investee but which is not control or joint control of those

policies.‘ (IAS 28)

62. Existence of significant influence

Representation on the board of directors (or equivalent) of the investeeParticipation in the policy making process

Material transactions between investor and investee

Interchange of management personnel

Provision of essential technical information

63. 12.What is goodwill in the consolidated statement of financial position?

On 1 January 2020 Hitech Co acquired 5,500,000 of the 8,000,000 $2 ordinaryshares of Pencil Co, paying $ 14,000,000 cash. On that date the fair value of Pencil

Co net assets was $12,450,000. The market price of the shares held by the noncontrolling shareholders just before the acquisition was $3.

A $5,950,000

B $1,550,000

C $9,050,000

D $11,000,000

64. Goodwill & NCIs

Goodwill & NCIsGoodwill

$

Fair value of consideration transferred

$

X

Plus fair value of NCI at acquisition

X

Less net acquisition-date fair value of identifiable assets acquired and

liabilities assumed:

Ordinary share capital

X

Share premium

X

Retained earnings at acquisition

X

Fair value adjustments at acquisition X

(X)

Goodwill

X

65.

Good preparation is main prerequisite for good markin exam