finance

financeSimilar presentations:

Methodology of accounting

1.

Accounting2.

Accounting in statementsA. Lincoln

Damn lucky for someone

who has never studied

accounting. Then he

would have immediately

realized that he was

ruined. And so, it seems

that everything is going

fine

2

3.

Accounting in statementsStanislav

Jerzy Lez

A good accountant is

expensive, and a bad

one is much more

expensive

3

4.

DefinitionAccounting is the formation of documented

systematized information about objects

provided for by law, in accordance with the

requirements established by law, and the

preparation of accounting (financial)

statements based on it

5.

Types of accounting1.

Financial accounting - focused on external

users of information (this is traditional

accounting);

2.

Tax accounting – accounting that is

conducted in accordance with the rules

established by the tax authorities;

3.

Management accounting - focused on

internal users of information

6.

Maintaining accounting recordsAll organizations are required to maintain

accounting records.

Some organizations (small businesses) may use

simplified methods of accounting.

For tax purposes, organizations keep tax records

in accordance with the selected tax rules

7.

Regulation of accountingAccounting is regulated by special documents standards.

The accounting standard is a document that

establishes the minimum necessary requirements

for accounting, as well as acceptable methods of

accounting for any object

8.

Regulation of accounting1)

federal accounting standards;

2)

branches of industry accounting standards;

3)

regulatory acts of the Central Bank;

4)

recommendations in the field of accounting;

5)

standards of the organization.

9.

Regulation of accountingIn addition to national accounting standards, there

are also international financial reporting standards

– IAS (IFRS)

10.

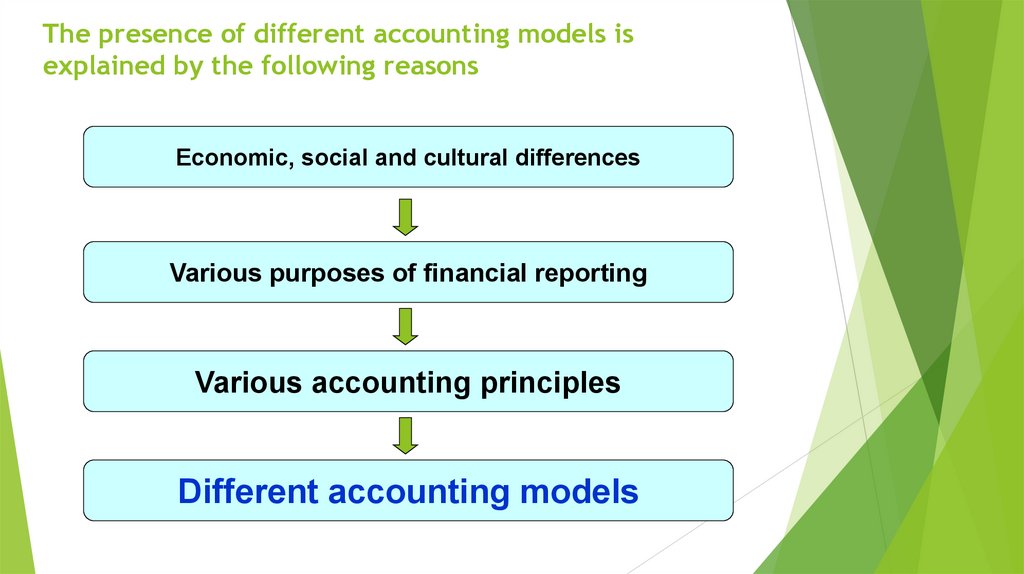

The presence of different accounting models isexplained by the following reasons

Economic, social and cultural differences

Various purposes of financial reporting

Various accounting principles

Different accounting models

10

11.

British-American model1.

Accounting statements are the main source of

information for investors, shareholders and only

then other creditors (banks). Weak influence of

the state on the reporting procedure.

2.

Great attention is paid to the audit of financial

statements

3.

One of the basic principles is True and fair value.

12.

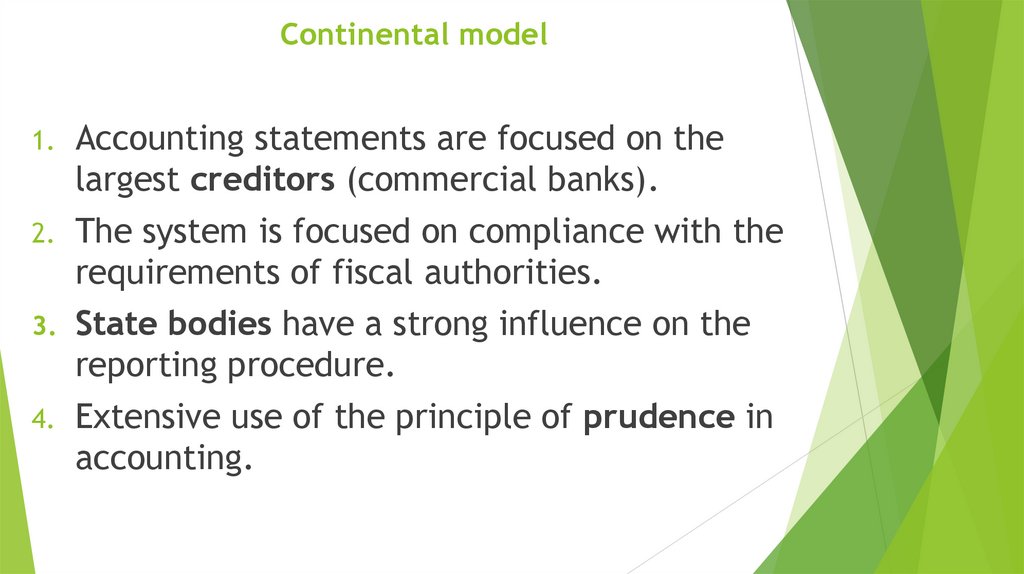

Continental model1.

Accounting statements are focused on the

largest creditors (commercial banks).

2.

The system is focused on compliance with the

requirements of fiscal authorities.

3.

State bodies have a strong influence on the

reporting procedure.

4.

Extensive use of the principle of prudence in

accounting.

13.

Other modelsSome authors, in addition to these two

models, distinguish other accounting models:

the South-American model;

the Islamic model;

the Japanese model;

the African model;

the Russian model.

14.

Lack of unity within the country.For example, in Germany,

IAS is used by:

-

Adidas, Bayer, Deutsche Bank, Dresdner

Bank, Henkel, Lufthansa, MAN, Wella,

Merck.

US GAAP is used by:

-

Daimler, Schwarzkopf, Puma

They give preference to national standards:

- BASF, Deutsche Telekom.

15.

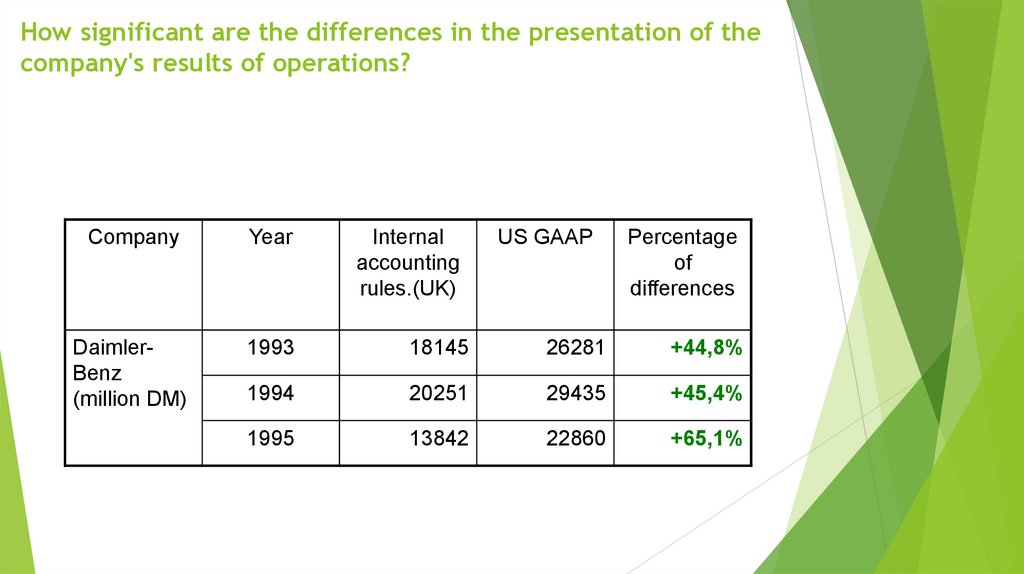

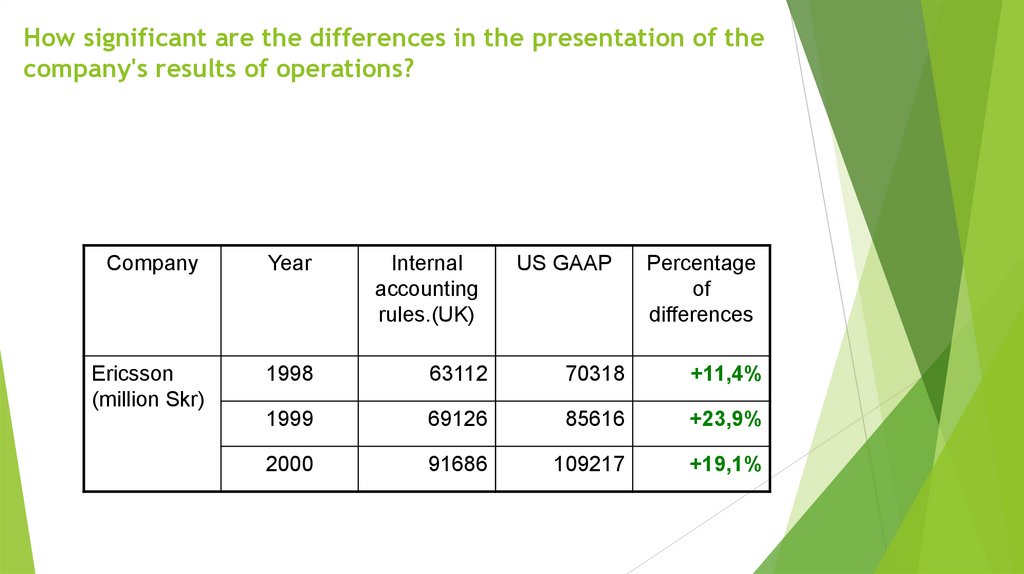

How significant are the differences in the presentation of thecompany's results of operations?

The table shows the results of the recalculation of

equity capital when some companies switch to

accounting standards adopted in other countries.

Company

British

Airways

(million ₤)

Year

Internal

accounting

rules.(UK)

US GAAP

Percentage

of

differences

1997

₤2984

₤2400

-19,6%

1998

₤3321

₤3044

-8,3%

1999

₤3355

₤3198

-4,7%

2000

₤3147

₤2389

-24,1%

2001

₤3215

₤2334

-27,4%

16.

How significant are the differences in the presentation of thecompany's results of operations?

Company

Year

Internal

accounting

rules.(UK)

US GAAP

Percentage

of

differences

DaimlerBenz

(million DM)

1993

18145

26281

+44,8%

1994

20251

29435

+45,4%

1995

13842

22860

+65,1%

17.

How significant are the differences in the presentation of thecompany's results of operations?

Company

Year

Internal

accounting

rules.(UK)

US GAAP

Percentage

of

differences

Ericsson

(million Skr)

1998

63112

70318

+11,4%

1999

69126

85616

+23,9%

2000

91686

109217

+19,1%

18.

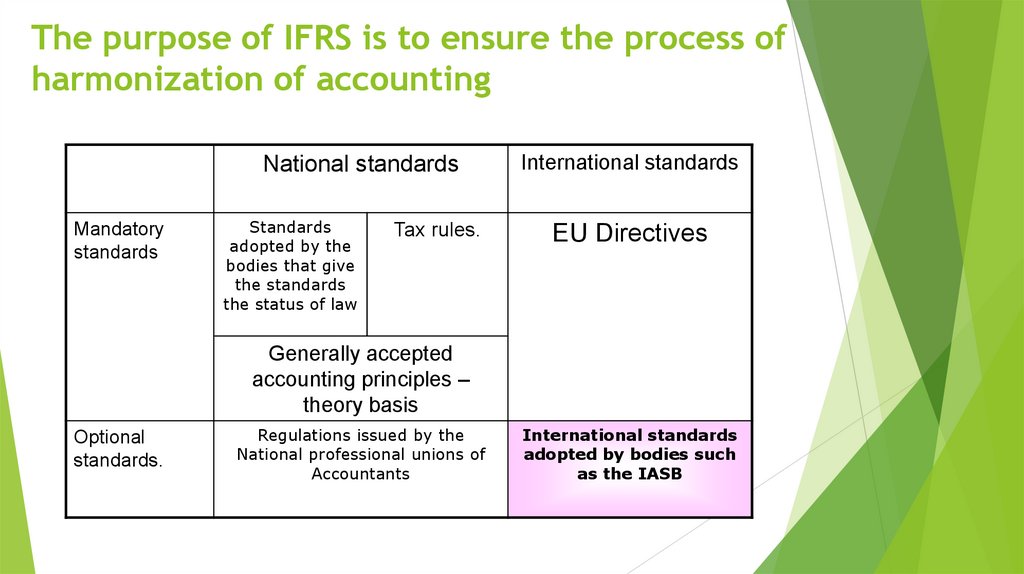

The purpose of IFRS is to ensure the process ofharmonization of accounting

National standards

Mandatory

standards

Standards

adopted by the

bodies that give

the standards

the status of law

Tax rules.

International standards

EU Directives

Generally accepted

accounting principles –

theory basis

Optional

standards.

Regulations issued by the

National professional unions of

Accountants

International standards

adopted by bodies such

as the IASB

19.

Application of the IFRS in the worldThere are several variants for applying IFRS:

1. Applying IFRS as national standards –

currently this is still not the most popular

option;

20.

Application of the IFRS in the world2. National organizations of the development of

financial reporting standards use IFRS as the

main reference for the development of their

own standards - most highly developed countries

and an ever-growing number of developing

countries and countries with economies in

transition use it;

21.

Application of the IFRS in the world3. Stock exchanges and bodies regulating the

securities market oblige listed companies

(whose securities are traded on the stock

exchanges) to provide consolidated financial

statements prepared in accordance with

IFRS.

22.

Application of the IFRS in the world4. Using of the IFRS in the preparation of

financial statements as a result of resolutions

of supranational organizations, for example,

the EU, which declared mandatory reporting in

accordance with the requirements of IFRS since

2005 for companies whose shares are listed on

international stock markets;

23.

Application of the IFRS in the world5. Using of the IFRS by the companies

themselves on their own when preparing

financial statements.

At the same time, an increasing number of

companies are voluntarily switching to

international standards, since this brings

certain benefits for them.

24.

Benefits of using the IFRS for businessImproving the quality of information for decisionmaking by managers;

Facilitating access to capital, including from foreign

sources;

Decrease in the cost of capital;

Easy application of uniform reporting standards in

subsidiaries registered in different countries;

Simplification of mergers and acquisitions;

•Increasing

competitiveness;

25.

Benefits of using the IFRS for potentialinvestors

Improving the quality of information for making

investment decisions;

Building confidence to the provided information;

Better understanding of risks and returns;

The ability to compare the results of the

company's activities with foreign companies;

26.

Benefits of using the IFRS for the stateStrengthening the capital market and increasing

its attractiveness;

Facilitating access to world capital markets and

through this economic growth in the country;

Assistance in attracting foreign investment as a

source of economic growth;

27.

International Accounting Standards BoardThe main goal of the IASB is to provide a process for

the development and implementation of

international financial reporting standards.

The IFRS Committee was founded in 1973 as a result

of an agreement of professional bodies from 10

countries: Australia, Canada, France, Germany,

Japan, Mexico, the Netherlands, Great Britain,

Ireland and the United States.

The official website of the organization:

www.iasb.org

27

28.

The IFRS development process1.

Creation of a Preparatory Committee from a

wide range of specialists in various fields to

discuss issues on the agenda of the IASB Board.

Consulting with the Standards Advisory Board.

29.

The IFRS development process2. Development and publication of the original

document - the primary draft of the standard - for

public discussion (term for discussion approximately

- 90 days). At this time, anyone can express their

opinion on the standard.

30.

The IFRS development process3. Preparation of a working draft of the

provisions of the standard, taking into

account the comments received from all

interested parties at the second stage.

The Board then prepares a Draft

International Financial Reporting Standard

and proposes alternative solutions and

arguments in favor of their acceptance or

rejection

31.

The IFRS development process4. Issue of the final international financial

reporting standard - IFRS (formerly IAS), which

is formed as a result of discussion of the Draft

IFRS and voting on the draft.

32.

The IFRS development process5. Introduction of the standard – in most

cases, new standards begin to be applied

without fail, as a rule, not earlier than 1.5

year after their adoption, but early

application of the standard is welcome.

33.

Types of standardsIAS - International accounting standards were issued until 2003. IAS 1-41 were issued,

some of which replaced previously adopted

standards

IFRS - International financial reporting

standards. IFRS 1-17 have been issued.

33

34.

Types of standardsIn addition, there are interpretations to the

standards (sequences) - SIC - Standards

Interpretations Committee, which are

currently called - IFRIC.

34

35.

BookkeepingAccounting and storage of accounting documents

are organized by the head of an organization.

The head of an organization is obliged to entrust

accounting to the chief accountant or other

official, or to conclude an agreement on the

provision of accounting services.

36.

Requirements for the chief accountant in RussiaFor chief accountants of some organizations

(PJSCs, investment funds, budgetary

organizations), special requirements are

established:

- higher education;

- work experience over 3 years;

- no outstanding convictions for economic crimes.

37.

BookkeepingThe totality of accounting methods forms the

accounting policy of the organization. An

organization independently forms an

accounting policy, guided by the accounting

legislation, federal and industry standards (IAS

8).

When forming an accounting policy in relation

to a specific object, a method of accounting is

selected from among those permitted by using

standards.

38.

Accounting objects1)

facts of economic life;

2)

assets;

3)

liabilities;

4)

sources of funding for its activities (capital);

5)

incomes;

6)

expenses

39.

Accounting objectsA fact of economic life is a transaction, event,

operation that has or is capable of influencing

the financial position of an organization, the

financial result of its activities and (or) its cash

flow.

Each fact of economic life is subject to

registration by a primary accounting document.

It is not allowed to accept for accounting

documents that formalize the facts of economic

life that did not take place.

40.

Source documentsMandatory details of the document:

1) the title of the document;

2) date of preparation of the document;

3) the title of the organization that compiled the

document;

4) the content of the fact of economic life;

5) the value of the natural and (or) monetary measurement

of the fact of economic life, indicating the units of

measurement;

6) the employee's position who made the transaction;

7) signatures

41.

Requirements for documentsIn addition to the required details, extra

information can be included in the documents.

Moreover, if the primary document is drawn up

on the basis of another, then an indication of this

source document is mandatory

42.

Source documentsThe primary accounting document must be drawn

up when the fact of economic life is committed or

immediately after its completion.

The person responsible for the registration of the

fact ensures the timely transfer of documents to

the accounting department, as well as their data

reliability. The person entrusted with accounting is

not responsible for the compliance of the primary

accounting documents drawn up by other persons

with the facts of economic life.

43.

Source documentsRequirements of the chief accountant in writing

form that are connected with the procedure of

documenting the facts of economic life, submitting

documents, etc. mandatory for all employees of an

economic entity.

44.

Source documentsThe primary accounting document is drawn

up on paper and (or) in the form of an

electronic document signed with an

electronic signature

45.

Source documentsThe documents must be kept in the form in which

they were drawn up. Translation of a paper

document into electronic form for subsequent

storage is not allowed.

In case of loss of documents, as well as their

damage, it is necessary to take all possible

measures to restore them.

46.

Source documents in RussiaThe documents are prepared in Russian. If the

primary document is in a foreign language, then it

must contain a line-by-line translation. An

exception is a situation when, in the place of

business outside the Russian Federation,

legislation obliges to draw up documents in the

language of this country

47.

Source documentsThe date of drawing up the primary document is

the day of its signing by the persons who made the

transaction and those responsible for its execution,

or by the persons responsible for the registration of

the event.

The document must indicate the date of the

commission of the fact of economic life, if it differs

from the date of compilation

48.

Source documentsWhen drawing up primary documents, you can

draw up several related facts of economic life

with one document

49.

Source documentsIt is possible to draw up lasting facts of

economic life (accrual of interest,

depreciation), as well as recurring facts of

economic life (delivery of products in batches

under one contract) by primary documents

drawn up at intervals determined by the

economic entity

50.

Source documentsIt is allowed to use as primary documents that

one that was drawn up or received from another

entity.

51.

Source documentsThe list of persons entitled to sign documents is

established by the head of the organization. The

correctness of the reflection of objects in the

registers is ensured by the persons who compiled

and signed them.

52.

BookkeepingThe data contained in primary accounting

documents are subject to timely registration and

accumulation in accounting registers

53.

Financial statementsThe financial statements should provide a

reliable representation of the financial position

of an economic entity as of the reporting date,

the financial result of its activities and cash

flows for the reporting period, which is

necessary for users of these statements to

make economic decisions.

54.

Financial statementsW. Churchill

The unprecedented thickness

of this report protected it

from the danger of being

read.

54

55.

Financial statementsJ. Bulatovich

(Polish

publicist)

There are three types of

lying: bragging, lying, and

reporting.

55

56.

Отчетность в высказыванияхV. Borisov

(Russian

programmer)

Automation can never completely

replace accounting. It is not profitable

56

57.

Отчетность в высказыванияхR. Kiyosaki

(American

entrepreneur,

investor,

writer)

If you want to take control

of your life, you must

regularly prepare personal

financial statements. If

you do not want to do

this, it is better to give

money to others in a

retirement fund.

57

58.

Financial statementsUsers

Financial statements are

provided to external users

of information

58

59.

Who are external users?Users with

direct

financial

interest

1. Shareholders

2. Investors

3. Suppliers

59

60.

Who are external users?Users with

indirect

financial

interest

1.

Tax authorities

2.

Banks

3.

Government bodies

4.

Auditing companies

5.

Buyers

60

61.

Who are external users?Users without

financial

interest

1.

Exchanges

2.

Statistical bodies

3.

Judiciary

61

62.

What is reporting for?Tasks

1.

Analysis of financial

condition

2.

Evaluation of the efficiency

of functioning

3.

Planning for future

activities

62

63.

Assumptions of Formation of Financial ReportingIndicators

Property

isolation

The assets and liabilities of

an organization exist

separately from the assets

and liabilities of the owners

of this organization and the

assets and liabilities of

other organizations

63

64.

Assumptions of Formation of FinancialReporting Indicators

Business

continuity going concern

The organization will

continue its activities for

the foreseeable future and

it has no intention and need

to liquidate or materially

reduce its activities, and,

therefore, the obligations

will be settled in due course

64

65.

Assumptions of Formation of FinancialReporting Indicators

Business

continuity going concern

65

66.

Assumptions of Formation of FinancialReporting Indicators

Consistency in

the application

of accounting

policies

The accounting policy

adopted by the organization is

applied consistently from one

reporting year to the next.

66

67.

Assumptions of Formation of FinancialReporting Indicators

Temporal

certainty of the

facts of

economic life –

accrual basis

They are reflected in the

accounting and reporting of

the period in which they are

committed, regardless of the

actual time of receipt or

payment of funds associated

with these facts.

67

68.

General requirements for financial statementsReliability

The reporting should give a reliable

view of the financial position of an

economic entity as of the reporting

date, the financial result of its

activities and cash flows for the

reporting period, which is necessary

for users of this reporting to make

economic decisions

68

69.

Financial statementsAnnual financial statements consist of a balance

sheet, a statement of financial results and

explanations to them

70.

Financial statementsIt is mandatory to draw up annual financial

statements (for a calendar year). Preparation of

interim financial statements is voluntary, or

mandatory if required by law

71.

Financial statementsThe financial statements are considered to be

drawn up after they are signed by the head of the

economic entity.

In case of publication of financial statements that

are subject to mandatory audit, such financial

statements must be published together with the

auditor's report.

With regard to financial statements, a trade

secret regime cannot be established.

72.

Financial statementsState information resource - a set of financial

statements of economic entities, as well as audit

reports on it in cases where the statements are

subject to mandatory audit.

In order to form a state information resource, an

economic entity is obliged to submit one copy of

the prepared reporting to the tax authority at the

location of the economic entity.

73.

Accounting method74.

Method elementsTraditionally, there are 8 elements of the

accounting method:

- Documentation

- Inventory

- Measurement

- Calculations (costing)

- Accounts

- Double entry

- Balance

- Reporting

75.

InventoryInventory is a check of the compliance of the

actual availability of assets with their presence

according to the documents.

Inventory must be carried out before drawing up the

annual financial statements, as well as when

changing materially responsible persons, revealing

the facts of theft

75

76.

Inventory - documents1. Order to conduct an inventory

2. Inventory list (including receipt of the materially

responsible person)

3. Collation sheet

4. Act on the results of the inventory

76

77.

Inventory - results1. Surplus (other incomes at market prices (fair

value))

"... Inventory, like any general cleaning, is good

because you find what you are not looking for ..."

2. Shortages (shortages and losses from

damage to values)

77

78.

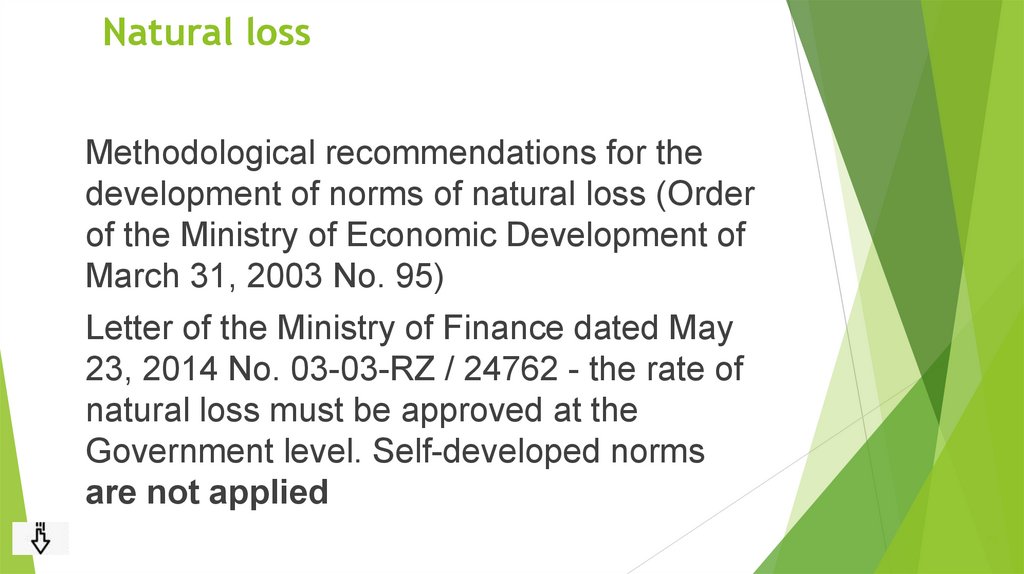

Natural lossMethodological recommendations for the

development of norms of natural loss (Order

of the Ministry of Economic Development of

March 31, 2003 No. 95)

Letter of the Ministry of Finance dated May

23, 2014 No. 03-03-RZ / 24762 - the rate of

natural loss must be approved at the

Government level. Self-developed norms

are not applied

78

79.

ExampleThe frozen berry was received on 08/10/19. Net

weight 1000 kg.

The berry was released:

600 kg - 12/14/2019

395 kg - 12/21/2019

After that, the remainder of the berry is 0 kg.

Natural loss rates:

when stored for 4 months 0.65%;

when stored for 5 months 0.77%;

79

80.

ExampleLosses during storage of berries released on

12/14/19 (4 months 5 days)

600 * 0.65% + 600 * (0.77% -0.65%) / 30.42 * 5

days = 4.0183 kg

Losses during storage of berries released on

12/21/19 (4 months 12 days)

(400 - 4.0183) * 0.65% + (400 - 4.0183) * (0.77% 0.65%) / 30.42 * 12 days = 2.761 kg

Losses by norms > Actual losses

80

81.

The culprit has not been identifiedLetter of the Ministry of Finance dated 20.05.14 No. 0303-07 / 23687 - losses from theft can be taken into

account in expenses in the absence of guilty persons

and the presence of a document confirming their

absence - decisions of the investigator (representative

of the authorized body) + letters dated 06.10.17 No. 03

-03-06 / 1/65418 + dated 17.12.18 No. 03-03-06 /

1/92021 + dated 20.08.19 No. 03-03-06 / 1/63646

81

82.

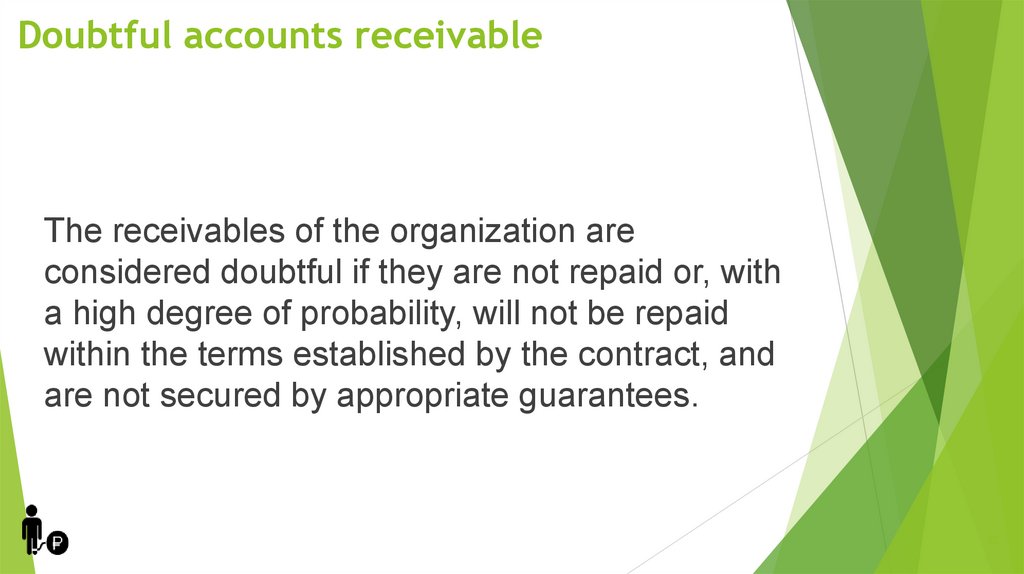

Doubtful accounts receivableThe receivables of the organization are

considered doubtful if they are not repaid or, with

a high degree of probability, will not be repaid

within the terms established by the contract, and

are not secured by appropriate guarantees.

82

83.

Doubtful accounts receivableSince 2011, organizations are required to

create reserves for doubtful debts.

Basis - the results of the inventory of accounts

receivable

83

84.

Doubtful accounts receivableAccounts receivable are recognized as doubtful

from the date of due date of payment under

the agreement - letter of the Ministry of Finance

dated July 26, 2018 No. 03-03-06 / 1/52667.

Provisions can be created depending on the

duration of the delay in payment (<45 days,

45-90 days,> 90 days)

84

85.

Monetary measurementAccounting objects are subject to monetary

measurement.

Monetary measurement of accounting objects in

the Russian Federation is performed in the

currency of the Russian Federation.

Unless otherwise provided by law, the value of

accounting items expressed in foreign currency is

subject to conversion into the currency of the

Russian Federation.

86.

Calculation (costing)In some cases, it is not possible to directly

determine the cost estimate of accounting

objects (costs relate to several objects, the cost

of an object consists of several cost items). In

this case, they resort to a special calculation calculation.

87.

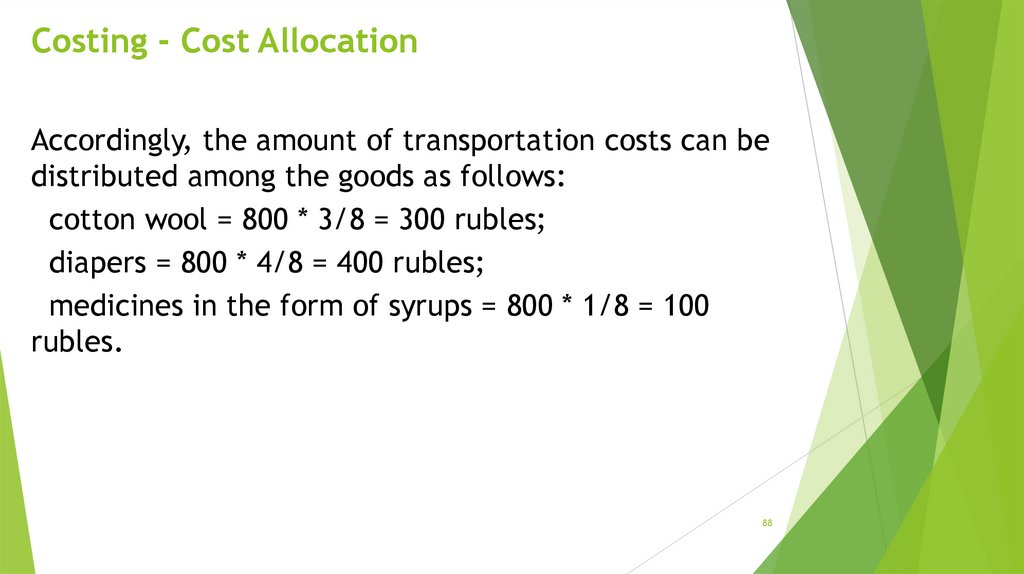

Costing - Cost AllocationLet the transported goods occupy the following volumes

and have masses:

cotton wool - 3 cubic meters - 300 kg;

diapers - 4 cubic meters - 400 kg;

syrup - 1 cubic meter - 2000 kg.

The total capacity of the car body is 8 cubic meters. m

.; total lifting capacity - 3000 kg.

Delivery costs amounted to 800 rubles.

88.

Costing - Cost AllocationAccordingly, the amount of transportation costs can be

distributed among the goods as follows:

cotton wool = 800 * 3/8 = 300 rubles;

diapers = 800 * 4/8 = 400 rubles;

medicines in the form of syrups = 800 * 1/8 = 100

rubles.

88

89.

Costing - Cost AllocationLet the transported goods occupy the following volumes

and have masses:

cotton wool - 3 cubic meters - 300 kg;

diapers - 4 cubic meters - 400 kg;

syrup - 1 cubic meter - 2000 kg.

The total capacity of the car body is 9 cubic meters. m

.; total lifting capacity - 2700 kg.

Delivery costs amounted to 800 rubles.

90.

Costing - Cost AllocationAccordingly, the amount of transportation costs can be

distributed among the goods as follows:

cotton wool = 800/2700 * 300 = 88.9 rubles;

diapers = 800/2700 * 400 = 118.5 rubles;

syrups = 800/2700 * 2000 = 592.6 rubles.

91.

RecommendationTry to account as many cost drivers as

possible.

For this, it is possible to propose to use

multi-factor approaches to the distribution of

costs.

But it should not be forgotten that the multifactor approach to cost allocation turns out

to be more time consuming.

92.

Costing - Cost AllocationLet the transported goods occupy the following

volumes and have masses:

cotton wool - 3 cubic meters - 300 kg;

diapers - 4 cubic meters - 400 kg;

syrup - 1 cubic meter - 2000 kg.

Delivery costs amounted to 800 rubles.

Distribute costs taking into account two bases: the

volume and weght of the transported values.

93.

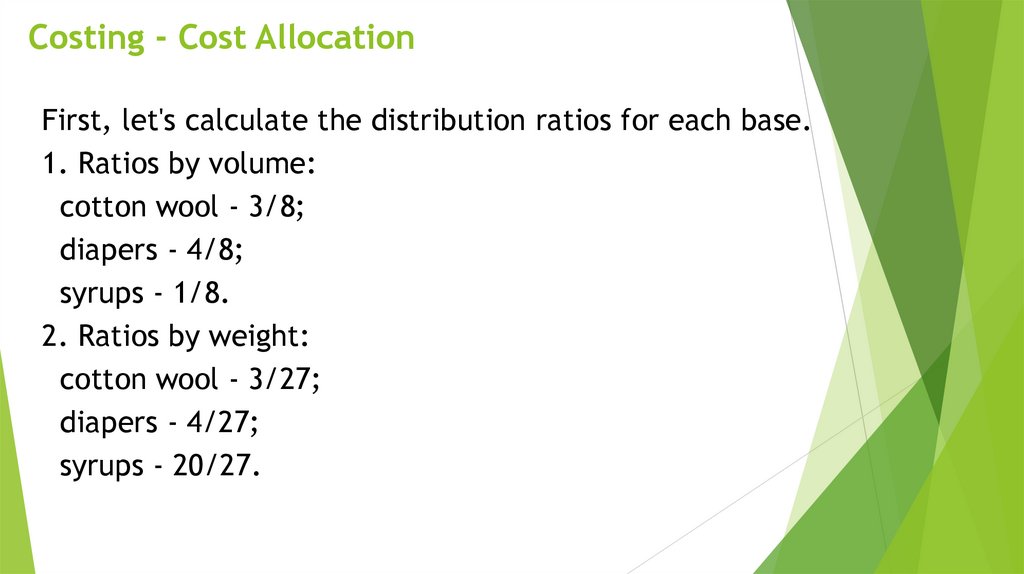

Costing - Cost AllocationFirst, let's calculate the distribution ratios for each base.

1. Ratios by volume:

cotton wool - 3/8;

diapers - 4/8;

syrups - 1/8.

2. Ratios by weight:

cotton wool - 3/27;

diapers - 4/27;

syrups - 20/27.

94.

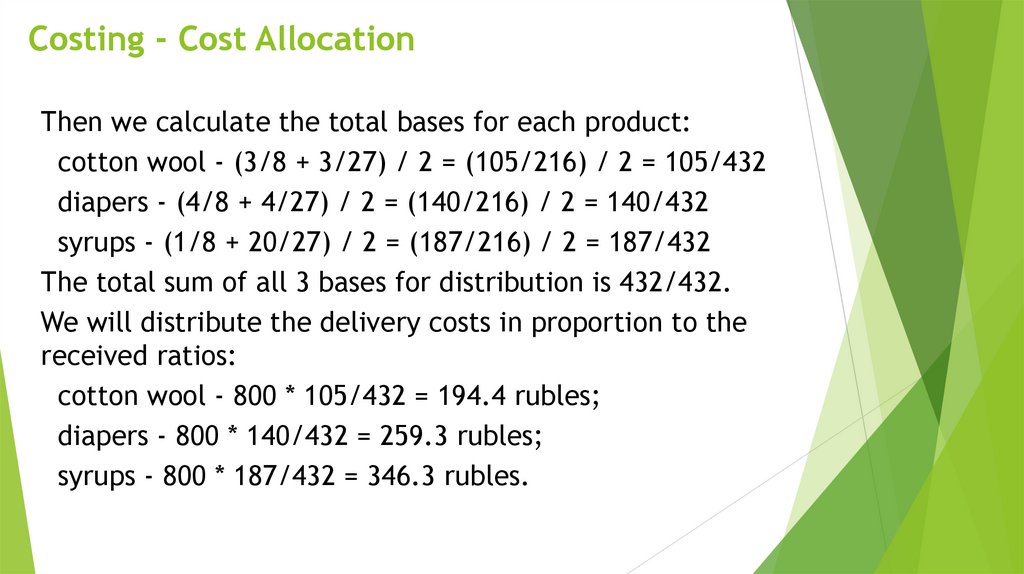

Costing - Cost AllocationThen we calculate the total bases for each product:

cotton wool - (3/8 + 3/27) / 2 = (105/216) / 2 = 105/432

diapers - (4/8 + 4/27) / 2 = (140/216) / 2 = 140/432

syrups - (1/8 + 20/27) / 2 = (187/216) / 2 = 187/432

The total sum of all 3 bases for distribution is 432/432.

We will distribute the delivery costs in proportion to the

received ratios:

cotton wool - 800 * 105/432 = 194.4 rubles;

diapers - 800 * 140/432 = 259.3 rubles;

syrups - 800 * 187/432 = 346.3 rubles.

95.

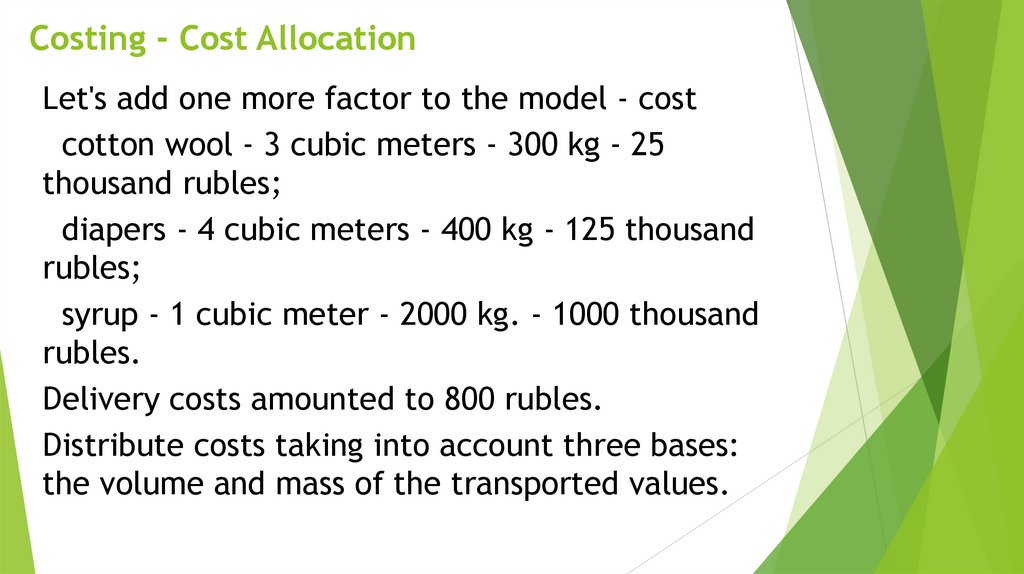

Costing - Cost AllocationLet's add one more factor to the model - cost

cotton wool - 3 cubic meters - 300 kg - 25

thousand rubles;

diapers - 4 cubic meters - 400 kg - 125 thousand

rubles;

syrup - 1 cubic meter - 2000 kg. - 1000 thousand

rubles.

Delivery costs amounted to 800 rubles.

Distribute costs taking into account three bases:

the volume and mass of the transported values.

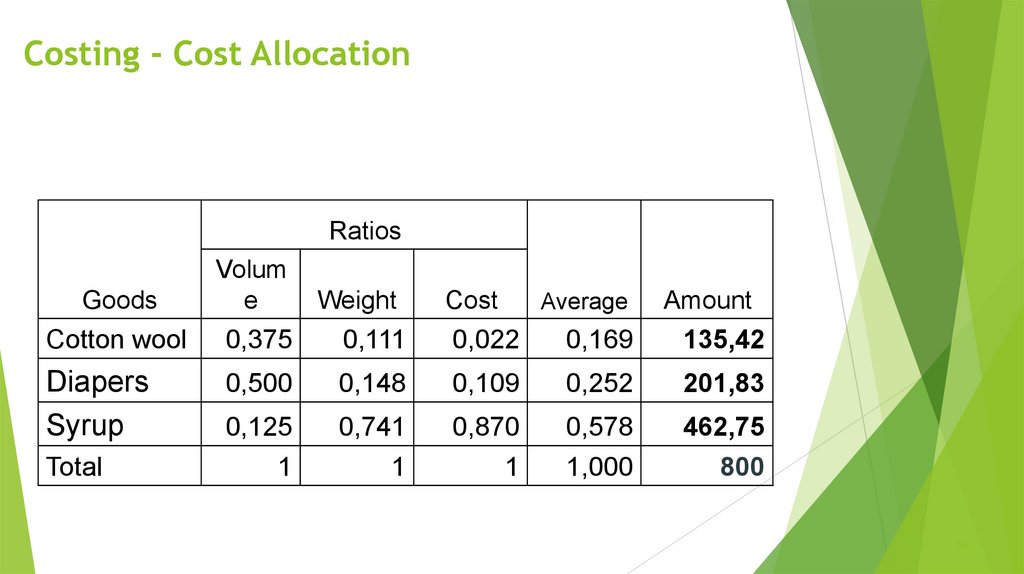

96.

Costing - Cost AllocationRatios

Goods

Volum

e

Cotton wool

0,375

0,111

0,022

0,169

135,42

Diapers

Syrup

0,500

0,148

0,109

0,252

201,83

0,125

1

0,741

1

0,870

1

0,578

1,000

462,75

800

Total

Weight

Cost

Average

Amount

96

97.

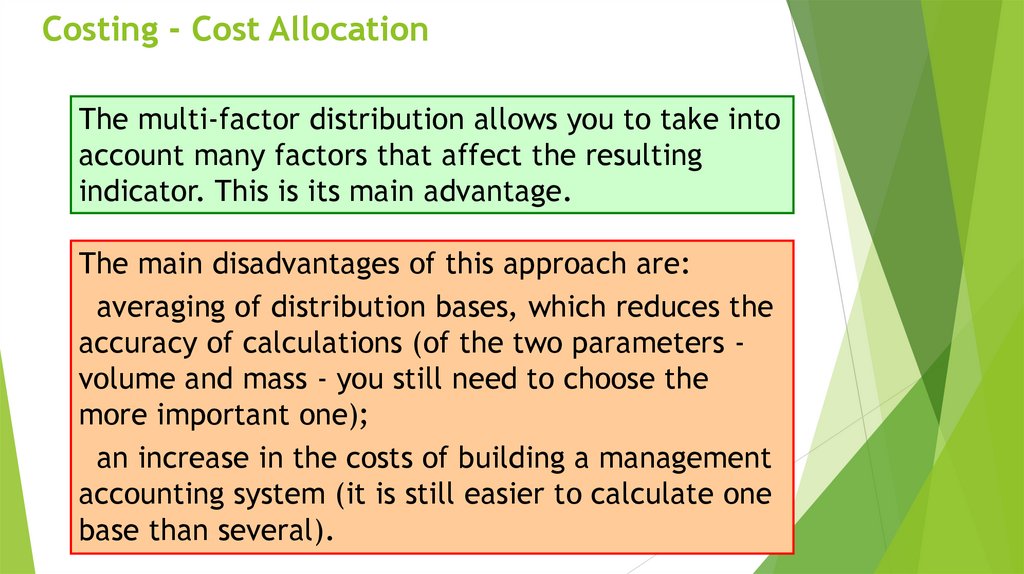

Costing - Cost AllocationThe multi-factor distribution allows you to take into

account many factors that affect the resulting

indicator. This is its main advantage.

The main disadvantages of this approach are:

averaging of distribution bases, which reduces the

accuracy of calculations (of the two parameters volume and mass - you still need to choose the

more important one);

an increase in the costs of building a management

accounting system (it is still easier to calculate one

base than several).

97

98.

AccountsIn accordance with the classical definition, an

account is a special two-sided table that allows you

to systematize information about accounting

objects.

The left side of the account is called debit.

The right side of the account is called a Credit.

The amount of the transaction on the debit or

credit of the account is called the turnover.

The balance of the account is called the balance.

99.

Активные счета – на них отражаетсяимущество организации

Dt

Bal

Materials

Ct

100

1. 200

2. 300

3. 500

1. 150

2. 350

Turn Dt 1000

Turn Ct 500

Bal

600

Bal end = Bal

start +

Turn Dt – Turn Ct

100.

Пассивные счета – на них отражаются источникиформирования имущество организации

Dt

Loans

Bal

Ct

100

1. 200

2. 300

3. 500

1. 750

2. 350

Turn Dt 1000

Turn Ct 1100

Bal

Bal end = Bal

start +

200

Turn Ct – Turn Dt

101.

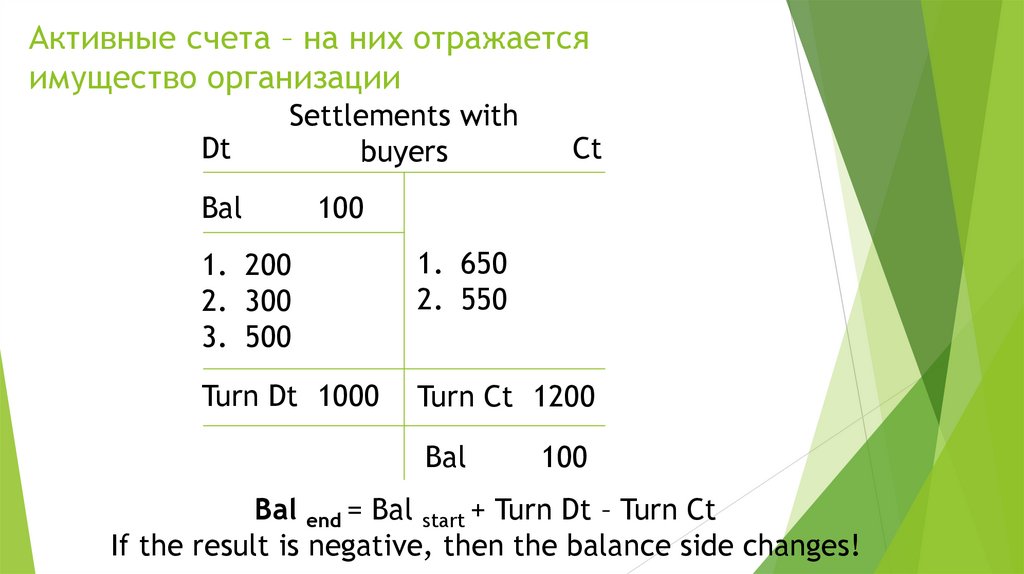

Активные счета – на них отражаетсяимущество организации

Dt

Settlements with

buyers

Bal

Ct

100

1. 200

2. 300

3. 500

1. 650

2. 550

Turn Dt 1000

Turn Ct 1200

Bal

100

Bal end = Bal start + Turn Dt – Turn Ct

If the result is negative, then the balance side changes!

102.

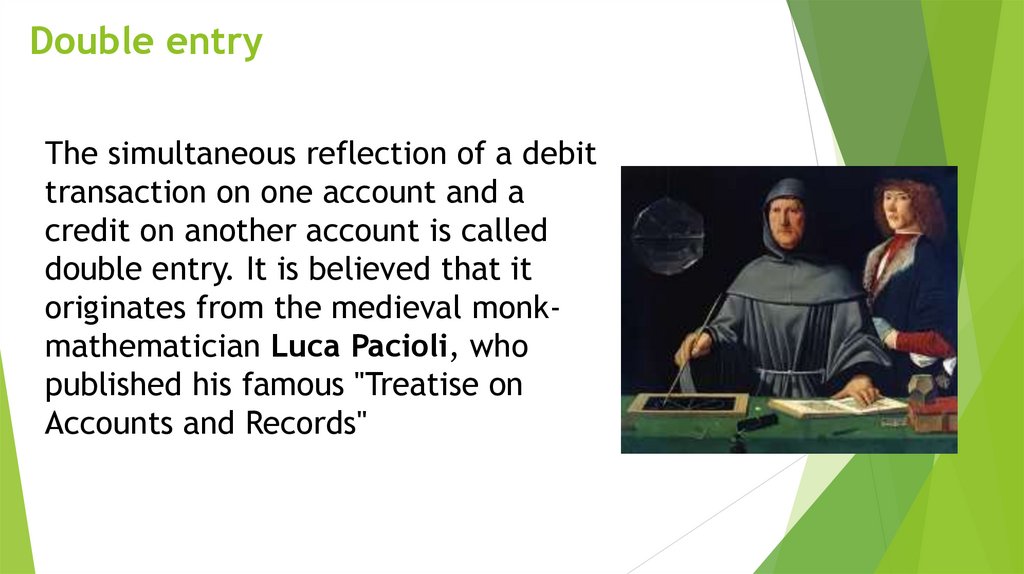

Double entryThe simultaneous reflection of a debit

transaction on one account and a

credit on another account is called

double entry. It is believed that it

originates from the medieval monkmathematician Luca Pacioli, who

published his famous "Treatise on

Accounts and Records"

103.

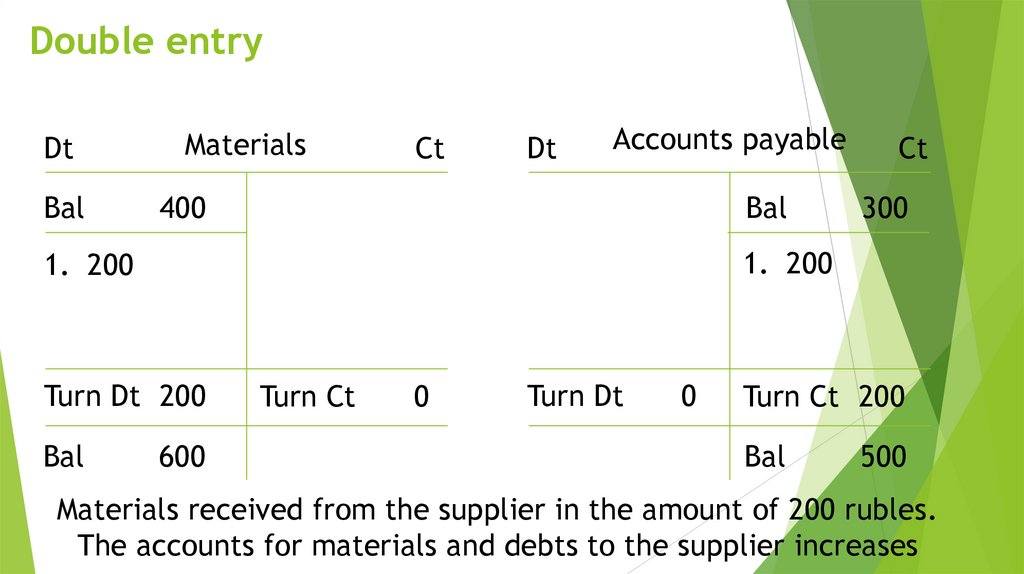

Double entryDt

Bal

Materials

Ct

Dt

Accounts payable

400

Bal

300

1. 200

1. 200

Turn Dt 200

Bal

Ct

600

Turn Ct

0

Turn Dt

0

Turn Ct 200

Bal

500

Materials received from the supplier in the amount of 200 rubles.

The accounts for materials and debts to the supplier increases

104.

Double entryThere are 4 types of business transactions in total

Asset + = Liability + (see previous example)

Asset - = Liabilities Asset ± = Passive

Asset = Passive ±

105.

Double entry (A- = P-)Cash

Dt

Bal

Turn Dt

Bal

Ct

Dt

Accounts payable

Bal

500

0

300

1. 200

1. 200

Turn Ct 200

Turn Dt 200

Turn Ct

Bal

The debt to the supplier in the amount of 200 rubles

was paid in cash.

Ct

300

0

100

106.

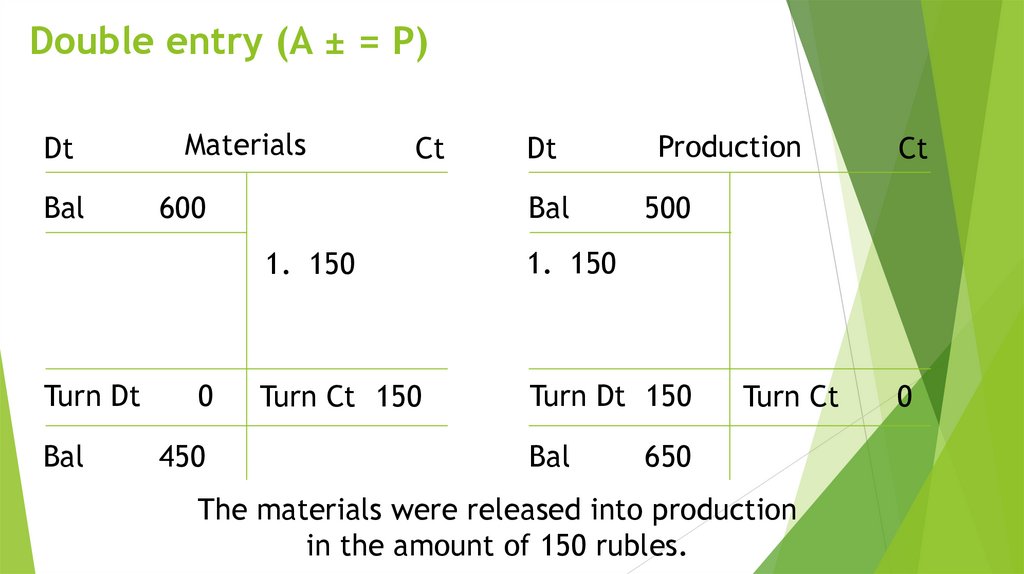

Double entry (A ± = P)Dt

Bal

Turn Dt

Bal

Materials

Ct

600

0

450

Dt

Bal

Production

500

1. 150

1. 150

Turn Ct 150

Turn Dt 150

Bal

Ct

Turn Ct

650

The materials were released into production

in the amount of 150 rubles.

0

107.

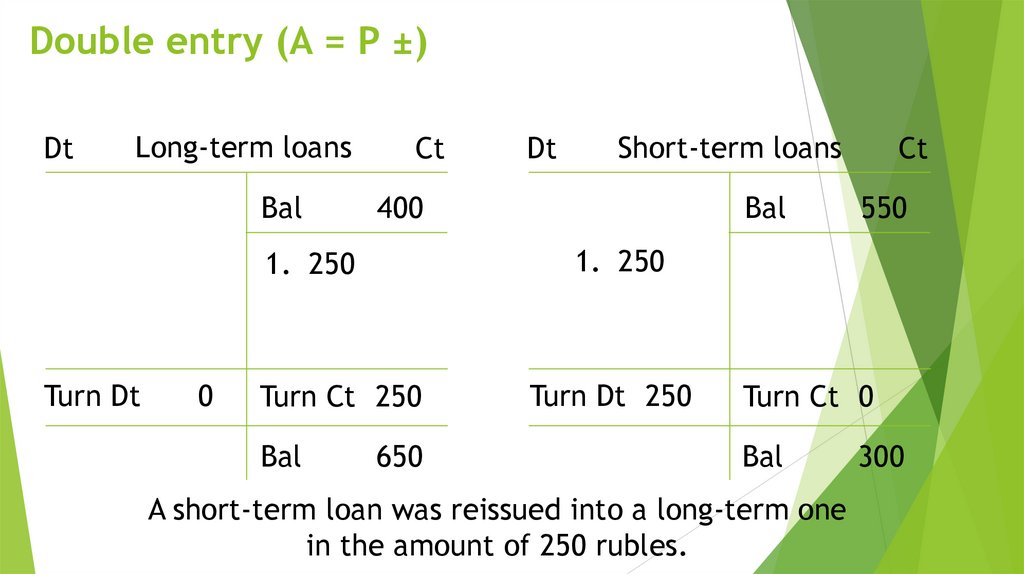

Double entry (A = P ±)Dt

Long-term loans

Bal

Ct

0

Bal

Ct

550

1. 250

Turn Ct 250

Bal

Short-term loans

400

1. 250

Turn Dt

Dt

650

Turn Dt 250

Turn Ct 0

Bal

A short-term loan was reissued into a long-term one

in the amount of 250 rubles.

300

108.

Accounting objects109.

AssetsAssets are resources whose value can be

estimated and from which the company expects

to receive economic benefits.

Depending on the term of their circulation, they

are divided into non-current (long-term) and

current (short-term) assets.

110.

CashCash means cash and non-cash funds of an

organization stored in the cash desk and on

settlement (currency) accounts in banks.

All cash must be kept at the cash desk of the

organization. At the same time, there is a "cash

limit" - a limit value, above which, as of the end

of the day, there should not be a cash balance

111.

CashNon-cash funds are kept in current accounts in

banks. Currently, almost all interaction of

organizations with banks about payments is carried

out in electronic form.

Most of the payments are made on the basis of

payment orders drawn up by the payer. Without

the client's order, funds are debited only by a court

decision and in other cases established by law

112.

CashIn some cases, transactions on current accounts may be

blocked. This usually happens at the request of the

Federal Tax Service. The grounds for blocking an account

are:

- non-payment of taxes (only within the amount specified

in the decision of the tax authority);

- failure to submit a tax return (all funds on current

accounts can be blocked);

- non-compliance with the rules of electronic document

management (as a rule, in relations between tax

authorities and an organization);

- the results of tax audit.

113.

CashTo store currency, organizations may use foreign

currency accounts. However, on the territory of the

Russian Federation, all payments should be carried

out only using the national currency. Therefore,

foreign currency accounts, as a rule, are opened by

organizations engaged in foreign economic activity.

When storing funds in a foreign currency account, an

organization may get exchange rate differences

(positive - income; negative - expense).

114.

CashIn addition to current and foreign currency accounts,

organizations may have special bank accounts. Today,

as a rule, this is represented by only one type of

accounts - letters of credit, but using of them is

constantly decreasing.

The essence of the letter of credit is that funds are

withdrawn to it to pay for one previously agreed

operation. When the bank receives documents from

the second party, the credit institution will make the

payment from the letter of credit account without

the agreement of the payer.

115.

CashOperations with cash is called cash flow.

The cash flows of the organization are divided into

cash flows from current, investment and financial

operations.

An entity's cash flows from operations in the ordinary

course of business that generate revenue are

classified as cash flows from current operations.

116.

Casha) receipts from the sale of products and goods to buyers;

b) payments to suppliers (contractors) for purchased raw

materials, materials, works, services;

c) payments to the employees of the organization, as well as

payments in their favor to third parties;

d) payments of corporate income tax;

e) payment of interest on debt obligations (loans and

borrowings), with the exception of interest included in the

cost of the acquired property;

f) receipt of interest on customer receivables (for example,

for deferred payment);

g) cash flows on financial investments purchased for the

purpose of their resale in the short term (as a rule, within

three months).

117.

CashAn entity's cash flows from transactions related to

the acquisition, creation or disposal of an entity's

non-current assets are classified as investment cash

flows.

118.

Casha) payments to suppliers and employees of the organization in

connection with the acquisition, creation, modernization,

reconstruction and preparation for the use of non-current

assets;

b) payment of interest on debt obligations included in the cost

of non-current assets;

c) receipts from the sale of non-current assets;

d) payments / receipts in connection with the acquisition of

shares of other organizations, with the exception of financial

investments acquired for the purpose of resale in the short

term;

e) loans to other persons;

f) dividends and similar receipts from equity participation in

other organizations;

119.

CashThe cash flows of the organization from operations

related to the attraction of financing by the

organization on a debt or equity basis, leading to a

change in the amount and structure of the equity and

borrowed funds of the organization are classified as

cash flows from financial operations

120.

Casha) monetary payments of owners to the capital, proceeds from

the issue of shares, an increase in participation interests;

b) payments to owners in connection with the redemption of

the organization's shares from them or their withdrawal from

the membership;

c) payment of dividends and other similar payments for the

distribution of profits in favor of the owners;

d) payments from the issue of own bonds, bills, and other

debt securities;

e) payments in connection with the redemption (redemption)

of own bills and other own debt securities;

f) getting credits and loans from other persons;

g) return of loans and borrowings received from other persons.

121.

Cash documentsMonetary documents are special protected in some

way documents (pin codes, passwords, etc.),

purchased and stored in the organization and having

some value estimate, giving them the right to pay for

any services.

Calculations for their purchase between the parties

have already been made, and the services that can

be obtained with the help of these documents have

not yet been provided (gas coupons, food coupons,

postage stamps, express payment cards, etc.).

122.

Cash equivalentsCash equivalents are highly liquid financial

investments that can be easily converted into a

predetermined amount of cash and are subject to an

insignificant risk of changes in value.

The legislation does not establish a specific list of

cash equivalents. As a rule, these include demand

deposits opened with credit institutions; bills

received and short-term loans issued for the period

up to three months.

123.

Short-term financial investmentsFinancial investments are investments in other companies

made through the acquisition of financial assets, which

include:

- equity securities (shares);

- debt securities (bonds and bills of exchange of other

organizations);

- loans granted, formalized by a loan agreement without

backing it with any kind of security;

- term bank deposits;

- the rights of claim redeemed from other organizations

(under an assignment agreement (assignment of the right

of claim)).

124.

Short-term financial investmentsThe main differences between short-term financial investments

and cash equivalents are:

- duration (for financial investments, as a rule, it is more than 3

months);

- the level of reliability of the assessment of the amount into

which the corresponding assets can be converted (for financial

investments, the amount may vary, while for cash equivalents it

is stable and in most cases is known in advance)

- the recovered economic benefit (financial investments are

made to generate income (dividends, interest, exchange rate

differences), and cash equivalents are considered as a reserve

option.

125.

Short-term financial investmentsAll financial investments are divided into two groups:

- financial investments, for which the current market

value can be determined (as a rule, these are

financial investments that circulate on the financial

market);

- financial investments for which their current market

value cannot be determined.

126.

Short-term financial investmentsIf the current market value can be determined (for

example, at the rate of securities on the stock

exchange), then the organization should revalue

financial investments, and show the difference

between two estimates as income or expense.

Otherwise, the assessment of financial investments

remains unchanged until they are sold.

127.

Accounts receivablesAccounts receivable are amounts owed to this

organization by other participants in economic

relations, which may be other organizations and

individual entrepreneurs (buyers for goods, suppliers

for advances issued to them), budgetary system

authorities (for example, if the organization has

made an overpayment of taxes and fees), extrabudgetary funds, employees of the organization,

insurance companies, etc.

128.

Accounts receivablesAccounts receivable are funds withdrawn from the

organization's turnover. At the moment, these funds

are used by some other economic entity, but for this

organization, these are virtual assets, quasi-assets

that will take on a real form only after their

conversion/

In addition, there is a risk of non-payment of

accounts receivable, that is, it may turn out to be

doubtful, and in the worst case - hopeless.

129.

Accounts receivablesA receivable is recognized as doubtful if the

organization has no assurance about the receipt of

cash or cash equivalents in the foreseeable future to

repay it.

Formally, doubtful debt is not the same as overdue

debt. However, in practice, as a rule, the first sign

indicating the need to consider the debt as doubtful

is the fact of delay in payment on the part of the

debtor.

130.

Accounts receivablesOrganizations can use several tools to manage

doubtful accounts receivable. One of the most

common ways is to create a provision for doubtful

debts with the inclusion of the corresponding

amounts in the organization's expenses. In fact, this

tool can be viewed as a kind of insurance tool.

131.

Accounts receivablesAn extreme case of doubtful accounts receivable is bad

accounts receivable. Bad debts (that is, debts that are

unrealistic to be collected) are those debts to an

organization for which:

a) the established limitation period has expired (as a

general rule, this is 3 years);

b) in accordance with civil legislation, the obligation is

terminated due to the impossibility of its fulfillment, on

the basis of an act of a state body or the liquidation of

an organization.

132.

Accounts receivablesIn addition the debtors of the organization may be its

own employees (for example, an employee of the

organization was given money for travel expenses, but

he did not completely use up the amounts issued).

Separately, it is necessary to highlight the receivables

of suppliers for advances issued. It will be redeemed

not in cash, but in commodity form.

133.

VATThe amounts of VAT on the purchased values are

actually a kind of accounts receivable, that is, the

organization has the right to return the VAT paid to the

supplier of inventory items from the budget. However,

so far these amounts have not become accounts

receivable, that is, they have not been presented for

reimbursement from the budget, since the formalities

established by the legislation have not been fulfilled.

134.

StocksInventories are one of the main group of assets, which

includes several important components:

- raw materials and supplies;

- semi-finished products and components;

- fuel;

- container;

- spare parts;

- construction Materials;

- overalls;

- unfinished production;

- finished products;

- goods.

135.

Fixed assetsFixed assets are assets that have a tangible form

that can bring economic benefits as a result of

their use in the production process or for

administrative purposes and have a useful life of

more than 12 months.

136.

Fixed assets- buildings and constructions. In recent years, this

subgroup is increasingly referred to as real estate;

- vehicles, including not only cars, but also planes, ships,

locomotives and wagons;

- equipment, including various production lines, machine

tools, office equipment;

- land plots and other similar objects.

137.

Fixed assetsOrganizations are given the right to revalue fixed assets,

that is, to bring their residual value to the current market

(or fair) value, since it becomes obsolete over time.

138.

Intangible assetsThese are non-monetary assets protected by certain

copyrights. These include:

- works of science, literature and art;

- exclusive rights to computer programs (as a rule, only

the developer himself has them);

- database;

- phonograms;

- rights to inventions, utility models, industrial designs;

- selection achievements;

- suitably protected trade names;

- trademarks and service marks, etc.

139.

GoodwillOne of the most specific types of intangible assets is

goodwill - business reputation.

Goodwill can arise from an organization only if it has

acquired another organization as an integral property

complex. If the amount paid for the acquired organization

is greater than the difference between the assets and

liabilities of this company, then this difference forms the

buyer's goodwill.

140.

Investments in future non-current assetsFixed assets and intangibles sometimes have a long

period of preparation for the start of use (for

example, fixed assets must be mounted, tested,

and permits obtained). "Future fixed assets" and

"future intangible assets" are called investments in

non-current assets

141.

Profitable investments in material assetsIncome investments in tangible assets include those fixed

assets that are intended to be leased (finance lease).

That is, the organization itself is not going to use the

objects for their intended purpose, receiving economic

benefits from this, but it grants such a right to the lessee,

and forms the benefit as a result of receiving lease

payments.

142.

Long-term financial investmentsLong-term financial investments are investments in

securities for a period of more than 12 months. As a rule,

these are investments that involve the extraction of

income not as a result of speculative transactions (bought

cheaper - sold more expensive), but in the form of

income directly related to the type of securities (for

shares - these are dividends, on bonds and bills - interest)

143.

Capital - sources of property formationThe sources of property formation are divided into

two groups:

- equity capital (within which there is no division

into subgroups);

- debt capital, including the most urgent

liabilities, short-term liabilities with a period of

up to 12 months and long-term liabilities with a

period of more than 12 months.

144.

Accounts payableAccounts payable is a debt owed by this

organization to someone.

There are many types of accounts payable:

- to suppliers and contractors;

- to buyers on advances received;

- organization personnel;

- budget, etc.

145.

Accounts payableAccounts payable to suppliers and contractors

for goods, works, services - this type of

organization’s liabilities is the main one in

accounts payable. Receiving material values

from the supplier, the organization

simultaneously forms a counter liability in an

amount equal to the assessment of the values

received. This is what gives the right to consider

accounts payable as a source of property

formation.

146.

Accounts payableWhen the liability is extinguished in cash or other

assets, then there is a simultaneous disposal of

property and an adequate decrease in the source

of formation of this property.

147.

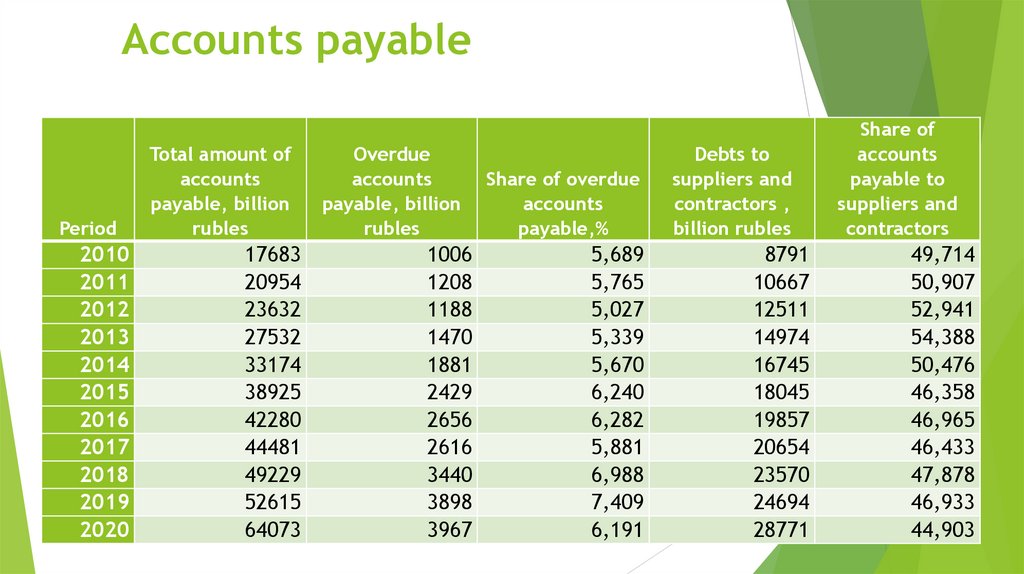

Accounts payablePeriod

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Total amount of

accounts

payable, billion

rubles

17683

20954

23632

27532

33174

38925

42280

44481

49229

52615

64073

Overdue

accounts

payable, billion

rubles

1006

1208

1188

1470

1881

2429

2656

2616

3440

3898

3967

Share of overdue

accounts

payable,%

5,689

5,765

5,027

5,339

5,670

6,240

6,282

5,881

6,988

7,409

6,191

Debts to

suppliers and

contractors ,

billion rubles

8791

10667

12511

14974

16745

18045

19857

20654

23570

24694

28771

Share of

accounts

payable to

suppliers and

contractors

49,714

50,907

52,941

54,388

50,476

46,358

46,965

46,433

47,878

46,933

44,903

148.

Short-term credit and loansShort-term credits and short-term loans provided to

organizations by other entities, for the period that is

less than 12 months.

The main difference between bank credit and loans is

the subject of the provision of borrowed funds: in the

case of a credit, these are credit organizations; loans

can be provided by any legal entity and even an

individual.

In addition, credit are issued only in cash, while loans

can be issued in commodity form.

149.

ProvisionsProvisions are liabilities with an uncertain amount or

period that either will necessarily arise in the future

because the obligating event has already occurred or are

highly probable.

The most common situations that give rise to provisions:

- participation of the organization in the trial as a

defendant;

- sale of goods with a warranty period;

- the liability to provide the next paid holidays to

employees of the organization.

150.

Long credit and loansLong-term credit and borrowings provided to

organizations by other entities for the period that is

more than 12 months. Moreover, even if the loan was

initially attracted for a period of more than 12

months, but less than 12 months remain until its

repayment as of the reporting date, then it must be

requalified as short-term.

151.

EquityThe authorized capital is the valuation of the

organization's property, which was contributed to it by the

founders at the time of its creation.

The amount of the authorized capital and the distribution

of shares in it between the founders is described in the

Charter of the organization.

As a rule, the minimum possible size of the authorized

capital is regulated by the legislation of the country. In

the Russian Federation, for non-public joint stock

companies, this value is at least 10 thousand rubles; for

public joint stock companies - at least 100 thousand

rubles.

152.

EquityThe share in the authorized capital belonging to the

participants of the established organization gives them

the right to participate in the distribution of profits. In a

joint-stock company, these are dividends

153.

EquityAdditional capital ("air capital") - capital resulting from

the revaluation of fixed assets. Gradually over the useful

life of property, plant and equipment, their residual value

begins to differ from their market (fair) value. In such

situations, entities gain the right to revalue their assets.

The increase in the value of assets, which arose "out of

nothing", forms additional capital.

154.

EquityIn addition to the revaluation of fixed assets, share

premium can also be a source of additional capital. This

is the difference between the par value of the shares

issued by the organization and the value at which they

were placed on the financial market.

155.

EquityProfit of the organization:

- gross profit, defined as the difference between the

revenues and the cost of sales of these products;

- profit from sales - gross profit, reduced by the amount

of commercial (selling expenses) and administrative

expenses of the organization;

- profit before tax is the profit from sales, adjusted for

the balance (difference) of other incomes and other

expenses of the organization;

- profit before tax, reduced by the amount of income tax,

forms retained earnings of the reporting year

156.

EquityPart of the profit can be used to pay dividends, and part to form reserve capital. In case of joint-stock companies,

the formation of a reserve capital is not the right of the

organization, but an obligation (5% of the authorized

capital).

In fact, the reserve capital is an allocated part of the

profit, which is not sent to payments to participants, but

can be used to cover losses in future periods.

157.

EquityTargeted financing and receipts are any

transfers from the budget that have a specific

purpose. It is to achieve this goal that these funds

can be spent. If the goal is not achieved, then in

most cases the funds will need to be returned.