economics

economicsSimilar presentations:

")

")

Sectoral Balances, Exchange Rates and Open Economy

1.

EC 224Intermediate Macroeconomics

Sectoral Balances, Exchange Rates and

Open Economy

Lavoie (2014) Post-Keynesian Economics: New Foundations, Chapter 4 and 7

Rey, H. (2015) “Dilemma not Trilemma: The Global Financial Cycle and

Monetary Policy Independence”, NBER Working Paper No. 21162.

1

2.

The overall structure of the Balance ofPayments

1. The Current Account

A: Goods and services

B: Income

C: Transfers

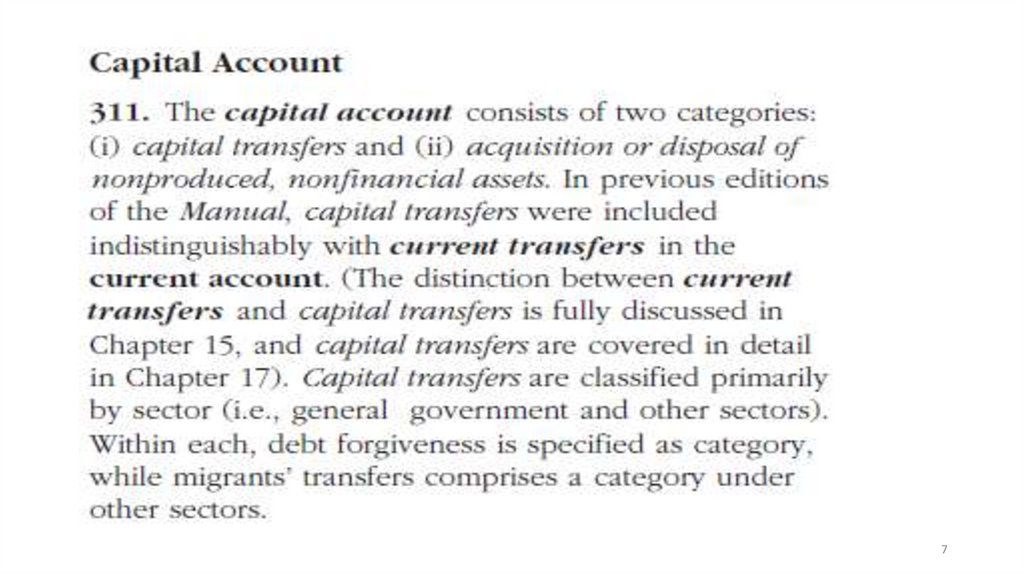

2. The capital and financial accounts

A: The Capital Account

B: The Financial Account

3.

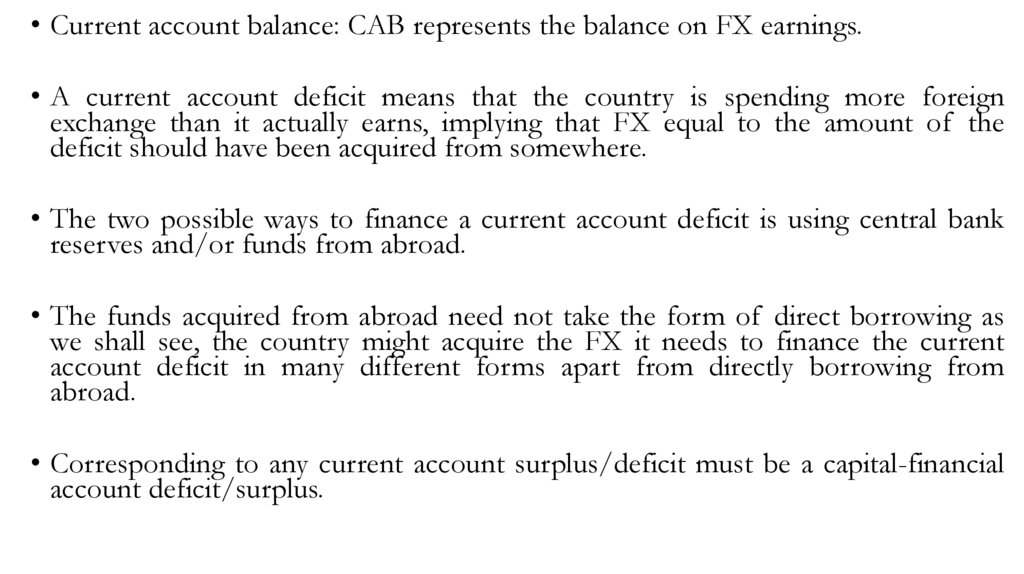

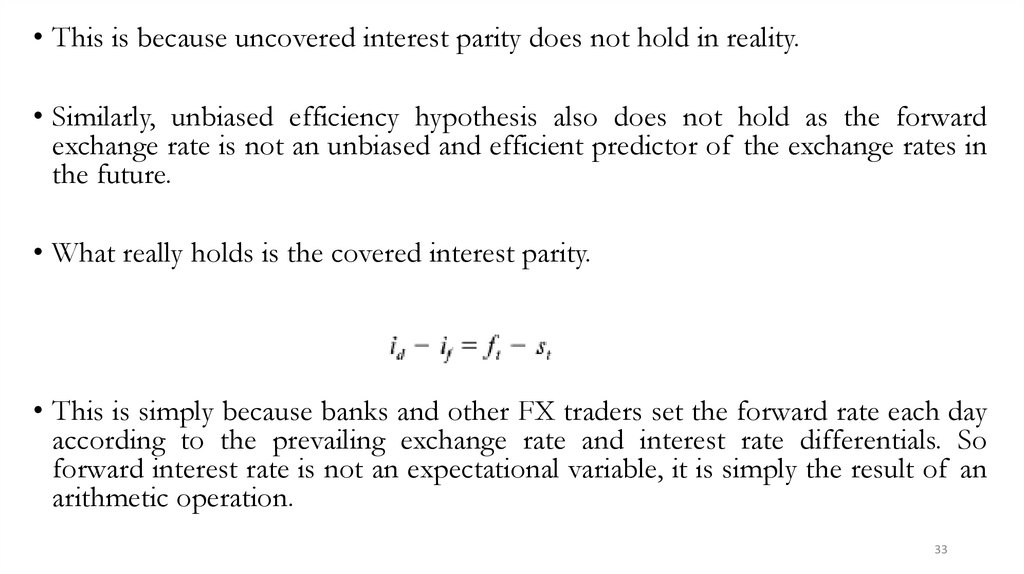

• Current account balance: CAB represents the balance on FX earnings.• A current account deficit means that the country is spending more foreign

exchange than it actually earns, implying that FX equal to the amount of the

deficit should have been acquired from somewhere.

• The two possible ways to finance a current account deficit is using central bank

reserves and/or funds from abroad.

• The funds acquired from abroad need not take the form of direct borrowing as

we shall see, the country might acquire the FX it needs to finance the current

account deficit in many different forms apart from directly borrowing from

abroad.

• Corresponding to any current account surplus/deficit must be a capital-financial

account deficit/surplus.

4.

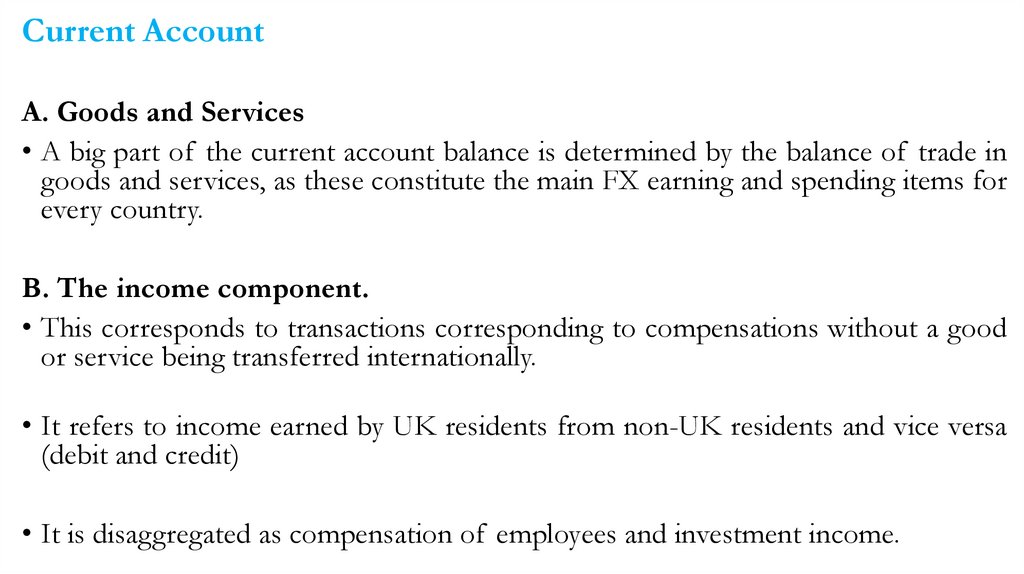

Current AccountA. Goods and Services

• A big part of the current account balance is determined by the balance of trade in

goods and services, as these constitute the main FX earning and spending items for

every country.

B. The income component.

• This corresponds to transactions corresponding to compensations without a good

or service being transferred internationally.

• It refers to income earned by UK residents from non-UK residents and vice versa

(debit and credit)

• It is disaggregated as compensation of employees and investment income.

5.

Compensation of employees comprises wages, salaries and other benefitsearned by individuals from economies other than those in which they are

residents, as well as earnings from extraterritorial bodies such as foreign

embassies.

Investment income comprises income earned from the provision of financial

capital and is classified by direct, portfolio and other investment income.

Transfers: Government and other transfers

6.

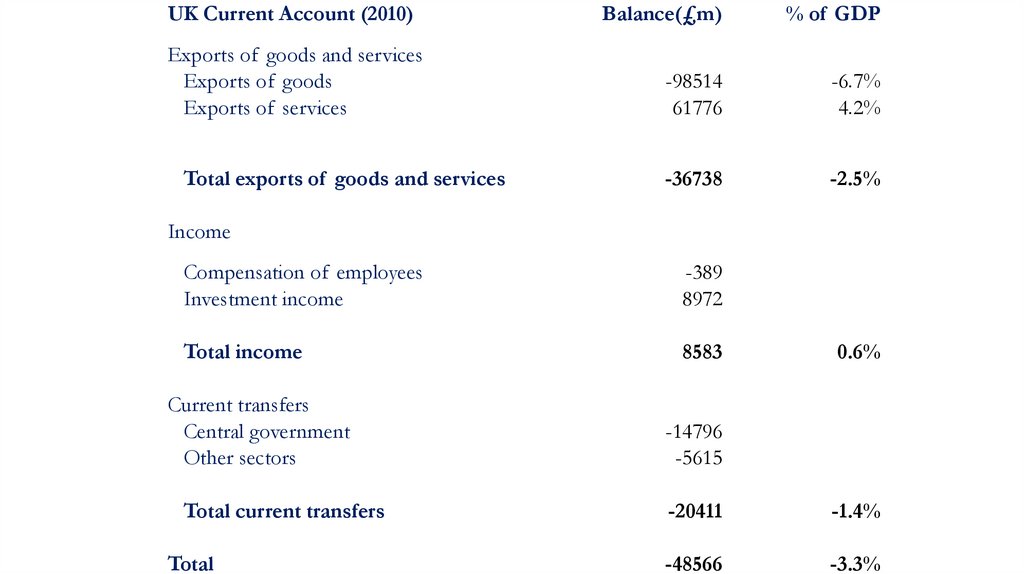

UK Current Account (2010)Balance(£m)

% of GDP

Exports of goods and services

Exports of goods

Exports of services

-98514

61776

-6.7%

4.2%

-36738

-2.5%

Total exports of goods and services

Income

Compensation of employees

Investment income

-389

8972

Total income

8583

Current transfers

Central government

Other sectors

Total current transfers

Total

0.6%

-14796

-5615

-20411

-1.4%

-48566

-3.3%

7.

78.

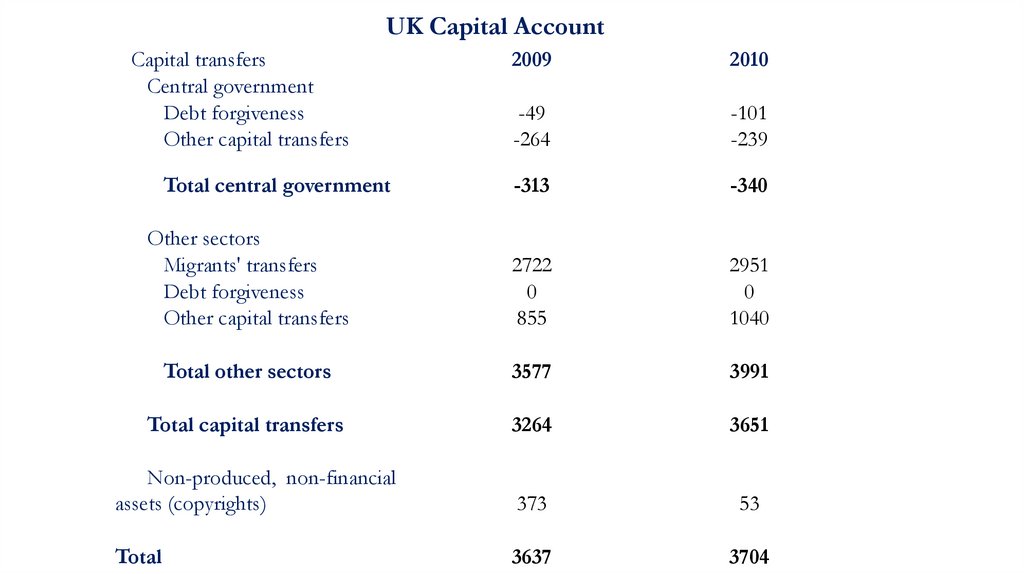

UK Capital AccountCapital transfers

Central government

Debt forgiveness

Other capital transfers

2009

2010

-49

-264

-101

-239

-313

-340

Other sectors

Migrants' transfers

Debt forgiveness

Other capital transfers

2722

0

855

2951

0

1040

Total other sectors

3577

3991

Total capital transfers

3264

3651

Non-produced, non-financial

assets (copyrights)

373

53

Total

3637

3704

Total central government

9.

The financial account• The financial account comprises transactions associated with changes of

ownership of the UK’s foreign financial assets and liabilities.

• Five major components

Direct Investment

Portfolio Investment

Financial Derivatives

Other Investment

Reserve Assets

10.

• Direct investment capital refers to capital provided to or received from an enterprise,by an investor in another country who is in a direct investment relationship with that

enterprise. A direct investment relationship exists if the investor has an equity interest in

an enterprise, resident in another country, of 10 per cent or more of the ordinary shares

or voting stock.

• Portfolio investment refers to transactions in equity and debt securities (apart from

those included in direct investment and reserve assets). Debt securities comprise bonds

and notes and money market instruments.

• Financial derivatives cover any financial instrument the price of which is based upon

the value of an underlying asset (typically another financial asset). Financial derivatives

include options (on currencies, interest rates, commodities, indices), traded financial

futures, warrants and currency and interest swaps.

• Other investment covers trade credits, loans (including financial leases), currency and

deposits, and a residual category for any other assets and liabilities.

11.

• Reserve assets refer to those foreign financial assets that are available to, andcontrolled by, the monetary authorities such as the Bank of England for financing

or regulating payments imbalances. Reserve assets comprise: monetary gold,

Special Drawing Rights, reserve position in the IMF and foreign exchange held by

the Bank.

12.

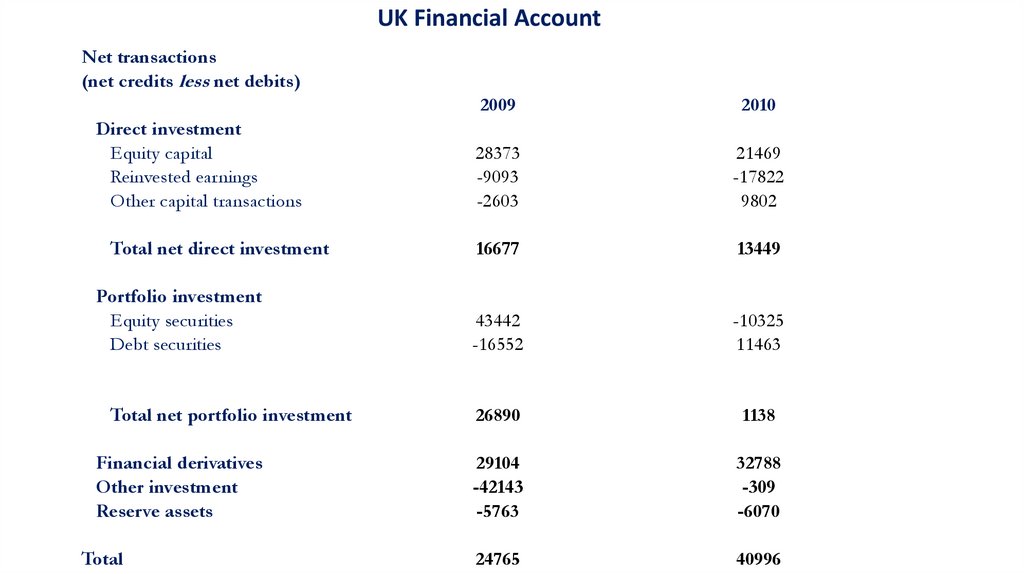

UK Financial AccountNet transactions

(net credits less net debits)

Direct investment

Equity capital

Reinvested earnings

Other capital transactions

Total net direct investment

Portfolio investment

Equity securities

Debt securities

Total net portfolio investment

Financial derivatives

Other investment

Reserve assets

Total

2009

2010

28373

-9093

-2603

21469

-17822

9802

16677

13449

43442

-16552

-10325

11463

26890

1138

29104

-42143

-5763

32788

-309

-6070

24765

40996

13.

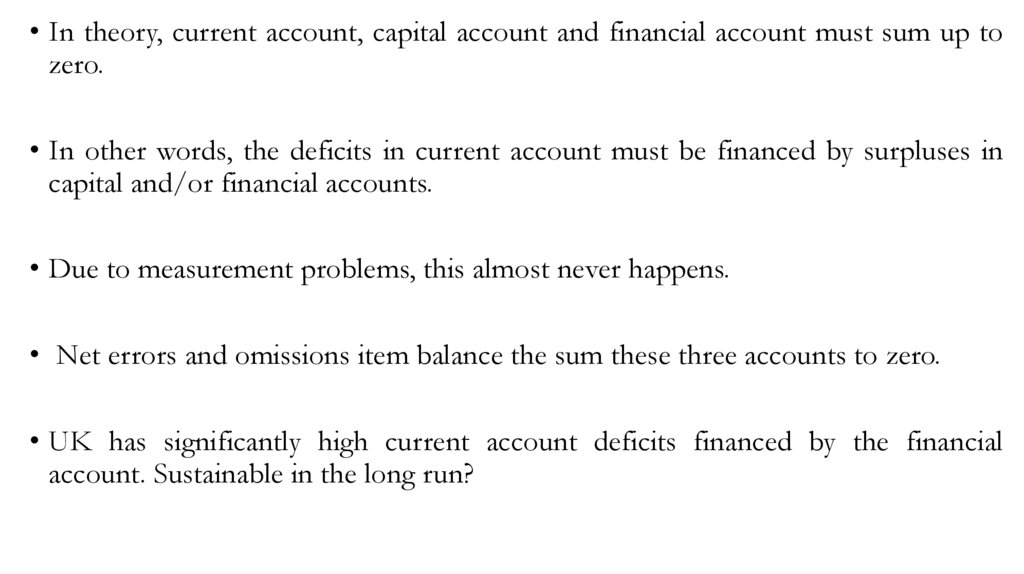

• In theory, current account, capital account and financial account must sum up tozero.

• In other words, the deficits in current account must be financed by surpluses in

capital and/or financial accounts.

• Due to measurement problems, this almost never happens.

• Net errors and omissions item balance the sum these three accounts to zero.

• UK has significantly high current account deficits financed by the financial

account. Sustainable in the long run?

14.

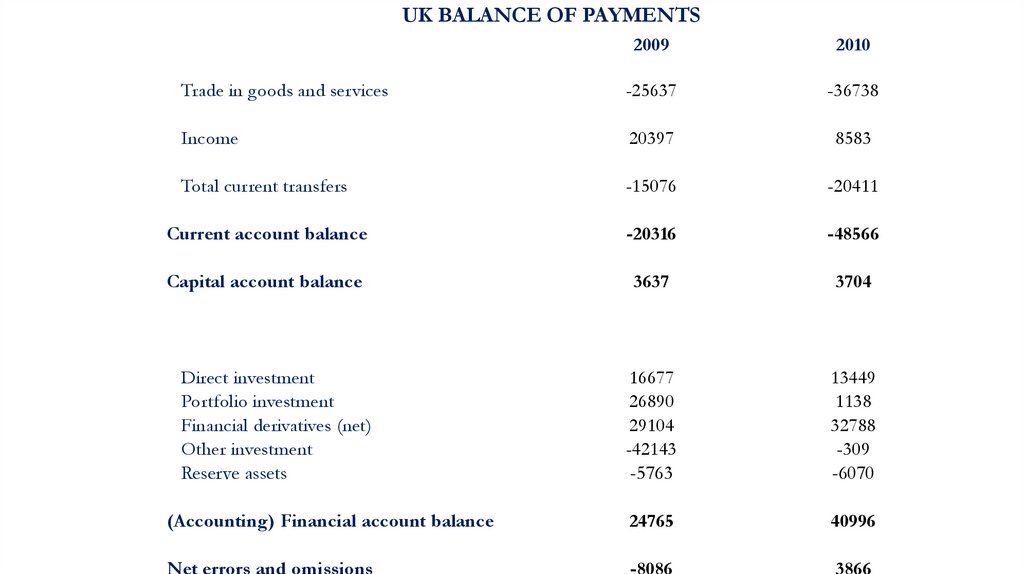

UK BALANCE OF PAYMENTS2009

2010

Trade in goods and services

-25637

-36738

Income

20397

8583

Total current transfers

-15076

-20411

Current account balance

-20316

-48566

Capital account balance

3637

3704

Direct investment

Portfolio investment

Financial derivatives (net)

Other investment

Reserve assets

16677

26890

29104

-42143

-5763

13449

1138

32788

-309

-6070

(Accounting) Financial account balance

24765

40996

Net errors and omissions

-8086

3866

15.

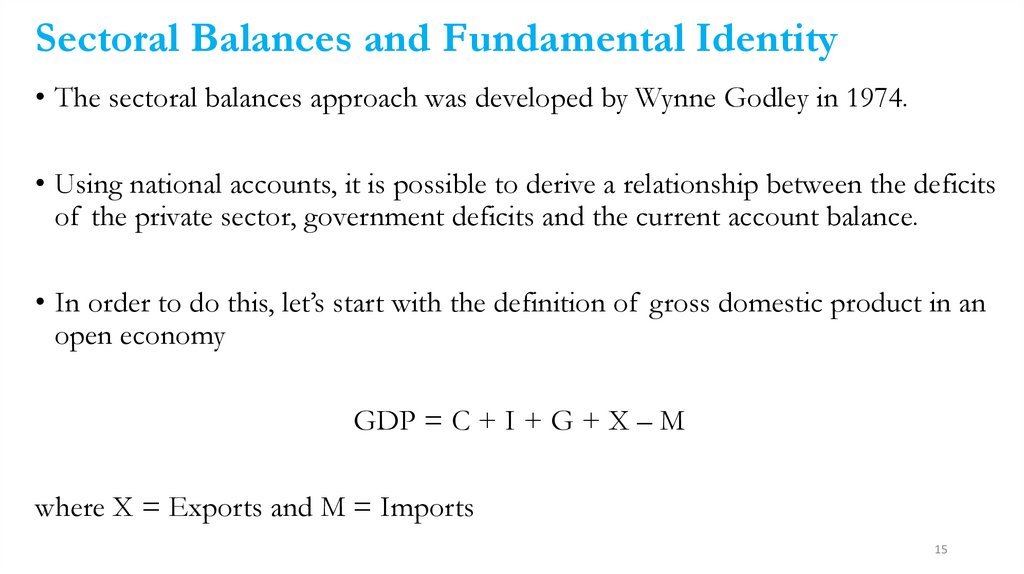

Sectoral Balances and Fundamental Identity• The sectoral balances approach was developed by Wynne Godley in 1974.

• Using national accounts, it is possible to derive a relationship between the deficits

of the private sector, government deficits and the current account balance.

• In order to do this, let’s start with the definition of gross domestic product in an

open economy

GDP = C + I + G + X – M

where X = Exports and M = Imports

15

16.

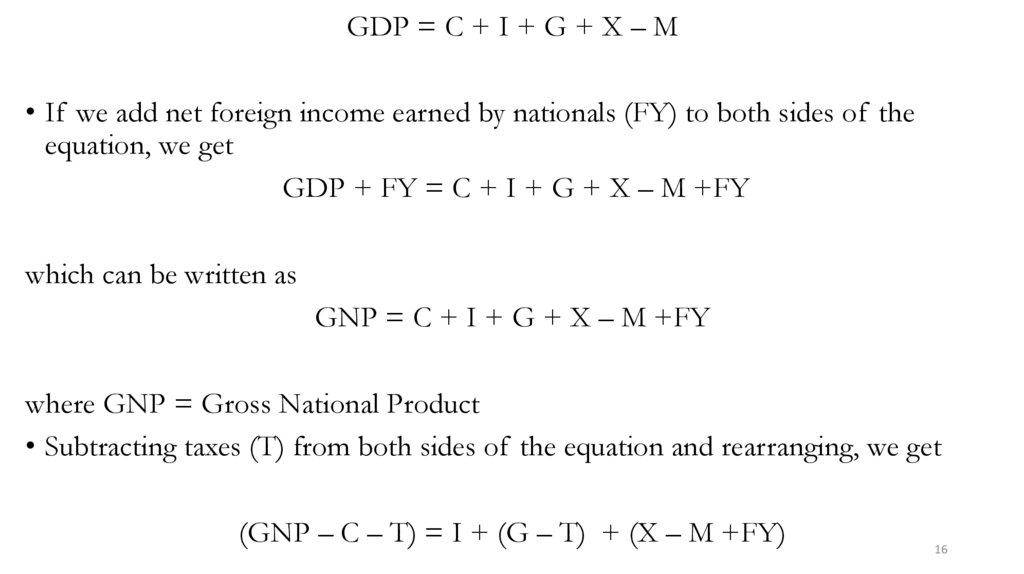

GDP = C + I + G + X – M• If we add net foreign income earned by nationals (FY) to both sides of the

equation, we get

GDP + FY = C + I + G + X – M +FY

which can be written as

GNP = C + I + G + X – M +FY

where GNP = Gross National Product

• Subtracting taxes (T) from both sides of the equation and rearranging, we get

(GNP – C – T) = I + (G – T) + (X – M +FY)

16

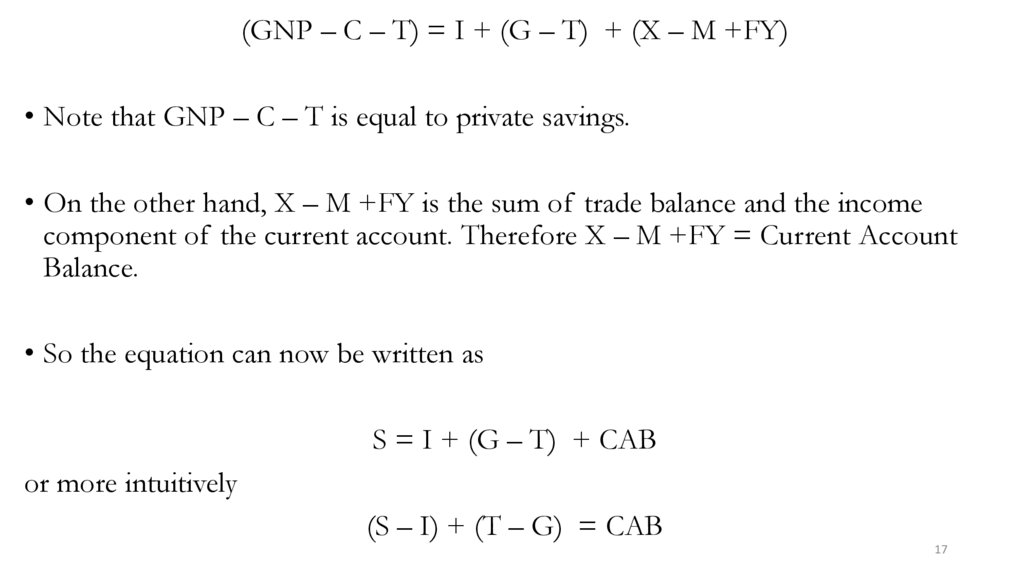

17.

(GNP – C – T) = I + (G – T) + (X – M +FY)• Note that GNP – C – T is equal to private savings.

• On the other hand, X – M +FY is the sum of trade balance and the income

component of the current account. Therefore X – M +FY = Current Account

Balance.

• So the equation can now be written as

S = I + (G – T) + CAB

or more intuitively

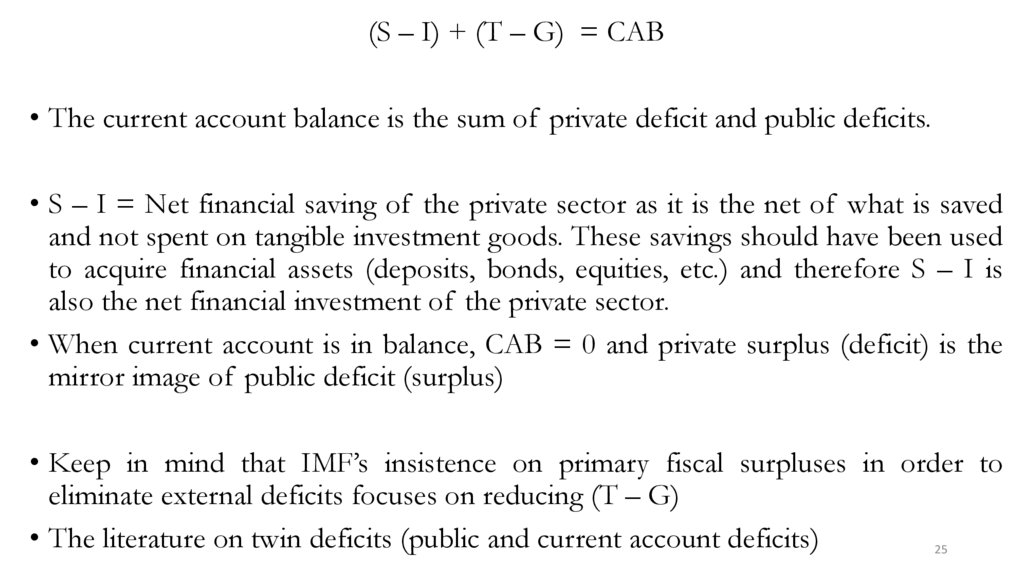

(S – I) + (T – G) = CAB

17

18.

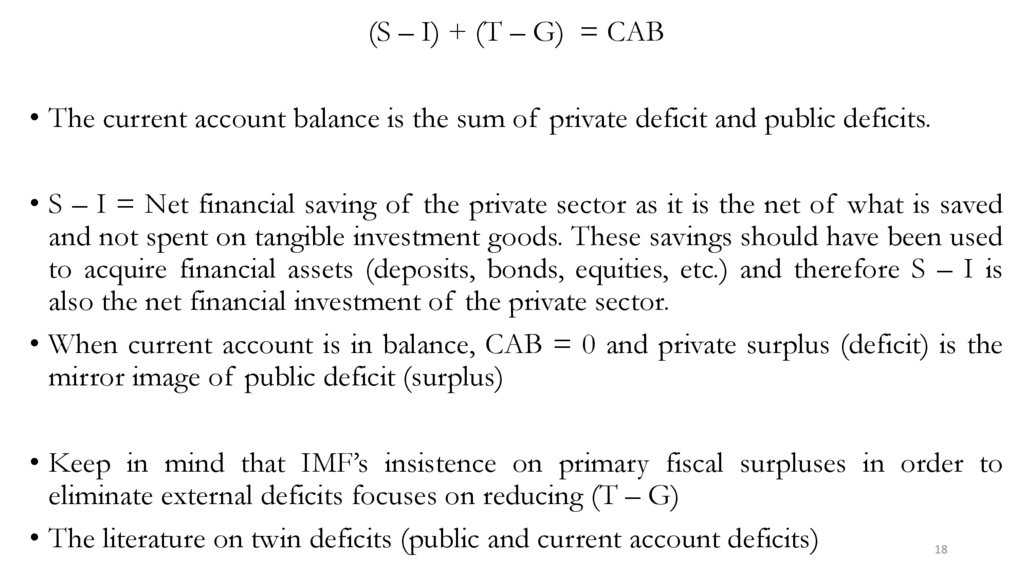

(S – I) + (T – G) = CAB• The current account balance is the sum of private deficit and public deficits.

• S – I = Net financial saving of the private sector as it is the net of what is saved

and not spent on tangible investment goods. These savings should have been used

to acquire financial assets (deposits, bonds, equities, etc.) and therefore S – I is

also the net financial investment of the private sector.

• When current account is in balance, CAB = 0 and private surplus (deficit) is the

mirror image of public deficit (surplus)

• Keep in mind that IMF’s insistence on primary fiscal surpluses in order to

eliminate external deficits focuses on reducing (T – G)

• The literature on twin deficits (public and current account deficits)

18

19.

1920.

21.

22.

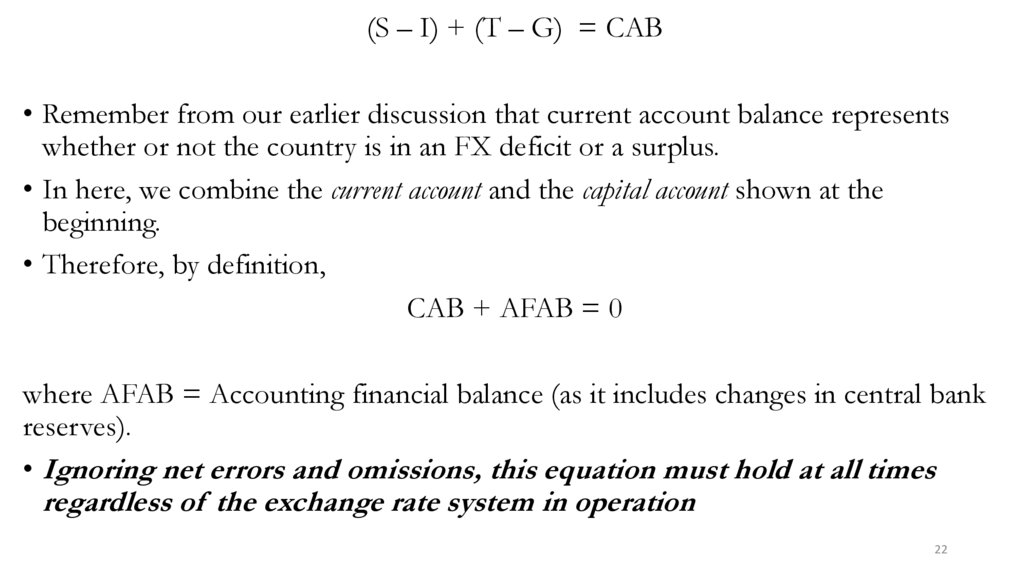

(S – I) + (T – G) = CAB• Remember from our earlier discussion that current account balance represents

whether or not the country is in an FX deficit or a surplus.

• In here, we combine the current account and the capital account shown at the

beginning.

• Therefore, by definition,

CAB + AFAB = 0

where AFAB = Accounting financial balance (as it includes changes in central bank

reserves).

• Ignoring net errors and omissions, this equation must hold at all times

regardless of the exchange rate system in operation

22

23.

UK Balance of Payments2009

2010

Current Account

Trade in goods and services

Income

Total current transfers

-25637

20397

-15076

-36738

8583

-20411

A. Current account balance

-20316

-48566

B. Capital account balance

3637

3704

Financial Account

Direct investment

Portfolio investment

Financial derivatives (net)

Other investment

Reserve assets

16677

26890

29104

-42143

-5763

13449

1138

32788

-309

-6070

C. (Accounting) Financial account balance

24765

40996

Net errors and omissions 1

-8086

3866

24.

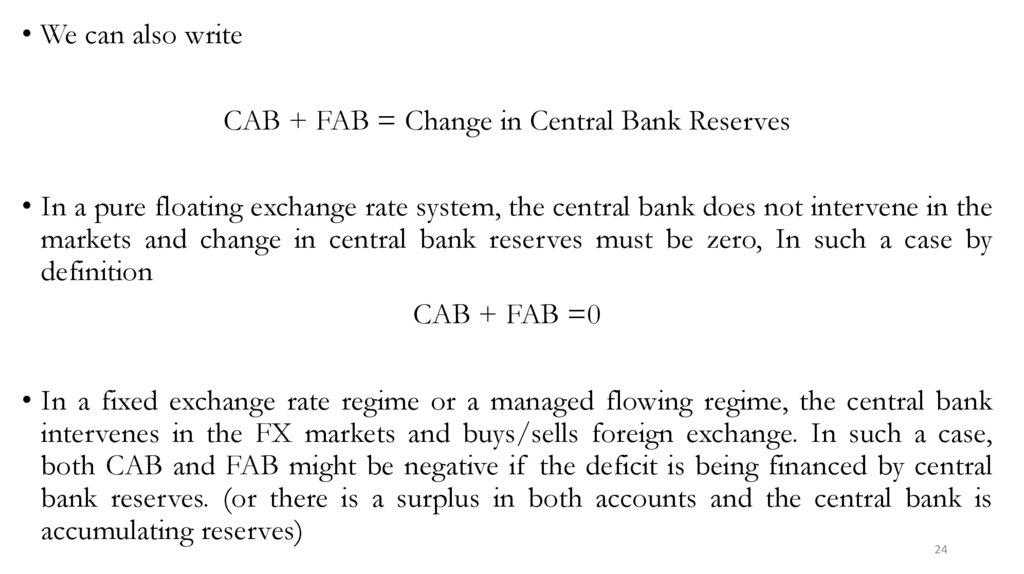

• We can also writeCAB + FAB = Change in Central Bank Reserves

• In a pure floating exchange rate system, the central bank does not intervene in the

markets and change in central bank reserves must be zero, In such a case by

definition

CAB + FAB =0

• In a fixed exchange rate regime or a managed flowing regime, the central bank

intervenes in the FX markets and buys/sells foreign exchange. In such a case,

both CAB and FAB might be negative if the deficit is being financed by central

bank reserves. (or there is a surplus in both accounts and the central bank is

accumulating reserves)

24

25.

(S – I) + (T – G) = CAB• The current account balance is the sum of private deficit and public deficits.

• S – I = Net financial saving of the private sector as it is the net of what is saved

and not spent on tangible investment goods. These savings should have been used

to acquire financial assets (deposits, bonds, equities, etc.) and therefore S – I is

also the net financial investment of the private sector.

• When current account is in balance, CAB = 0 and private surplus (deficit) is the

mirror image of public deficit (surplus)

• Keep in mind that IMF’s insistence on primary fiscal surpluses in order to

eliminate external deficits focuses on reducing (T – G)

• The literature on twin deficits (public and current account deficits)

25

26.

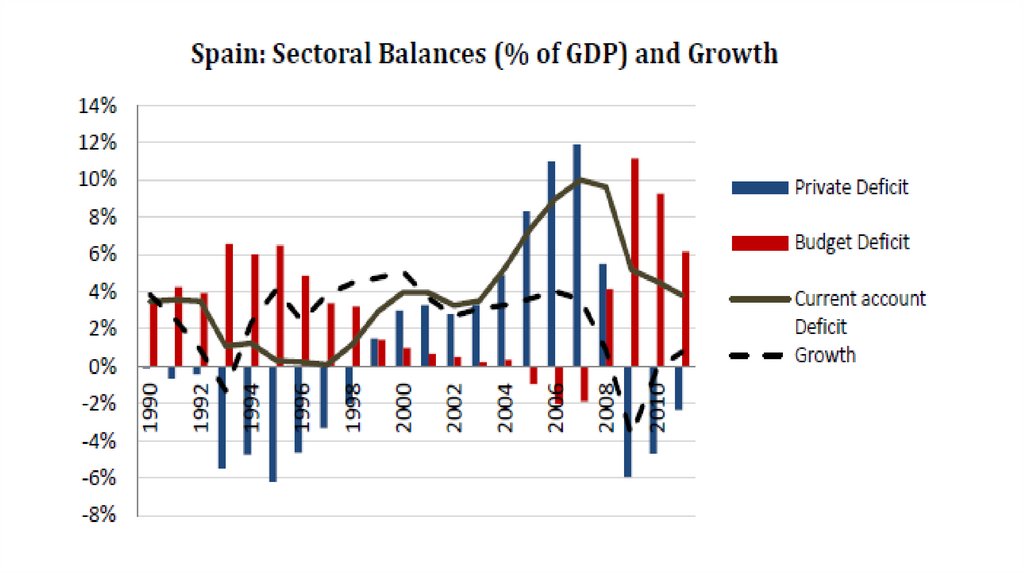

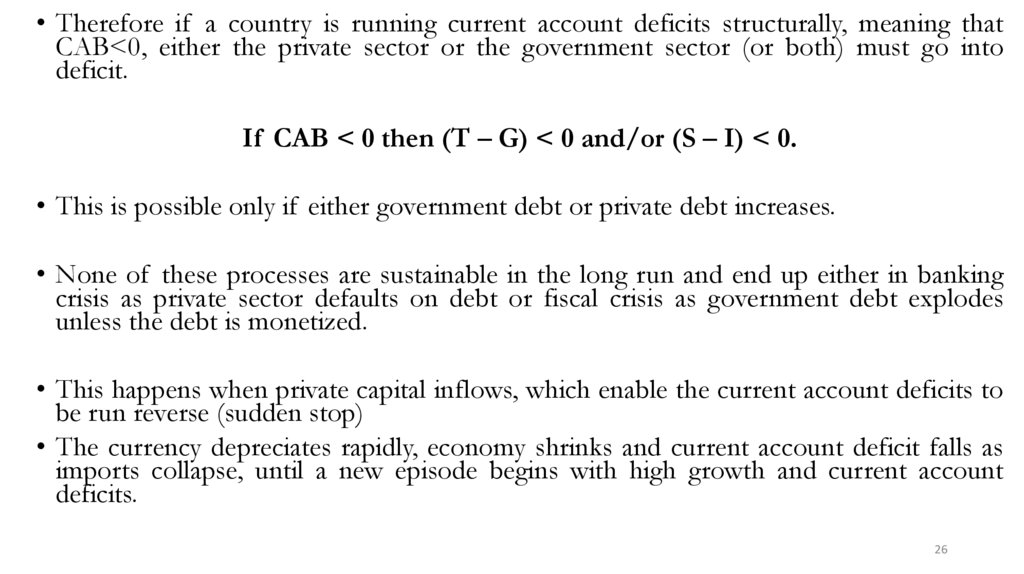

• Therefore if a country is running current account deficits structurally, meaning thatCAB<0, either the private sector or the government sector (or both) must go into

deficit.

If CAB < 0 then (T – G) < 0 and/or (S – I) < 0.

• This is possible only if either government debt or private debt increases.

• None of these processes are sustainable in the long run and end up either in banking

crisis as private sector defaults on debt or fiscal crisis as government debt explodes

unless the debt is monetized.

• This happens when private capital inflows, which enable the current account deficits to

be run reverse (sudden stop)

• The currency depreciates rapidly, economy shrinks and current account deficit falls as

imports collapse, until a new episode begins with high growth and current account

deficits.

26

27.

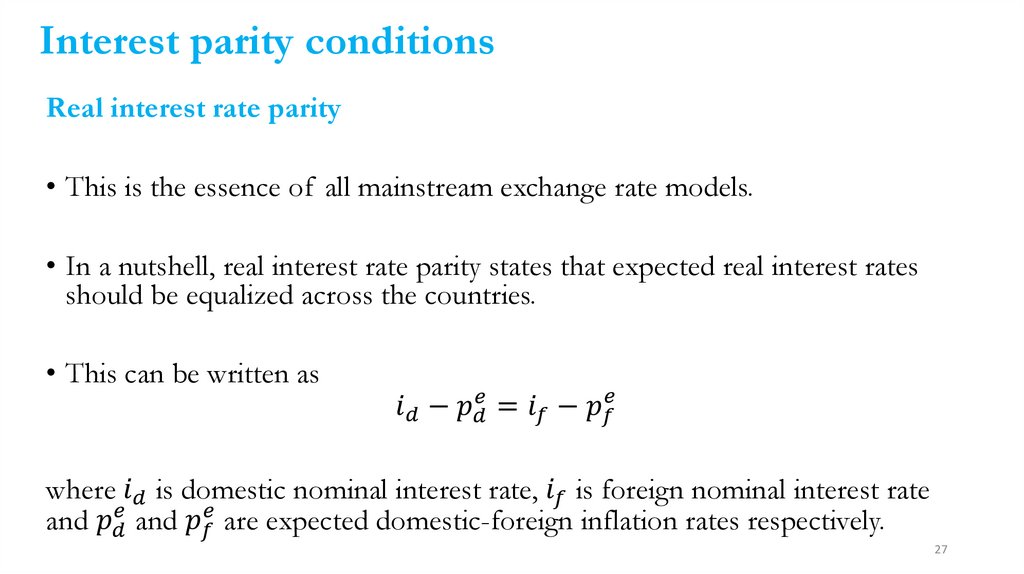

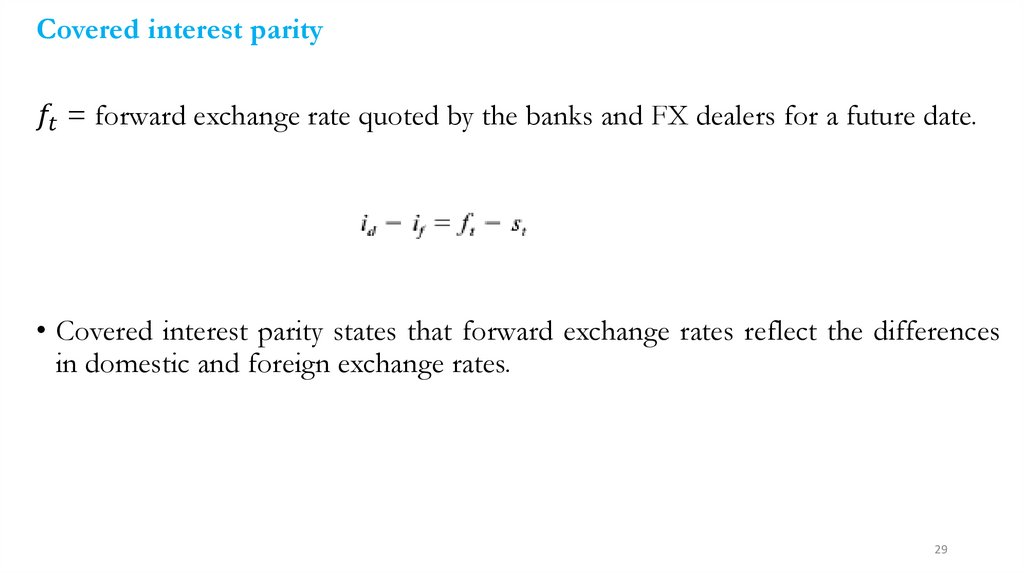

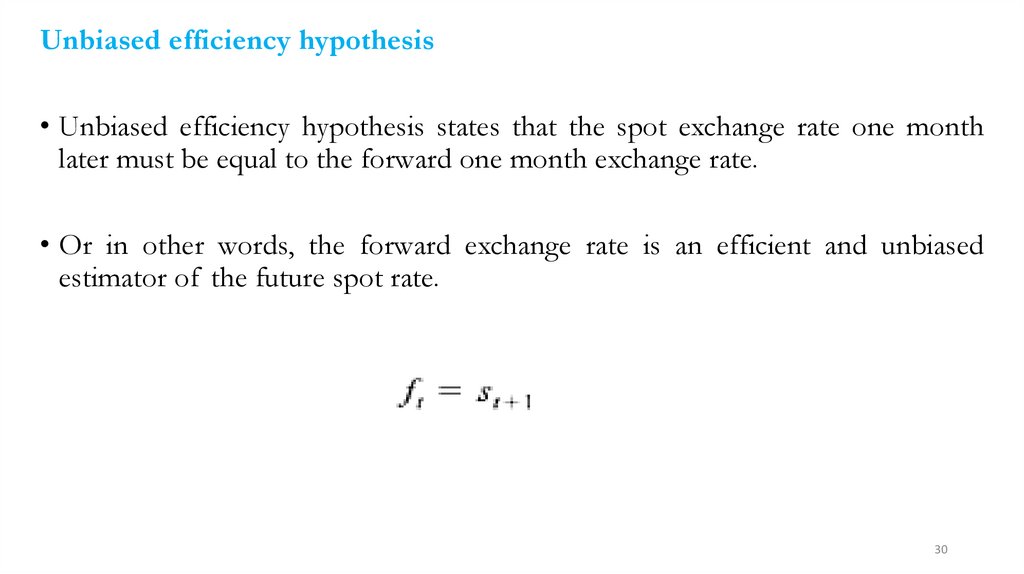

Interest parity conditionsReal interest rate parity

• This is the essence of all mainstream exchange rate models.

• In a nutshell, real interest rate parity states that expected real interest rates

should be equalized across the countries.

• This can be written as