mathematics

mathematicsSimilar presentations:

")

")

")

")

")

")

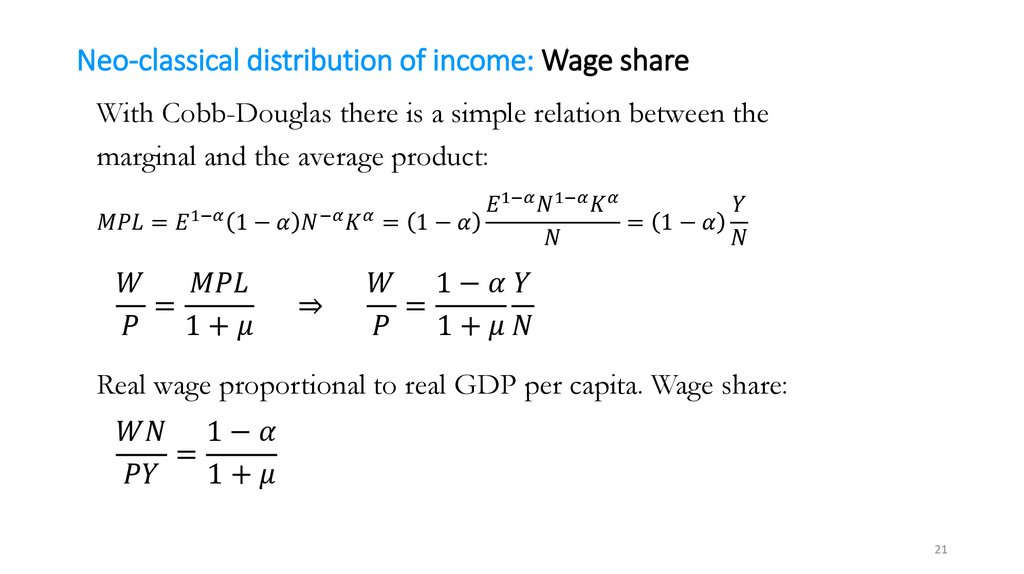

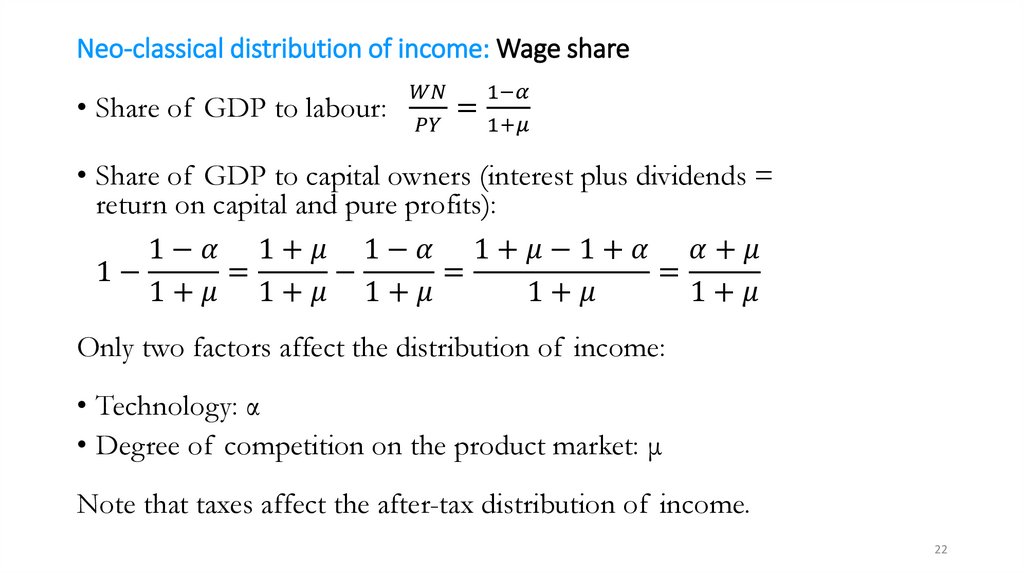

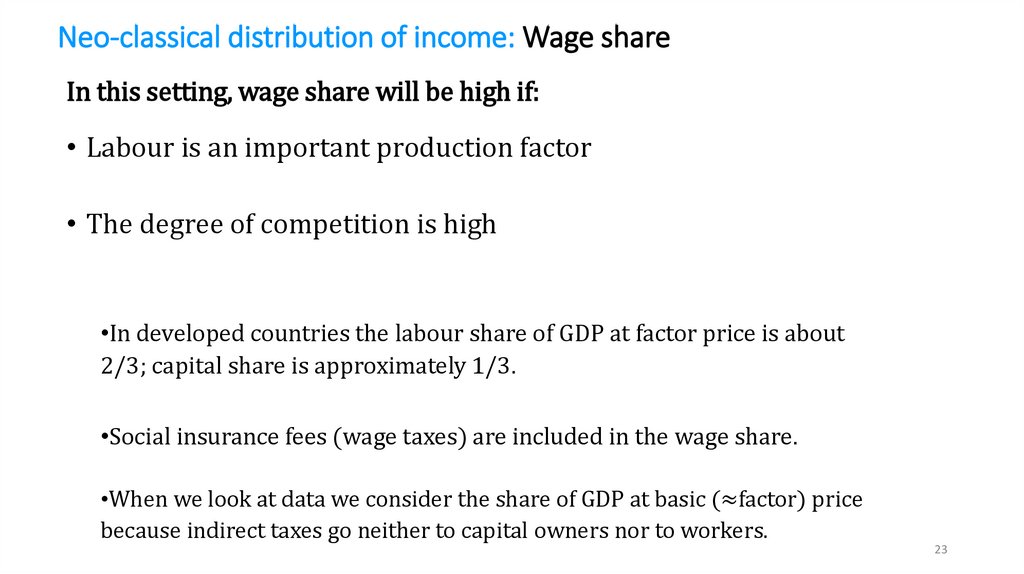

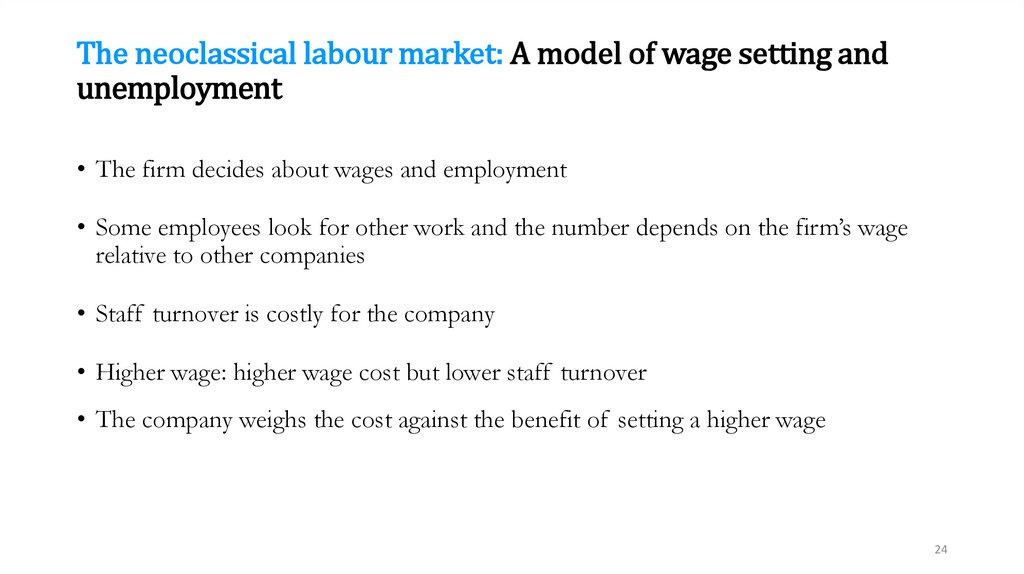

Neoclassical Theory of Production and Distribution of Income. Intermediate Macroeconomics

1.

EC 224Intermediate Macroeconomics

Neoclassical Theory of Production and

Distribution of Income

Gottfries, Chapters 2 and 6

2.

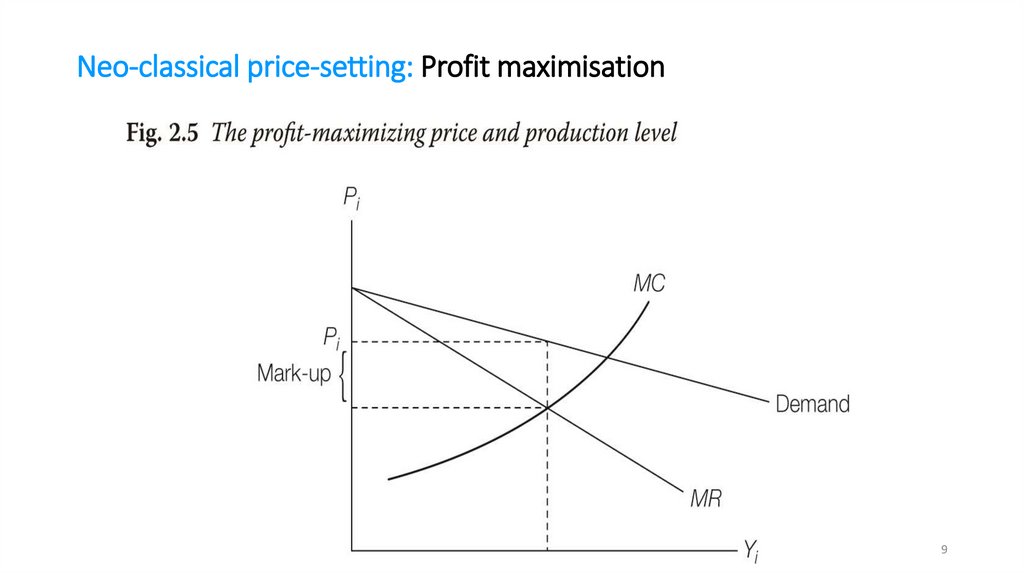

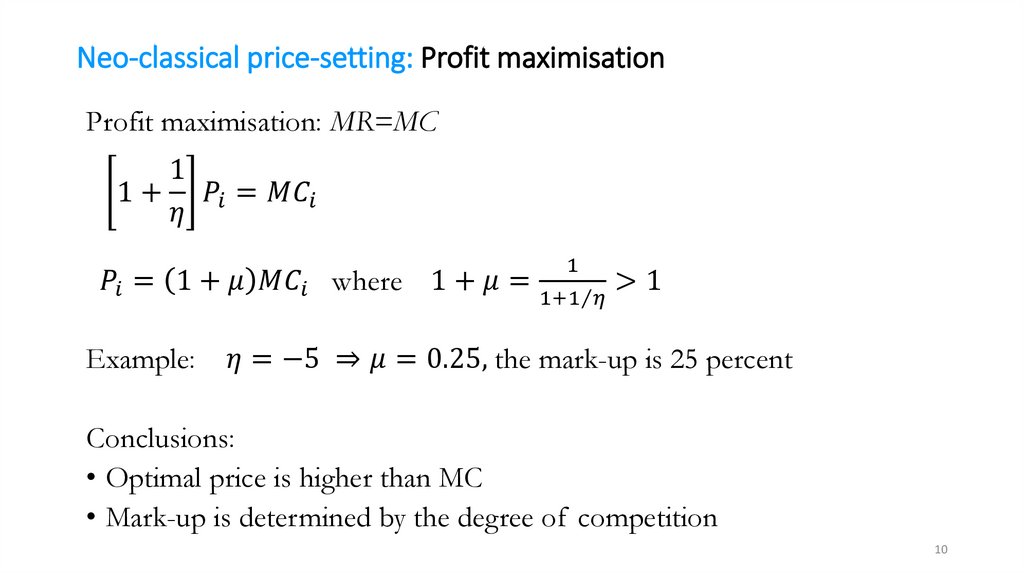

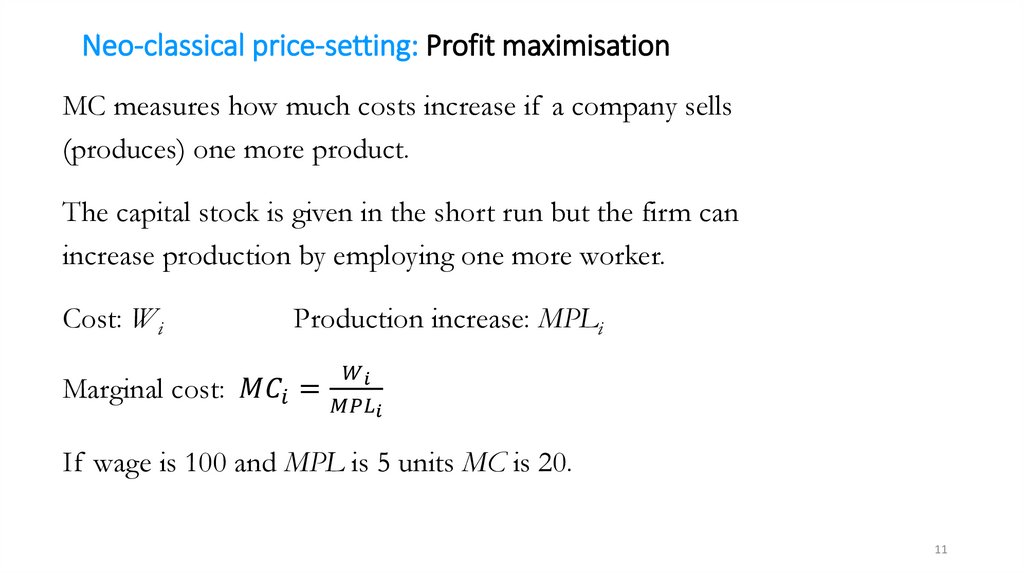

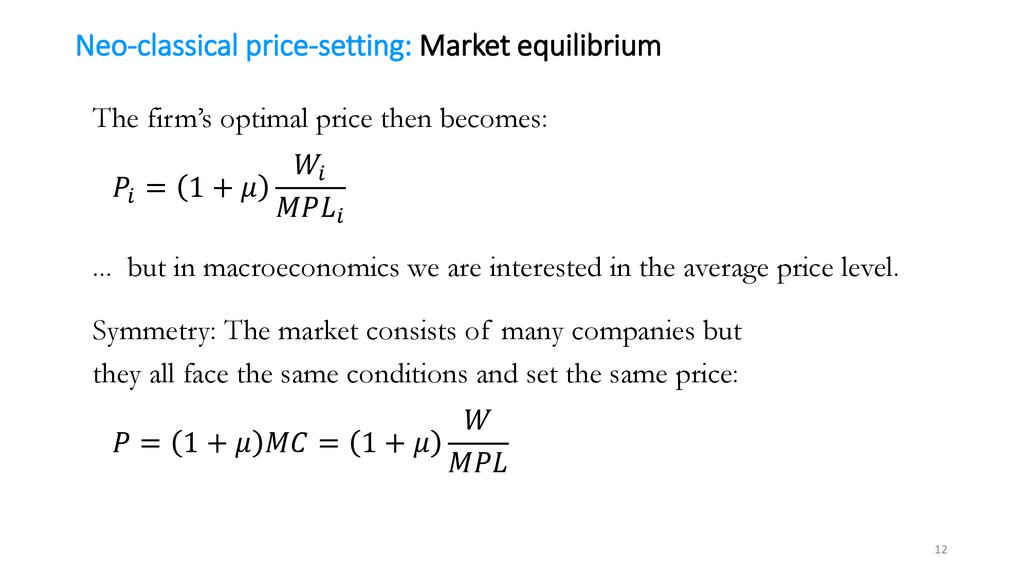

Neo-classical price-setting: IntroductionPerfect competition:

Firms produce identical goods and they can sell everything they produce at the

market price

Monopolistic competition:

Firms produce goods that are similar but not identical

A firm can set its own price and sales depend on the price A higher price will

reduce sales

In both cases: many firms – no ‘strategic’ interaction (no tacit collusion /

cartels /price wars)

2

3.

Neo-classical price-setting: DemandWe study a company named i – one of many companies in the

economy.

• How much will the company produce and sell?

• What price will the company set?

These two decisions are really just one because the company must choose

a point on the demand curve

3

4.

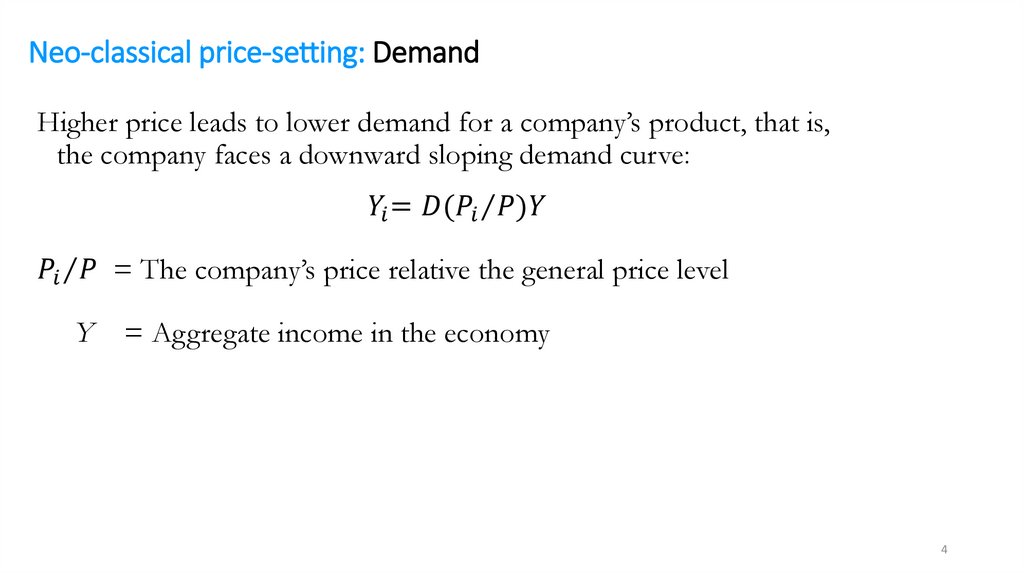

Neo-classical price-setting: DemandHigher price leads to lower demand for a company’s product, that is,

the company faces a downward sloping demand curve: