finance

financeSimilar presentations:

")

International sceintific and expert conference 2

1. INTERNATIONAL SCEINTIFIC AND EXPERT CONFERENCE Economic Development and Competitiveness of European Countries: Achievements –

NOVI SAD SCHOOL OF BUSINESSINTERNATIONAL SCEINTIFIC AND EXPERT CONFERENCE

Economic Development and Competitiveness of European Countries:

Achievements – Challenges – Opportunities

FROM THE GEORGE SIMMEL'S

"PHILOSOPHY OF MONEY"

TO THE CHARLES SPRAGUE'S

«PHILOSOPHY OF ACCOUNTS»

Pavel Baranov

Alexander Shaposhnikov

October 3-5, 2018

Novi Sad, Republic of Serbia

2.

Initial theses• The financial statements as the result of

accounting procedures are the main source of

information for decision-making by subjects of

market economy.

• In the conditions of dynamic development of

the economic relations and digitalization of

market economy traditional accounting faces

serious calls.

3.

Illustration of Initial thesesWeakness of the

modern

fundamental

philosophical

bases of

accounting

Problems of

ensuring

reliability of

financial

statements

Growth of

information risk

in decisionmaking by users

of financial

statement

4.

Research hypothesis:• The appeal to historical heritage of scientists

and integration of philosophical and economic

views are capable to lift the theory and

practice of accounting to qualitatively new

level.

5.

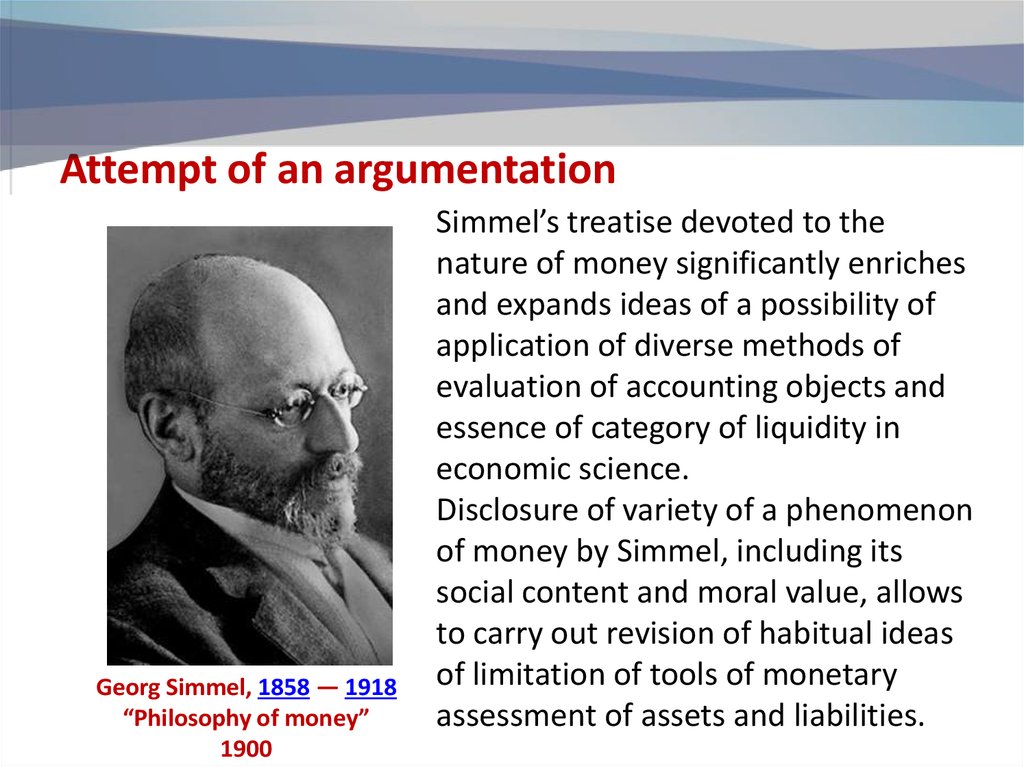

Attempt of an argumentationGeorg Simmel, 1858 — 1918

“Philosophy of money”

1900

Charles Sprague, 1842 – 1912

“Philosophy of accounts”

1907

6.

Attempt of an argumentationGeorg Simmel, 1858 — 1918

“Philosophy of money”

1900

Simmel’s treatise devoted to the

nature of money significantly enriches

and expands ideas of a possibility of

application of diverse methods of

evaluation of accounting objects and

essence of category of liquidity in

economic science.

Disclosure of variety of a phenomenon

of money by Simmel, including its

social content and moral value, allows

to carry out revision of habitual ideas

of limitation of tools of monetary

assessment of assets and liabilities.

7.

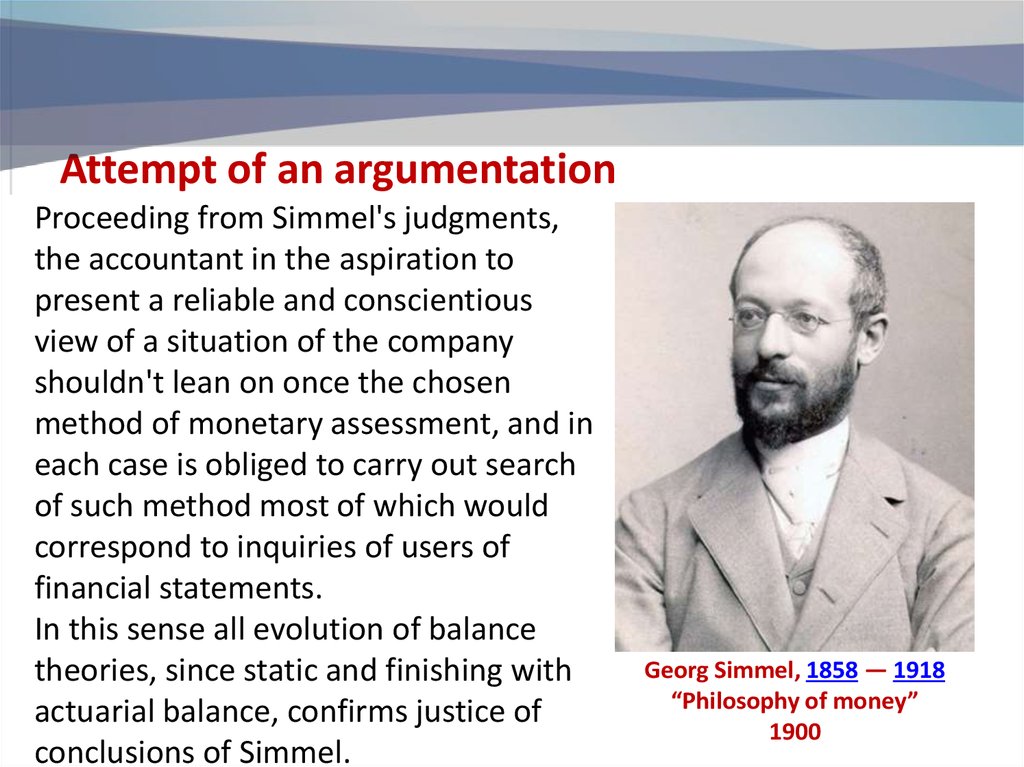

Attempt of an argumentationProceeding from Simmel's judgments,

the accountant in the aspiration to

present a reliable and conscientious

view of a situation of the company

shouldn't lean on once the chosen

method of monetary assessment, and in

each case is obliged to carry out search

of such method most of which would

correspond to inquiries of users of

financial statements.

In this sense all evolution of balance

theories, since static and finishing with

actuarial balance, confirms justice of

conclusions of Simmel.

Georg Simmel, 1858 — 1918

“Philosophy of money”

1900

8.

Attempt of an argumentationPhilosophical Simmel’s platform for

money role in economic relations is very

close to the Charles Sprague’s ideas of

account construction and form. Sprague’s

point of view on the priority of law basis

of economic transactions can’t be realized

without application of money evaluation

principle.

Sprague’s vision of the nature of accounts

is examined through the prism of

transformation of assets and loans as a

unique process of circulation of the rights

and obligations.

Charles Sprague, 1842 – 1912

“Philosophy of accounts”

1907

9.

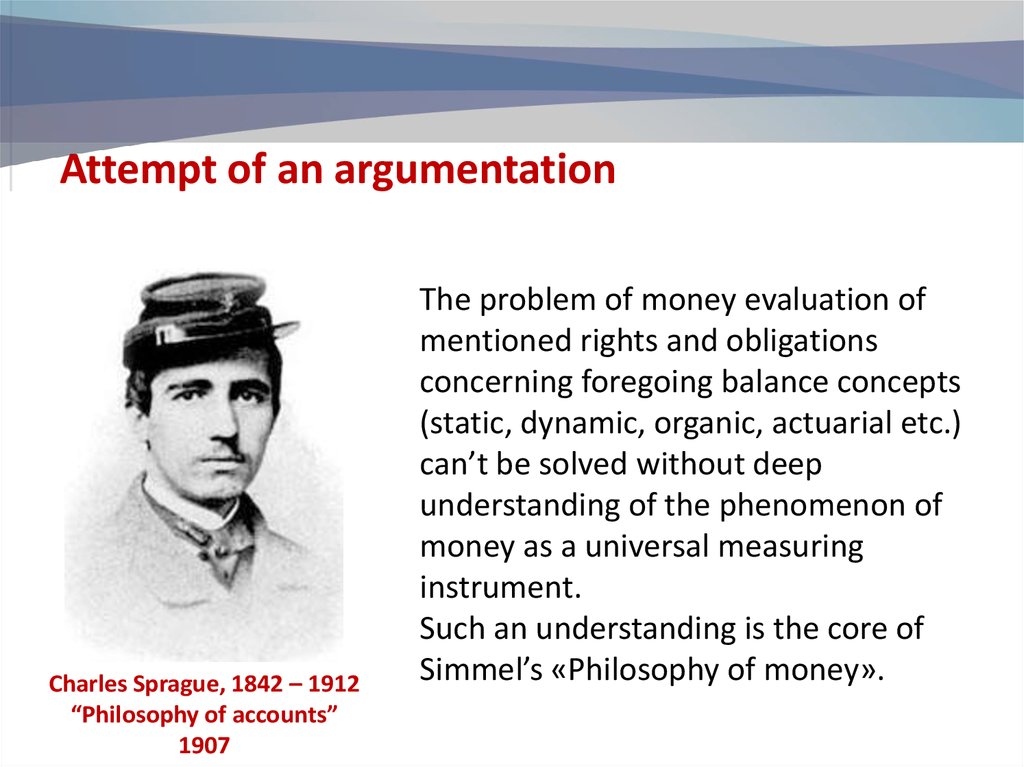

Attempt of an argumentationCharles Sprague, 1842 – 1912

“Philosophy of accounts”

1907

The problem of money evaluation of

mentioned rights and obligations

concerning foregoing balance concepts

(static, dynamic, organic, actuarial etc.)

can’t be solved without deep

understanding of the phenomenon of

money as a universal measuring

instrument.

Such an understanding is the core of

Simmel’s «Philosophy of money».

10.

IMPLICATIONS AND CONTRIBUTIONS• Conclusions based on conducted research have a

wide perspective against the background of

digitalization of accounting and emergence of

new accounting subjects such as digital assets,

cryptocurrencies, blockchain transactions etc.

Regeneration of economic relations is forming

demand for new approach to economic

modelling in terms of accounting system.

• This demand is new in its nature and it can’t be

satisfied without reconsideration of meaning of

the money and widening mission of modern

accounting.

11.

KEY RECOMMENDATIONS• Creation and development of new accounting

and financial reporting methods which is

inevitable in transforming economic conditions

must be based on interdisciplinary platform

reflecting specific features of accounting as

socially constructed science and socially oriented

activity. Moreover, this platform must involve

current apperception of money in the vision of

economic agents who generate the principles and

mechanisms for evaluation of assets, loans and

facts of enterprises life.

12.

Thank You for attention!!!Pavel Baranov, Doctor of Economics, Head of

information-analytical support and accounting

department,

Alexander Shaposhnikov, Doctor of Economics,

Professor of information-analytical support and

accounting department,

Novosibirsk state university for economics and

management, Novosibirsk, Russian Federation

email: bpavel1974@yandex.ru

www.nsuem.ru