Similar presentations:

High-Frequency Mini Ultrasound Probe for Aesthetic Medicine (2)

1.

MEDICAL DEVICE • NWFDRUSSIA

High-F requency Mini Ultras ound

P robe for Aes thetic Medicine

CMAS visualization • filler guidance • complication risk reduction

1

2

3

Real-time visualization of superficial anatomical

layers

Vessel mapping for safer injection

procedures

Complication management with ultrasound-guided

interventions

DAWEI Medical | Distribution in NWFD | Registration (RU) in progress | 2025

2.

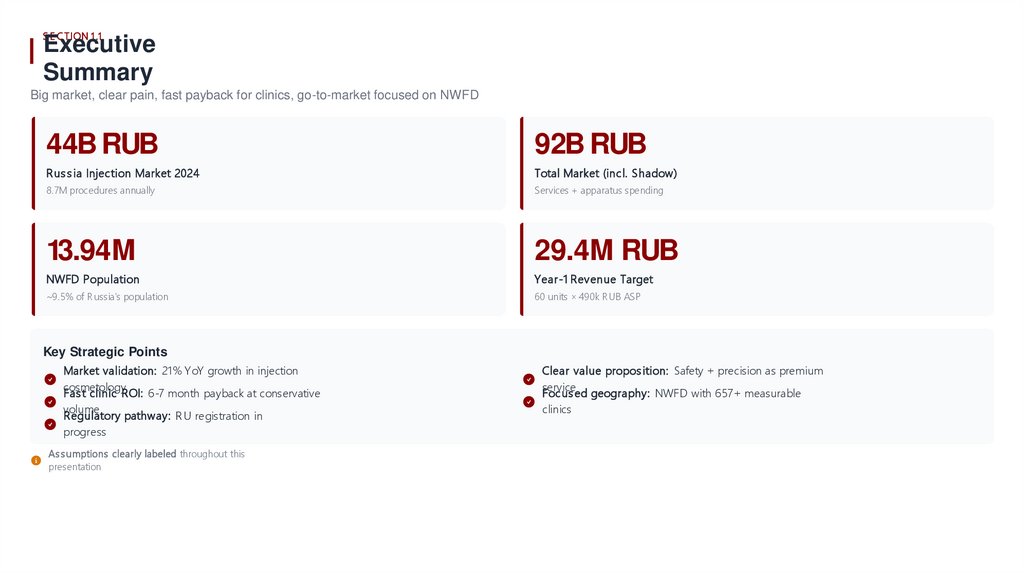

S E C T ION 1 .1Executive

Summary

Big market, clear pain, fast payback for clinics, go-to-market focused on NWFD

44B RUB

92B RUB

Rus s ia Injection Market 2024

Total Market (incl. Shadow)

8.7M procedures annually

Services + apparatus spending

13.94M

29.4M RUB

NWFD Population

Year-1 Revenue Target

~9.5% of R ussia's population

60 units × 490k R UB ASP

Key Strategic Points

Market validation: 21% YoY growth in injection

cosmetology

Fas t clinic ROI: 6-7 month payback at conservative

volume

Regulatory pathway: R U registration in

progress

As s umptions clearly labeled throughout this

presentation

Clear value propos ition: Safety + precision as premium

service

Focus ed geography: NWFD with 657+ measurable

clinics

3.

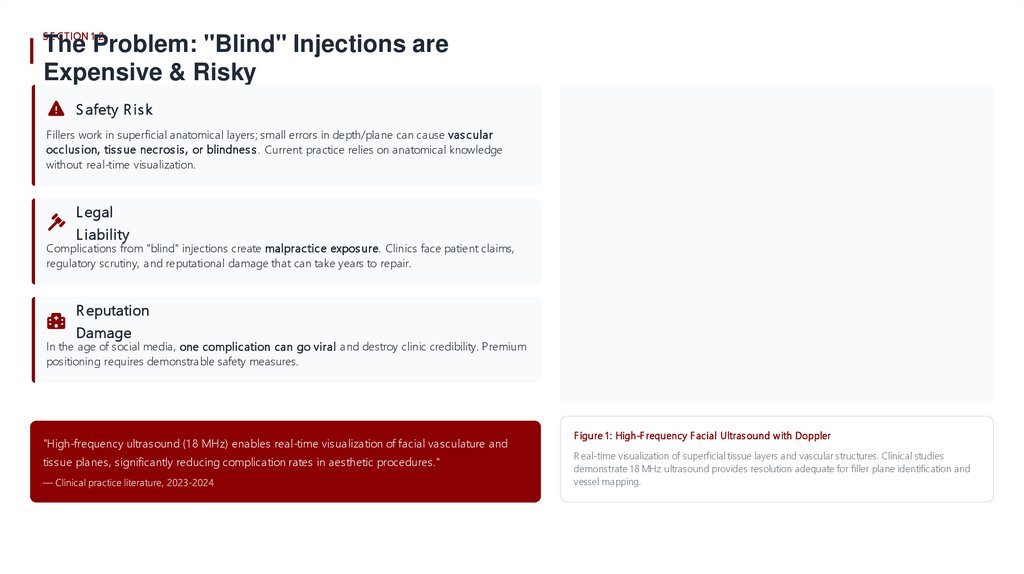

S E C T ION 1 .2The Problem: "Blind" Injections are

Expensive & Risky

S afety R is k

Fillers work in superficial anatomical layers; small errors in depth/plane can cause vas cular

occlus ion, tis s ue necros is , or blindnes s . Current practice relies on anatomical knowledge

without real-time visualization.

L egal

L iability

Complications from "blind" injections create malpractice expos ure. Clinics face patient claims,

regulatory scrutiny, and reputational damage that can take years to repair.

R eputation

Damage

In the age of social media, one complication can go viral and destroy clinic credibility. Premium

positioning requires demonstrable safety measures.

"High-frequency ultrasound (1 8 MHz) enables real-time visualization of facial vasculature and

tissue planes, significantly reducing complication rates in aesthetic procedures."

F igure 1 : High-F requency F acial Ultras ound with Doppler

R eal-time visualization of superficial tissue layers and vascular structures. Clinical studies

demonstrate 18 MHz ultrasound provides resolution adequate for filler plane identification and

vessel mapping.

4.

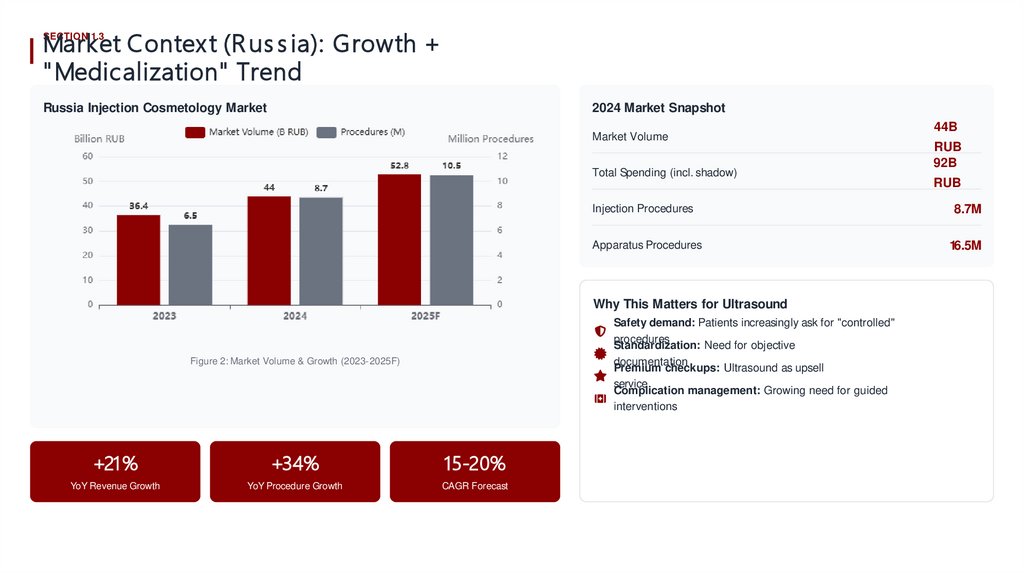

Market Contex t (R us s ia): Growth +" Medicalization" Trend

SECTION 1.3

Russia Injection Cosmetology Market

2024 Market Snapshot

Market Volume

Total Spending (incl. shadow)

+34%

15-20%

YoY Revenue Growth

YoY Procedure Growth

CAGR Forecast

RUB

8.7M

Apparatus Procedures

16.5M

Safety demand: Patients increasingly ask for "controlled"

procedures

Standardization: Need for objective

documentation

Premium checkups: Ultrasound as upsell

service

Complication management: Growing need for guided

interventions

+21%

RUB

92B

Injection Procedures

Why This Matters for Ultrasound

Figure 2: Market Volume & Growth (2023-2025F)

44B

5.

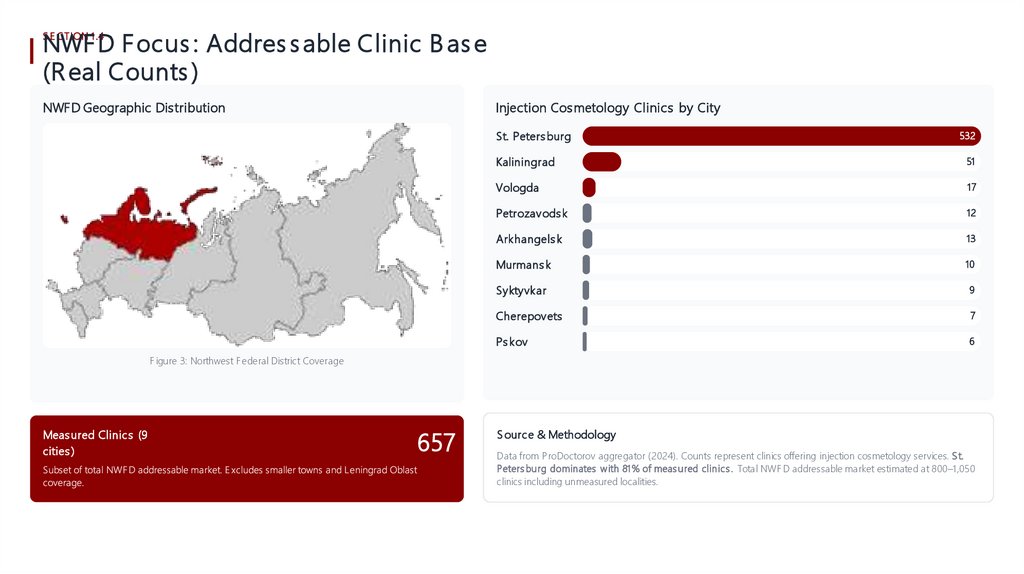

NWF D F ocus : Addres s able Clinic B as e(R eal Counts )

S E C T ION 1 .4

NWFD Geographic Dis tribution

Injection Cos metology Clinics by City

St. Peters burg

532

Kaliningrad

51

Vologda

17

Petrozavods k

12

Arkhangels k

13

Murmans k

10

Syktyvkar

9

Cherepovets

7

Ps kov

6

F igure 3: Northwest F ederal District Coverage

Meas ured Clinics (9

cities )

657

S ource & Methodology

Data from P roDoctorov aggregator (2024). Counts represent clinics offering injection cosmetology services. S t.

Peters burg dominates with 81% of meas ured clinics . Total NWF D addressable market estimated at 800–1 ,050

clinics including unmeasured localities.

6.

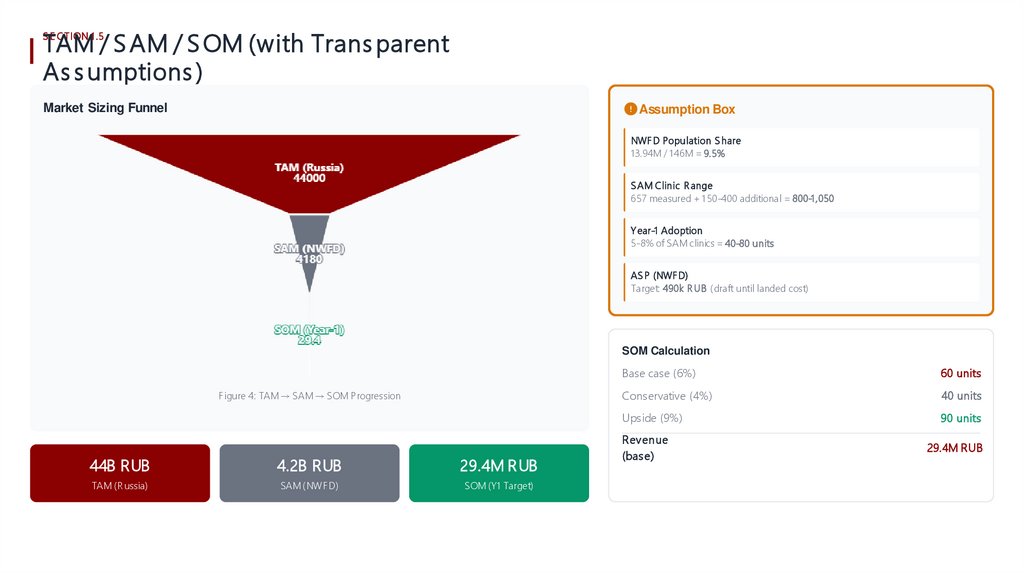

TAM / S AM / S OM (with Trans parentAs s umptions )

S E C T ION 1 .5

Market Sizing Funnel

Assumption Box

NWF D Population S hare

13.94M / 1 46M = 9.5%

S AM Clinic R ange

657 measured + 1 50-400 additional = 800-1 ,050

Y ear-1 Adoption

5-8% of S AM clinics = 40-80 units

AS P (NWF D)

Target: 490k R UB (draft until landed cost)

SOM Calculation

F igure 4: TAM → SAM → SOM Progression

44B RUB

4.2B RUB

29.4M RUB

TAM (R ussia)

SAM (NWF D)

SOM (Y1 Target)

Base case (6%)

60 units

Conservative (4%)

40 units

Upside (9%)

90 units

Revenue

(bas e)

29.4M RUB

7.

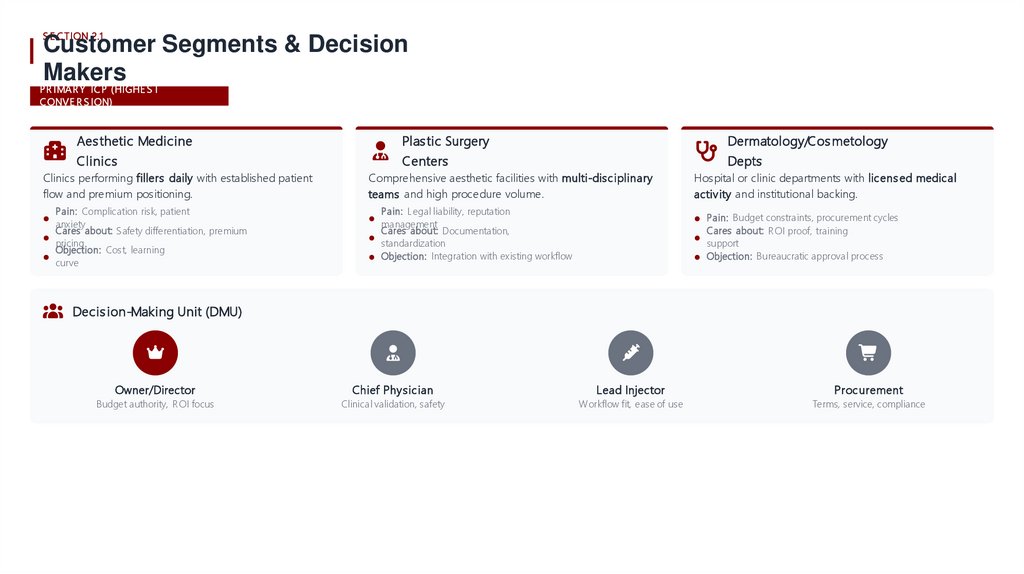

S E C T ION 2.1Customer Segments & Decision

Makers

PR IMA R Y IC P (HIGHE S T

C ONVE R S ION)

Aes thetic Medicine

Clinics

Clinics performing fillers daily with established patient

flow and premium positioning.

Pain: Complication risk, patient

anxiety

Cares about: S afety differentiation, premium

pricing

Objection: Cost, learning

curve

Plas tic Surgery

Dermatology/Cos metology

Centers

Depts

Comprehensive aesthetic facilities with multi-disciplinary

teams and high procedure volume.

Pain: Legal liability, reputation

management

Cares about: Documentation,

standardization

Objection: Integration with existing workflow

Hospital or clinic departments with licens ed medical

activity and institutional backing.

Pain: Budget constraints, procurement cycles

Cares about: R OI proof, training

support

Objection: Bureaucratic approval process

Decis ion-Making Unit (DMU)

Owner/Director

Chief Physician

Lead Injector

Procurement

Budget authority, R OI focus

Clinical validation, safety

Workflow fit, ease of use

Terms, service, compliance

8.

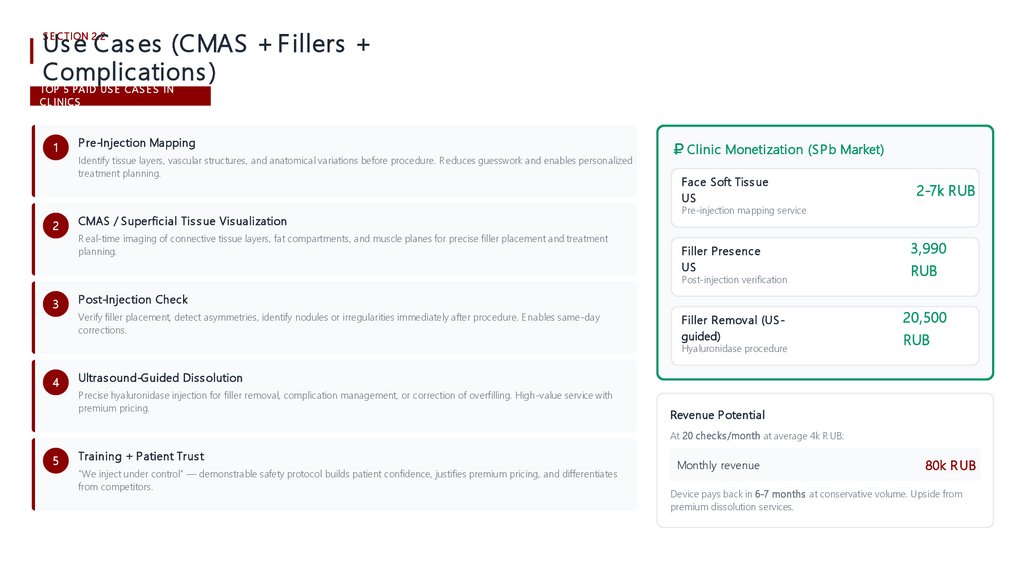

Us e Cas es (CMAS + F illers +Complications )

S E C T ION 2.2

TOP 5 PA ID US E C A S E S IN

C L INIC S

1

2

P re-Injection Mapping

Identify tissue layers, vascular structures, and anatomical variations before procedure. R educes guesswork and enables personalized

treatment planning.

CMAS / Superficial Tis s ue Vis ualization

R eal-time imaging of connective tissue layers, fat compartments, and muscle planes for precise filler placement and treatment

planning.

Clinic Monetization (S Pb Market)

Face Soft Tiss ue

US

Pre-injection mapping service

Filler Pres ence

US

3,990

Filler Removal (US guided)

20,500

Post-injection verification

3

RUB

P ost-Injection Check

Verify filler placement, detect asymmetries, identify nodules or irregularities immediately after procedure. E nables same-day

corrections.

Hyaluronidase procedure

4

2-7k RUB

RUB

Ultras ound-Guided Diss olution

Precise hyaluronidase injection for filler removal, complication management, or correction of overfilling. High-value service with

premium pricing.

Revenue P otential

At 20 checks /month at average 4k R UB:

5

Training + P atient Trus t

"We inject under control" — demonstrable safety protocol builds patient confidence, justifies premium pricing, and differentiates

from competitors.

Monthly revenue

80k R UB

Device pays back in 6-7 months at conservative volume. Upside from

premium dissolution services.

9.

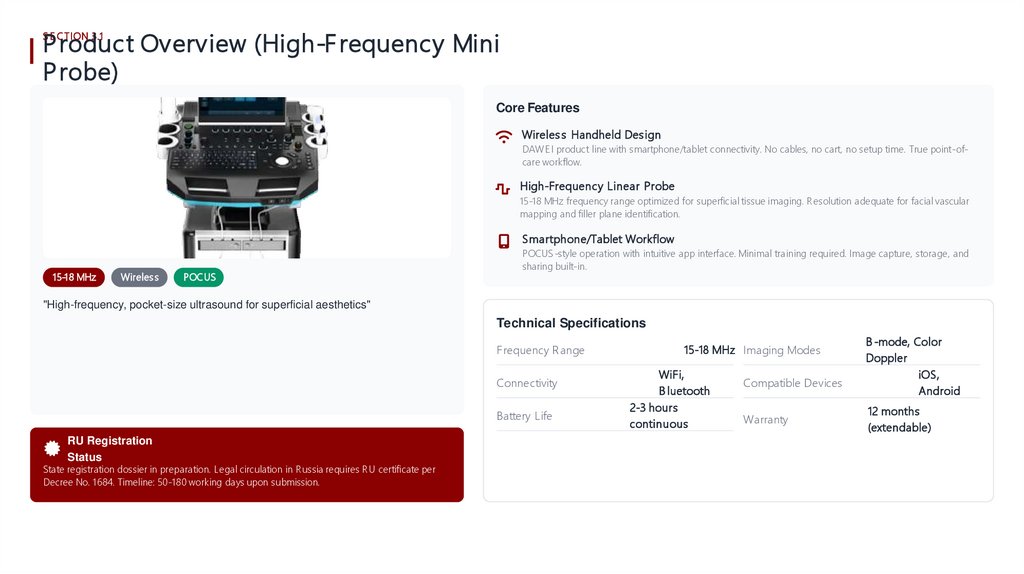

P roduct Overview (High-F requency MiniP robe)

S E C T ION 3.1

Core Features

Wireles s Handheld Des ign

DAWE I product line with smartphone/tablet connectivity. No cables, no cart, no setup time. True point-ofcare workflow.

High-Frequency Linear Probe

15-18 MHz frequency range optimized for superficial tissue imaging. R esolution adequate for facial vascular

mapping and filler plane identification.

Smartphone/Tablet Workflow

15-18 MHz

Wireles s

POCUS

POCUS -style operation with intuitive app interface. Minimal training required. Image capture, storage, and

sharing built-in.

"High-frequency, pocket-size ultrasound for superficial aesthetics"

Technical Specifications

Frequency R ange

Connectivity

Battery Life

RU Registration

Status

State registration dossier in preparation. Legal circulation in R ussia requires R U certificate per

Decree No. 1684. Timeline: 50-180 working days upon submission.

15-18 MHz Imaging Modes

WiFi,

B luetooth

2-3 hours

continuous

Compatible Devices

Warranty

B -mode, Color

Doppler

iOS,

Android

12 months

(extendable)

10.

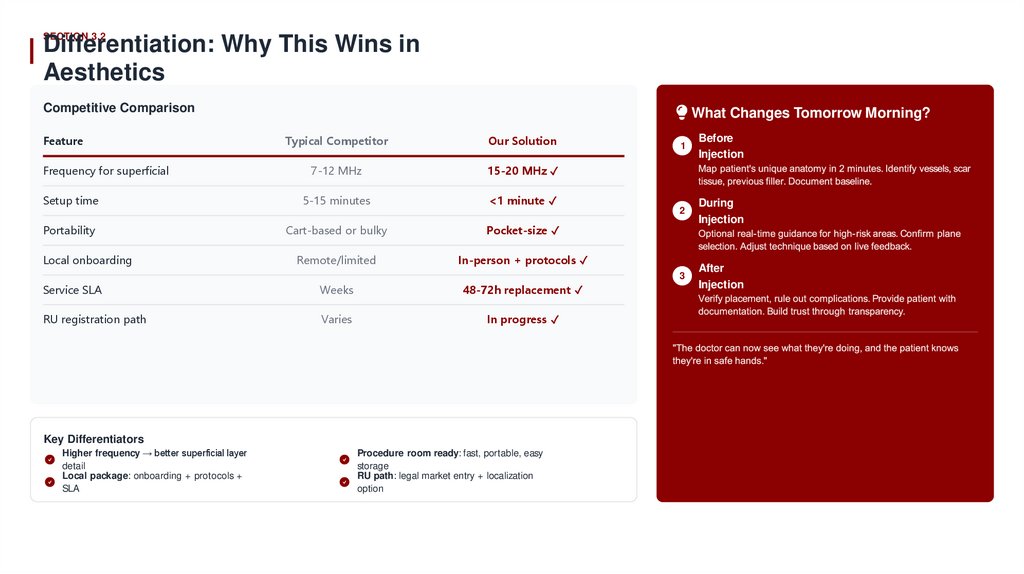

SECTION 3.2Differentiation: Why This Wins in

Aesthetics

Competitive Comparison

Feature

What Changes Tomorrow Morning?

Typical Competitor

Our Solution

7-12 MHz

15-20 MHz ✓

Setup time

5-15 minutes

<1 minute ✓

Portability

Cart-based or bulky

Pocket-size ✓

Remote/limited

In-person + protocols ✓

Frequency for superficial

Local onboarding

Service SLA

Weeks

48-72h replacement ✓

RU registration path

Varies

In progress ✓

Key Differentiators

Higher frequency → better superficial layer

detail

Local package: onboarding + protocols +

SLA

Procedure room ready: fast, portable, easy

storage

RU path: legal market entry + localization

option

1

Before

Injection

2

During

Injection

3

After

Injection

11.

S E C T ION 3.3Competitive Landscape (Pricing Anchor +

Positioning)

Our Positioning

High aes thetic quality at optimized total

cos t.

Positioning Matrix

Target ASP 490k R UB (~$5,400) with local service, training, and support

included. No recurring membership fees.

Competitive Advantages

F requency optimized for facial aesthetics (15-18

MHz)

L ocal pres ence in NWF D with R ussian-language

support

Integrated package: device + training + protocols +

service

F as t replacement program (48-72h) minimizes

downtime

R egulatory pathway for legal R ussian market

entry

F igure 5: Aesthetic Superficial Quality vs. Total Cost of Ownership

Competitor Price Reference

CL

Clarius L20 HD

$5,395 + $595/year membership

Listed price

Manufacturer

store

S ource: Competitor pricing from manufacturer website (Dec 2024).

Subject to change.

12.

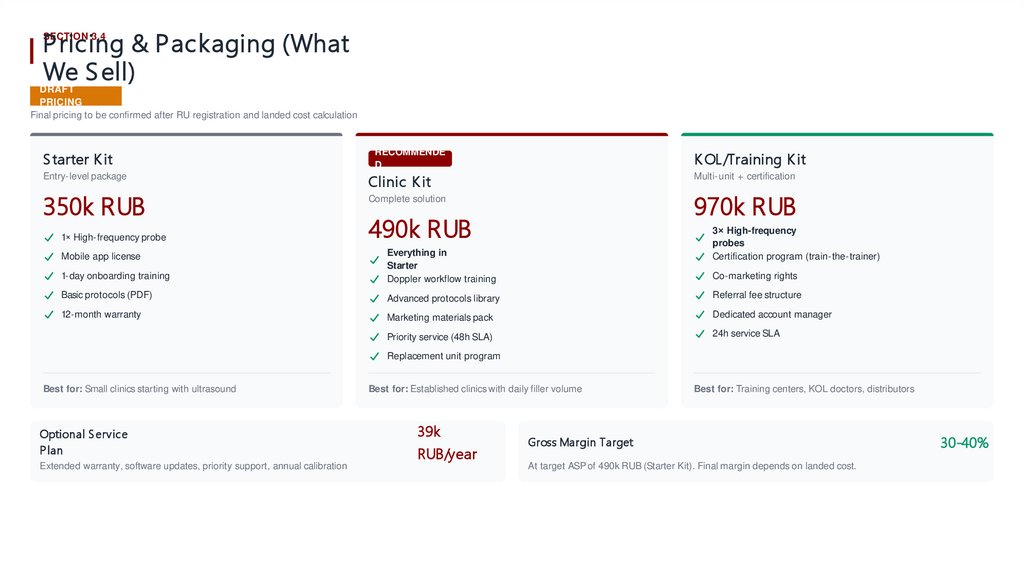

P ricing & P ackaging (WhatWe S ell)

SECTION 3.4

DRAFT

PRICING

Final pricing to be confirmed after RU registration and landed cost calculation

S tarter K it

RECOMMENDE

D

K OL/Training K it

Entry-level package

Clinic K it

Multi-unit + certification

350k RUB

1× High-frequency probe

970k RUB

Complete solution

490k RUB

3× High-frequency

probes

Certification program (train-the-trainer)

1-day onboarding training

Everything in

Starter

Doppler workflow training

Basic protocols (PDF)

Advanced protocols library

Referral fee structure

12-month warranty

Marketing materials pack

Dedicated account manager

Priority service (48h SLA)

24h service SLA

Mobile app license

Co-marketing rights

Replacement unit program

Best for: Small clinics starting with ultrasound

Optional S ervice

P lan

Extended warranty, software updates, priority support, annual calibration

Best for: Established clinics with daily filler volume

39k

RUB/year

Best for: Training centers, KOL doctors, distributors

Gross Margin Target

At target ASP of 490k RUB (Starter Kit). Final margin depends on landed cost.

30-40%

13.

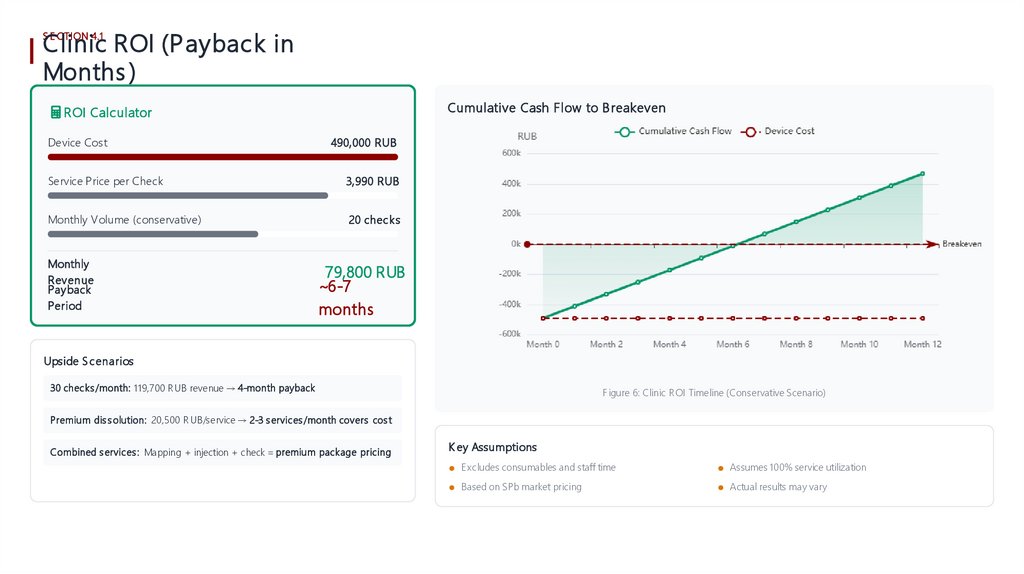

Clinic ROI (P ayback inMonths )

S E C T ION 4.1

Cumulative Cash Flow to B reakeven

ROI Calculator

Device Cost

490,000 RUB

Service Price per Check

3,990 RUB

Monthly Volume (conservative)

20 checks

Monthly

Revenue

Payback

Period

79,800 RUB

~6-7

months

Upside S cenarios

30 checks /month: 119,700 R UB revenue → 4-month payback

F igure 6: Clinic R OI Timeline (Conservative Scenario)

Premium dis s olution: 20,500 R UB/service → 2-3 s ervices /month covers cos t

Combined s ervices : Mapping + injection + check = premium package pricing

K ey Assumptions

E xcludes consumables and staff time

Assumes 100% service utilization

Based on SPb market pricing

Actual results may vary

14.

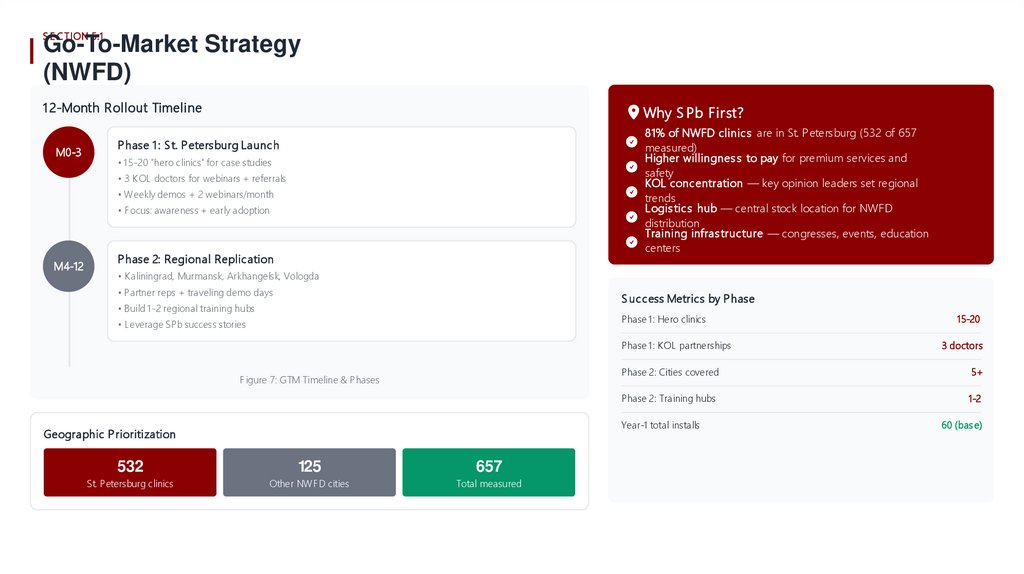

S E C T ION 5.1Go-To-Market Strategy

(NWFD)

1 2-Month Rollout Timeline

M0-3

Why S Pb First?

81% of NWFD clinics are in St. Petersburg (532 of 657

measured)

Higher willingnes s to pay for premium services and

safety

KOL concentration — key opinion leaders set regional

trends

Logis tics hub — central stock location for NWFD

distribution

Training infras tructure — congresses, events, education

centers

P hase 1 : S t. P etersburg Launch

• 1 5-20 "hero clinics" for case studies

• 3 K OL doctors for webinars + referrals

• Weekly demos + 2 webinars/month

• F ocus: awareness + early adoption

M4-12

P hase 2: Regional Replication

• K aliningrad, Murmansk, Arkhangelsk, Vologda

• Partner reps + traveling demo days

S uccess Metrics by P hase

• Build 1-2 regional training hubs

Phase 1: Hero clinics

• Leverage SPb success stories

Phase 1: K OL partnerships

F igure 7: GTM Timeline & P hases

532

125

657

St. Petersburg clinics

Other NWF D cities

Total measured

3 doctors

Phase 2: Cities covered

5+

Phase 2: Training hubs

1-2

Year-1 total installs

Geographic P rioritization

15-20

60 (bas e)

15.

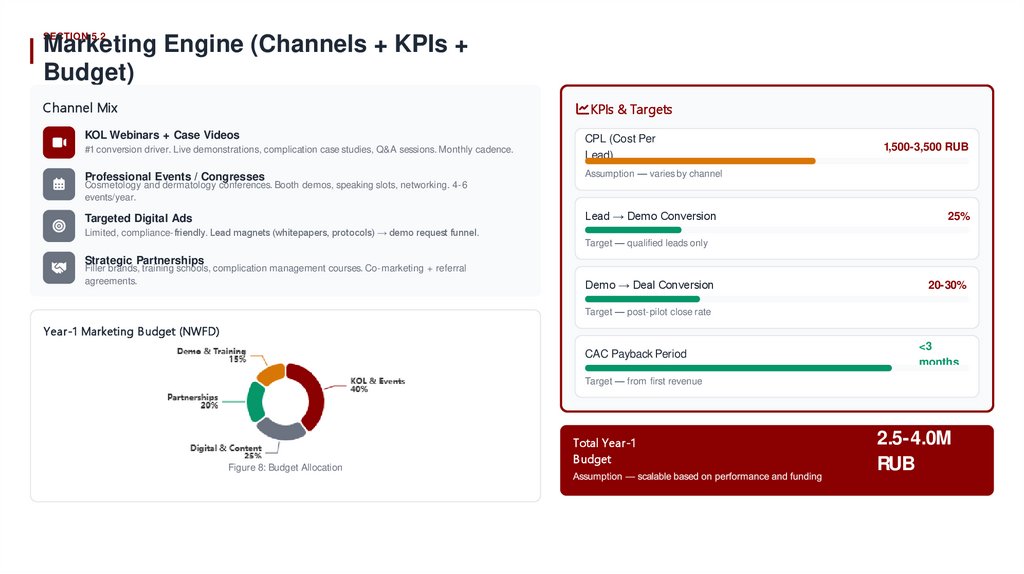

SECTION 5.2Marketing Engine (Channels + KPIs +

Budget)

Channel Mix

KPIs & Targets

KOL Webinars + Case Videos

#1 conversion driver. Live demonstrations, complication case studies, Q&A sessions. Monthly cadence.

CPL (Cost Per

Lead)

Professional Events / Congresses

Assumption — varies by channel

Targeted Digital Ads

Lead → Demo Conversion

1,500-3,500 RUB

Cosmetology and dermatology conferences. Booth demos, speaking slots, networking. 4-6

events/year.

Limited, compliance-friendly. Lead magnets (whitepapers, protocols) → demo request funnel.

25%

Target — qualified leads only

Strategic Partnerships

Filler brands, training schools, complication management courses. Co-marketing + referral

agreements.

Demo → Deal Conversion

20-30%

Target — post-pilot close rate

Year-1 Marketing B udget (NWFD)

CAC Payback Period

<3

months

Target — from first revenue

Figure 8: Budget Allocation

Total Year-1

B udget

2.5-4.0M

RUB

16.

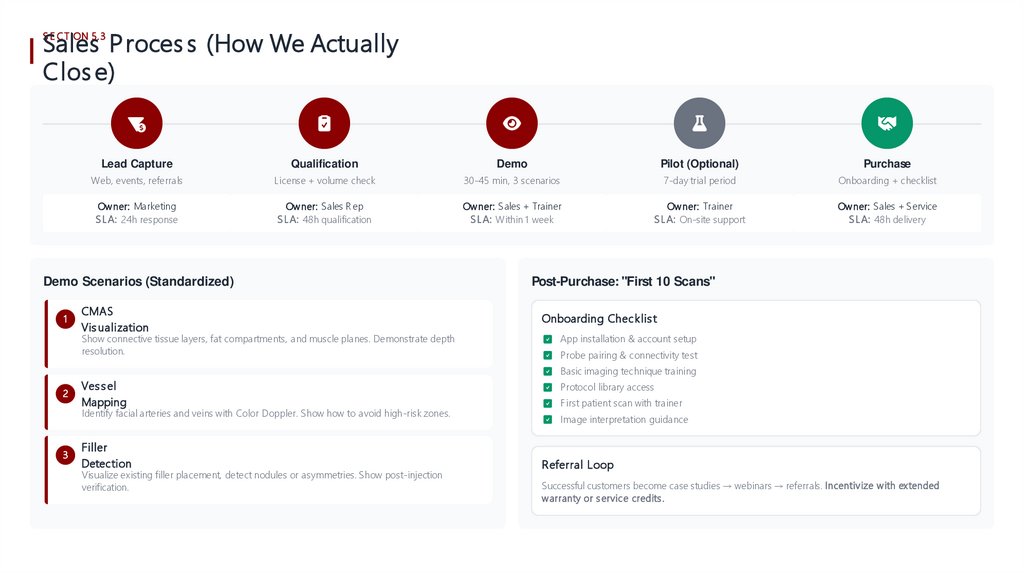

Sales P roces s (How We ActuallyClos e)

S E C T ION 5.3

Lead Capture

Qualification

Demo

Pilot (Optional)

Purchase

Web, events, referrals

License + volume check

30-45 min, 3 scenarios

7-day trial period

Onboarding + checklist

Owner: Marketing

S L A: 24h response

Owner: S ales R ep

S L A: 48h qualification

Owner: S ales + Trainer

S L A: Within 1 week

Owner: Trainer

S L A: On-site support

Owner: S ales + S ervice

S L A: 48h delivery

Demo Scenarios (Standardized)

1

CMAS

Vis ualization

Show connective tissue layers, fat compartments, and muscle planes. Demonstrate depth

resolution.

Post-Purchase: "First 10 Scans"

Onboarding Checklis t

App installation & account setup

Probe pairing & connectivity test

Basic imaging technique training

2

Ves s el

Mapping

Identify facial arteries and veins with Color Doppler. Show how to avoid high-risk zones.

3

Filler

Detection

Visualize existing filler placement, detect nodules or asymmetries. Show post-injection

verification.

Protocol library access

F irst patient scan with trainer

Image interpretation guidance

Referral Loop

Successful customers become case studies → webinars → referrals. Incentivize with extended

warranty or s ervice credits .

17.

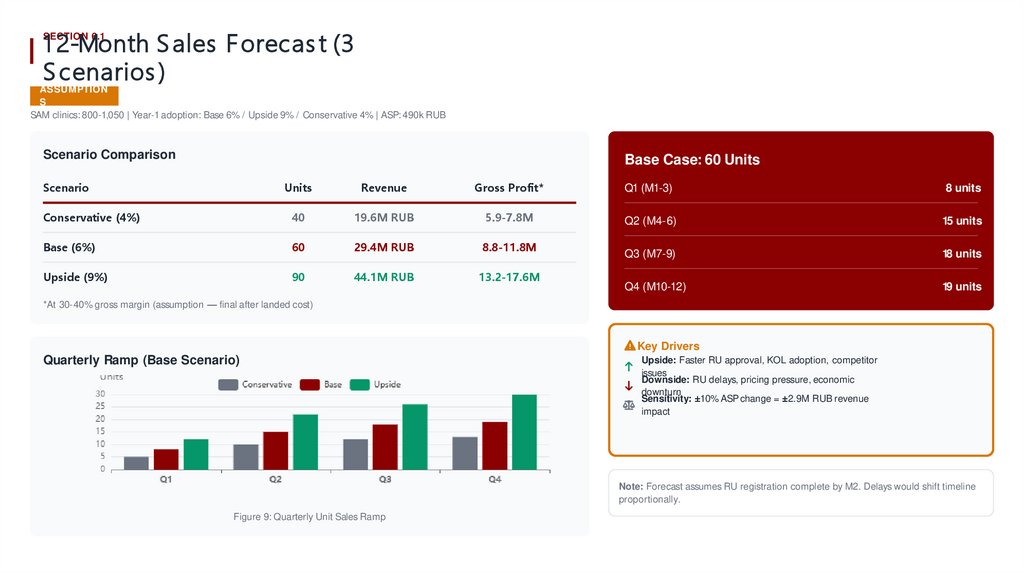

1 2-Month S ales F orecas t (3S cenarios )

SECTION 6.1

ASSUMPTION

S

SAM clinics: 800-1,050 | Year-1 adoption: Base 6% / Upside 9% / Conservative 4% | ASP: 490k RUB

Scenario Comparison

Base Case: 60 Units

Scenario

Units

Revenue

Gross Profit*

Q1 (M1-3)

8 units

Conservative (4%)

40

19.6M RUB

5.9-7.8M

Q2 (M4-6)

15 units

Base (6%)

60

29.4M RUB

8.8-11.8M

Q3 (M7-9)

18 units

Upside (9%)

90

44.1M RUB

13.2-17.6M

Q4 (M10-12)

19 units

*At 30-40% gross margin (assumption — final after landed cost)

Key Drivers

Quarterly Ramp (Base Scenario)

Upside: Faster RU approval, KOL adoption, competitor

issues

Downside: RU delays, pricing pressure, economic

downturn

Sensitivity: ±10% ASP change = ±2.9M RUB revenue

impact

Note: Forecast assumes RU registration complete by M2. Delays would shift timeline

proportionally.

Figure 9: Quarterly Unit Sales Ramp

18.

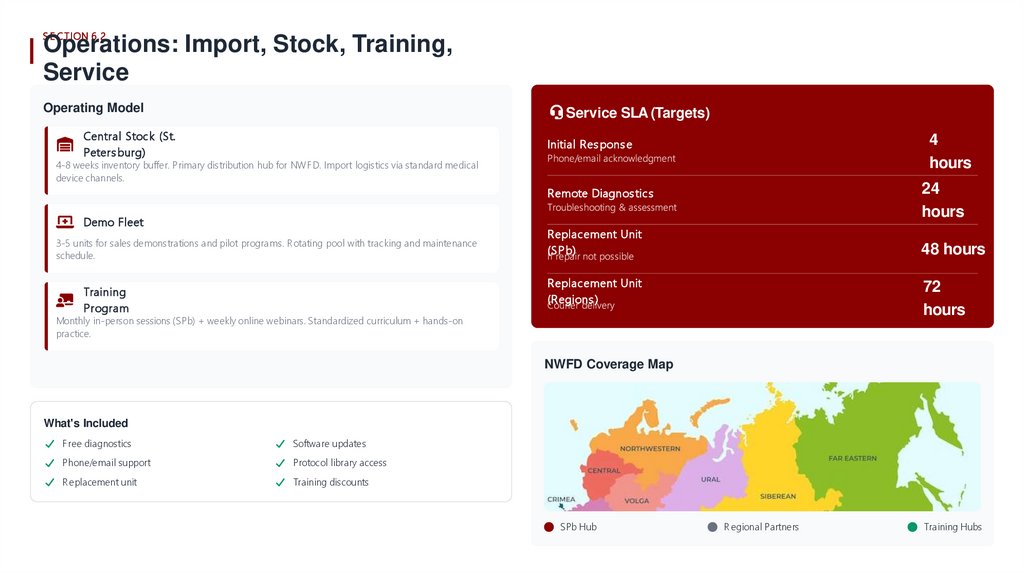

S E C T ION 6.2Operations: Import, Stock, Training,

Service

Operating Model

Service SLA (Targets)

Central Stock (St.

Peters burg)

Initial Res pons e

4

hours

Remote Diagnos tics

24

hours

4-8 weeks inventory buffer. Primary distribution hub for NWF D. Import logistics via standard medical

device channels.

Demo Fleet

3-5 units for sales demonstrations and pilot programs. R otating pool with tracking and maintenance

schedule.

Replacement Unit

(S Pb)

48 hours

Replacement Unit

(R egions )

Training

Program

72

hours

Monthly in-person sessions (SPb) + weekly online webinars. Standardized curriculum + hands-on

practice.

NWFD Coverage Map

What's Included

F ree diagnostics

Software updates

Phone/email support

Protocol library access

R eplacement unit

Training discounts

SPb Hub

R egional Partners

Training Hubs

19.

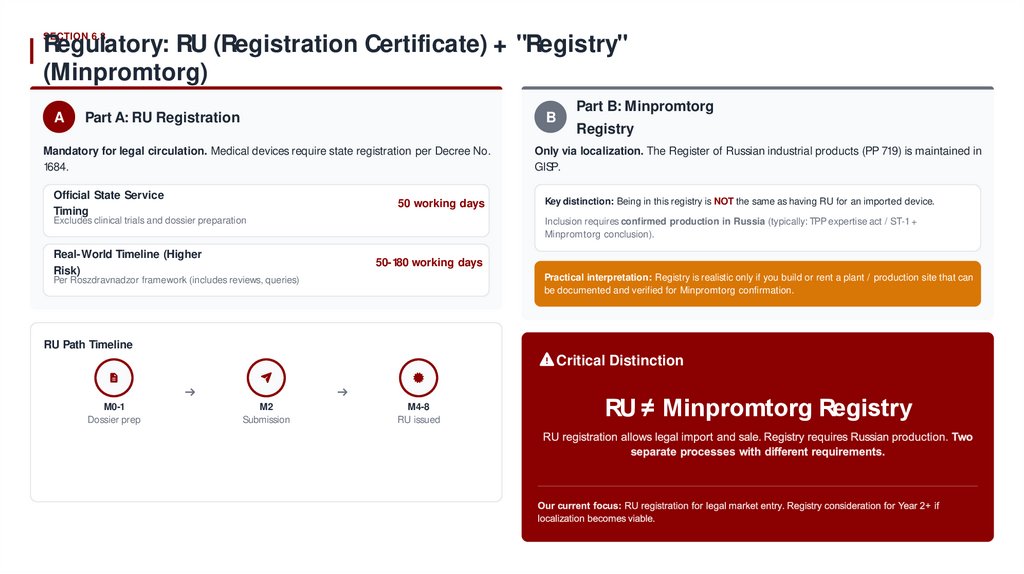

SECTION 6.3Regulatory: RU (Registration Certificate) + "Registry"

(Minpromtorg)

A

Part A: RU Registration

B

Mandatory for legal circulation. Medical devices require state registration per Decree No.

1684.

Official State Service

Timing

50 working days

Excludes clinical trials and dossier preparation

Real-World Timeline (Higher

Risk)

Part B: Minpromtorg

Registry

Only via localization. The Register of Russian industrial products (PP 719) is maintained in

GISP.

Key distinction: Being in this registry is NOT the same as having RU for an imported device.

Inclusion requires confirmed production in Russia (typically: TPP expertise act / ST-1 +

Minpromtorg conclusion).

50-180 working days

Practical interpretation: Registry is realistic only if you build or rent a plant / production site that can

be documented and verified for Minpromtorg confirmation.

Per Roszdravnadzor framework (includes reviews, queries)

RU Path Timeline

Critical Distinction

M0-1

Dossier prep

M2

Submission

M4-8

RU issued

RU ≠ Minpromtorg Registry

20.

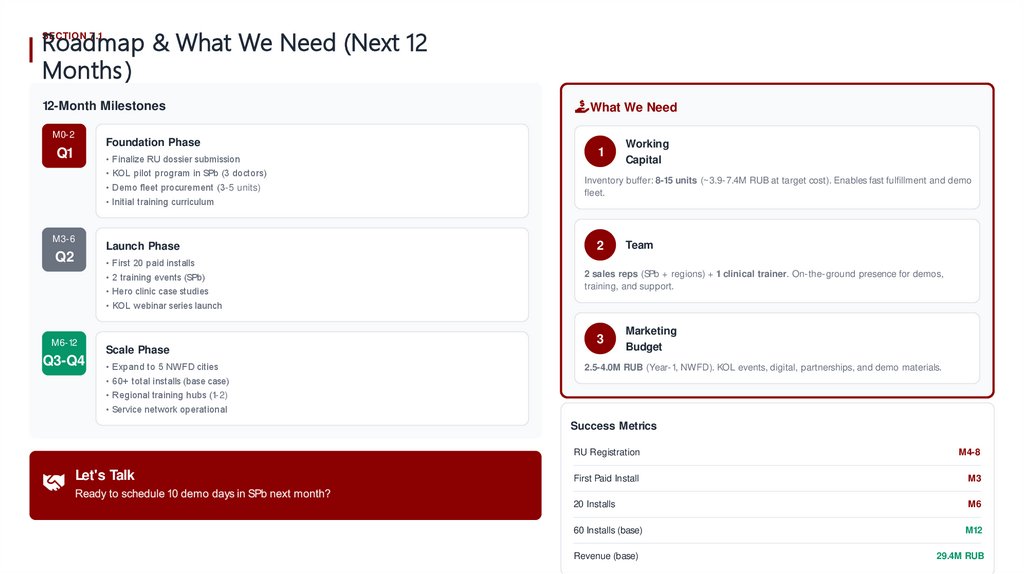

Roadmap & What We Need (Next 12Months )

SECTION 7.1

12-Month Milestones

M0-2

Foundation Phase

Q1

• Finalize RU dossier submission

• KOL pilot program in SPb (3 doctors)

• Demo fleet procurement (3-5 units)

• Initial training curriculum

M3-6

Launch Phase

Q2

What We Need

1

Working

Capital

Inventory buffer: 8-15 units (~3.9-7.4M RUB at target cost). Enables fast fulfillment and demo

fleet.

2

Team

• First 20 paid installs

• 2 training events (SPb)

• Hero clinic case studies

2 sales reps (SPb + regions) + 1 clinical trainer. On-the-ground presence for demos,

training, and support.

• KOL webinar series launch

M6-12

Q3-Q4

Scale Phase

• Expand to 5 NWFD cities

3

Marketing

Budget

2.5-4.0M RUB (Year-1, NWFD). KOL events, digital, partnerships, and demo materials.

• 60+ total installs (base case)

• Regional training hubs (1-2)

• Service network operational

Success Metrics

Let's Talk

RU Registration

M4-8

First Paid Install

M3

20 Installs

M6

60 Installs (base)

M12

Revenue (base)

29.4M RUB