industry

industrySimilar presentations:

Bolshaya kruzhka myagkoe

1.

Prepared byBRIF Research Group

September 2025

2.

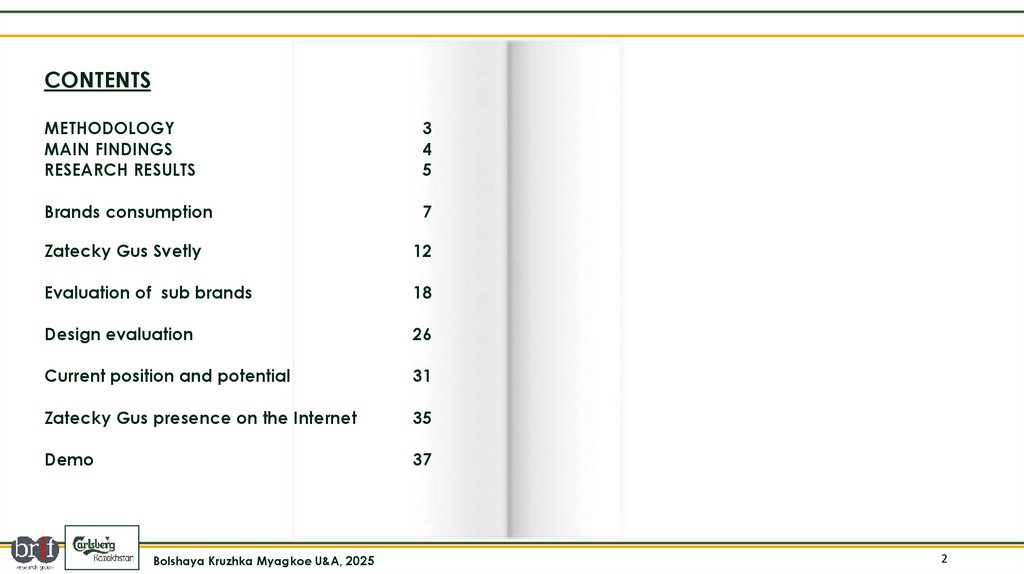

CONTENTSMETHODOLOGY

MAIN FINDINGS

RESEARCH RESULTS

3

4

5

Brands consumption

7

Zatecky Gus Svetly

12

Evaluation of sub brands

18

Design evaluation

26

Current position and potential

31

Zatecky Gus presence on the Internet

35

Demo

37

Bolshaya Kruzhka Myagkoe U&A, 2025

2

3.

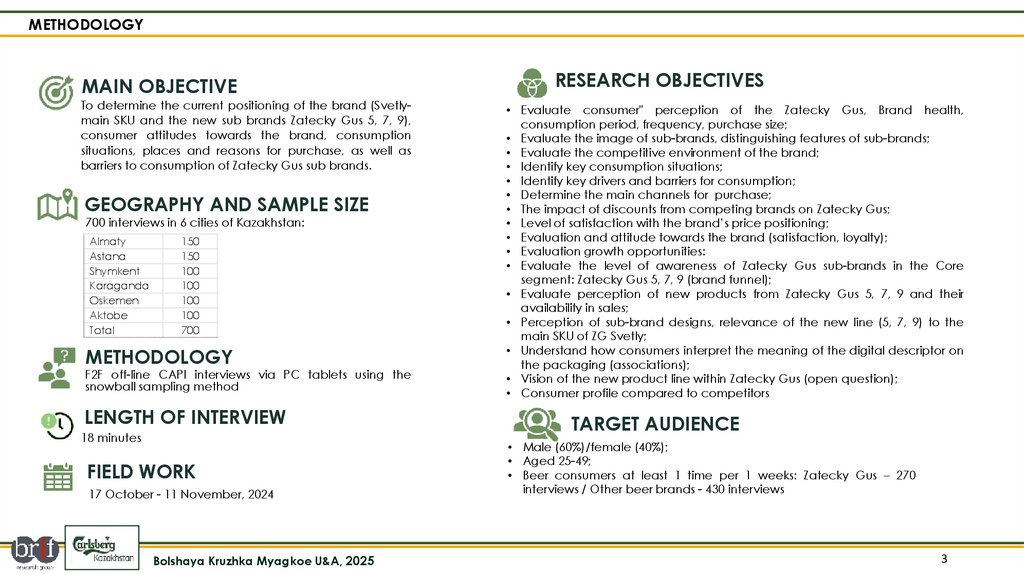

METHODOLOGYMAIN OBJECTIVE

To determine the current positioning of the brand (Svetlymain SKU and the new sub brands Zatecky Gus 5, 7, 9),

consumer attitudes towards the brand, consumption

situations, places and reasons for purchase, as well as

barriers to consumption of Zatecky Gus sub brands.

GEOGRAPHY AND SAMPLE SIZE

700 interviews in 6 cities of Kazakhstan:

Almaty

Astana

Shymkent

Karaganda

Oskemen

Aktobe

Total

150

150

100

100

100

100

700

METHODOLOGY

F2F off-line CAPI interviews via PC tablets using the

snowball sampling method

LENGTH OF INTERVIEW

18 minutes

FIELD WORK

17 October - 11 November, 2024

Bolshaya Kruzhka Myagkoe U&A, 2025

RESEARCH OBJECTIVES

• Evaluate consumer" perception of the Zatecky Gus, Brand health,

consumption period, frequency, purchase size;

• Evaluate the image of sub-brands, distinguishing features of sub-brands;

• Evaluate the competitive environment of the brand;

• Identify key consumption situations;

• Identify key drivers and barriers for consumption;

• Determine the main channels for purchase;

• The impact of discounts from competing brands on Zatecky Gus;

• Level of satisfaction with the brand’s price positioning;

• Evaluation and attitude towards the brand (satisfaction, loyalty);

• Evaluation growth opportunities:

• Evaluate the level of awareness of Zatecky Gus sub-brands in the Core

segment: Zatecky Gus 5, 7, 9 (brand funnel);

• Evaluate perception of new products from Zatecky Gus 5, 7, 9 and their

availability in sales;

• Perception of sub-brand designs, relevance of the new line (5, 7, 9) to the

main SKU of ZG Svetly;

• Understand how consumers interpret the meaning of the digital descriptor on

the packaging (associations);

• Vision of the new product line within Zatecky Gus (open question);

• Consumer profile compared to competitors

TARGET AUDIENCE

• Male (60%)/female (40%);

• Aged 25-49;

• Beer consumers at least 1 time per 1 weeks: Zatecky Gus – 270

interviews / Other beer brands - 430 interviews

3

4.

MAIN FINDINGSBolshaya Kruzhka Myagkoe U&A, 2025

4

5.

BRANDSCONSUMPTION

6.

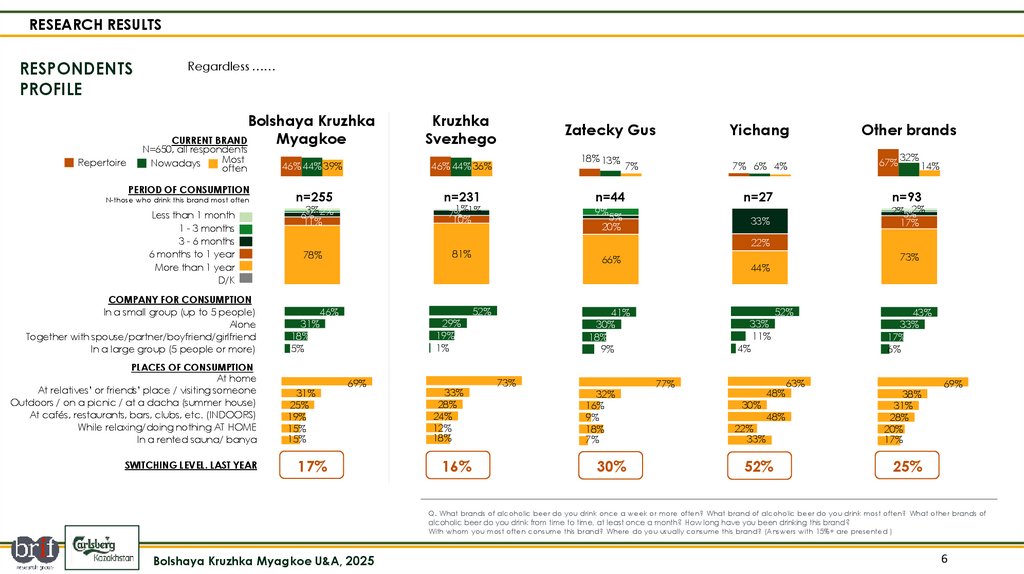

RESEARCH RESULTSRESPONDENTS

PROFILE

Regardless ……

Bolshaya Kruzhka

Myagkoe

CURRENT BRAND

Repertoire

N=650, all respondents

Most

Nowadays

often

PERIOD OF CONSUMPTION

N-those who drink this brand most often

Less than 1 month

1 - 3 months

3 - 6 months

6 months to 1 year

More than 1 year

D/K

46% 44% 39%

46% 44% 36%

n=255

n=231

PLACES OF CONSUMPTION

At home

At relatives’ or friends’ place / visiting someone

Outdoors / on a picnic / at a dacha (summer house)

At cafés, restaurants, bars, clubs, etc. (INDOORS)

While relaxing/doing nothing AT HOME

In a rented sauna/ banya

31%

25%

19%

15%

15%

18% 13%

17%

33%

28%

24%

12%

18%

16%

7% 6% 4%

n=27

5%

20%

Other brands

67%

32%

14%

n=93

2%5%2%

17%

33%

22%

66%

73%

32%

16%

9%

18%

7%

30%

73%

44%

52%

41%

30%

18%

9%

29%

19%

1%

69%

7%

n=44

52%

46%

Yichang

9%

81%

78%

31%

18%

5%

Zatecky Gus

1%

7% 1%

10%

3%

6% 2%

11%

COMPANY FOR CONSUMPTION

In a small group (up to 5 people)

Alone

Together with spouse/partner/boyfriend/girlfriend

In a large group (5 people or more)

SWITCHING LEVEL. LAST YEAR

Kruzhka

Svezhego

33%

11%

4%

77%

48%

30%

48%

22%

33%

52%

63%

43%

33%

17%

6%

38%

31%

28%

20%

17%

69%

25%

Q. What brands of alcoholic beer do you drink once a week or more often? What brand of alcoholic beer do you drink most often? What other brands of

alcoholic beer do you drink from time to time, at least once a month? How long have you been drinking this brand?

With whom you most often consume this brand? Where do you usually consume this brand? (Answers with 15%+ are presented )

Bolshaya Kruzhka Myagkoe U&A, 2025

6

7.

RESEARCH RESULTSDRIVERS FOR

CONSUMPTION

Period of

consumption

(above a year)

Total

n=650

Bolshaya Kruzhka

Myagkoe

n=255

Kruzhka

Svezhego

n=231

Zatecky

Gus

n=44

Yichang

n=27

Other

brands

n=93

76%

78%

81%

66%

44%

73%

Easy to drink / smooth taste

Liked the taste

18%

Wanted to try something new

Suitable packaging

size/volume

Convenient packaging format

Prestigious brand

19%

20%

18%

53%

59%

32%

24%

19%

11%

14%

15%

26%

14%

13%

9%

11%

12%

12%

11%

11%

9%

12%

14%

8%

10%

7%

5%

7%

5%

7%

11%

5%

2%

4%

4%

6%

9%

5%

2%

0%

3%

6%

5%

5%

2%

0%

16%

Easy to find in stores

There was a

discount/promotion

57%

57%

24%

23%

The price was acceptable

Recommendations from

friends/colleagues

43%

51%

26%

9%

4%

12%

15%

10%

Q. Why did you start drinking this brand?

Drivers with 6%+ by Total are shown in the graph

Bolshaya Kruzhka Myagkoe U&A, 2025

7

8.

RESEARCH RESULTSPLACE OF

PURCHASE

Hypermarkets /

Supermarkets / Chain stores

(e.g., Magnum, Small, Toi)

Mini-markets (small selfservice store with 1–2 cash

registers)

Total

n=650

Bolshaya Kruzhka

Myagkoe

n=255

Kruzhka

Svezhego

n=231

26%

41%

43%

Zatecky

Gus

n=44

Yichang

n=27

34%

Other

brands

n=93

41%

59%

6%

6%

14%

10%

10%

Small grocery store / corner

shop / convenience store

11%

26%

51%

44%

43%

50%

30%

Other places

2%

3%

3%

2%

6%

Q. Where do you buy this brand most often?

Bolshaya Kruzhka Myagkoe U&A, 2025

8

9.

BKM FORMATCONSUMPTION

10.

RESEARCH RESULTSSHARE OF FORMAT

TOP2 PLACES OF PURCHASE AND REASONS FOR CHOICE

n- BKM consumers

Small grocery store

n=440

33%

50%

CAN/BOTTLE d/e

n=78

Convenient 49%

Promotions/discounts 39%

Affordable price 33%

18%

Convenient 96%

Convenient 88%

DESIRED NEW

FLAVORS

0.45L BKM

BOTTLE INTEREST

IMPACT OF

BKM STRONG

BK VS ANOTHER

BRAND

KS

39%

YICHAN

3%

I will buy BK regardless

of the discount on

another brand

No Preference

65%

• BKM - Versatile Brand 40%

59%

75% b

• BKM - Versatile Brand 44%

67%

56%

• BKM - Versatile Brand 39%

64%

46%

• BKM - Mild Brand 31%

• Fruit/Berry flavor 6%

• Too fragile 25%

Convenient 49%

Promotions/discounts 35%

• Inconvenient to drink 19%

Affordable price 25%

• Inconvenient to open 18%

Bottle

38%

• Inconvenient to transport 21%

• Inconvenient to drink 22%

Convenient 43%

Promotions/discounts 40%

• Less natural 14%

Affordable price 41%

• Heats up quickly 14%

41%

58%

50% с

52% b

BOTTLE c

n=218

Convenient 95%

BK

43%

40%

CAN b

n=144

Convenient 95%

BEST «SOFT» DESIGN

Hyper/ Super market

46%

Total BKM a

BARRIERS TO PURCHASING

THIS FORMAT

Can

• Inconvenient to open 17%

53%

42%

4%

61%

36%

3%

40%

• BKM - Mild Brand 27%

50% b

• BKM - Mild Brand 32%

45%

Convenient 63%

Promotions/discounts 46%

Affordable price 29%

Bolshaya Kruzhka Myagkoe U&A, 2025

58%

41%

1%

64%

76% d

• BKM - Versatile Brand 35%

45%

• BKM - Mild Brand 33%

10

11.

RESEARCH RESULTSAmong BKM consumers, the most preferred format is the bottle (49%). The smallest group of BKM consumers are those who are indifferent to the format, i.e. they consume this brand both in cans and in bottles (18%). Moreover, among the

“indifferent” consumers, there is no difference in the place of consumption and the company of consumption between cans and bottles.

Significant differences were identified:

• among can consumers compared to bottle consumers – consumption in small groups and brands in the Prague and Zhigulevskoye repertoire

• among bottle consumers compared to can consumers – consumption alone and in large groups.

SHARE OF FORMAT

GENDER

TOP3 PLACES OF

CONSUMPTION

n- BKM consumers

Male

Female

Total BKM a

60%

n=440

40%

At

home

Visiting

someone

Outdoors

72%

33%

22%

33%

BOTTLE c

n=218

Group

5-

50%

Alone

30%

TOP5 BRANDS IN

REPERTOIRE

Group

5+

Together

18%

KS

45%

3%

c

CAN b

n=144

CONSUMPTION

COMPANY

55%

63%

50%

45%

37%

64%

18%

35%

19%

59%

41%

73%

27%

72%

CAN/BOTTLE d/e

n=78

67%

33%

56%

17%

31%

37%

26%

Bolshaya Kruzhka Myagkoe U&A, 2025

56%

31%

Miller

Praga

17%

13%

c

c

19%

13%

Zhigulevskoe

PURCHASE

FREQUENCY

AVERAGE

NUMBER

PRICE

PERCEPTION

1 year +

1 time per week

Per purchase

45%

52%

3,1

85%

Mid-price segment

12%

12%

18%

17%

10%

36%

49%

3,3

80%

10%

9%

13%

50% b

53%

2,9

85%

14%

10%

14%

46%

56%

3,4

40%

19%

19%

36%

77%

49%

1%

b

35%

19%

c

45%

24%

ZG

PERIOD OF

CONSUMPTION

19%

6%

1%

50%

c

24%

91% b

82%

1%

a, b, c, d, e - This score is significantly higher compared to other group

11

12.

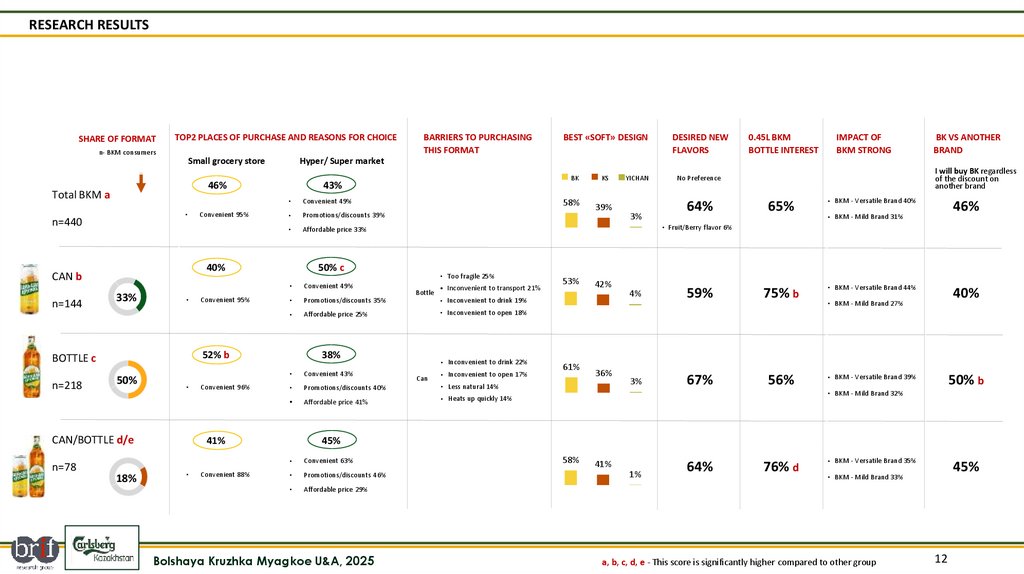

RESEARCH RESULTSSHARE OF FORMAT

TOP2 PLACES OF PURCHASE AND REASONS FOR CHOICE

n- BKM consumers

Small grocery store

n=440

33%

50%

CAN/BOTTLE d/e

n=78

Convenient 49%

Promotions/discounts 39%

Affordable price 33%

18%

Convenient 96%

Convenient 88%

DESIRED NEW

FLAVORS

0.45L BKM

BOTTLE INTEREST

IMPACT OF

BKM STRONG

BK VS ANOTHER

BRAND

KS

39%

YICHAN

3%

I will buy BK regardless

of the discount on

another brand

No Preference

65%

• BKM - Versatile Brand 40%

59%

75% b

• BKM - Versatile Brand 44%

67%

56%

• BKM - Versatile Brand 39%

64%

46%

• BKM - Mild Brand 31%

• Fruit/Berry flavor 6%

• Too fragile 25%

Convenient 49%

Promotions/discounts 35%

• Inconvenient to drink 19%

Affordable price 25%

• Inconvenient to open 18%

Bottle

38%

• Inconvenient to transport 21%

• Inconvenient to drink 22%

Convenient 43%

Promotions/discounts 40%

• Less natural 14%

Affordable price 41%

• Heats up quickly 14%

41%

58%

50% с

52% b

BOTTLE c

n=218

Convenient 95%

BK

43%

40%

CAN b

n=144

Convenient 95%

BEST «SOFT» DESIGN

Hyper/ Super market

46%

Total BKM a

BARRIERS TO PURCHASING

THIS FORMAT

Can

• Inconvenient to open 17%

53%

42%

4%

61%

36%

3%

40%

• BKM - Mild Brand 27%

50% b

• BKM - Mild Brand 32%

45%

Convenient 63%

Promotions/discounts 46%

Affordable price 29%

Bolshaya Kruzhka Myagkoe U&A, 2025

58%

41%

1%

64%

76% d

• BKM - Versatile Brand 35%

45%

• BKM - Mild Brand 33%

a, b, c, d, e - This score is significantly higher compared to other group

12

13.

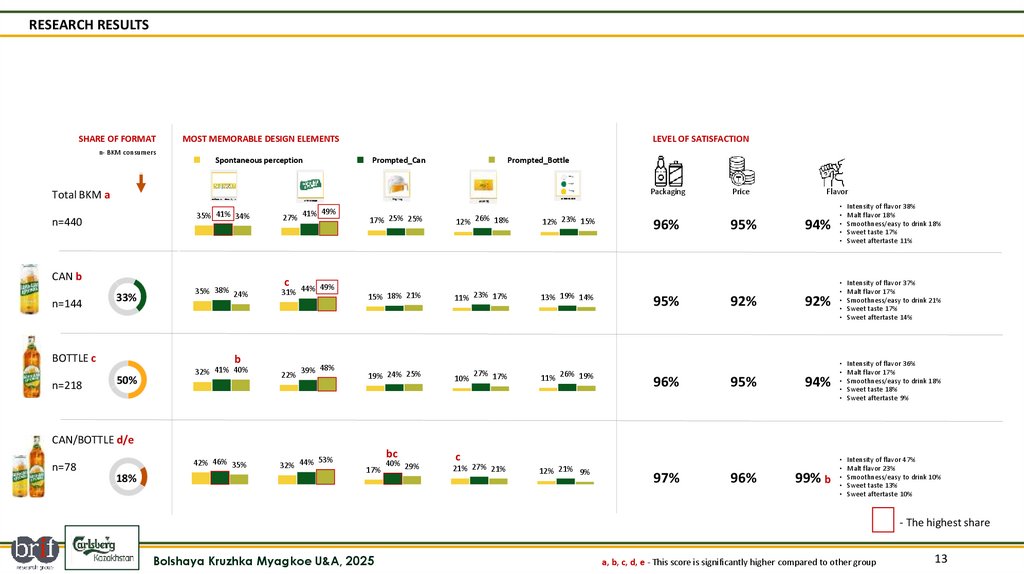

RESEARCH RESULTSSHARE OF FORMAT

n- BKM consumers

MOST MEMORABLE DESIGN ELEMENTS

Spontaneous perception

LEVEL OF SATISFACTION

Prompted_Can

Prompted_Bottle

Packaging

Total BKM a

n=440

35% 41% 34%

27% 41%

35% 38% 24%

31% 44%

CAN b

n=144

33%

BOTTLE c

n=218

c

b

50%

49%

49%

39% 48%

32% 41% 40%

22%

42% 46% 35%

32% 44%

17% 25% 25%

12% 26% 18%

12% 23% 15%

15% 18% 21%

11% 23% 17%

13% 19% 14%

19% 24% 25%

27% 17%

11% 26% 19%

21% 27% 21%

12% 21% 9%

10%

96%

95%

96%

Price

95%

92%

95%

Flavor

94%

• Intensity of flavor 38%

• Malt flavor 18%

• Smoothness/easy to drink 18%

• Sweet taste 17%

• Sweet aftertaste 11%

92%

• Intensity of flavor 37%

• Malt flavor 17%

• Smoothness/easy to drink 21%

• Sweet taste 17%

• Sweet aftertaste 14%

94%

• Intensity of flavor 36%

• Malt flavor 17%

• Smoothness/easy to drink 18%

• Sweet taste 18%

• Sweet aftertaste 9%

99% b

• Intensity of flavor 47%

• Malt flavor 23%

• Smoothness/easy to drink 10%

• Sweet taste 13%

• Sweet aftertaste 10%

CAN/BOTTLE d/e

n=78

18%

bc

53%

17%

40% 29%

c

97%

96%

- The highest share

Bolshaya Kruzhka Myagkoe U&A, 2025

a, b, c, d, e - This score is significantly higher compared to other group

13

14.

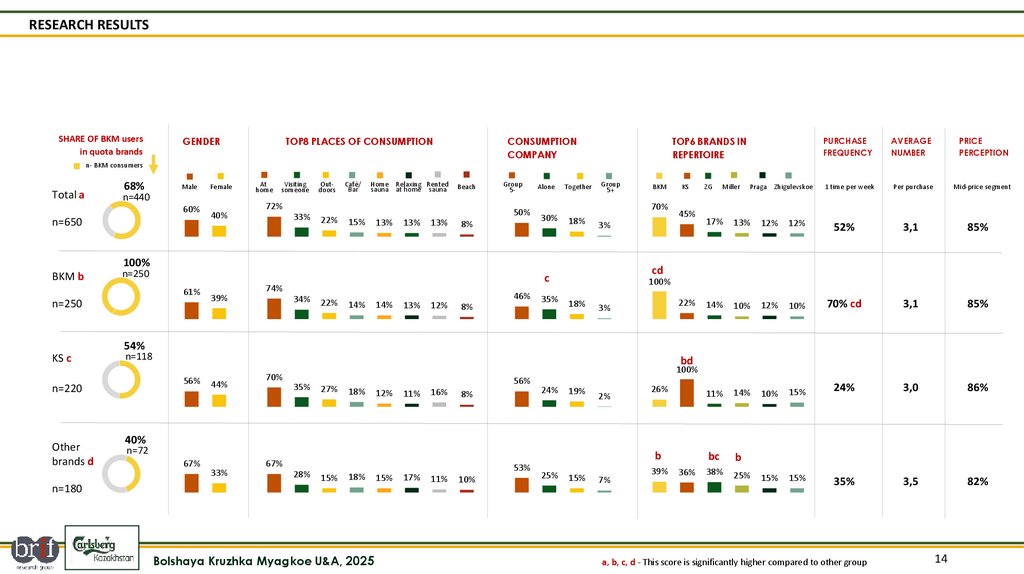

RESEARCH RESULTSSHARE OF BKM users

in quota brands

GENDER

TOP8 PLACES OF CONSUMPTION

CONSUMPTION

COMPANY

TOP6 BRANDS IN

REPERTOIRE

PURCHASE

FREQUENCY

AVERAGE

NUMBER

PRICE

PERCEPTION

1 time per week

Per purchase

Mid-price segment

n- BKM consumers

Total a

68%

Male

Female

n=440

60%

n=650

40%

At

home

Visiting

someone

Outdoors

Café/

Bar

Home Relaxing Rented

sauna at home sauna

Beach

72%

33%

22%

15%

Group

5-

50%

13%

13%

13%

8%

Alone

Together

30%

18%

Group

5+

70%

n=250

61%

n=250

34%

22%

14%

14%

13%

12%

46%

8%

35%

45%

ZG

Miller

Praga Zhigulevskoe

17%

13%

12%

12%

52%

3,1

85%

14%

10%

12%

10%

70% cd

3,1

85%

26%

11%

14%

10%

15%

24%

3,0

86%

b

bc

b

38%

25%

15%

15%

35%

3,5

82%

cd

с

74%

39%

KS

3%

100%

BKM b

BKM

100%

18%

22%

3%

54%

KS c

n=118

56%

n=220

Other

brands d

n=180

bd

44%

100%

70%

35%

27%

56%

18%

12%

11%

16%

8%

24%

19%

2%

40%

n=72

67%

33%

67%

28%

15%

18%

Bolshaya Kruzhka Myagkoe U&A, 2025

53%

15%

17%

11%

10%

25%

15%

7%

39%

36%

a, b, c, d - This score is significantly higher compared to other group

14

15.

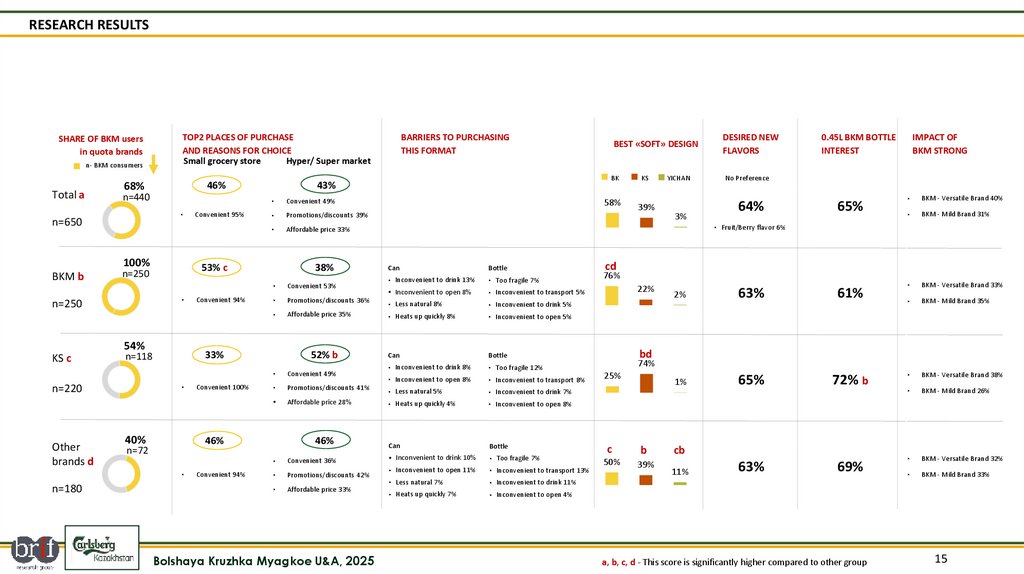

RESEARCH RESULTSSHARE OF BKM users

in quota brands

n- BKM consumers

Total a

TOP2 PLACES OF PURCHASE

AND REASONS FOR CHOICE

Small grocery store

Hyper/ Super market

46%

68%

n=440

n=650

100%

BKM b

54%

KS c

Other

brands d

40%

Convenient 49%

Promotions/discounts 39%

Affordable price 33%

Convenient 94%

38%

Convenient 100%

Convenient 94%

Can

Bottle

• Inconvenient to drink 13%

• Too fragile 7%

• Inconvenient to open 8%

• Inconvenient to transport 5%

Promotions/discounts 36%

• Less natural 8%

• Inconvenient to drink 5%

Affordable price 35%

• Heats up quickly 8%

• Inconvenient to open 5%

Can

Bottle

• Inconvenient to drink 8%

• Too fragile 12%

Convenient 49%

• Inconvenient to open 8%

• Inconvenient to transport 8%

Promotions/discounts 41%

• Less natural 5%

• Inconvenient to drink 7%

Affordable price 28%

• Heats up quickly 4%

• Inconvenient to open 8%

Can

Bottle

• Inconvenient to drink 10%

• Too fragile 7%

• Inconvenient to open 11%

• Inconvenient to transport 13%

• Less natural 7%

• Inconvenient to drink 11%

• Heats up quickly 7%

• Inconvenient to open 4%

46%

Convenient 36%

Promotions/discounts 42%

Affordable price 33%

Bolshaya Kruzhka Myagkoe U&A, 2025

DESIRED NEW

FLAVORS

BK

No Preference

KS

39%

YICHAN

3%

64%

0.45L BKM BOTTLE

INTEREST

65%

IMPACT OF

BKM STRONG

BKM - Versatile Brand 40%

BKM - Mild Brand 31%

BKM - Versatile Brand 33%

BKM - Mild Brand 35%

BKM - Versatile Brand 38%

BKM - Mild Brand 26%

BKM - Versatile Brand 32%

BKM - Mild Brand 33%

• Fruit/Berry flavor 6%

Convenient 53%

52% b

BEST «SOFT» DESIGN

58%

46%

n=72

n=180

33%

n=118

n=220

43%

53% c

n=250

n=250

Convenient 95%

BARRIERS TO PURCHASING

THIS FORMAT

cd

76%

22%

2%

63%

61%

1%

65%

72% b

63%

69%

bd

74%

25%

c

b

50%

39%

cb

11%

a, b, c, d - This score is significantly higher compared to other group

15

16.

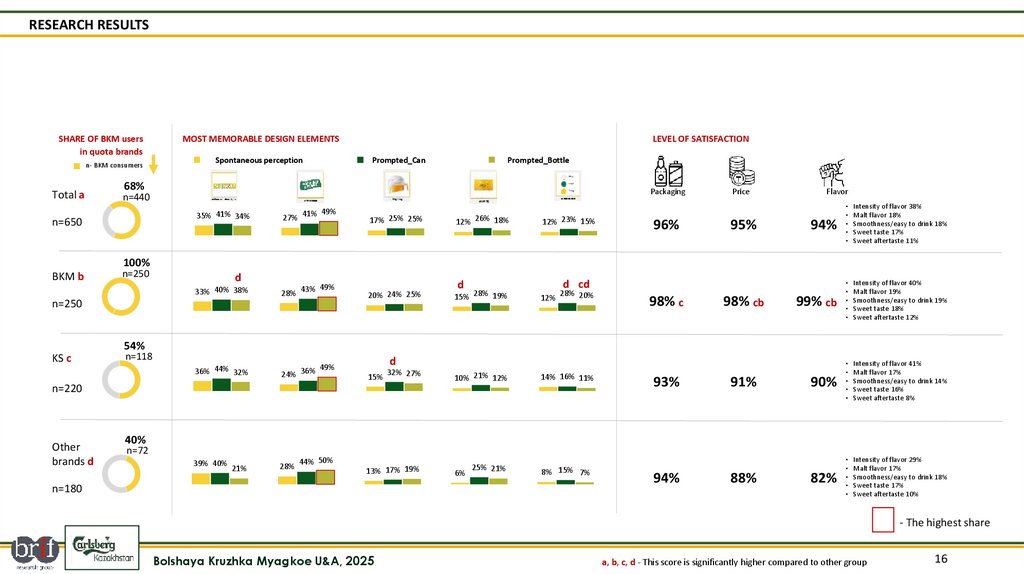

RESEARCH RESULTSSHARE OF BKM users

in quota brands

n- BKM consumers

Total a

MOST MEMORABLE DESIGN ELEMENTS

Spontaneous perception

LEVEL OF SATISFACTION

Prompted_Can

Prompted_Bottle

68%

Packaging

n=440

27% 41%

49%

33% 40% 38%

28% 43%

49%

36% 44% 32%

24% 36%

49%

39% 40%

28%

35% 41% 34%

n=650

17% 25% 25%

12% 26% 18%

20% 24% 25%

15% 28% 19%

12% 23% 15%

96%

Price

95%

Flavor

94%

• Intensity of flavor 38%

• Malt flavor 18%

• Smoothness/easy to drink 18%

• Sweet taste 17%

• Sweet aftertaste 11%

99% cb

• Intensity of flavor 40%

• Malt flavor 19%

• Smoothness/easy to drink 19%

• Sweet taste 18%

• Sweet aftertaste 12%

90%

• Intensity of flavor 41%

• Malt flavor 17%

• Smoothness/easy to drink 14%

• Sweet taste 16%

• Sweet aftertaste 8%

82%

• Intensity of flavor 29%

• Malt flavor 17%

• Smoothness/easy to drink 18%

• Sweet taste 17%

• Sweet aftertaste 10%

100%

BKM b

n=250

d

n=250

d cd

d

12%

28% 20%

98% c

98% cb

54%

KS c

n=118

d

15%

32% 27%

10% 21% 12%

14% 16% 11%

25% 21%

8% 15% 7%

n=220

Other

brands d

93%

91%

40%

n=72

21%

44% 50%

13% 17% 19%

n=180

6%

94%

88%

- The highest share

Bolshaya Kruzhka Myagkoe U&A, 2025

a, b, c, d - This score is significantly higher compared to other group

16