finance

financeSimilar presentations:

Pricing and Resilience of Commodity Markets

1.

Pricing and Resilience of CommodityMarkets:

Historical Analysis of Metal and Gas Price Dependencies and Their

Business Impact

Author: Ronald Medvedev

Supervisor: Olivier Gallay

UNIL | University of Lausanne

Faculty of Management

Master in Business Analytics

Lausanne, 2025

2.

Introduction & Relevance of the StudyMetals and natural gas are critical for Europe's economic stability and

energy security. Price fluctuations significantly impact industries. The

2022 energy crisis, intensified by geopolitical tensions, exposed

vulnerabilities and triggered inflation.

Traditional analysis methods are insufficient for extreme market volatility.

Advanced forecasting, integrating geopolitical, regulatory, and ESG

factors, is crucial. The EU Green Deal further highlights the strategic

relevance of commodities like lithium and cobalt for electrification and

renewable energy.

3.

Research ObjectiveThe core objective of this thesis is to

analyze historical interdependencies between metal and

natural gas prices in Europe

and to

develop forecasting

models that enhance resilience and

support

practical decision-making

for businesses

navigating volatile commodity

markets.

4.

Key Research TasksSystematize theoretical approaches to

commodity pricing and identify core price

drivers.

Analyze key market participants, their

business models, and risk mitigation

strategies.

Review traditional and modern forecasting

methods, assessing their accuracy and

applicability.

Compile and analyze historical price data,

identifying trends, anomalies, and

seasonal effects.

Develop forecasting models using

Random Forest, XGBoost, and LSTM.

Test model performance under shocks

such as COVID-19 and the energy crisis.

Simulate business cases to quantify the

practical value of forecasting models.

Formulate practical recommendations and

explore future research directions,

including ESG integration and XAI.

5.

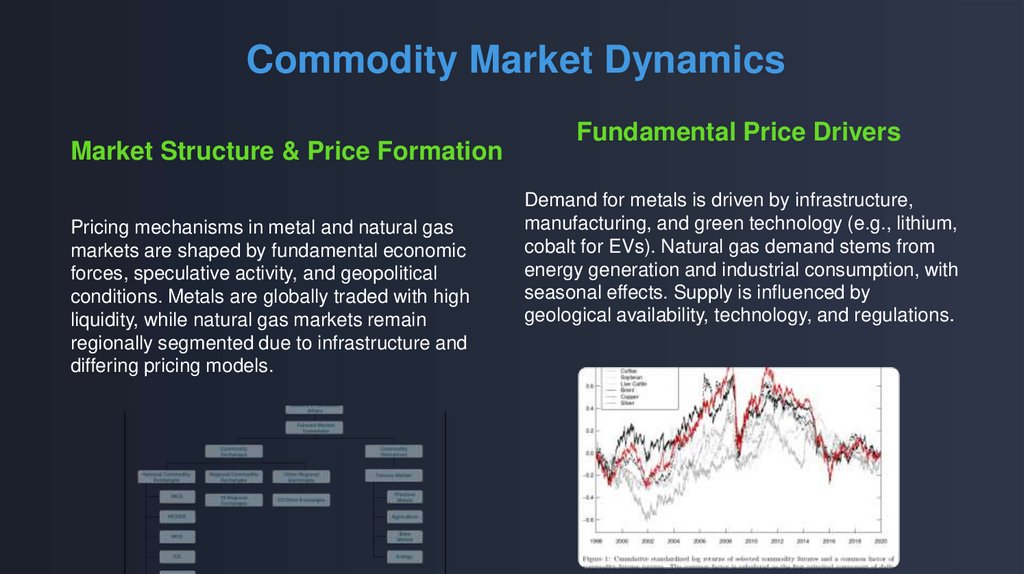

Commodity Market DynamicsMarket Structure & Price Formation

Pricing mechanisms in metal and natural gas

markets are shaped by fundamental economic

forces, speculative activity, and geopolitical

conditions. Metals are globally traded with high

liquidity, while natural gas markets remain

regionally segmented due to infrastructure and

differing pricing models.

Fundamental Price Drivers

Demand for metals is driven by infrastructure,

manufacturing, and green technology (e.g., lithium,

cobalt for EVs). Natural gas demand stems from

energy generation and industrial consumption, with

seasonal effects. Supply is influenced by

geological availability, technology, and regulations.

6.

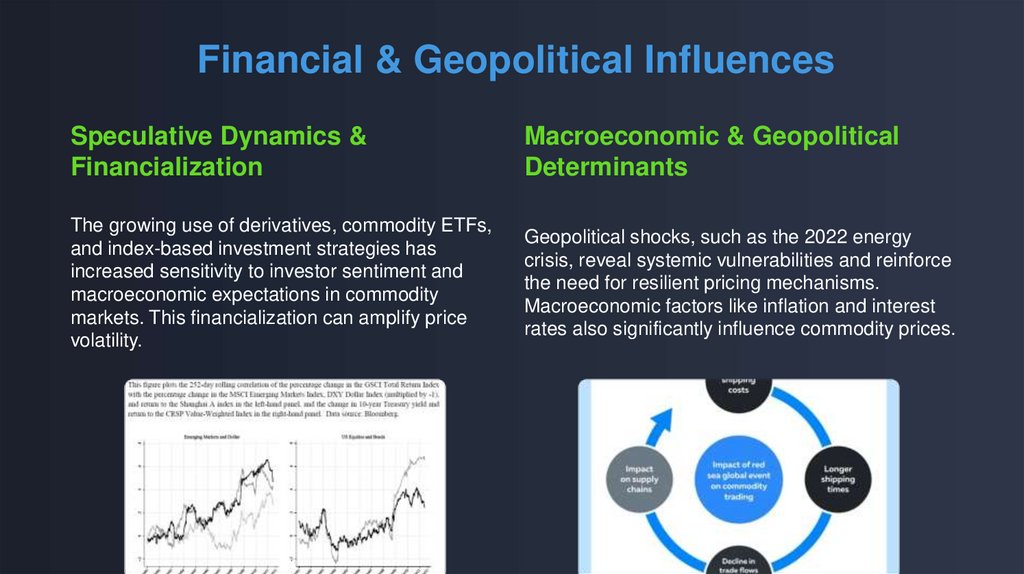

Financial & Geopolitical InfluencesSpeculative Dynamics &

Financialization

Macroeconomic & Geopolitical

Determinants

The growing use of derivatives, commodity ETFs,

and index-based investment strategies has

increased sensitivity to investor sentiment and

macroeconomic expectations in commodity

markets. This financialization can amplify price

volatility.

Geopolitical shocks, such as the 2022 energy

crisis, reveal systemic vulnerabilities and reinforce

the need for resilient pricing mechanisms.

Macroeconomic factors like inflation and interest

rates also significantly influence commodity prices.

7.

Key Market Participants & Risk ManagementStrategic Roles of Participants

Hedging & Risk Management

Commodity markets involve diverse participants:

producers, consumers, traders, and financial

institutions. Each plays a strategic role in price

discovery, supply chain management, and risk

mitigation. Understanding their interactions is

crucial for market stability.

Effective risk management, particularly through

hedging strategies, is vital for navigating volatile

commodity markets. This includes using financial

instruments like futures and options to mitigate

price exposure and ensure business continuity.

8.

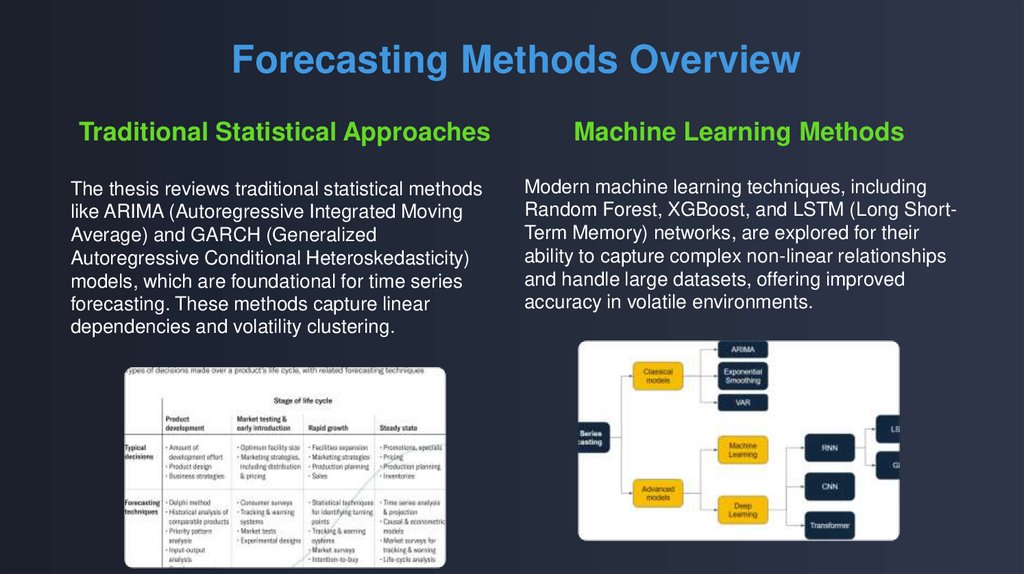

Forecasting Methods OverviewTraditional Statistical Approaches

Machine Learning Methods

The thesis reviews traditional statistical methods

like ARIMA (Autoregressive Integrated Moving

Average) and GARCH (Generalized

Autoregressive Conditional Heteroskedasticity)

models, which are foundational for time series

forecasting. These methods capture linear

dependencies and volatility clustering.

Modern machine learning techniques, including

Random Forest, XGBoost, and LSTM (Long ShortTerm Memory) networks, are explored for their

ability to capture complex non-linear relationships

and handle large datasets, offering improved

accuracy in volatile environments.

9.

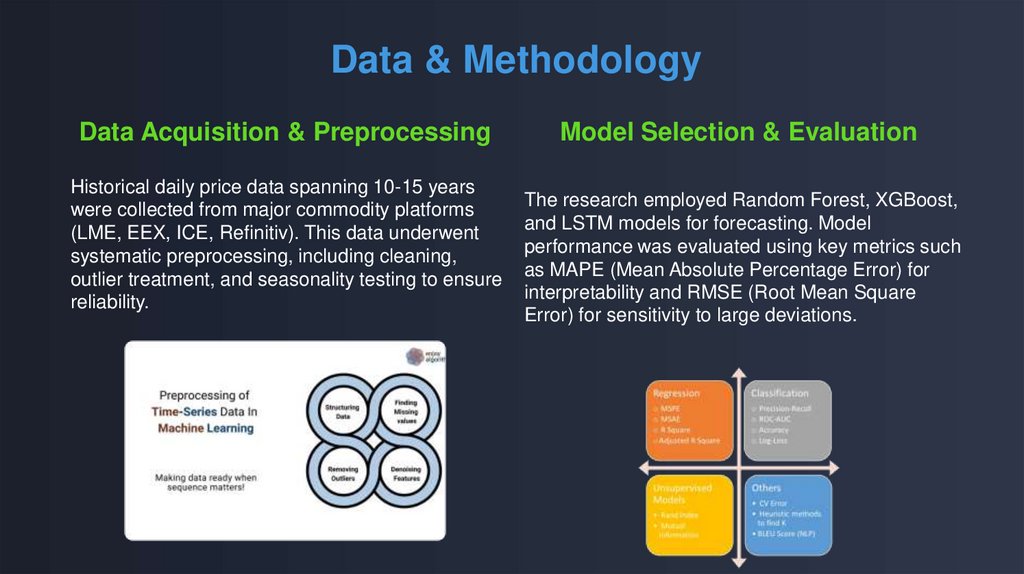

Data & MethodologyData Acquisition & Preprocessing

Historical daily price data spanning 10-15 years

were collected from major commodity platforms

(LME, EEX, ICE, Refinitiv). This data underwent

systematic preprocessing, including cleaning,

outlier treatment, and seasonality testing to ensure

reliability.

Model Selection & Evaluation

The research employed Random Forest, XGBoost,

and LSTM models for forecasting. Model

performance was evaluated using key metrics such

as MAPE (Mean Absolute Percentage Error) for

interpretability and RMSE (Root Mean Square

Error) for sensitivity to large deviations.

10.

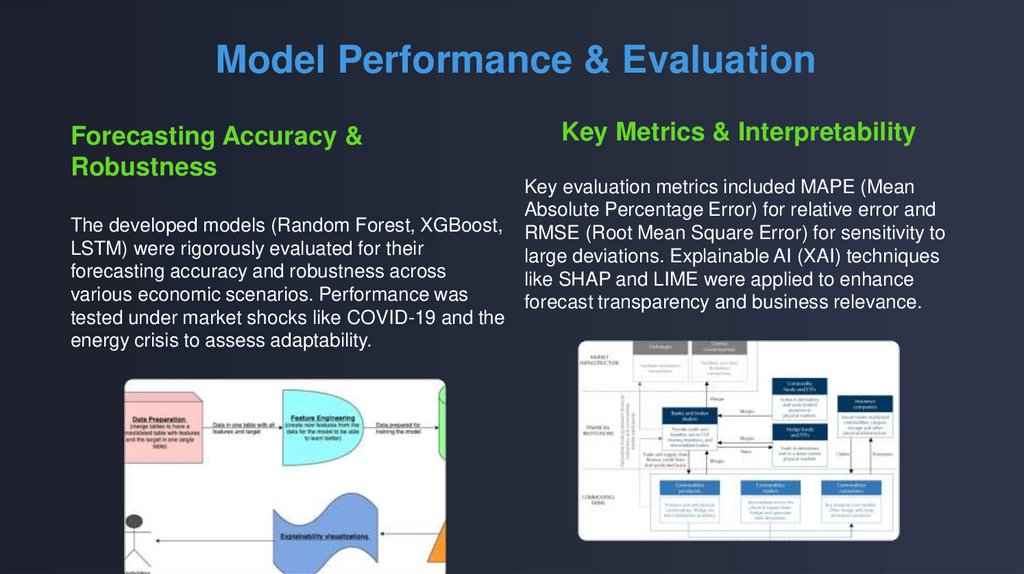

Model Performance & EvaluationForecasting Accuracy &

Robustness

The developed models (Random Forest, XGBoost,

LSTM) were rigorously evaluated for their

forecasting accuracy and robustness across

various economic scenarios. Performance was

tested under market shocks like COVID-19 and the

energy crisis to assess adaptability.

Key Metrics & Interpretability

Key evaluation metrics included MAPE (Mean

Absolute Percentage Error) for relative error and

RMSE (Root Mean Square Error) for sensitivity to

large deviations. Explainable AI (XAI) techniques

like SHAP and LIME were applied to enhance

forecast transparency and business relevance.

11.

Resilience and ESG in Commodity MarketsConceptualizing Resilience

The Rise of ESG Metrics

Resilience in commodity markets refers to the

ability of market systems and participants to adapt

and recover from disruptions, such as geopolitical

shocks, supply chain failures, or extreme weather

events. This thesis emphasizes building robust

strategies against such vulnerabilities.

Environmental, Social, and Governance (ESG)

factors are increasingly influencing commodity

markets. Integrating ESG metrics into forecasting

and risk management is crucial for sustainable

business practices and aligning with global

sustainability goals, such as those outlined in the

EU Green Deal.

12.

Integrating ESG into ForecastingMethodological Foundations

ESG as a Strategic Axis

The thesis proposes methodological foundations

for integrating ESG metrics into forecasting

models. This involves incorporating non-financial

data points related to environmental impact, social

responsibility, and corporate governance alongside

traditional market fundamentals.

Integrating ESG into forecasting transforms it into a

strategic discipline. It allows businesses to

anticipate risks and opportunities related to

sustainability, enhancing long-term resilience and

aligning with evolving regulatory landscapes and

stakeholder expectations.

13.

Strategic Implications of ESG-Integrated ForecastingEnhanced Decision-Making & Risk

Mitigation

Alignment with Sustainability Goals

ESG-integrated forecasting provides a holistic view

of market dynamics, enabling businesses to make

more informed decisions and proactively mitigate

risks associated with environmental, social, and

governance factors. This leads to more resilient

supply chains and investment portfolios.

By incorporating ESG into forecasting, companies

can better align their operations and strategies with

global sustainability goals, such as those outlined

in the EU Green Deal. This not only enhances

corporate reputation but also unlocks new

opportunities in green finance and sustainable

markets.

14.

Key Findings & ContributionsInterdependencies & Volatility

Forecasting Model Superiority

The research confirms significant

interdependencies between metal and gas prices,

highlighting how these relationships contribute to

market volatility. Understanding these dynamics is

crucial for accurate forecasting and risk

management.

The developed machine learning models (Random

Forest, XGBoost, LSTM) demonstrate superior

forecasting accuracy compared to traditional

statistical methods, especially during periods of

high market turbulence. This provides a robust tool

for proactive decision-making.

15.

Practical RecommendationsFor Businesses & Traders

For Policymakers & Regulators

Implement ESG-integrated forecasting models to

enhance risk management and strategic planning.

Adopt machine learning approaches for improved

accuracy in volatile markets. Develop robust

hedging strategies based on interdependency

analysis.

Establish frameworks that encourage ESG

transparency in commodity markets. Develop

policies that support market resilience and stability.

Promote the integration of sustainability metrics in

financial reporting and risk assessment.

16.

Future Research DirectionsAdvanced Model Development

Expanding ESG Integration

Future research should focus on developing more

sophisticated hybrid models that combine the

strengths of different machine learning

approaches. Integration of real-time data streams

and alternative data sources could further enhance

forecasting accuracy.

Research opportunities exist in expanding ESG

integration beyond current metrics to include

emerging sustainability indicators. Cross-sector

analysis and global market integration could

provide deeper insights into resilience

mechanisms.

17.

ConclusionThis thesis demonstrates that integrating ESG factors into

commodity market forecasting creates a powerful framework for

enhanced resilience and sustainable decision-making.

By combining advanced machine learning techniques with ESG metrics, we can better

understand market interdependencies, improve forecasting accuracy, and build more resilient

commodity markets. This research contributes to both academic knowledge and practical

applications in an era of increasing market volatility and sustainability imperatives.

18.

Q&AQuestions & Answers

Thank you for your attention!

I welcome your questions and discussion about this research.

Ready to discuss the implications of ESG-integrated forecasting

for commodity market resilience and sustainability