industry

industrySimilar presentations:

Energy Storage and Conversion

1.

SCIENCEPASSION

TECHNOLOGY

Energy Storage and Conversion CHE.524

Prof. Viktor HACKER

Institut für Chemische Verfahrenstechnik und Umwelttechnik

Technische Universität Graz

2023

ceet.tugraz.at

2.

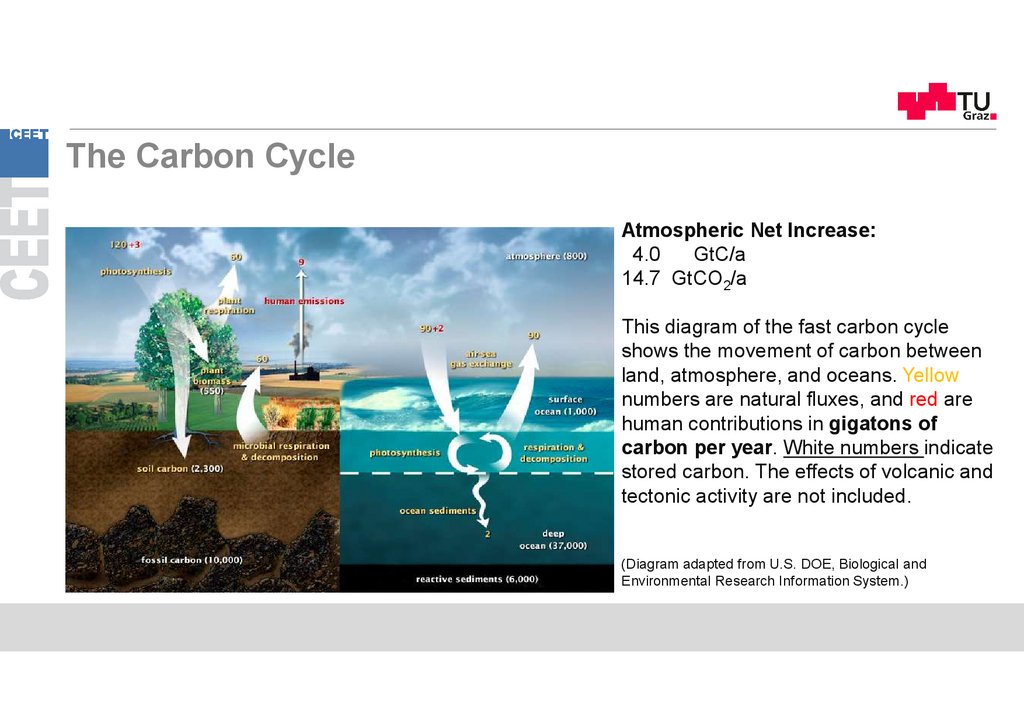

The Carbon CycleAtmospheric Net Increase:

4.0

GtC/a

14.7 GtCO2/a

This diagram of the fast carbon cycle

shows the movement of carbon between

land, atmosphere, and oceans. Yellow

numbers are natural fluxes, and red are

human contributions in gigatons of

carbon per year. White numbers indicate

stored carbon. The effects of volcanic and

tectonic activity are not included.

(Diagram adapted from U.S. DOE, Biological and

Environmental Research Information System.)

3.

3AG Hacker:

Wasserstoff & Brennstoffzellen

www.ceet.tugraz.at / Research

4.

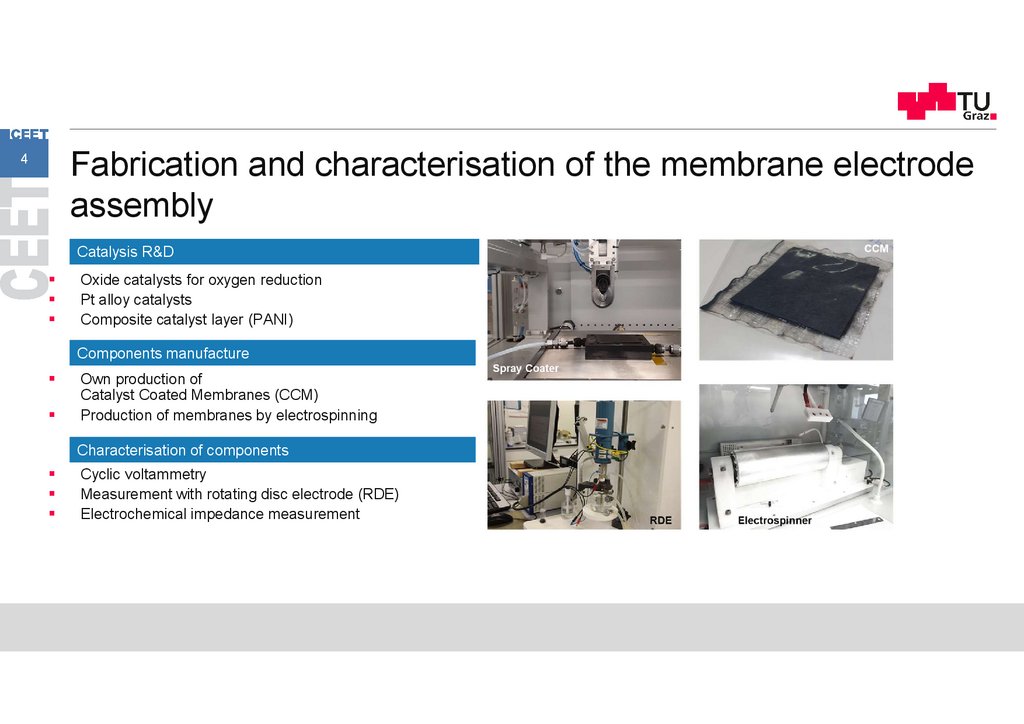

Fabrication and characterisation of the membrane electrodeassembly

4

Catalysis R&D

Oxide catalysts for oxygen reduction

Pt alloy catalysts

Composite catalyst layer (PANI)

Components manufacture

Own production of

Catalyst Coated Membranes (CCM)

Production of membranes by electrospinning

Characterisation of components

Cyclic voltammetry

Measurement with rotating disc electrode (RDE)

Electrochemical impedance measurement

5.

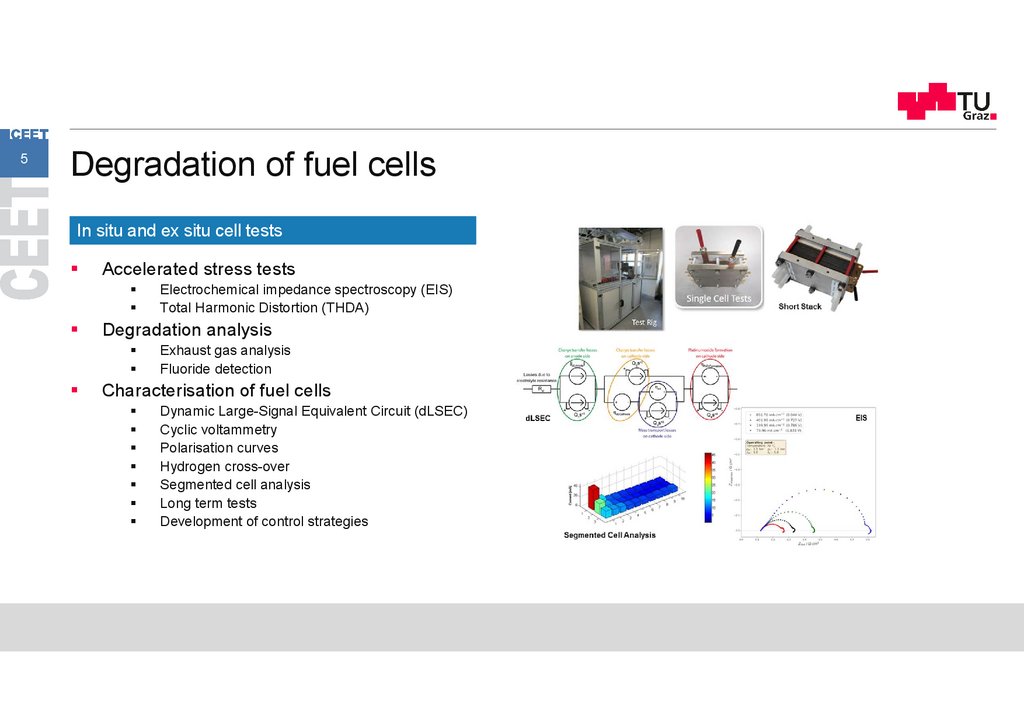

5Degradation of fuel cells

In situ and ex situ cell tests

Accelerated stress tests

Degradation analysis

Electrochemical impedance spectroscopy (EIS)

Total Harmonic Distortion (THDA)

Exhaust gas analysis

Fluoride detection

Characterisation of fuel cells

Dynamic Large-Signal Equivalent Circuit (dLSEC)

Cyclic voltammetry

Polarisation curves

Hydrogen cross-over

Segmented cell analysis

Long term tests

Development of control strategies

6.

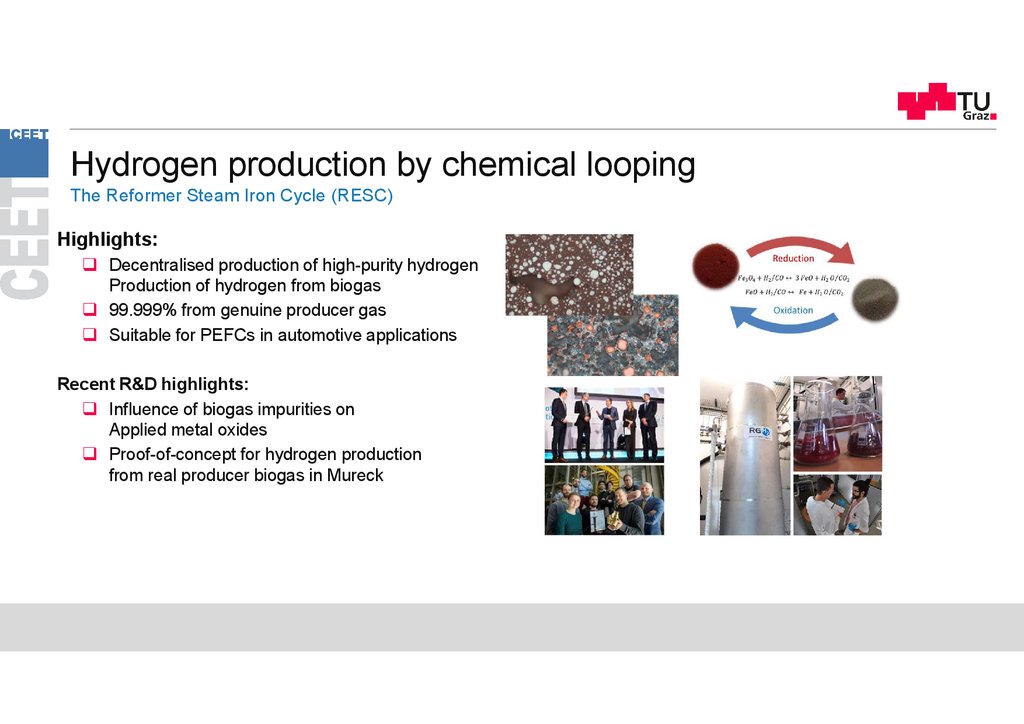

Hydrogen production by chemical loopingThe Reformer Steam Iron Cycle (RESC)

6

Highlights:

Decentralised production of high-purity hydrogen

Production of hydrogen from biogas

99.999% from genuine producer gas

Suitable for PEFCs in automotive applications

Recent R&D highlights:

Influence of biogas impurities on

Applied metal oxides

Proof-of-concept for hydrogen production

from real producer biogas in Mureck

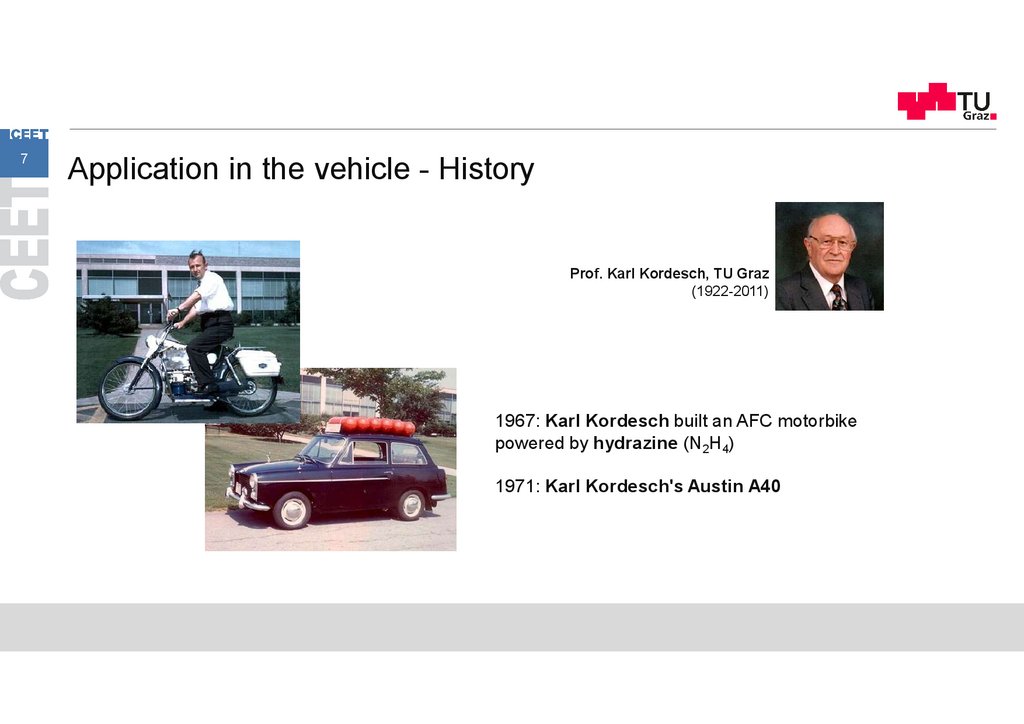

7.

7Application in the vehicle - History

Prof. Karl Kordesch, TU Graz

(1922-2011)

1967: Karl Kordesch built an AFC motorbike

powered by hydrazine (N2H4)

1971: Karl Kordesch's Austin A40

8.

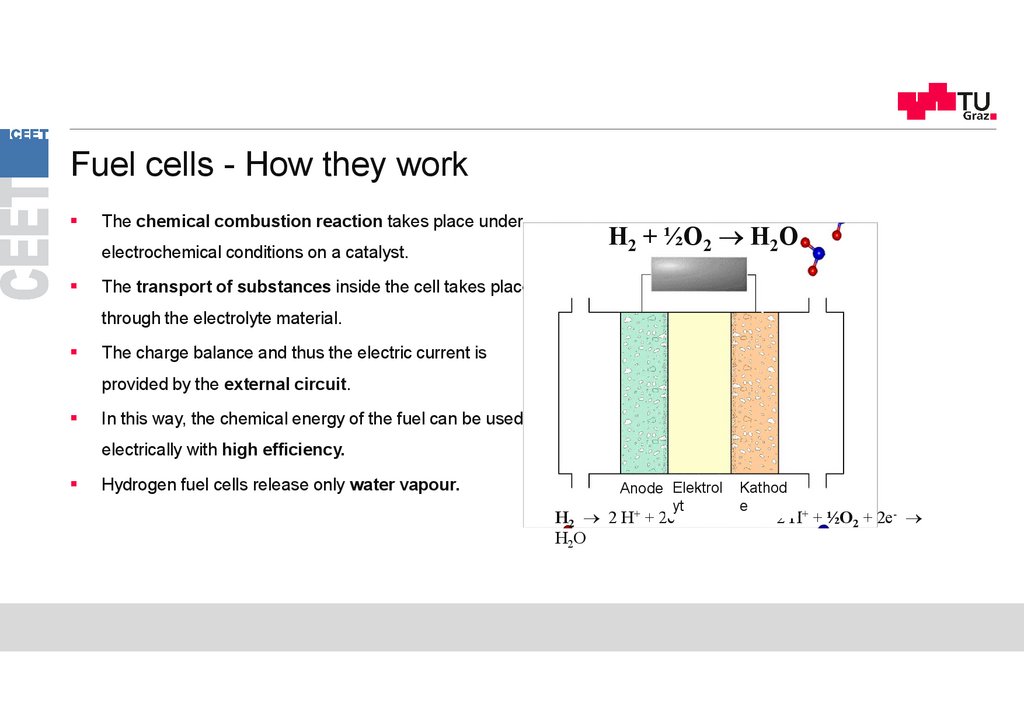

Fuel cells - How they work9

The chemical combustion reaction takes place under

electrochemical conditions on a catalyst.

H2 + ½O2 H2O

The transport of substances inside the cell takes place

through the electrolyte material.

The charge balance and thus the electric current is

provided by the external circuit.

In this way, the chemical energy of the fuel can be used

electrically with high efficiency.

Hydrogen fuel cells release only water vapour.

Electrolyt

Anode Elektrol

e

yt

+

-

H2 2 H + 2e

H2O

Kathod

e

2 H+ + ½O2 + 2e-

9.

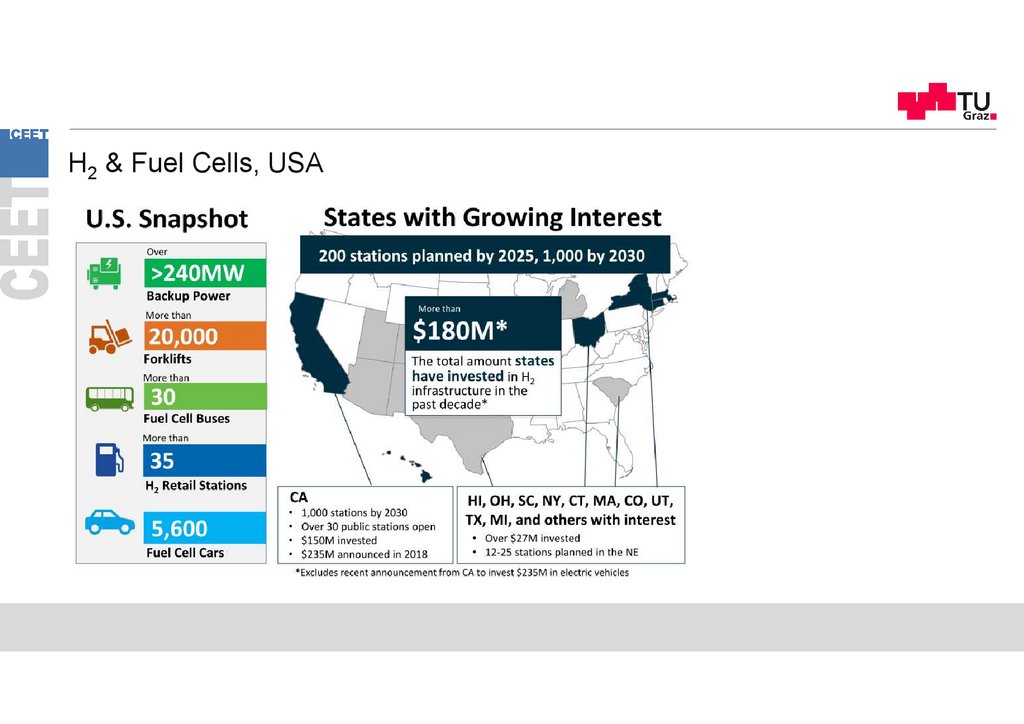

H2 & Fuel Cells, USA10

10.

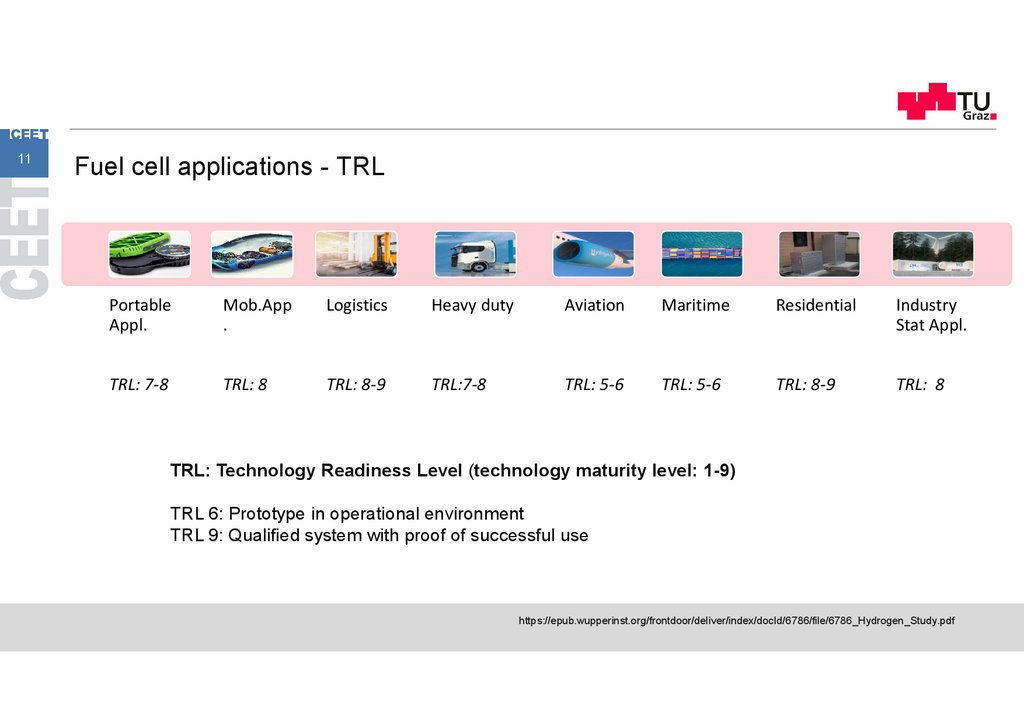

11Fuel cell applications - TRL

Portable

Appl.

Mob.App

.

Logistics

Heavy duty

Aviation

Maritime

TRL: 7-8

TRL: 8

TRL: 8-9

TRL:7-8

TRL: 5-6

TRL: 5-6

• TRL:

approx.

8-9

TRL: Technology Readiness Level (technology maturity level: 1-9)

Residential

Industry

Stat Appl.

TRL: 8-9

TRL: 8

TRL 6: Prototype in operational environment

TRL 9: Qualified system with proof of successful use

https://epub.wupperinst.org/frontdoor/deliver/index/docId/6786/file/6786_Hydrogen_Study.pdf

11.

12The challenges

12.

13Typical power requirement / energy demand

Human body (average power)

80 W

Heavy work

290 W

Energy consumption (fossil)

12 Gtoe/a (140 000 TWh/a)

Per capita energy consumption (fossil)

approx. 2 kW per person

Daily oil consumption

100 mio. barrels oil/day (appr. 159 litres)

Austria, summer, cloudless, noon

800 W/m2

13.

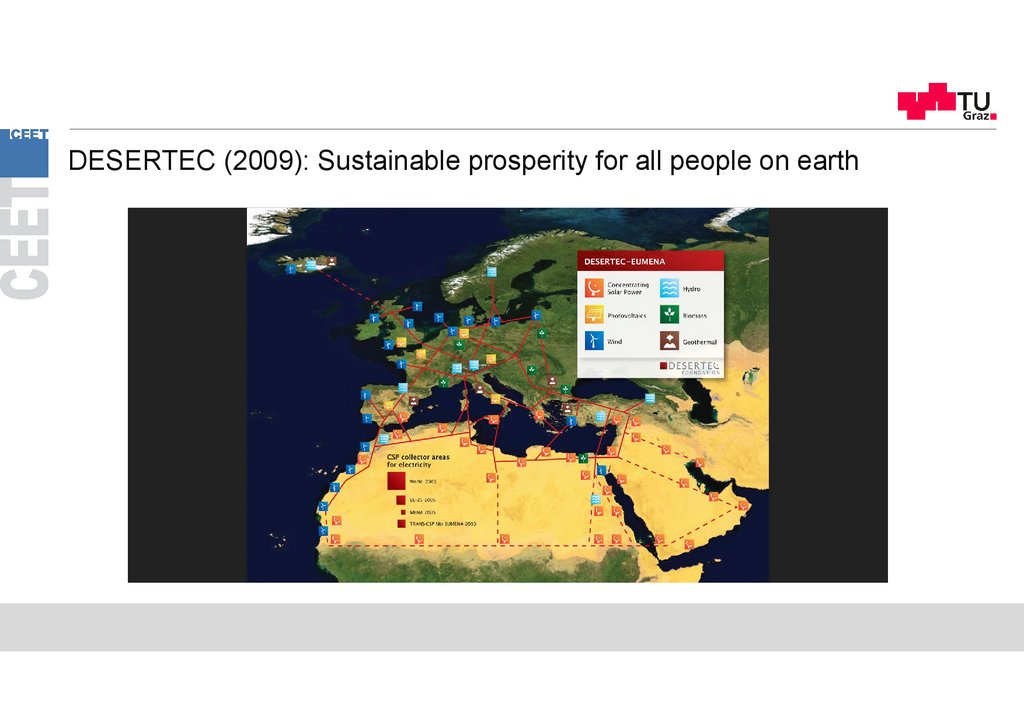

DESERTEC (2009): Sustainable prosperity for all people on earth14.

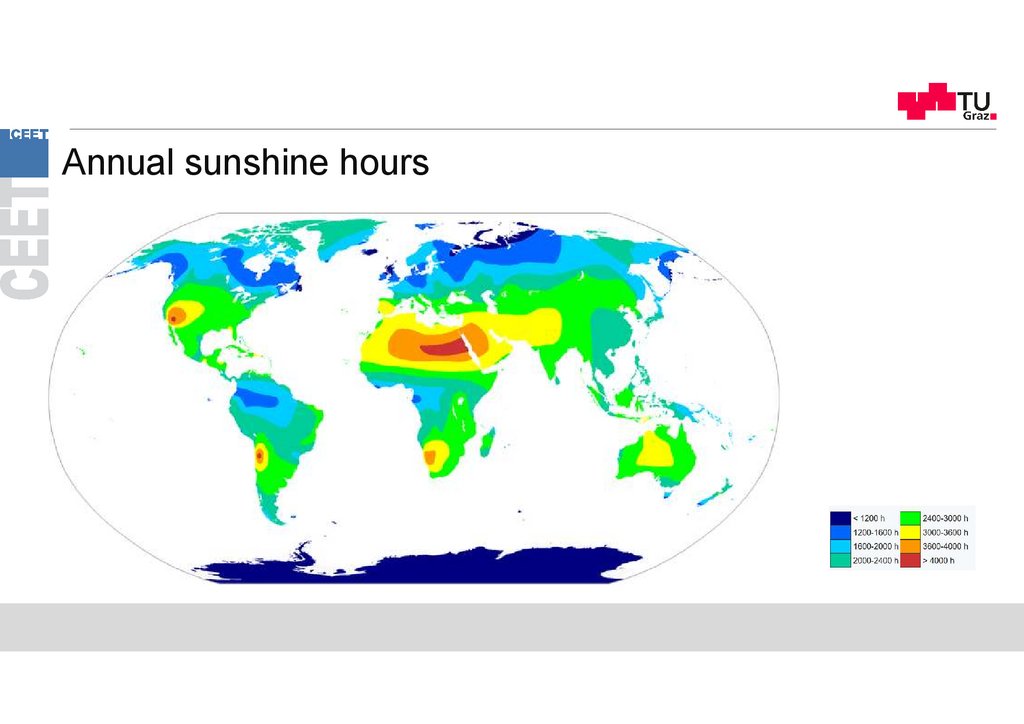

Annual sunshine hours15

15.

1616.

Crude oil trade flows worldwide (Mt/a)17

bp Statistical Review of World Energy 2021

17.

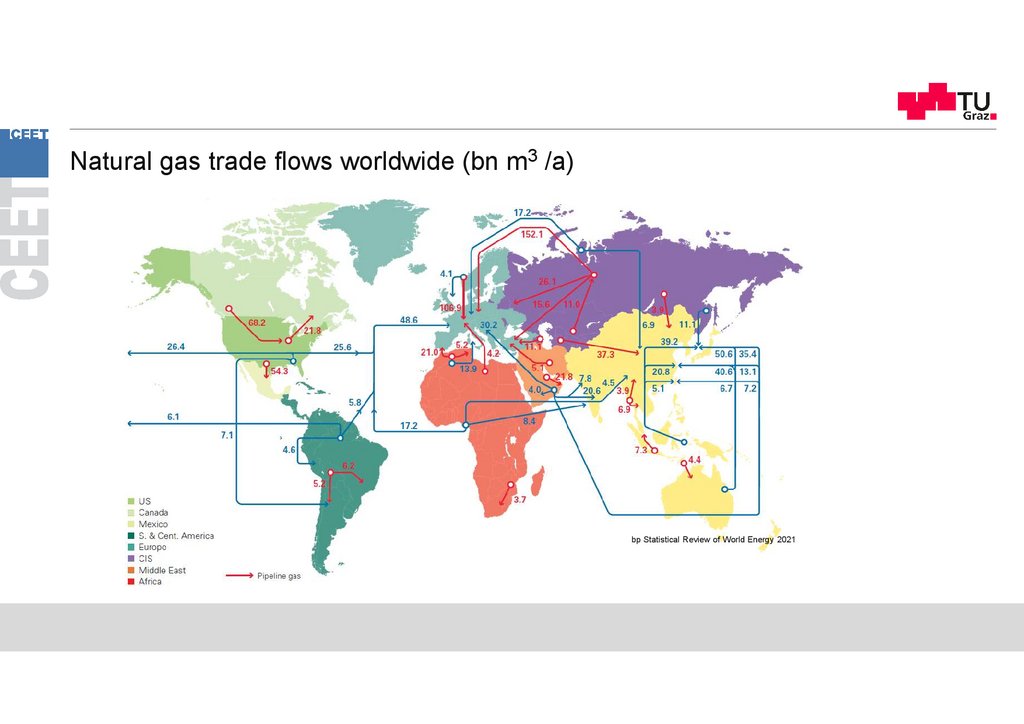

Natural gas trade flows worldwide (bn m3 /a)18

bp Statistical Review of World Energy 2021

18.

Wind and solar energy are now competitive19

19.

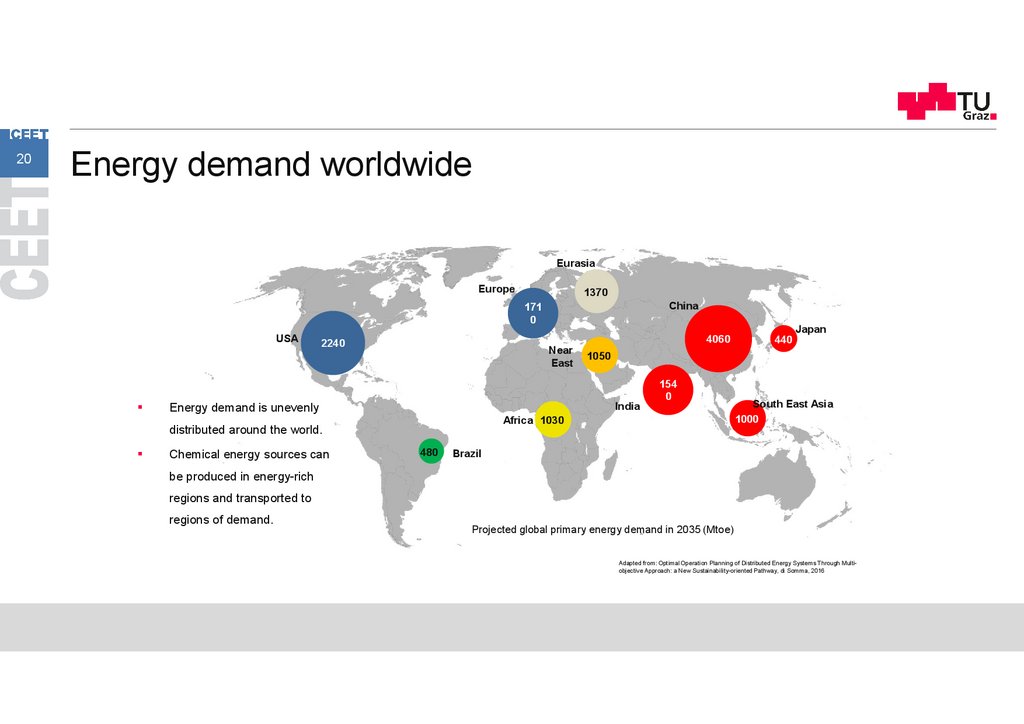

20Energy demand worldwide

Eurasia

Europe

1370

China

171

0

USA

2240

Near

East

Chemical energy sources can

154

0

Africa 1030

480

440

Japan

1050

India

Energy demand is unevenly

distributed around the world.

4060

South East Asia

1000

Brazil

be produced in energy-rich

regions and transported to

regions of demand.

Projected global primary energy demand in 2035 (Mtoe)

Adapted from: Optimal Operation Planning of Distributed Energy Systems Through Multiobjective Approach: a New Sustainability-oriented Pathway, di Somma, 2016

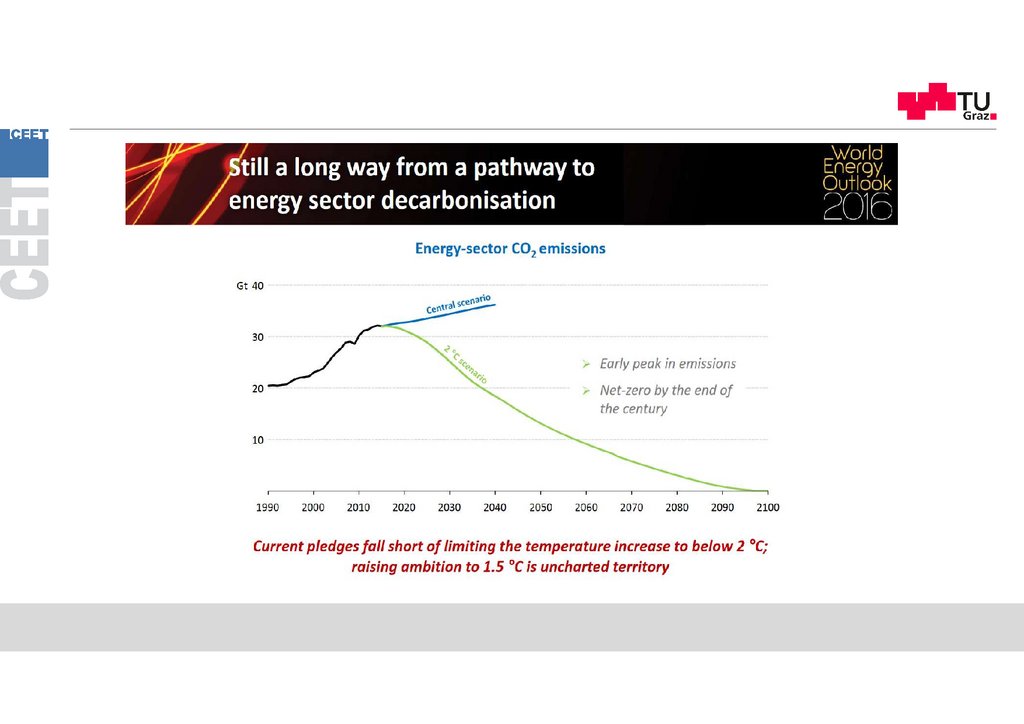

20.

World Energy Outlook• The World Energy Outlook does not provide a forecast of what will

happen. Instead, it provides a set of scenarios that explore different

possible futures, the actions – or inactions – that bring them about and

the interconnections between different parts of the system.

• Scenarios are used to present quantitative projections of longterm

energy trends. There are three core scenarios, which differ in their

assumptions about the evolution of energy-related government policies:

NZE / APS / STEPS

(former report: New (Stated) Policies Scenario; Current Policies

Scenario; Sustainable Development Scenario).

(Source: IEA, WEO 2018)

21.

Main scenarios in the outlook WEO-2021Net Zero Emissions by 2050 Scenario (NZE), which sets out a narrow but achievable pathway for the global energy

sector to achieve net zero CO2 emissions by 2050 to an achievable roadmap to a 1.5 °C stabilisation in rising global

temperatures.

Announced Pledges Scenario (APS), which assumes that all climate commitments made by governments around the

world, including Nationally Determined Contributions (NDCs) and longer term net zero targets, will be met in full and on

time. To 2030, low emissions sources of power generation account for the vast majority of capacity additions, with

annual additions of solar PV and wind approaching 500 gigawatts (GW) by 2030. Efficiency gains mean that global

energy demand plateaus post-2030. The global average temperature rise in 2100 is held to around 2.1 °C above preindustrial levels, although this scenario does not hit net zero emissions, so the temperature trend has still not stabilised.

Stated Policies Scenario (STEPS), which reflects current policy settings based on a sector-by-sector assessment of the

specific policies that are in place, as well as those that have been announced by governments around the world. In the

STEPS, almost all of the net growth in energy demand to 2050 is met by low emissions sources, but that leaves

annual emissions at around current levels. As a result, global average temperatures are still rising when they hit 2.6 °C

above pre-industrial levels in 2100. This growth largely comes from emerging market and developing economies as they

build up their nationwide infrastructure.

(Source: IEA, WEO 2021)

22.

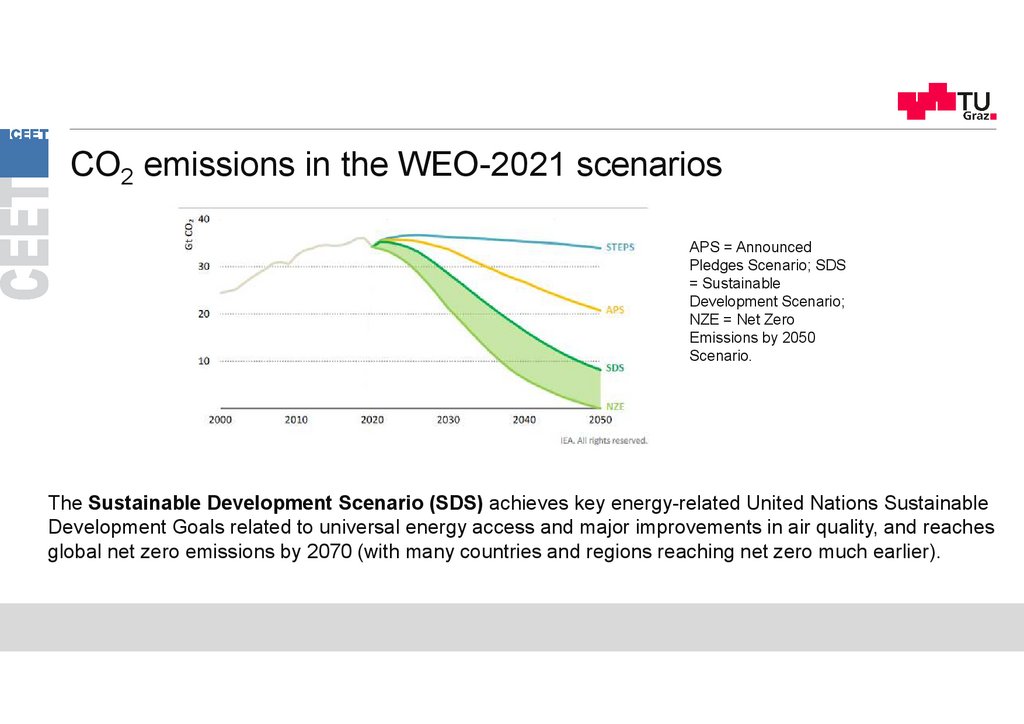

CO2 emissions in the WEO-2021 scenariosAPS = Announced

Pledges Scenario; SDS

= Sustainable

Development Scenario;

NZE = Net Zero

Emissions by 2050

Scenario.

The Sustainable Development Scenario (SDS) achieves key energy-related United Nations Sustainable

Development Goals related to universal energy access and major improvements in air quality, and reaches

global net zero emissions by 2070 (with many countries and regions reaching net zero much earlier).

23.

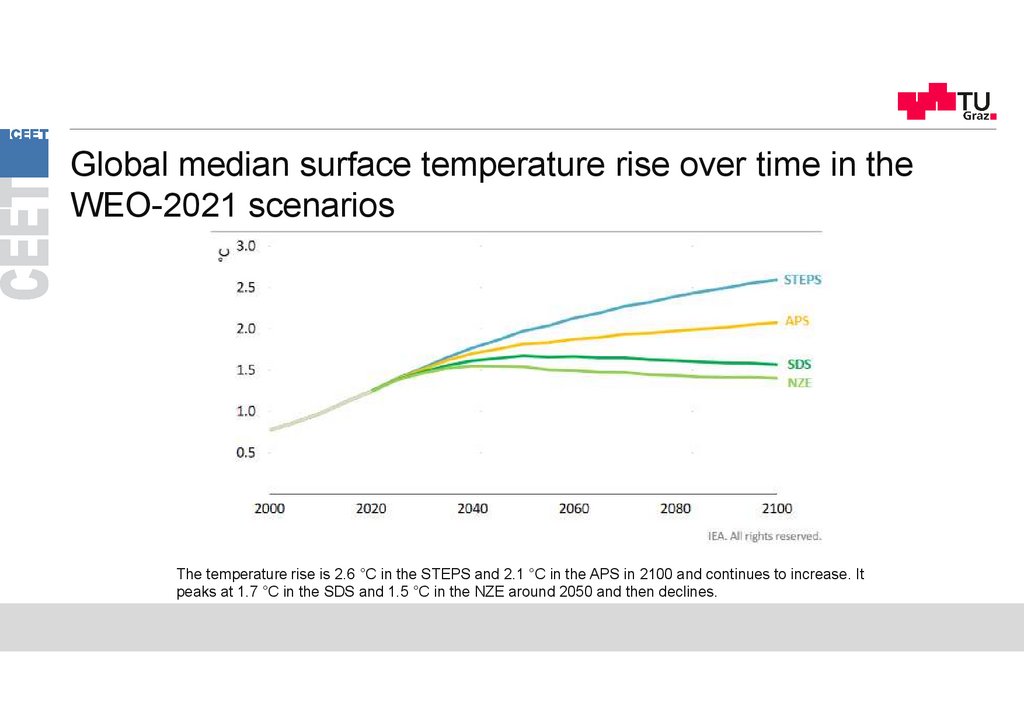

Global median surface temperature rise over time in theWEO-2021 scenarios

The temperature rise is 2.6 °C in the STEPS and 2.1 °C in the APS in 2100 and continues to increase. It

peaks at 1.7 °C in the SDS and 1.5 °C in the NZE around 2050 and then declines.

24.

Uncertaintiesthe scenarios are intended to demonstrate how markets could evolve under certain

conditions.

Population, even by region, is unlikely to deviate much from the assumptions used

(World population is projected to grow from an estimated 6.8 billion in 2010 to 8.6 billion

in 2035, or by some 1.7 billion new energy consumers.)

And we can be reasonably confident about how technology is likely to evolve in the

short to medium term, even if there are surprises, such as the improved technologies

that have recently unlocked huge unconventional gas and oil resources in the United

States and elsewhere.

Price remains an important determinant of energy trends.

“it is tough to make predictions,

especially about the future”

Niels Bohr

25.

TechnologyThe types of energy technology that are developed and deployed, for application to energy

supply and energy use, will affect investment decisions, the cost of supply of different forms of

energy, and the level and composition of future energy demand.

• These assumptions vary by fuel, end-use sector, location and scenario, and are based on our

assessment of the current stage of technological development, how far the optimal scope for

deployment will be realised and the potential for further gains, as well as our analysis of how

effectively different policy assumptions will drive technological advances.

• While no breakthrough technologies are deployed in any of the scenarios, we assume that

technologies that are in use today or are approaching the commercialisation phase will achieve

further cost reductions as a result of increased learning and deployment.

• On the supply side, exploration and production techniques are also expected to improve, which

could lower unit production costs and open up new opportunities for developing resources.

26.

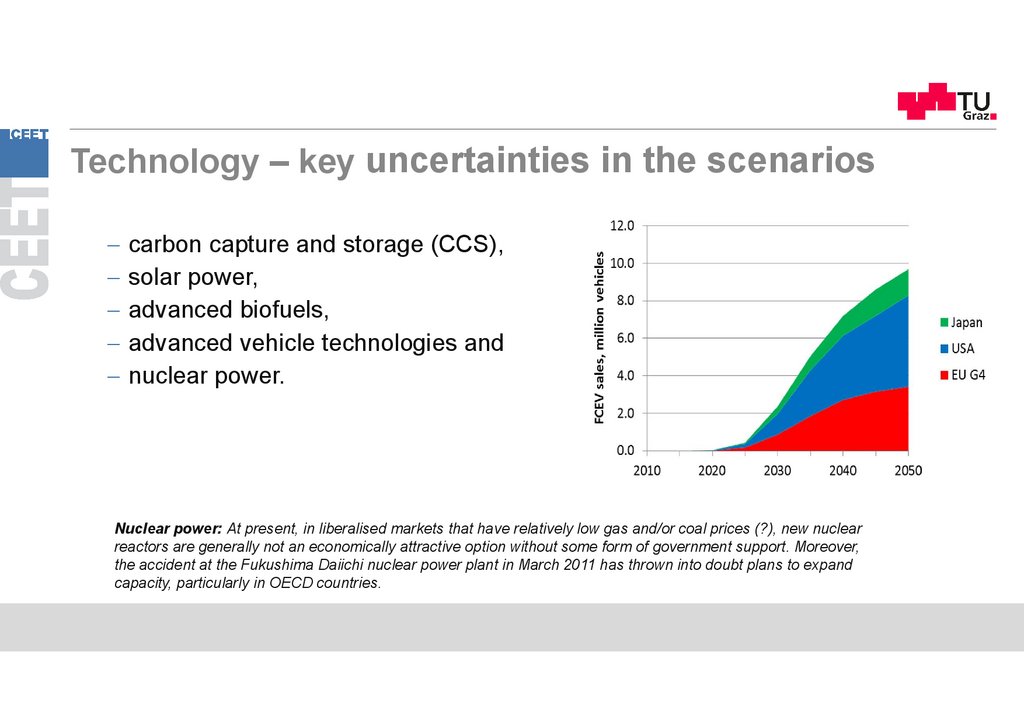

Technology – key uncertainties in the scenarioscarbon capture and storage (CCS),

solar power,

advanced biofuels,

advanced vehicle technologies and

nuclear power.

Nuclear power: At present, in liberalised markets that have relatively low gas and/or coal prices (?), new nuclear

reactors are generally not an economically attractive option without some form of government support. Moreover,

the accident at the Fukushima Daiichi nuclear power plant in March 2011 has thrown into doubt plans to expand

capacity, particularly in OECD countries.

27.

Key measures to close the gap between today’s pledges and a 1.5 °Ctrajectory

A massive additional push for clean electrification that requires a doubling of solar PV and

wind deployment relative to the APS; a major expansion of other low-emissions generation.

Accelerating the decarbonisation of the electricity mix is the single most important lever: it closes

more than one-third of the emissions gap between the APS and NZE. The low costs of wind

and solar PV mean that more than half of the additional emissions reductions could be gained

at no cost to electricity consumers.

A relentless focus on energy efficiency, together with measures to temper energy service

demand through materials efficiency and behavioural change. We estimate that almost 80% of

the additional energy efficiency gains in the NZE over the next decade result in cost savings to

consumers.

(Source: IEA, WEO 2021)

28.

Key measures to close the gap between today’s pledges and a 1.5 °Ctrajectory

A broad drive to cut methane emissions from fossil fuel operations. Rapid reductions in methane

emissions are a key tool to limit near-term global warming, and the most cost-effective abatement

opportunities are in the energy sector, particularly in oil and gas operations. Methane abatement is

not addressed quickly or effectively enough by simply reducing fossil fuel use; concerted efforts from

governments and industry are vital to secure the emissions cuts that close nearly 15% of the gap to

the NZE.

A big boost to clean energy innovation. This is another crucial gap to be filled in the 2020s, even

though most of the impacts on emissions are not felt until later. All the technologies needed to

achieve deep emissions cuts to 2030 are available. But almost half of the emissions reductions

achieved in the NZE in 2050 come from technologies that today are at the demonstration or

prototype stage. These are particularly important to address emissions from iron and steel, cement

and other energy-intensive industrial sectors – and also from long-distance transport. Today’s

announced pledges fall short of key NZE milestones for the deployment of hydrogen-based and

other low-carbon fuels, as well as carbon capture, utilisation and storage

(CCUS).

(Source: IEA, WEO 2021)

29.

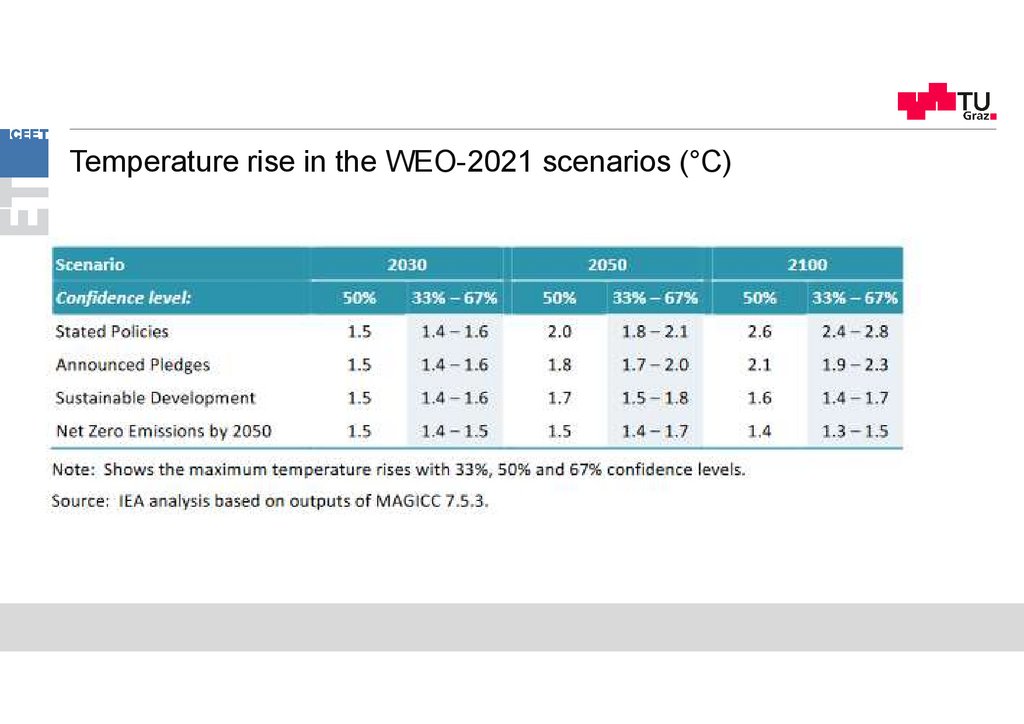

Temperature rise in the WEO-2021 scenarios (°C)30.

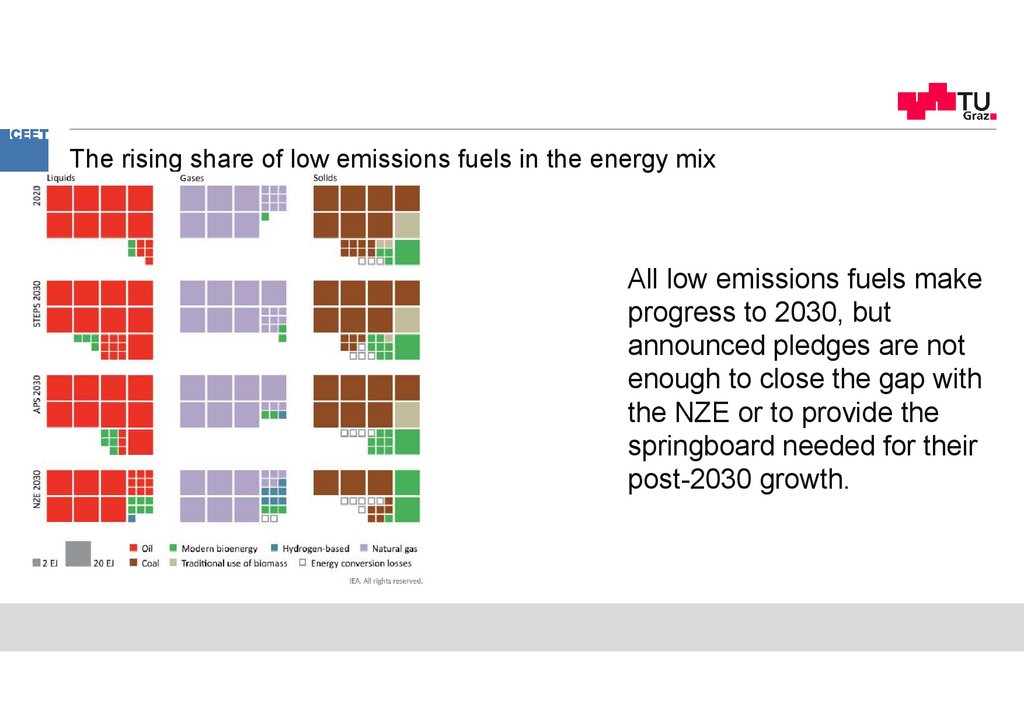

The rising share of low emissions fuels in the energy mixAll low emissions fuels make

progress to 2030, but

announced pledges are not

enough to close the gap with

the NZE or to provide the

springboard needed for their

post-2030 growth.

31.

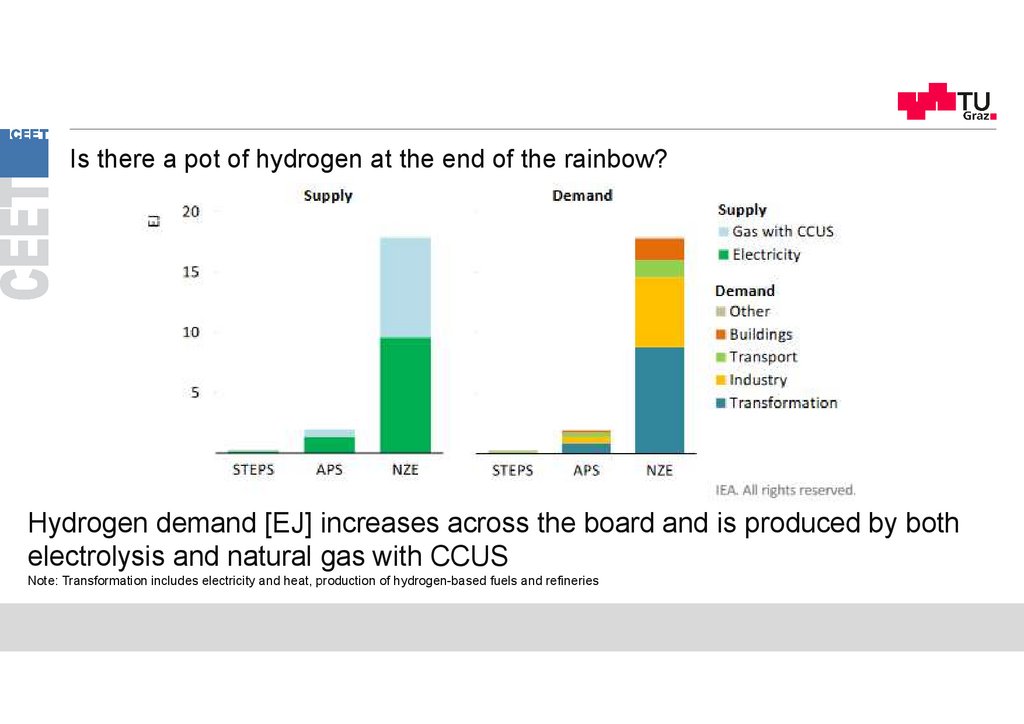

Is there a pot of hydrogen at the end of the rainbow?Hydrogen demand [EJ] increases across the board and is produced by both

electrolysis and natural gas with CCUS

Note: Transformation includes electricity and heat, production of hydrogen-based fuels and refineries

32.

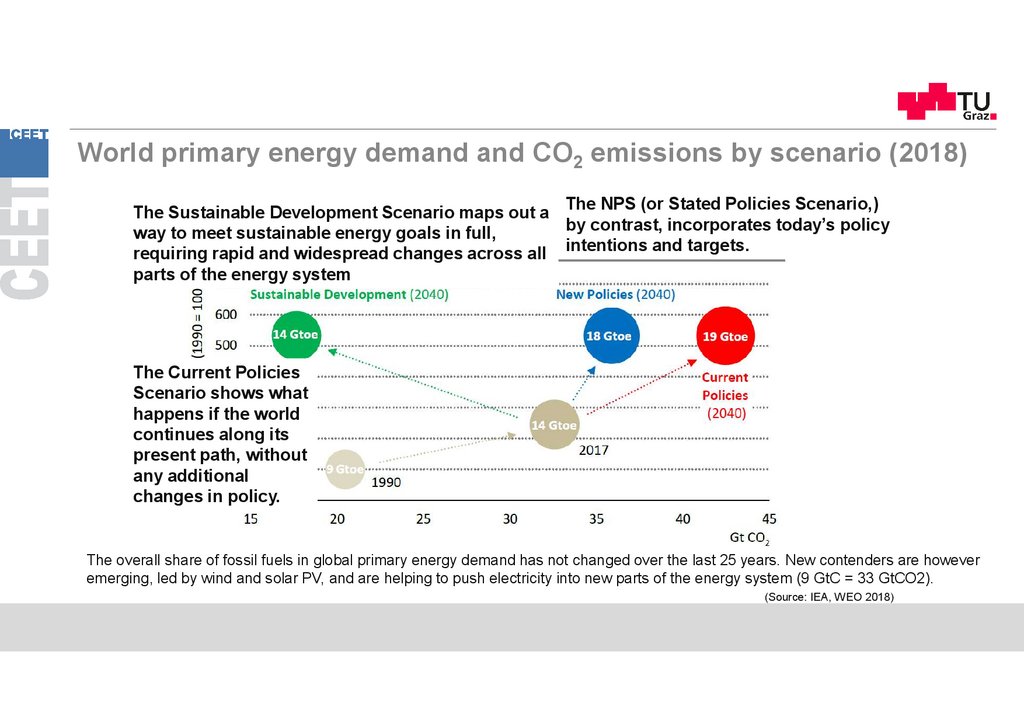

World primary energy demand and CO2 emissions by scenario (2018)The Sustainable Development Scenario maps out a The NPS (or Stated Policies Scenario,)

by contrast, incorporates today’s policy

way to meet sustainable energy goals in full,

requiring rapid and widespread changes across all intentions and targets.

parts of the energy system

The Current Policies

Scenario shows what

happens if the world

continues along its

present path, without

any additional

changes in policy.

The overall share of fossil fuels in global primary energy demand has not changed over the last 25 years. New contenders are however

emerging, led by wind and solar PV, and are helping to push electricity into new parts of the energy system (9 GtC = 33 GtCO2).

(Source: IEA, WEO 2018)

33.

34.

A Brief History of CO2 Emissions https://youtu.be/EQ7S0D1iucYPotsdam Institute for Climate Impact Research

https://youtu.be/EQ7S0D1iucY

35.

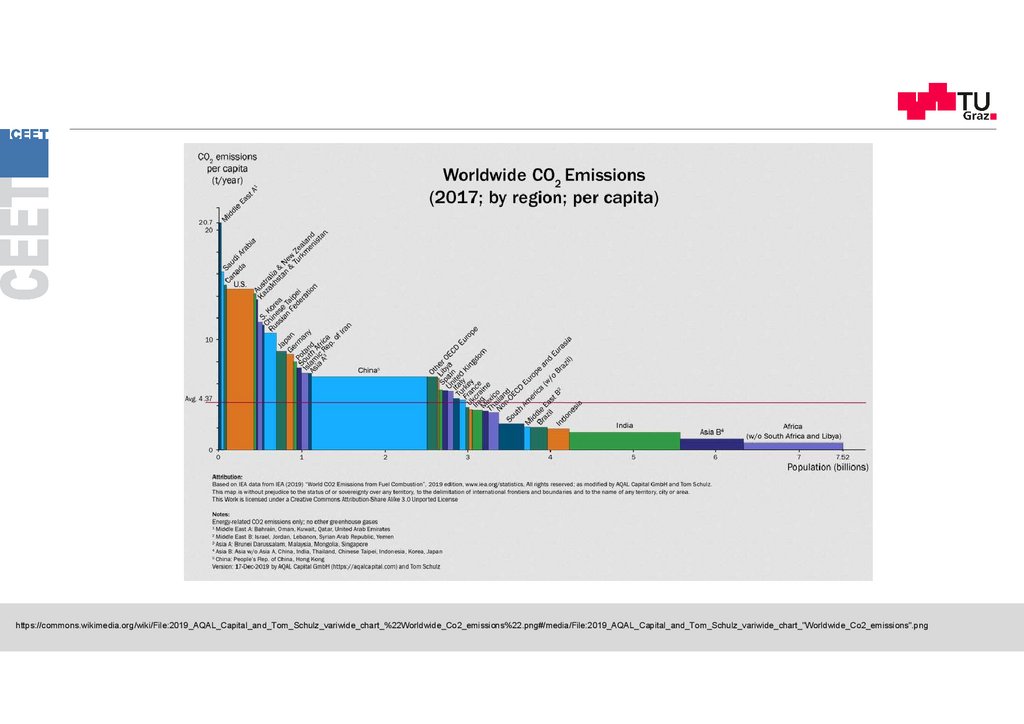

https://commons.wikimedia.org/wiki/File:2019_AQAL_Capital_and_Tom_Schulz_variwide_chart_%22Worldwide_Co2_emissions%22.png#/media/File:2019_AQAL_Capital_and_Tom_Schulz_variwide_chart_"Worldwide_Co2_emissions".png36.

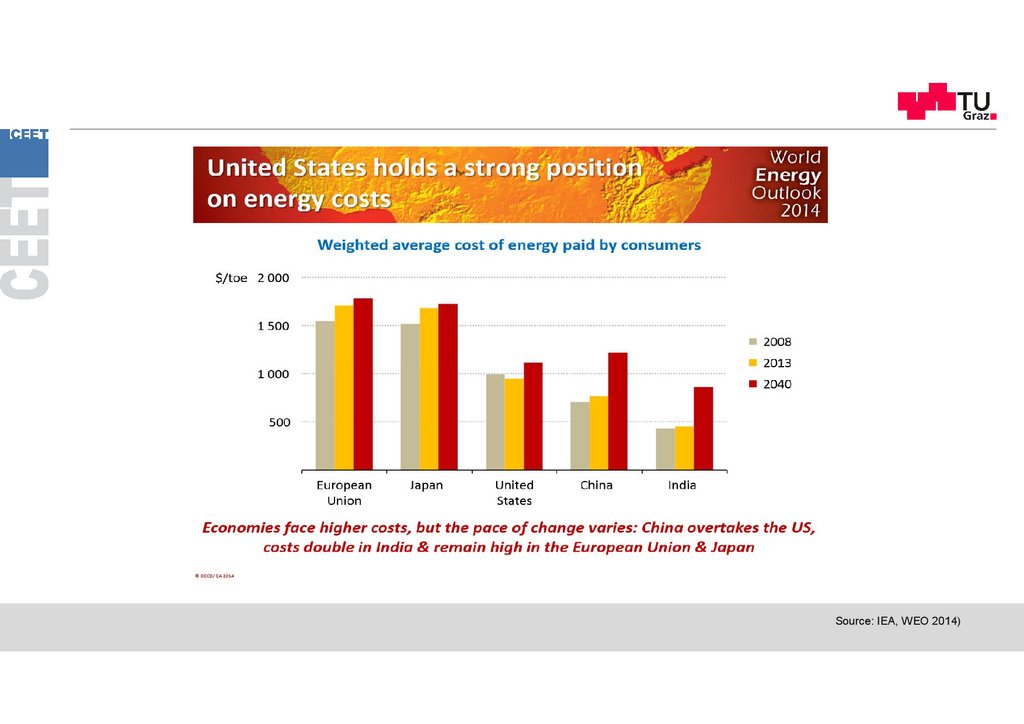

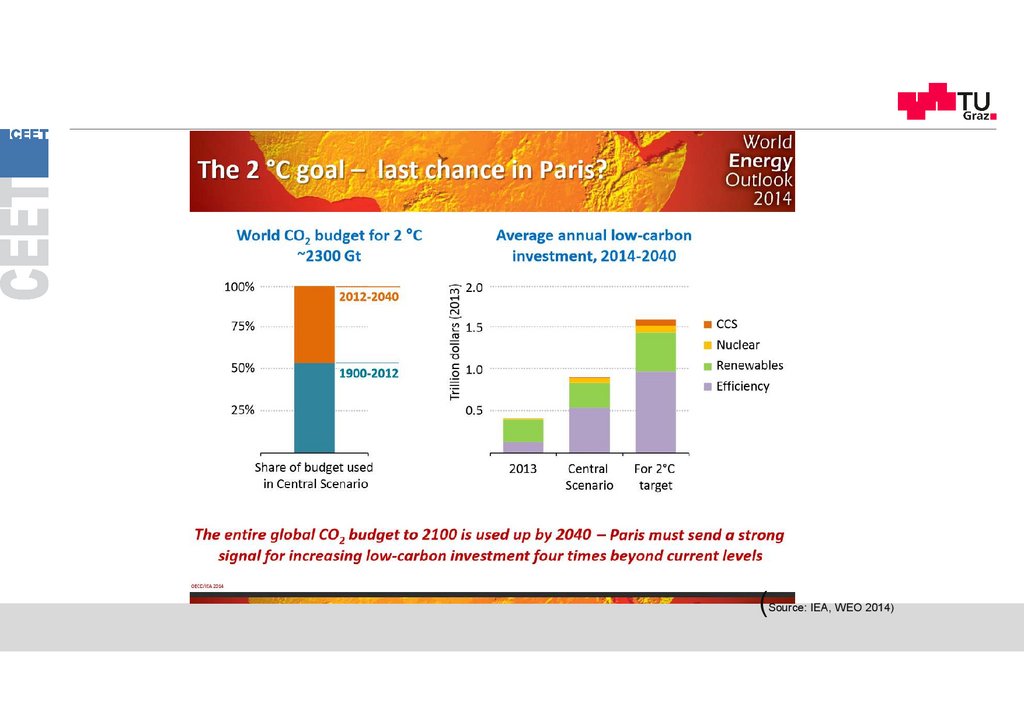

Source: IEA, WEO 2014)37.

(Source: IEA, WEO 2014)38.

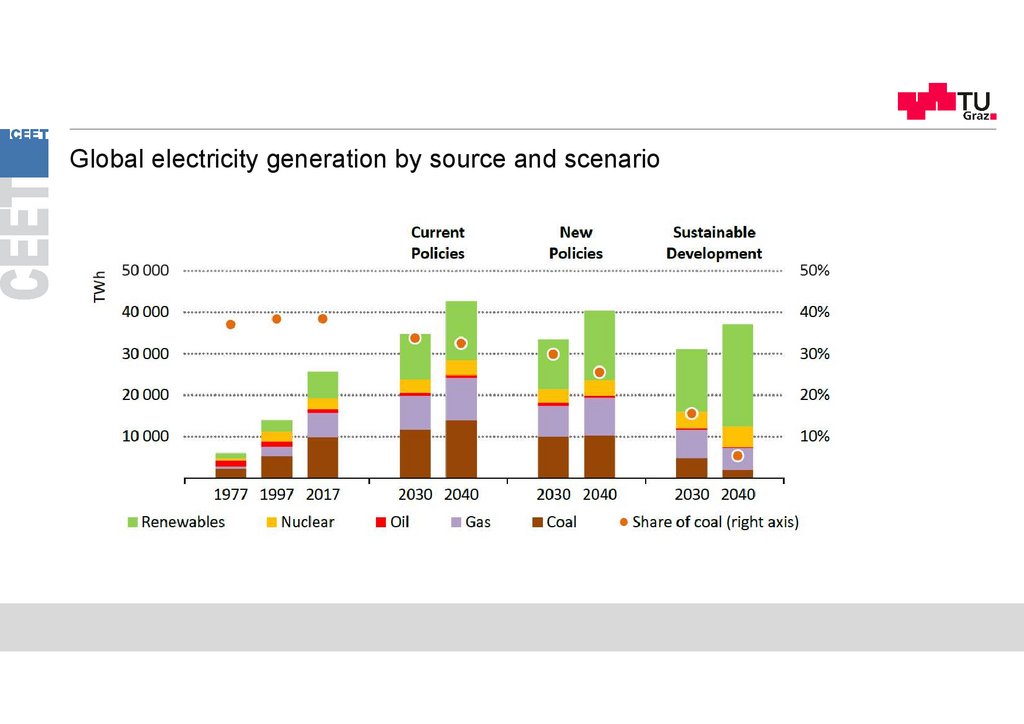

Global electricity generation by source and scenario39.

40.

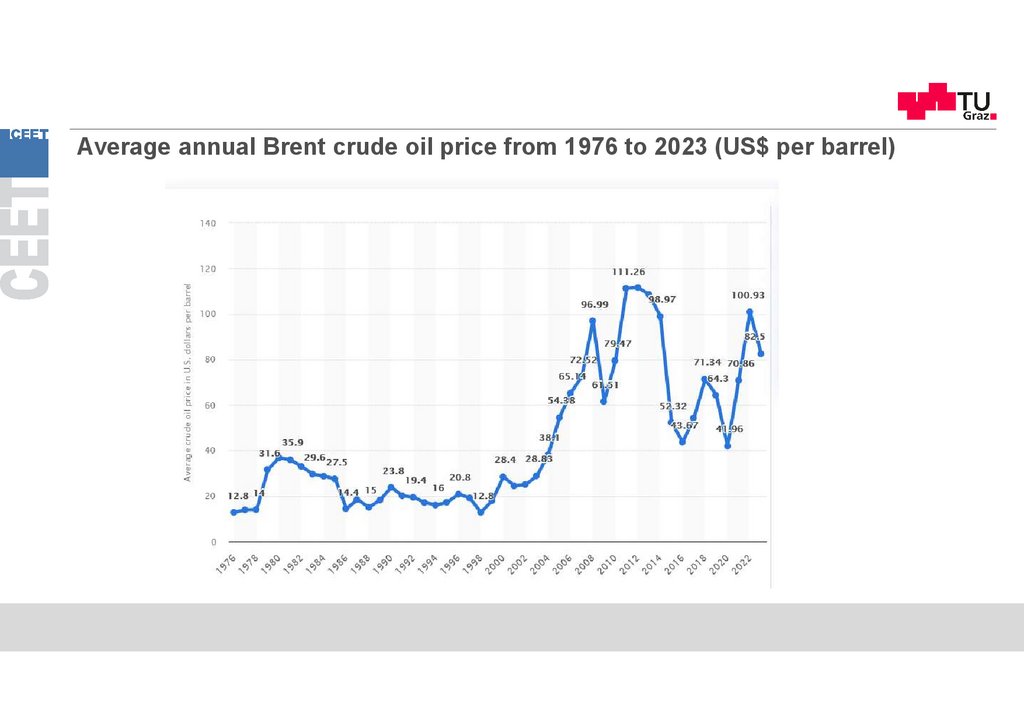

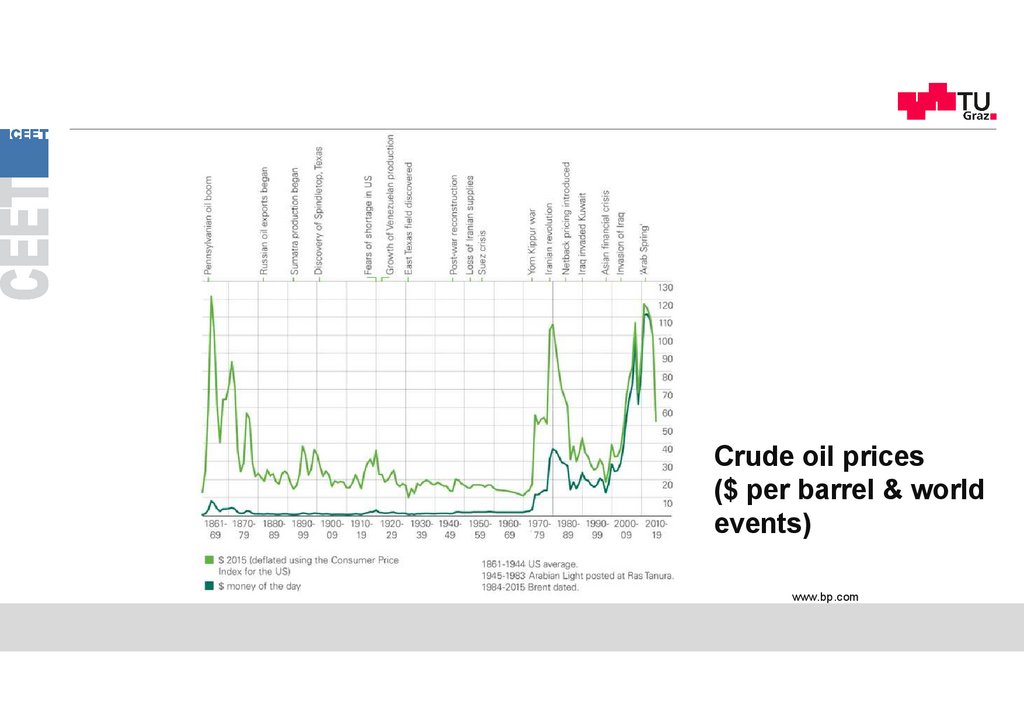

Average annual Brent crude oil price from 1976 to 2023 (US$ per barrel)41.

Crude oil prices($ per barrel & world

events)

www.bp.com

42.

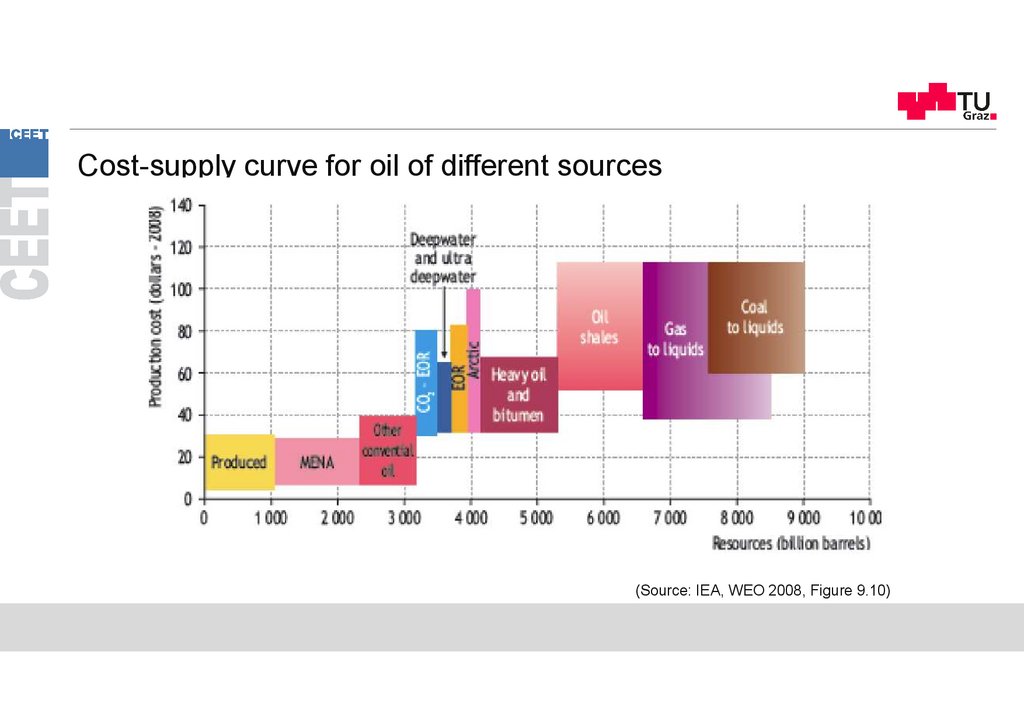

Cost-supply curve for oil of different sources(Source: IEA, WEO 2008, Figure 9.10)

43.

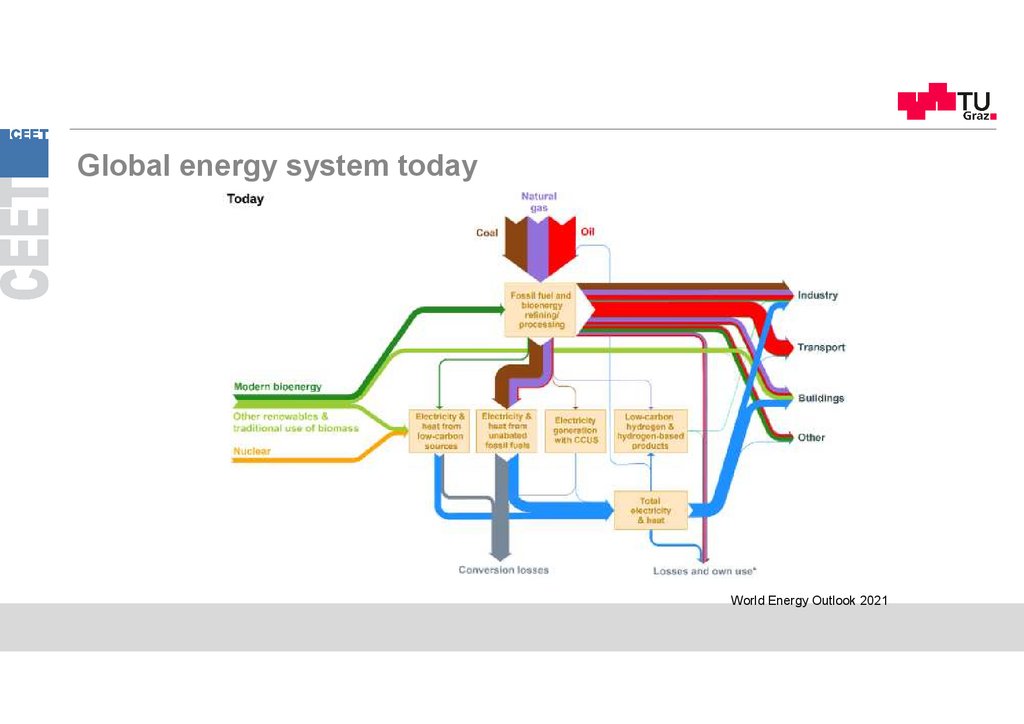

Global energy system todayWorld Energy Outlook 2021

44.

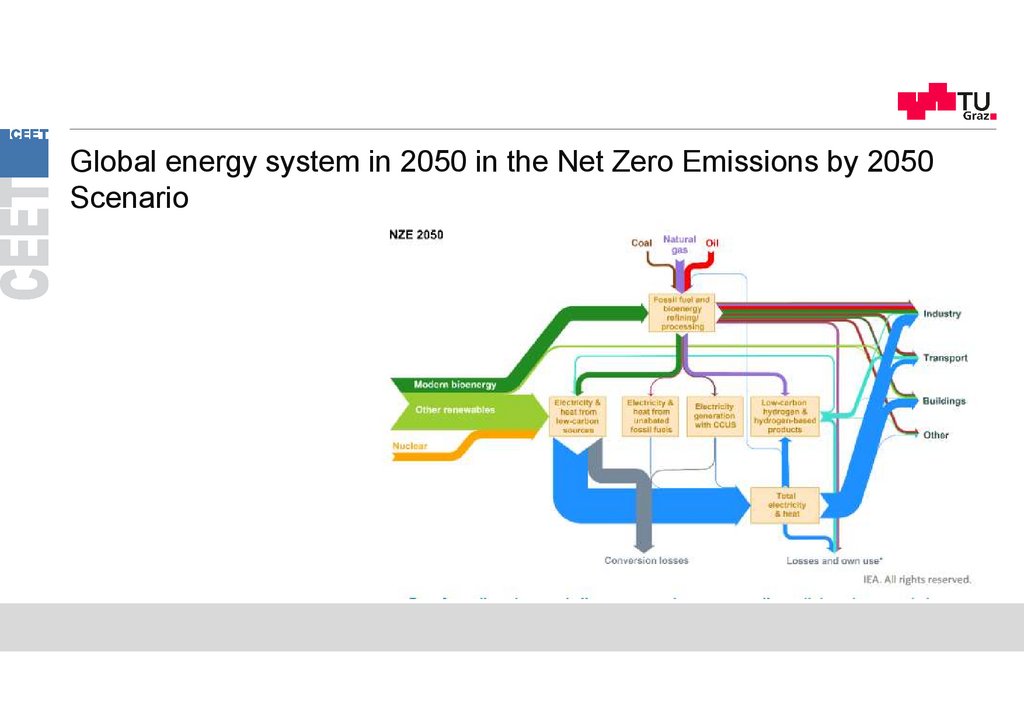

Global energy system in 2050 in the Net Zero Emissions by 2050Scenario

45.

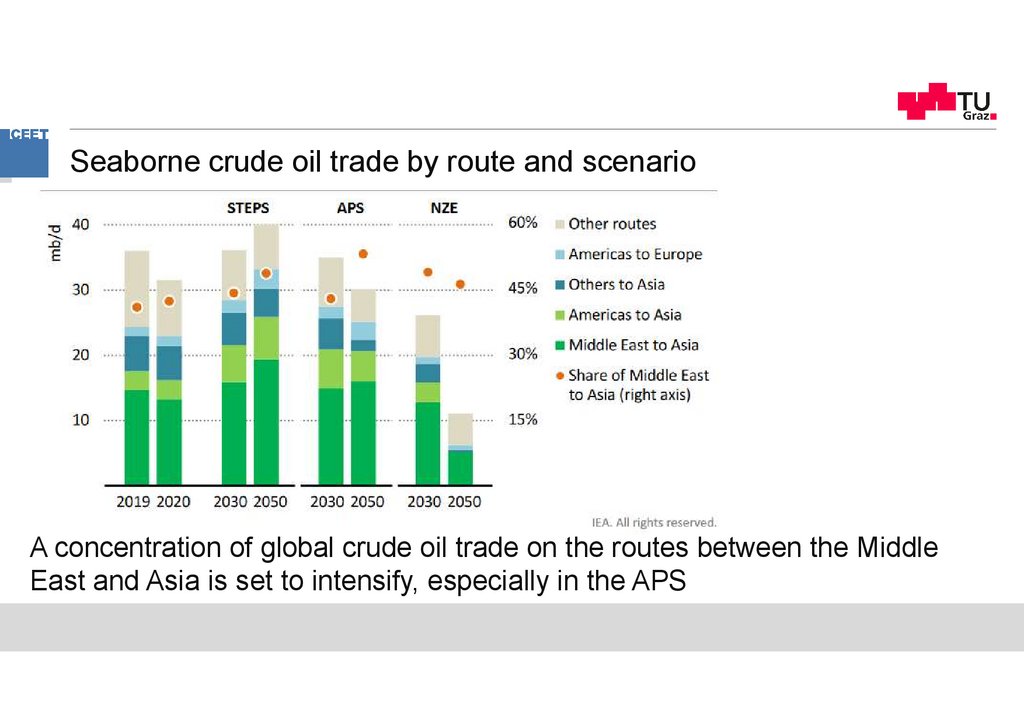

Seaborne crude oil trade by route and scenarioA concentration of global crude oil trade on the routes between the Middle

East and Asia is set to intensify, especially in the APS

46.

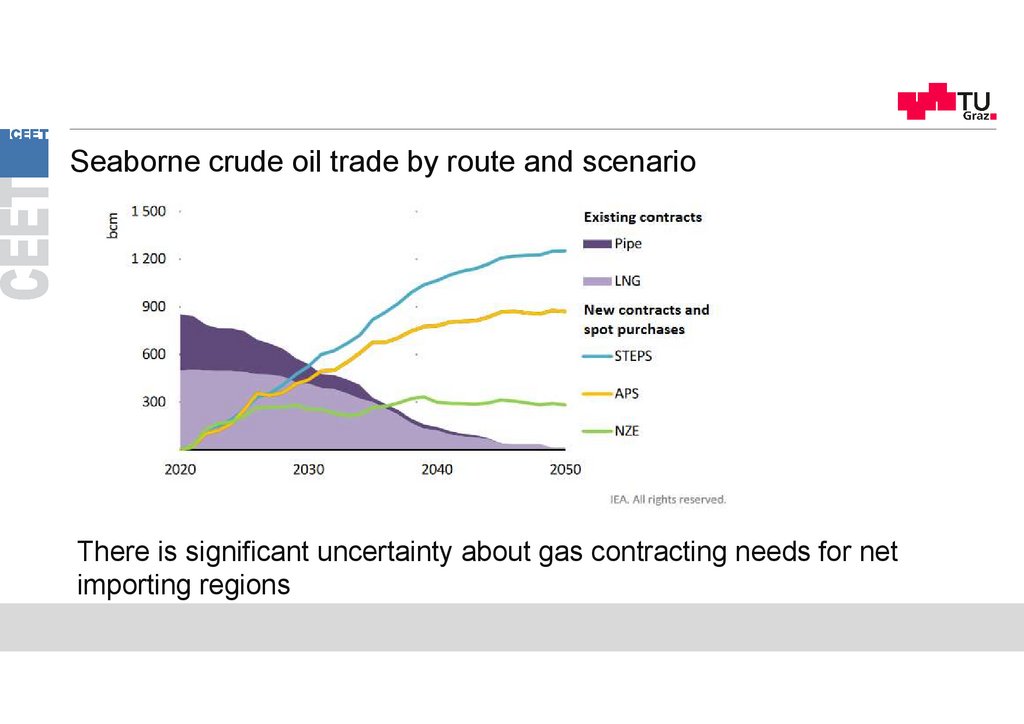

Seaborne crude oil trade by route and scenarioThere is significant uncertainty about gas contracting needs for net

importing regions

47.

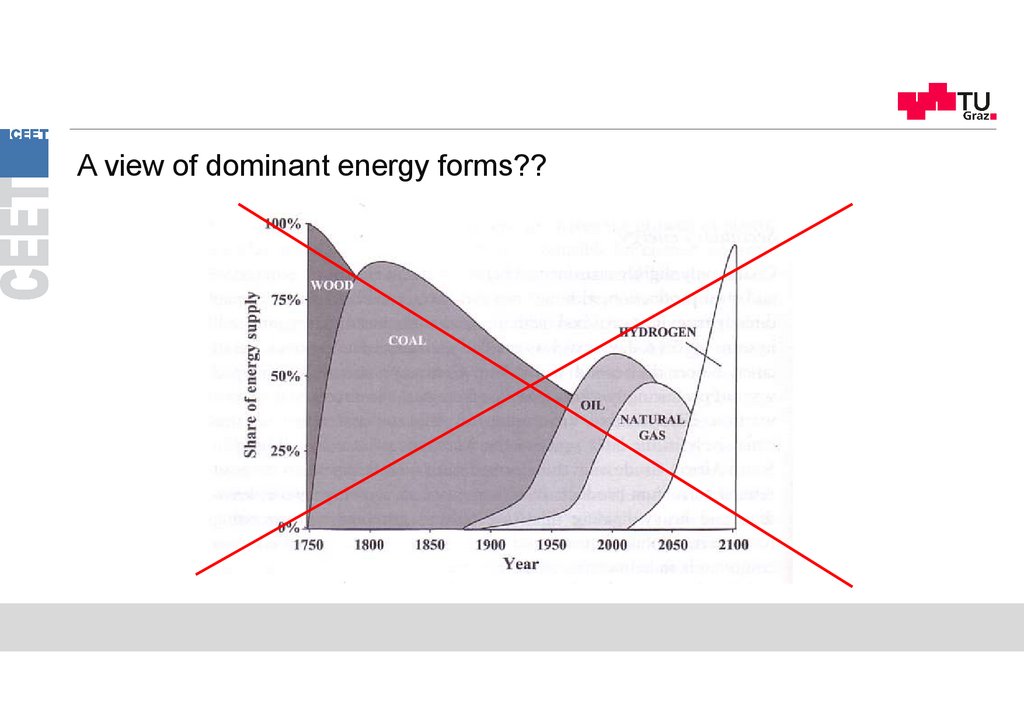

A view of dominant energy forms??48.

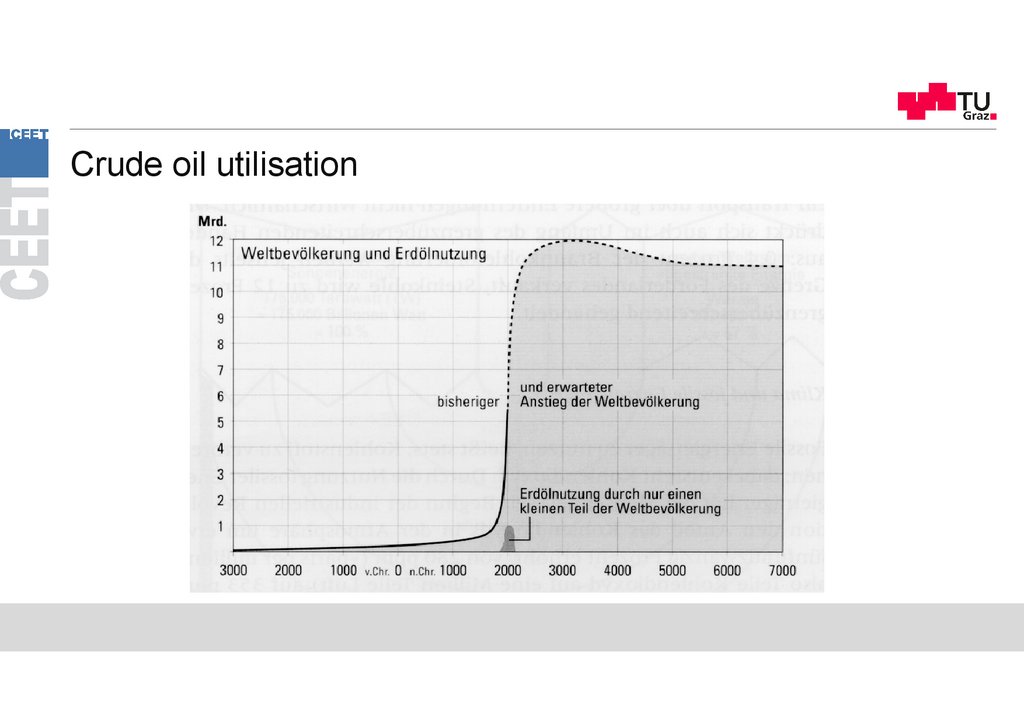

Crude oil utilisation49.

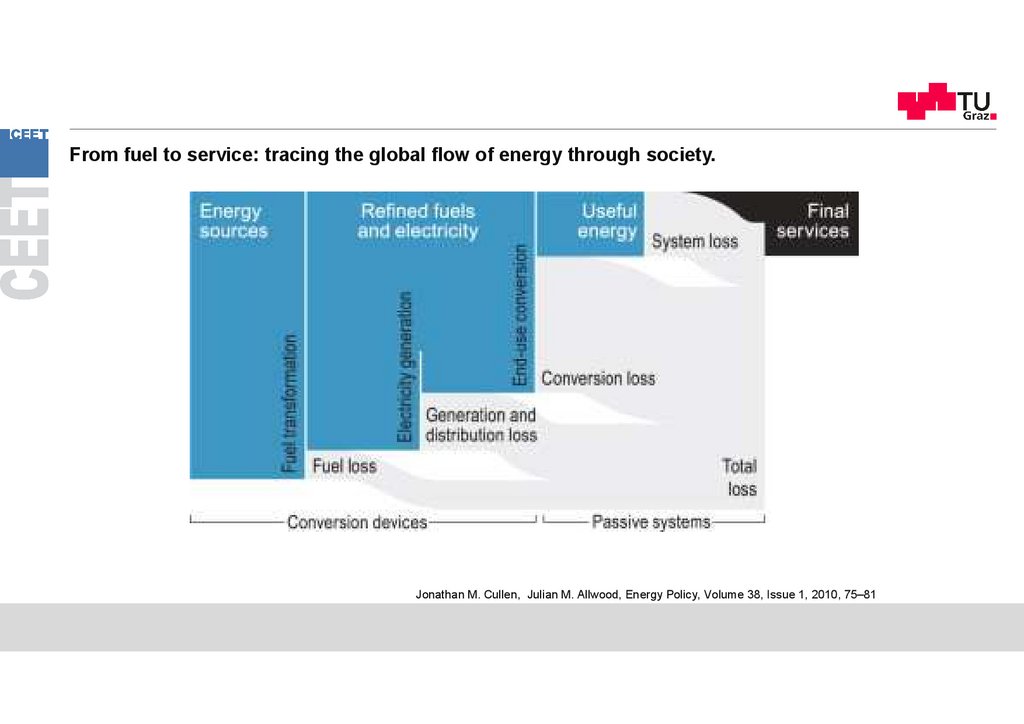

From fuel to service: tracing the global flow of energy through society.Jonathan M. Cullen, Julian M. Allwood, Energy Policy, Volume 38, Issue 1, 2010, 75–81

50.

From fuel to service: tracing the global flow of energy through society.Jonathan M. Cullen, Julian M. Allwood, Energy Policy, Volume 38, Issue 1, 2010, 75–81

51.

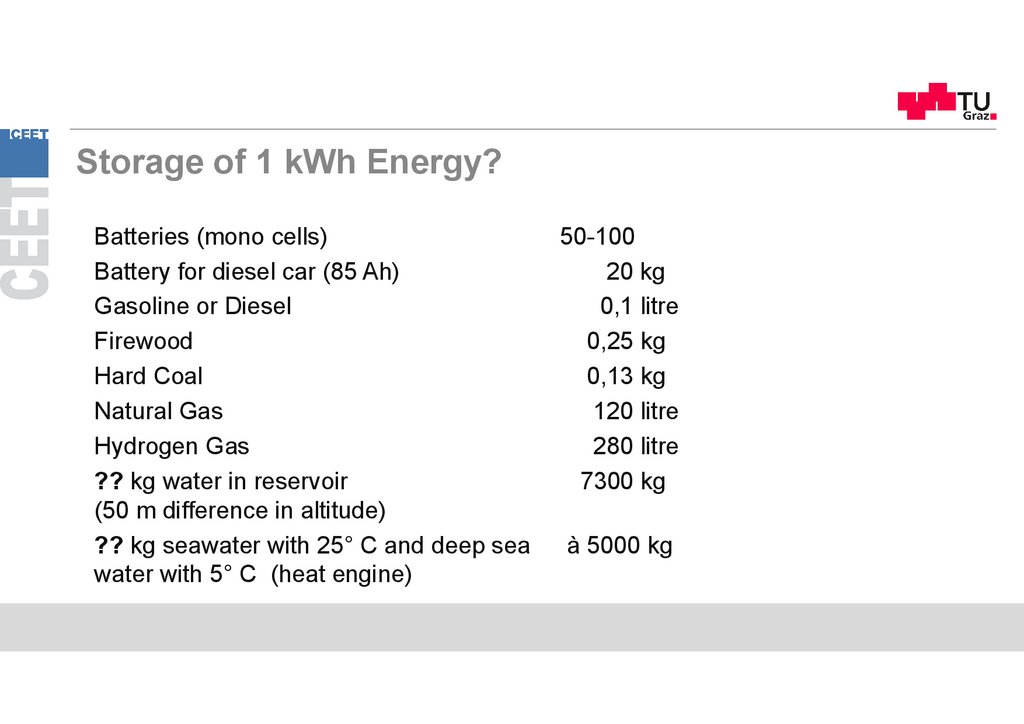

Storage of 1 kWh Energy?Batteries (mono cells)

Battery for diesel car (85 Ah)

Gasoline or Diesel

Firewood

Hard Coal

Natural Gas

Hydrogen Gas

?? kg water in reservoir

(50 m difference in altitude)

?? kg seawater with 25° C and deep sea

water with 5° C (heat engine)

50-100

20 kg

0,1 litre

0,25 kg

0,13 kg

120 litre

280 litre

7300 kg

à 5000 kg

52.

1 kWh (without losses) is able to …Lift 1 t Masse ?? m

Lift ?? t Masse 1 m high

367 m

367 t

Heat ?? litre of water up

from 10°C to 99°C

9,5 l

Fill a 30 litre compressed

air cylinder to ?? bar

200 bar

Accelerate a mass of

1 ton from 0 to ?? km/h

305 km/h

53.

Regenerative Energy Supply AustriaSolar radiation

1100 kWh/m2a

Solar radiation, summer

day, no clouds, 12:00

800 W/m2

Worldwide energy

consumption

approx. 14 Gtoe

54.

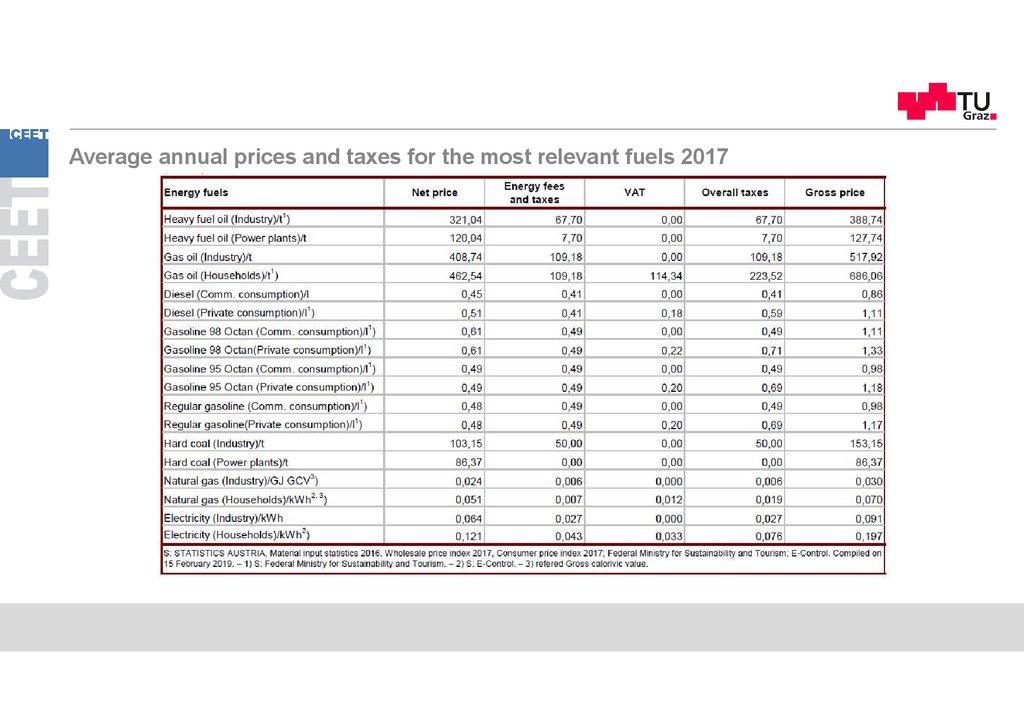

Average annual prices and taxes for the most relevant fuels 201755.

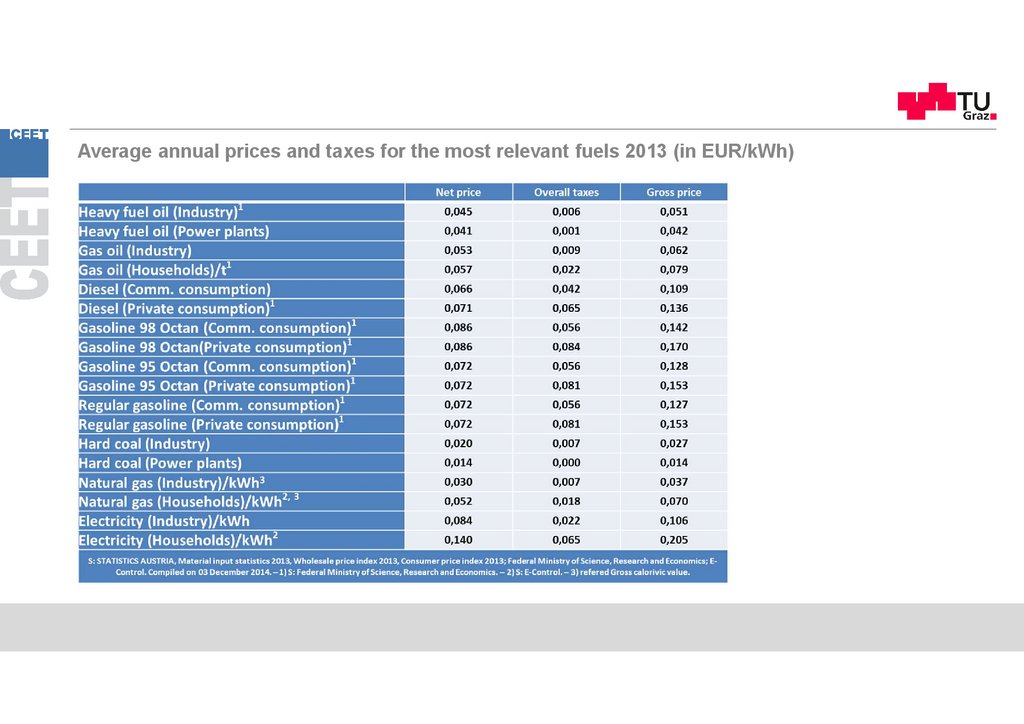

Average annual prices and taxes for the most relevant fuels 2013 (in EUR/kWh)56.

Thank you!57

www.ceet.tugraz.at

Master-Infoveranstaltung der Studienvertretung Verfahrenstechnik