")

")

management

management business

businessSimilar presentations:

")

Accounting for Partnership. Topic 9

1. Topic 9: Accounting for Partnership

1ACC30305 Principles of Accounting

Topic 9:

Accounting for

Partnership

2. Learning Objectives

2Learning Objectives

1.

2.

3.

4.

5.

6.

Explain the characteristics and types of a partnership.

Explain the contents of a partnership agreement.

Explain accounting for a partnership business.

Prepare the partners’ capital and current accounts.

Prepare the Financial Statements of a partnership

business.

Compute allocation of profit / loss to the partners.

3. Learning Objective 1

3Learning Objective 1

Identify the characteristics and types of

partnerships

4. The need for a partnership

4The need for a partnership

(a)Additional capital

an incoming partner may be able to bring in the

additional capital required to expand the business.

(b)Additional expertise

new skills (e.g. technical skills required for the new line

of business undertaken by the partnership.

(c) Additional management time

to manage the expanded business operations

5. What are the Characteristics and Types of Partnerships?

5What are the

Characteristics

and

Types of

Partnerships?

Registration

Registered with the Companies Commission of Malaysia

under the Business Registration Act 1956 & 1957.

Capital

Contributed by partners according to the Partnership

Agreement or Partnership Act 1961.

Ownership

Owned by between 2 and 20 partners.

Management

Control

& Managed and controlled by partners or by a board which

consists of a few partners.

Liability

Each partner has unlimited liability for the partnership’s

debt. If the business fails and the assets are not enough to

cover the debts, the accounts payable have a right against

the partner’s / partners’ personal properties.

Profit or Loss

Shared by partners according to their profit-sharing ratio as

stated in the Partnership Agreement or Partnership Act

1961.

Book of accounts

No legal obligation to keep the books and prepare accounts.

6. Types of Partnerships

6Types of Partnerships

* Limited partner: A partner whose liability is limited to the amount of

capital invested by him into the partnership business. His personal

possessions cannot be taken to pay the partnership debts.

7. Partnership agreements

7Partnership agreements

It is best to have a written agreement drawn up by a lawyer or

accountant to avoid problems later on. It should include:

1)The name and nature of the business of the partnership

2)The capital to be contributed by each partner.

3)The profit/loss sharing ratio.

4)The responsibilities of each partner.

5)The rate of interest paid on capital.

6)The rate of interest charged on drawings.

7)Salaries to be paid.

8)Arrangements for admitting new partners.

9)The procedures for the exit of a partner.

8. Learning Objective 2

8Learning Objective 2

The Partnership Agreement

9. The Partnership Agreement

9The Partnership Agreement

The agreement may contains matters relating to:

(i) Capital: To state the amount to be contributed as well as any interest and the

rate of the interest.

(ii) Profit shared: To state the division of profit.

(iii) Withdrawals: To state the amount and charges.

(iv) Advances or loans: To state the rate, if any, on the advances or loans actually

made to the business.

(v) Remunerations: To state the amount if partners are to be paid salaries and /

or commissions.

10. Partnership Act 1961

10Partnership Act 1961

In Malaysia, a partnership is governed by the Partnership Act 1961.

The following terms according to Section 26 of the Partnership Act 1961 shall apply if an

agreement does not exist:

1. Profit or loss is divided equally.

2. Interest on capital is NOT allowed.

3. Remunerations: Salary and any compensation to partner are NOT allowed.

4. Interest of 8% per annum is allowed to partners who provide loans to the partnership.

5. All partners can actively managed the partnership.

6. New partner can only join upon majority agreement from existing partners.

7. The form of the partnership or the principle activities can be changed upon agreement from

all parties.

8. Accounting records must be kept diligently and can be viewed by all partners.

11. Learning Objective 3

11Learning Objective 3

Accounting for a Partnership Business

12.

12The usual business transactions for a partnership

business are no different from those of any type of

business.

● The transactions may involve those affecting assets,

liabilities, expenses and owner’s equity.

● However, each time a transaction affects a particular

partner, the account must be specifically state the name

of the partner who is involved in that transaction.

● E.g.: if a partner contribute office furniture to the

partnership business, the partner’s capital account is

affected and thus must be credited.

13. The transactions that may affect a partnership business are:

13The transactions that may affect a

partnership business are:

a)

b)

c)

d)

e)

f)

Interest on drawings.

Interest on capital.

Remunerations such as salaries and commissions.

Loan made by a partner to the business

Drawings made by a partner

Interest on loans, if any.

14. Recording Interest on Drawings

14Recording Interest on Drawings

Interest on drawings

• Partners may withdraw their share from the business.

• Withdrawal by partners will decrease the business’ cash balances.

• Therefore, intereston drawings is charged on drawings made by the partners during

the financial year. Charging interest on drawings is a means of discouraging

partners from withdrawing excessive amounts from the business.

• Interest on drawings will be added to the net profit before the profit is

between the partners.

DR. Partner’s Current Account

CR. Profit & loss appropriation account

shared

15.

15Interest on drawings – EXAMPLE:

Harry withdrew cash of RM6,000 on 1st June 2019 and RM5,200

on 1st September 2019, with interest on drawings at 5% per

annum, at the end of 31 December 2019.

The calculation is as follows:

1st June 2019 RM6,000 x 5% x 7/12 = RM175

1st Sept 2019 RM5,200 x 5% x 4/12 = RM87

Total interest on drawings at the end of December is RM262.

16. Recording Interest on Capitals

16Recording Interest on Capitals

• When partners contribute some amount of capital into the business, they are

entitled to an additional reward in terms of interest.

• The rate is usually fixed in the partnership agreement.

• The calculation of interest is based on the duration of

the capital

contributed.

• The interest is treated as a deduction of net profits before distribution

according to the profit sharing ratio in the appropriation account.

• Journal entry :

Debit Profit & Loss Appropriation Account

Credit Partners’ Current Account

17.

17Interest on capitals – EXAMPLE:

• On 1st January 2019, capital contributed by Abu is RM20,000 and that of Bakar is

RM15,000.

• On 1st August 2019, Bakar contributed additional capital of RM10,000. Each partner

is entitled to interest on capitals allowed 10% per annum. Calculation of interest on

capital at the end of December is as follows:

Abu: RM20,000 x 10% = RM2,000

Bakar: RM15,000 x 10% = RM1,500

: RM10,000 x 10% x 5/12 = RM417

*at the end of December 2019, the interest on capital for Abu is RM2,000 and Bakar is

RM1,917 (RM1,500 + RM417).

18. Recording the Partners’ Salary

18Recording the Partners’ Salary

• Partners do not only place their capital into the business, they can also work and be

treated as employees of the business.

• They are paid salaries as stated in the partnership agreement.

• Salary for the partners are deducted from the net profit before sharing the balance

of profits.

• The journal entry is as follows:

Debit profit & loss appropriation account

Credit Partner’s Current account

19. Distribution Net Profit/ Net Loss

19Distribution Net Profit/ Net Loss

• At the end of the financial year, the balances of net profit or loss will

be divided between partners according to the profit sharing ratio

stipulated in the agreement.

• The profit sharing ratio depends on the capital contributed by the

partners.

• After considering the interest on drawings, salaries, interest on

capital and other allocations of profit, the balances of net profit

or loss will be distributed.

• The profit shared by each partner are credited and losses will be

debited to the Partners’ Current Account.

20. Distribution Net Profit/ Net Loss

20Distribution Net Profit/ Net Loss

Example

Chong and David are partners sharing profit according to their partnership’s capital

contribution ratio. Chong’s capital is RM30,000 and David’s capital is RM60,000. The

balance of net profit after considering interest on drawings, interest on capital and

partners’ salaries is RM14,500. Calculate the profit or loss shared by each of the

partners.

Capital contribution ratio between Chong and David

= 30,000 : 60,000

= 1:2

Profit shared:

Chong = 1/3 x RM14,500 = RM4,833

David = 2/3 x RM14,500 = RM9,667

21. Learning Objective 4

21Learning Objective 4

Prepare the partner’s capital and current

account.

22. Preparing the Partners’ Capital & Current Account

22Preparing the Partners’ Capital & Current Account

• Capital Account

- Records capital contributed and must be prepared for each partner.

- The amount of capital will generally remain unchanged and fixed unless there is

additional capital introduced by partners.

• Current Account

- Record frequent transactions between the partners and the business.

- It represent each partner’s accumulated share of profit less any amount withdrawn

to date.

- Interest on capital, interest on loan, salaries and shared profit will increase the

current account.

- Drawings by the partners and interest on drawings will decrease the current

account.

23.

23Normally, Partner's Current Account has a Credit Balance but, if a partner

has withdrawn more than his or her share of profits, then it will have a

Debit Balance.

24. Learning Objective 5

24Learning Objective 5

The Financial Statement of a Partnership

Business

25. Financial Statements of a Partnership Business

25Financial Statements of a Partnership

Business

● An additional statement called the “Profit & Loss Appropriation

Account” is another statement that needs to be prepared for a

partnership business.

● This account is peculiar to a partnership business as it shows how the

business’s profit and loss is altered after taking into consideration the

interest or the involvement of the partners in the business.

26. Example of Profit & Loss Appropriation Account

26Example of

Profit & Loss

Appropriatio

n Account

27. Example of Profit & Loss Appropriation Account (t-format)

27Example of Profit & Loss Appropriation

Account (t-format)

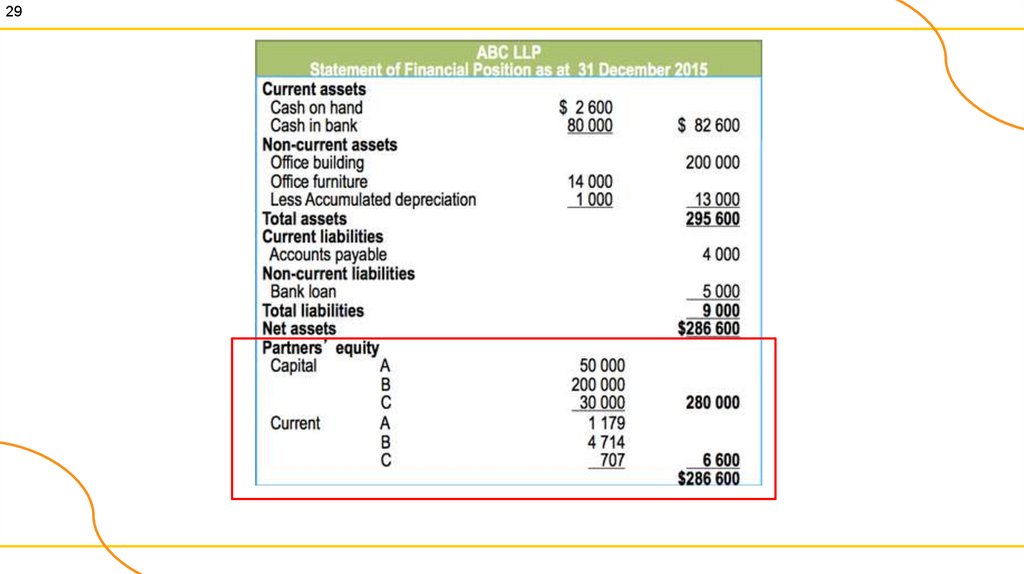

28. Partnership’s Statement of Financial Position

28Partnership’s Statement of Financial Position

● The asset and liability sections for a partnership Statement of Financial

Position (balance sheet) do not differ from other forms of business.

● A partnership equity statement is called the statement of partners’

equity.

● The equity section of a partnership balance sheet reports a separate

capital balance for each partner.

29.

2930. ILLUSTRATION (1/3)

30ILLUSTRATION (1/3)

• Taylor and Clarke formed a partnership business

on 1 January 20X3.

• Taylor and Clarke share profits in the ratio = 3 : 2

• They are entitled to 5% interest on capital.

• Taylor invested £20,000 capital and Clarke

invested £60,000 capital.

• Clarke receives a salary of £15,000.

• Taylor is to be charged £500 interest on drawings

and Clarke £1,000.

• Net profits amounted to £50,000.

31.

31ILLUSTRATION (2/3)

Profit and Loss Appropriation Account

32.

32ILLUSTRATION (3/3)

33. Thank You

33Thank You