finance

financeSimilar presentations:

")

")

Corporate Finance

1.

Course: Corporate Finance.Professors: Wael ROUATBI (w.rouatbi@montpellier-bs.com);

Samuel NYARKO (s.nyarko@montpellier-bs.com).

Session 4

Investment Decision Tools

Copyright: Many slides of the present session are based on the book:

Berk, J. B., and DeMarzo, P. M., 2019, Corporate finance, Fifth Edition (Pearson Education).

2.

Measuring investment worthSeveral methods of evaluating investment projects are used by financial managers,

including:

1. Payback period,

2. Net Present Value (NPV),

3. Internal Rate of Return (IRR),

3.

1. Payback periodThe length of time it will take the company to recover its initial investment.

When cash inflows are equal, the payback period is computed by dividing the initial

investment by the cash inflows generated by the project.

When cash inflows are not even, you must find the payback period by trial and error.

Example 1: Assume: Cost of investment = €18,000

Annual cash flows = €3,000

Payback period?

Payback period = 18,000/3000 = 6 years.

4.

Example 2: Consider to projects with uneven after-tax cash inflows. Assume each projectcosts €1,000

Cash Inflow

Year

A(€)

B(€)

1

100

500

2

200

400

3

300

300

4

400

100

5

500

6

600

Payback period of each project?

5.

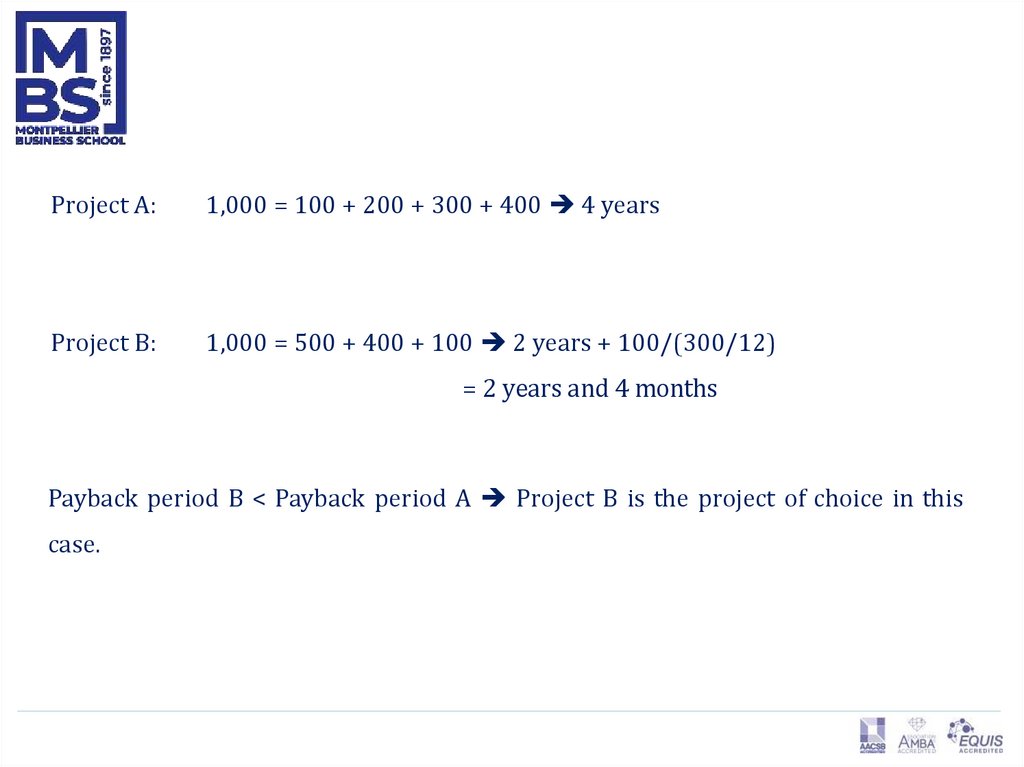

Project A:1,000 = 100 + 200 + 300 + 400 4 years

Project B:

1,000 = 500 + 400 + 100 2 years + 100/(300/12)

= 2 years and 4 months

Payback period B < Payback period A Project B is the project of choice in this

case.

6.

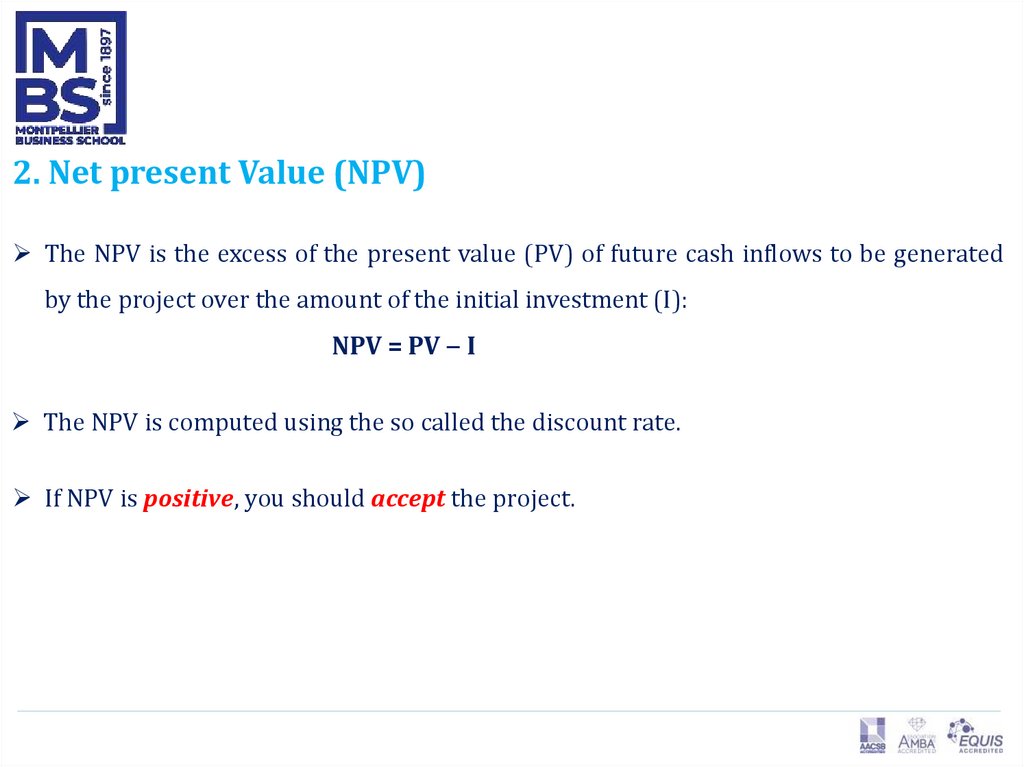

2. Net present Value (NPV)The NPV is the excess of the present value (PV) of future cash inflows to be generated

by the project over the amount of the initial investment (I):

NPV = PV ‒ I

The NPV is computed using the so called the discount rate.

If NPV is positive, you should accept the project.

7.

Example 3: Consider the following investment:Initial investment = €12,950

Estimated life = 10 years,

Annual cash inflows = €3,000

Cost of capital = 12%

NPV?

PV = € 16,950

NPV = PV – I = €4,000

Since the NPV is positive, the investment should be accepted.

8.

3. Internal rate of return (IRR)The IRR is defined as the rate that equates the initial investment I with the present

value (PV) of future cash inflows. In other words, at IRR, I = PV or NPV = 0.

Generally you should accept the project if the IRR exceeds the cost of capital.

Example 4: Consider the following investment:

Initial investment = €12,950

Estimated life = 10 years,

Annual cash inflows = €3,000

Cost of capital = 12%

IRR?

9.

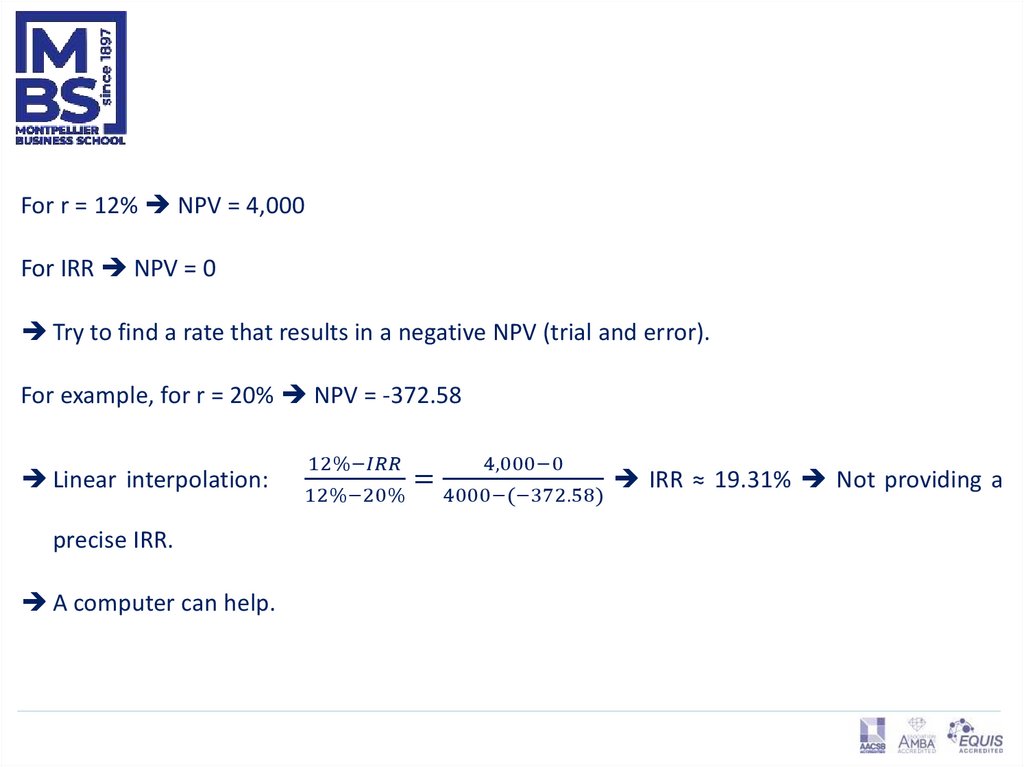

For r = 12% NPV = 4,000For IRR NPV = 0

Try to find a rate that results in a negative NPV (trial and error).

For example, for r = 20% NPV = -372.58

Linear interpolation:

precise IRR.

A computer can help.

12%−