Similar presentations:

")

Types of Taxes Ісаєнко

1.

Types of TaxesYou Should

Know About

Understanding Global Taxation Systems and Policies

"Nothing is certain but death and taxes." —

Benjamin Franklin

2.

Basic Classificationof Taxes

Direct vs. Indirect Taxes

Direct Taxes: Paid directly to the government by

individuals or organizations (e.g., Personal Property Tax,

Federal Income Tax). These cannot be shifted to others.

Examples: Personal property taxes, federal income taxes.

Key Difference: In indirect taxes, the person paying the

tax to the government (the retailer) is different from

the person bearing the actual cost (the customer).

Indirect Taxes: Levied on the production or sale of goods

and services. Included in the price paid by the consumer

(e.g., VAT, Sales Tax, Excise Duties).

Examples: VAT (Value Added Tax), Sales Tax, Excise

duties on tobacco or alcohol.

3.

Common Types of TaxesIncome & Corporate:

• Individual Income Tax: Levied on wages,

salaries, and other earnings.

• Corporation Tax: Levied on business profits.

Note: Profits are often "taxed twice" (once

as corporate profit, and again as individual

income when dividends are paid).

Assets & Wealth:

• Capital Gains Tax: Tax on profits from selling assets

like stocks or shares (often at a lower rate than

income tax).

• Inheritance/Estate Tax: Often called "death duty,"

imposed on money or property passed down to

heirs.

International Trade:

• Tariffs: Special taxes charged on goods

imported from abroad to protect domestic

markets.

4.

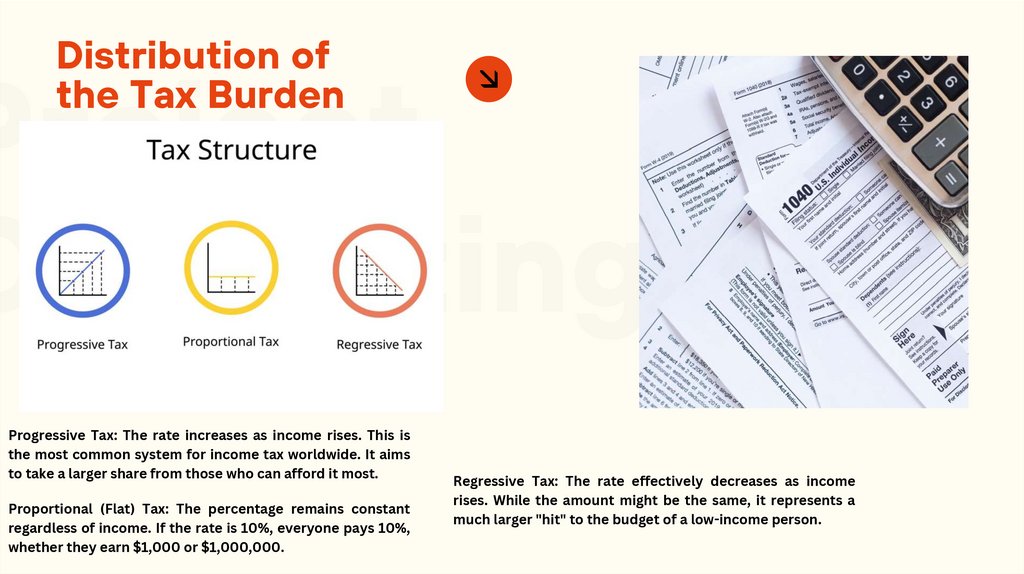

Distribution ofthe Tax Burden

Progressive Tax: The rate increases as income rises. This is

the most common system for income tax worldwide. It aims

to take a larger share from those who can afford it most.

Proportional (Flat) Tax: The percentage remains constant

regardless of income. If the rate is 10%, everyone pays 10%,

whether they earn $1,000 or $1,000,000.

Regressive Tax: The rate effectively decreases as income

rises. While the amount might be the same, it represents a

much larger "hit" to the budget of a low-income person.

5.

Tax Avoidancevs. Tax Evasion

Tax

Avoidance

(Legal):

Using

legitimate "loopholes" or technicalities

to minimize payments.

Examples: Receiving "perks" (company

cars, free health insurance) instead of

taxable salary, or registering companies

in Tax Havens (Monaco, Cayman Islands)

where rates are extremely low.

Tax Evasion (Illegal): Deliberately

misreporting or not declaring income.

This is a criminal offense and leads to

severe legal penalties.

6.

Why they are Regressive: Lower-incomeconsumers spend nearly all their income on

essentials like food, clothing, and shelter.

The Math of Inequality:

• If a package of cigarettes has a $1 tax:

• For a person earning $10, that $1 is 10% of

their income.

• For a person earning $20, that same $1 is

only 5% of their income.

The Social Impact

of Sales Taxes

Conclusion: Uniform taxes on

essentials hit the poor harder

because they have less "disposable"

income left over.

7.

Conclusion: TheStrategic Goals of

Taxation

Economic Motivation: Regressive taxes can

sometimes be used to stimulate economic

activity among certain groups.

Social Justice: Progressive taxes are used to

reduce the "wealth gap" and income

inequality.

Public Welfare: The primary goal is to

mobilize surplus income from the "haves"

and reinvest it into public services

(healthcare, infrastructure, education) to

benefit the "have-nots."

8.

ThankYou