economics

economicsSimilar presentations:

Economics. Learning objectives

1. Economics

Week 2. Lessons 1-32. Learning objectives

• Understand the formula ofcalculation deposit

profitability and loan

payments.

• Calculate deposit profitability

and loan payments using

simple and compound

interest.

3. Discuss

If you put $100 in a bank at 5%per year, how much will you

have after 1 year?

4. Interest

Interest is the amount of money alender or financial institution

receives for lending out money.

“Interest” is defined as the cost of

borrowing money.

5. Simple and Compound Interest

• Simple interest – interest is paid onlyon the principal.

“Principal” refers to the original sum of

money borrowed in a loan or put into

an investment.

• Compound interest is paid on both

principal and interest, compounded at

regular intervals.

6. Simple Interest Formula

Simple interest = P×i×nwhere:

P=Principal

i=interest rate

n=term of the loan (in years)

Simple Interest

Formula

7. Example

Example: a $1000 principal paying 10%simple interest after 3 years pays.

1000$ ×0.1 ×3 = $300

Simple interest = P×i×n

(0.1= 10%:100)

where:

P=Principal

i=interest rate

n=term of the loan (in years)

8. Compound interest

If interest is compounded annually, it pays0.1 × $1000 = $100 the first year,

0.1 × $1100 = $110 the second year and

0.1 × $1210 = $121 the third year

totaling $100 + $110 + $121 = $331 interest

9. Compound Interest Formula

FV = the compound amount or future valueP = principal

i = interest rate per period of compounding

n = number of periods

I = interest earned

10. Activity 1

• Example: $800 is invested at 7% for 6years. Find the simple interest and the

interest compounded annually.

• Simple interest:

• Compound interest:

11. Solution

• Example: $800 is invested at 7% for 6 years. Findthe simple interest and the interest compounded

annually.

• Simple interest: FV=PV*i*n

• Compound interest:

12. Compounding periods

• In the formula for calculating compoundinterest, the variables "i" and "n" have to be

adjusted if the number of compounding

periods is more than once a year.

• For example, for a 10-year loan at 10%,

where interest is compounded semi-annually

(number of compounding periods = 2), i =

5% (i.e., 10% / 2) and n = 20 (i.e., 10 x 2).

13. Compound Interest

PeriodInterest

Credited

Annual

year

Semiannual

6 months 2

Quarterly

quarter

4

Monthly

month

12

Times

Credited

per year

1

Rate per

compounding

period

R

14. Compound Interest

where:i=interest rate in percentage terms

n=number of compounding periods per year

t=total number of years for the investment or loan

Example: $32000 is invested at 10% for 2 years. Find the

interest compounded monthly:

15. Activity 1

Example: $32000 is invested at 10% for 2years. Find the interest compounded yearly,

semiannually, quarterly, and monthly:

16. Answer

• Example: $32000 is invested at 10% for 2 years.Find the interest compounded yearly,

semiannually, quarterly, and monthly.

yearly:

semiannually:

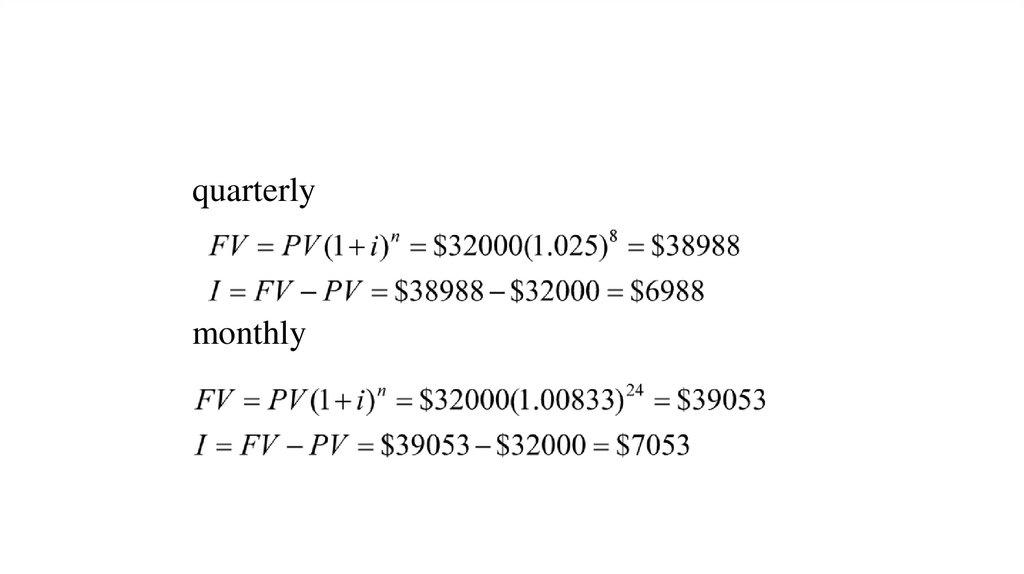

17.

quarterlymonthly

18. Activity 2 The following table demonstrates the difference that the number of compounding periods can make overtime for a

$10,000 loantaken for a 10-year period.

Complete the table and compare. What is more beneficial?

Compounding

Frequency

No. of

Compounding

Periods

Values for i/n and nt

Total Interest

Annually

1

i/n = __%, nt = __

$_________

Semi-annually

2

i/n = __%, nt = __

$_________

Quarterly

4

i/n = __%, nt = __

$_________

Monthly

12

i/n = ___%, nt = ___

$__________

19. Answers: The following table demonstrates the difference that the number of compounding periods can make overtime for a $10,000

loan taken for a 10-year period.Compounding

Frequency

No. of

Compounding

Periods

Values for i/n and nt

Total Interest

Annually

1

i/n = 10%, nt = 10

$15,937.42

Semi-annually

2

i/n = 5%, nt = 20

$16,532.98

Quarterly

4

i/n = 2.5%, nt = 40

$16,850.64

Monthly

12

i/n = 0.833%, nt = 120

$17,059.68

20. Daily and Continuous Compounding

• Daily compound interest formula: divide i by 365and multiply n by 365

21. Activity Daily and Continuous Compounding

• Example: Find the compound amount if$2900 is deposited at 5% interest for 10

years if interest is compounded daily.

22. Solution

• Example: Find the compound amount if $2900 isdeposited at 5% interest for 10 years if interest is

compounded daily.