")

")

")

, would anyone buy the stock, and what is its value?")

of Bonds")

finance

financeSimilar presentations:

")

")

Introduction to Finance: Chapter 10. Bonds and Stocks: Characteristics and Valuations

1. Introduction to Finance: Chapter 10. Bonds and Stocks: Characteristics and Valuations

Corporations secure long-term financing through bonds,preferred stock, and common stock. Bonds vary in

security, maturity, and return, with covenants and

ratings managing risk. Stocks provide ownership, with

dividends or repurchases distributing earnings. Securities

are valued based on future cash flows, with economic

and industry factors influencing stock prices.

Valuation of financial securities depends on future cash

flows and discount rates. Bonds are valued based on

present value of future interest payments and principal,

while stock prices are influenced by firm performance,

economic conditions, and industry trends.

by Rustem Karimov, SDU University, BS, Kaskelen, 2025

2. Overview

Features of Common StockIntrinsic Value and Stock Price

Determining Common Stock Values

Discounted Dividend Model

Corporate Valuation Model

Other Approaches

Preferred Stock

3. Facts About Common Stock

Represents ownershipOwnership implies control

Stockholders elect directors

Directors elect management

Management’s goal: Maximize the stock price

4. Intrinsic Value and Stock Price

Outside investors, corporate insiders, and analysts use a

variety of approaches to estimate a stock’s intrinsic value

In equilibrium we assume that a stock’s price equals its intrinsic

value.

Outsiders estimate intrinsic value to help determine which stocks are

attractive to buy and/or sell.

Stocks with a price below (above) its intrinsic value are undervalued

(overvalued).

5. Different Approaches for Estimating the Intrinsic Value of a Common Stock

Discounted dividend modelCorporate valuation model

Models based on market multiples

6. Discounted Dividend Model

Value of a stock is the present value of the future

dividends expected to be generated by the stock.

D3

D1

D2

D

P̂0

...

1

2

3

(1 rs )

(1 rs )

(1 rs )

(1 rs )

7. Constant Growth Stock

A stock whose dividends are expected to grow forever at

a constant rate, g.

D1 = D0(1 + g)1

D2 = D0(1 + g)2

Dt = D0(1 + g)t

If g is constant, the discounted dividend formula

converges to:

D0 (1 g)

D1

P̂0

rs g

rs g

8. Future Dividends and Their Present Values

9. What happens if g > rs?

What happens if g > rs?If g > rs, the constant growth formula leads to a

negative stock price, which does not make sense.

The constant growth model can be used only if:

rs > g

g is expected to be constant forever.

10. Use the SML to Calculate the Required Rate of Return (rs)

If rRF = 3%, rM = 8%, and b = 1.2, what is the required rate of return on thefirm’s stock?

rs = rRF + (rM – rRF)b

= 3% + (8% – 3%)1.2

= 9%

11. Find the Expected Dividend Stream for the Next 3 Years and Their PVs

D0 = $2 and g is a constant 4%.12. What is the stock’s intrinsic value?

Using the constant growth model:

D1

$2.08

P̂0

rs g

0.09 0.04

$2.08

0.05

$41.60

13. What is the stock’s expected value, one year from now?

D1 will have been paid out already. So, expected P1 is the

present value (as of Year 1) of D2, D3, D4, etc.

D2

$2.1632

P̂1

rs g

0.09 0.04

$43.26

Could also find expected P1 as:

P̂1 P0 (1.04) $43.26

14. Find Expected Dividend Yield, Capital Gains Yield, and Total Return During First Year

Dividend yield= D1/P0 = $2.08/$41.60 = 5.0%

Capital gains yield

= (P1 – P0)/P0

= ($43.26 – $41.60)/$41.60 = 4.0%

Total return (rs)

= Dividend yield + Capital gains yield

= 5.0% + 4.0% = 9.0%

15. What would the expected price today be, if g = 0?

The dividend stream would be a perpetuity.PMT $2.00

P̂0

$22.22

r

0.09

16. Supernormal Growth

What if g = 30% for 1 yr., 20% for 1 yr., and 10% for 1 yr. beforeachieving long-run growth of 4%?

Can no longer use just the constant growth model to

find stock value.

However, the growth does become constant after 3

years.

17. Valuing Common Stock with Nonconstant Growth

D0 = $2.00.18. Find Expected Dividend and Capital Gains Yields During the First and Fourth Years (1 of 2)

Dividend yield (first year)= $2.60/$62.78 = 4.14%

Capital gains yield (first year)

= 9.00% – 4.14% = 4.86%

During nonconstant growth, dividend yield and capital gains yield are not

constant, and capital gains yield ≠ g.

After t = 3, the stock has constant growth and dividend yield = 5%, while

capital gains yield = 4%.

19. Nonconstant Growth: What if g = 0% for 3 years before long-run growth of 4%?

D0 = $2.00.20. Find Expected Dividend and Capital Gains Yields During the First and Fourth Years (2 of 2)

Dividend yield (first year)= $2.00/$37.19 = 5.38%

Capital gains yield (first year)

= 9.00% – 5.38% = 3.62%

After t = 3, the stock has constant growth and dividend yield = 5%, while

capital gains yield = 4%.

21. If the stock was expected to have negative growth (g = −4%), would anyone buy the stock, and what is its value?

Yes. Even though the dividends are declining, the stock is still

producing cash flows and therefore has positive value.

D0 (1 g)

D1

P̂0

rs g

rs g

$2.00 (0.96)

$1.92

$14.77

0.09 ( 0.04) 0.13

22. Find Expected Annual Dividend and Capital Gains Yields

Capital gains yield= g = –4.00%

Dividend yield

= 9.00% – (–4.00%) = 13.00%

Since the stock is experiencing constant growth, dividend yield and capital

gains yield are constant. Dividend yield is sufficiently large (13%) to offset

negative capital gains.

23. Corporate Valuation Model

Also called the free cash flow method. Suggests the value of

the entire firm equals the present value of the firm’s free cash

flows (which is the MV of its operations) plus the market value

of its non-operating assets.

Remember, free cash flow is the firm’s after-tax operating

income less the net capital investment.

FCF EBIT(1 T) Depreciation and amortization

Capital expenditures ΔNOWC

24. Applying the Corporate Valuation Model

Find the market value (MV) of the firm’s operations, by finding the PV of thefirm’s future FCFs.

Add the market value of the firm’s non-operating assets.

Subtract MV of firm’s debt and preferred stock to get MV of common stock.

Divide MV of common stock by the number of shares outstanding to get

intrinsic stock price (value).

25. Issues Regarding the Corporate Valuation Model

Often preferred to the discounted dividend model, especially whenconsidering number of firms that don’t pay dividends or when dividends are

hard to forecast.

Similar to discounted dividend model, assumes at some point free cash flow

will grow at a constant rate.

Horizon value (HVN) represents value of firm’s operations at the point that

growth becomes constant.

26. Use the Corporate Valuation Model to Find the Value of the Firm’s Operations

Given: Long-Run gFCF = 5% and WACC = 7%27. What is the firm’s intrinsic value per share?

The firm has $40 million total in debt and preferred stock, $5 million of

non-operating assets, and 10 million shares of common stock.

MV of equity MV of operations MV of nonoperating assets MV of debt and preferred

$877.50 $5 $40

$842.50 million

Value per share MV of equity/# of shares

$842.50/10

$84.25

28. Firm Multiples Method

Analysts often use the followingmultiples to value stocks.

P/E

P/CF

P/Sales

EXAMPLE: Based on comparable

firms, estimate the appropriate

P/E. Multiply this by expected

earnings to back out an estimate of

the stock price.

Enterprise-Based Multiples

EV/EBITDA

29. Preferred Stock

Hybrid securityLike bonds, preferred stockholders receive a fixed dividend that must be paid

before dividends are paid to common stockholders.

However, companies can omit preferred dividend payments without fear of pushing

the firm into bankruptcy.

30. If preferred stock with an annual dividend of $5 sells for $100, what is the preferred stock’s expected return?

DVp

rp

$5

$100

rp

$5

r̂p

$100

0.05 5%

31. Bonds and their Valuation: Overview

Key Features of BondsBond Valuation

Measuring Yield

Assessing Risk

32. What is a bond?

A long-term debt instrument in which a borrower agreesto make payments of principal and interest, on specific

dates, to the holders of the bond.

Here's a simple example:

1. You buy a bond: Let's say you buy a bond from a company

for $1,000 with a 5% interest rate, and it matures in 10

years.

2. Interest payments: Every year, the company pays you 5%

of $1,000, which is $50. You receive this payment each

year for 10 years.

3. Getting your money back: At the end of the 10 years, the

company returns your $1,000.

33. What is a bond?

34. Key Features of a Bond

Par value: face amount of thebond, which is paid at maturity

(assume $10,000,000 like in the

picture).

Coupon interest rate: stated

interest rate (generally fixed)

paid by the issuer. Multiply by

par value to get dollar payment

of interest.

Maturity date: years until the

bond must be repaid.

Issue date: when the bond was

issued.

Yield to maturity: rate of return

earned on a bond held until

maturity (also called the

“promised yield”).

35. Other Types (Features) of Bonds

Convertible bond: may be exchanged for common stock of the firm, at theholder’s option.

Warrant: long-term option to buy a stated number of shares of common stock

at a specified price.

Putable bond: allows holder to sell the bond back to the company prior to

maturity.

Income bond: pays interest only when interest is earned by the firm.

Indexed bond: interest rate paid is based upon the rate of inflation.

36. Effect of a Call Provision

A call provision is a special feature of some bonds that allows the company(or government) that issued the bond to pay it back early.

Allows issuer to refund the bond issue if rates decline (helps the issuer, but

hurts the investor).

The issuer: They can save money by replacing the old, higher-interest bond with a

new bond that has a lower interest rate.

The investor: Investors lose their higher-interest bond and may have to reinvest

their money at lower rates, meaning they earn less.

Bond investors require higher yields on callable bonds.

In many cases, callable bonds include a deferred call provision and a

declining call premium:

Deferred Call Provision: This means the issuer cannot call (pay back) the bond for

a certain number of years. This gives investors some security because they know

they will receive interest payments for that time.

Declining Call Premium: If the issuer calls the bond, they pay a penalty, known as

a call premium. This penalty decreases over time.

37. What is a sinking fund?

Provision to pay off a loan over its life rather than all at maturity.Similar to amortization on a term loan.

Reduces risk to investor, shortens average maturity.

But not good for investors if rates decline after issuance.

Example:

Suppose a company issues bonds that will mature in 10 years. To prepare for

paying back the bondholders, the company creates a sinking fund and decides to

contribute a specific amount of money each year. By the time the bonds mature,

the company will have enough saved up in the sinking fund to pay back the

bondholders without financial strain.

38. The Value of Financial Assets

The value of any financial asset is determined by the present value of itsexpected cash flows.

For bonds, cash flows include interest payments and the principal at maturity.

Different types of bonds have different cash flow structures, affecting their

overall value.

CFN

CF1

CF2

Value

...

1

2

N

(1 r) (1 r)

(1 r)

39. What is the opportunity cost of debt capital?

The discount rate (ri) is the opportunity cost ofcapital, and is the rate that could be earned on

alternative investments of equal risk.

ri = r* + IP + MRP + DRP + LP

40. What is the value of a 10-year, 10% annual coupon bond, if rd = 10%?

CFNCF1

CF2

Value

...

1

2

N

(1 r) (1 r)

(1 r)

VB

$100

1.10

1

VB $90.91

VB $1, 000

$100

1.10

10

$1,000

1.10

10

$38.55 $385.54

41. Calculating the Value of a Bond

This bond has a $1,000 lump sum (the par value) due at

maturity (t = 10), and annual $100 coupon payments beginning

at t = 1 and continuing through t = 10. The price of the bond

can be found by solving for the PV of these cash flows.

Excel: =PV(.10,10,100,1000)

42. What’s the value of a 10-year bond outstanding with the same risk but a 13% annual coupon rate?

The annual coupon payment is $130. Since the risk is the same it has thesame yield to maturity as the previous bond (10%).

This bond sells at a premium because:

The coupon rate (13%) > The yield to maturity (10%).

Excel: =PV(.10,10,130,1000)

43. What’s the value of a 10-year bond outstanding with the same risk but a 7% annual coupon rate?

The annual coupon payment is $70. Since the risk is the same it hasthe same yield to maturity as the previous bonds (10%). This bond

sells at a discount because:

The coupon rate < The yield to maturity.

Excel: =PV(.10,10,70,1000)

44. Changes in Bond Value over Time

What would happen to the value of these three bonds if therequired rate of return remained at 10%?

45. Bond Values over Time

At maturity, the value of any bond must equal its par value.If rd remains constant:

The value of a premium bond would decrease over time, until it

reached $1,000.

The value of a discount bond would increase over time, until it

reached $1,000.

The value of a par bond stays at $1,000.

46. What is the YTM on the following bond?

10-year; 9% annual coupon; $1,000 par value; selling for $887.Must find the rd that solves this equation.

VB

$887

INT

1 rd

1

90

1 rd

1

INT

1 rd

N

90

1 rd

10

M

1 rd

N

1, 000

1 rd

10

47. What is the YTM on the following bond?

10-year; 9% annual coupon; $1,000 par value; selling for $887.Must find the rd that solves this equation.

48.

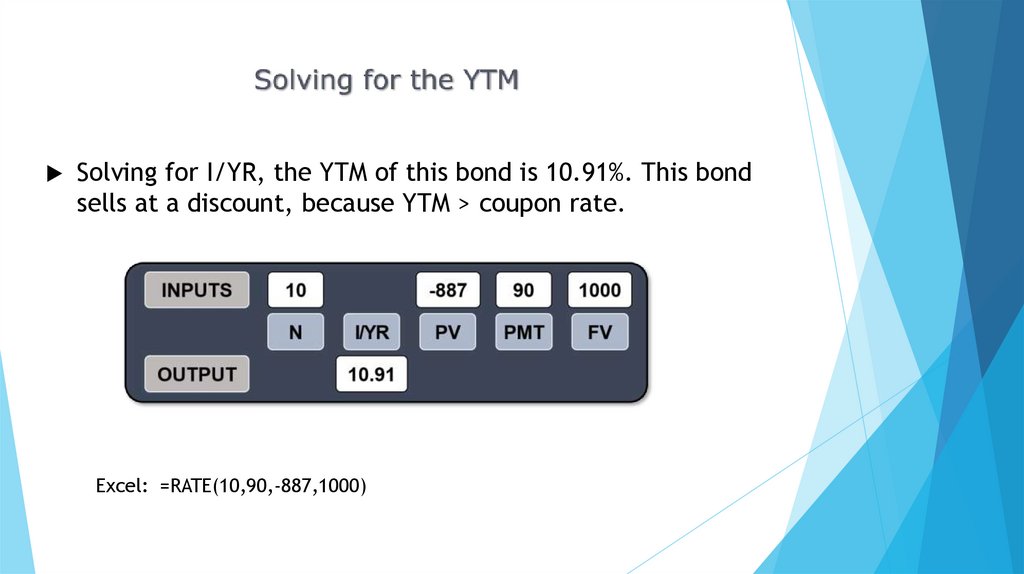

Solving for I/YR, the YTM of this bond is 10.91%. This bondsells at a discount, because YTM > coupon rate.

Excel: =RATE(10,90,-887,1000)

49. Find YTM If the Bond Price is $1,134.20

Solving for I/YR, the YTM of this bond is 7.08%.at a premium, because YTM < coupon rate.

Excel: =RATE(10,90,-1134.20,1000)

This bond sells

50. Definitions

Annual coupon paymentCurrent yield (CY)

Current price

Change in price

Capital gains yield (CGY)

Beginning price

Expected total return YTM Expected CY Expected CGY

51. An Example: Current and Capital Gains Yields

Find the current yield and the capital gains yield for a 10-year,9% annual coupon bond that sells for $887, and has a face value

of $1,000.

$90

Current yield

$887

0.1015 10.15%

52. Calculating Capital Gains Yield

YTM = Current yield + Capital gains yieldCGY YTM CY

10.91% 10.15%

0.76%

Could also find the expected price one year from now and divide the change in

price by the beginning price, which gives the same answer.

53. What is price risk? Does a 1-year or 10-year bond have more price risk?

What is price risk? Does a 1-year or 10year bond have more price risk?Price risk is the concern that rising rd will cause the value of a bond to fall.

rd

1-year

Change

10-year

Change

5%

$1,048

10%

1,000

+ 4.8%

1,000

+38.6%

15%

956

– 4.4%

749

–25.1%

$1,386

The 10-year bond is more sensitive to interest rate changes, and hence has more

price risk.

54. Illustrating Price Risk

Value ($)YTM(%)

55. What is reinvestment risk?

Reinvestment risk is the concern that rd will fall, and future CFs will have tobe reinvested at lower rates, hence reducing income.

EXAMPLE: Suppose you just won $500,000 playing the lottery. You intend to

invest the money and live off the interest.

56. Reinvestment Risk Example

You may invest in either a 10-year bond or a series of ten 1-year bonds. Both10-year and 1-year bonds currently yield 10%.

If you choose the 1-year bond strategy:

After Year 1, you receive $50,000 in income and have $500,000 to

reinvest. But, if 1-year rates fall to 3%, your annual income would

fall to $15,000.

If you choose the 10-year bond strategy:

You can lock in a 10% interest rate, and $50,000 annual income for

10 years, assuming the bond is not callable.

57. Conclusions about Price Risk and Reinvestment Risk

Price riskReinvestment risk

Short term

AND/OR

High coupon

Bonds

Low

High

Long term

AND/OR

Low coupon

Bonds

High

Low

58. Semiannual Bonds

1.Multiply years by 2: Number of periods = 2N

2.

Divide nominal rate by 2: Periodic rate (I/YR) = rd/2

3.

Divide annual coupon by 2: PMT = Annual coupon/2

59. What is the value of a 10-year, 10% semiannual coupon bond, if rd = 13%?

1. Multiply years by 2: N = 2 × 10 = 202. Divide nominal rate by 2: I/YR = 13/2 = 6.5

3. Divide annual coupon by 2: PMT = 100/2 = 50

Excel: =PV(.065,20,50,1000)

60. Would you prefer to buy a 10-year, 10% annual coupon bond or a 10-year, 10% semiannual coupon bond, all else equal?

The semiannual bond’s effective rate is:M

2

rNOM

0.10

EFF% 1

1 10.25%

1 1

M

2

Excel:

=EFFECT(.10,2)

= 10.25%

10.25% > 10% (the annual bond’s effective rate), so you would prefer the semiannual

bond.

61. If the proper price for this semiannual bond is $1,000, what would be the proper price for the annual coupon bond?

The semiannual bond has a 10.25% effective rate, so theannual bond should earn the same EAR. At these prices, the

annual and semiannual bonds are in equilibrium.

Excel: =PV(.1025,10,100,1000)

62. A 10-year, 10% semiannual coupon bond selling for $1,135.90 can be called in 4 years for $1,050, what is its yield to call

(YTC)?The bond’s yield to maturity is 8%.

Solving for the YTC is

identical to solving for YTM, except the time to call is used

for N and the call premium is FV.

Excel: =RATE(8,50,-1135.90,1050)

63. Yield to Call

3.568% represents the periodic semiannual yield to call.YTCNOM = rNOM = 3.568% × 2 = 7.137% is the rate that a broker would quote.

The effective yield to call can be calculated.

YTCEFF = (1.03568)2 – 1 = 7.26%

Excel: =EFFECT(.07137,2) = 7.26%

64. If you bought these callable bonds, would you be more likely to earn the YTM or YTC?

The coupon rate = 10% compared to YTC = 7.137%. The firm could raisemoney by selling new bonds which pay 7.137%.

Could replace bonds paying $100 per year with bonds paying only $71.37 per

year.

Investors should expect a call, and to earn the YTC of 7.137%, rather than the

YTM of 8%.

65. When is a call more likely to occur?

In general, if a bond sells at a premium, then (1) coupon > rd, so (2) a call ismore likely.

So, expect to earn:

YTC on premium bonds.

YTM on par and discount bonds.

66. Default Risk

If an issuer defaults, investors receive less than the promised return.Therefore, the expected return on corporate and municipal bonds is less than

the promised return.

Influenced by the issuer’s financial strength and the terms of the bond

contract.

67. Evaluating Default Risk: Bond Ratings

Moody’sInvestment Grade

Aaa Aa A Baa

Junk Bonds

Ba B Caa C

S&P

AAA AA A BBB

BB B CCC C

Bond ratings are designed to reflect the probability of a bond issue going into default.

68. Factors Affecting Default Risk and Bond Ratings

Financial performanceDebt ratio

TIE ratio

Current ratio

Qualitative factors: Bond contract terms

Secured vs. unsecured debt

Senior vs. subordinated debt

Guarantee and sinking fund provisions

Debt maturity

69. Other Factors Affecting Default Risk

Miscellaneous qualitative factorsEarnings stability

Regulatory environment

Potential antitrust or product liabilities

Pension liabilities

Potential labor problems

70. Chapter 11 Bankruptcy

If company can’t meet its obligations…It files under Chapter 11 to stop creditors from foreclosing, taking

assets, and closing the business and it has 120 days to file a

reorganization plan.

Court appoints a “trustee” to supervise reorganization.

Management usually stays in control.

Company must demonstrate in its reorganization plan that it is “worth more

alive than dead.”

If not, judge will order liquidation under Chapter 7.

71. Priority of Claims in Liquidation

1.Secured creditors from sales of secured assets

2.

Trustee’s costs

3.

Wages, subject to limits

4.

Taxes

5.

Unfunded pension liabilities

6.

Unsecured creditors

7.

Preferred stock

8.

Common stock

72. Reorganization

In a liquidation, unsecured creditors generally receive nothing. This makesthem more willing to participate in reorganization even though their claims

are greatly scaled back.

Various groups of creditors vote on the reorganization plan. If both the

majority of the creditors and the judge approve, the company “emerges”

from bankruptcy with lower debts, reduced interest charges, and a chance

for success.