finance

financeSimilar presentations:

The income statement

1.

The income statementASB 1110 Financial Accounting

2.

Lecture outline• The income statement

– Purpose & nature

– Items

– Layout

– Recognition of revenue

3.

The purpose of the income statement• Primary purpose of a business is to generate

wealth (profit)

– Statement of financial position lays out in which forms

this wealth is held

• Income statement

– measures and reports how much profit (wealth) the

business has generated over a period

– Helps users to understand how that profit was made

– Lists revenues (incomes) and expenses (costs)

4.

Revenue• Revenue =

a measure of the inflow of economic

benefits arising from the ordinary

operations of a business

• In order to measure profits, the total revenue

of a business, generated during a particular

period, must be identified

5.

Forms of revenues• Different forms of business enterprise will

generate different forms of revenue:

– Sales of goods (for example, by a manufacturer)

– Fees for services (for example, of a solicitor)

– Subscriptions (for example, of a club)

– Interest received (for example, on an investment

fund)

6.

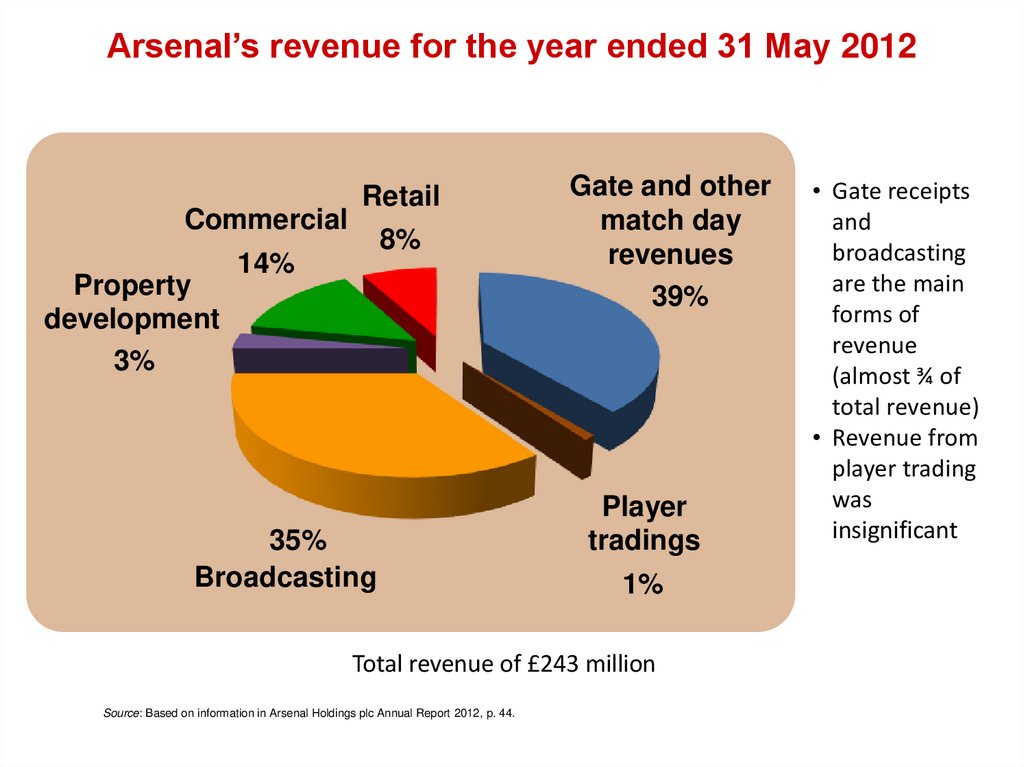

Arsenal’s revenue for the year ended 31 May 2012Commercial

Property

development

3%

Retail

8%

14%

35%

Broadcasting

Gate and other

match day

revenues

39%

Player

tradings

1%

Total revenue of £243 million

Source: Based on information in Arsenal Holdings plc Annual Report 2012, p. 44.

• Gate receipts

and

broadcasting

are the main

forms of

revenue

(almost ¾ of

total revenue)

• Revenue from

player trading

was

insignificant

7.

Expense• Expense =

the outflow of economic benefits arising from the

ordinary operations of a business

• In order to measure profits, the total expenses of a

business, generated during a particular period, must

also be identified

• It is the opposite of revenue

• Expenses are incurred in the process of generating, or

attempting to generate, revenue

8.

Forms of expense• The nature of the business will again determine the type

of expenses that will be incurred

• Common types of expenses:

– The cost of buying or making the goods that are sold during

the period concerned – cost of sales, costs of goods sold

– Salaries and wages

– Rent and rates

– Motor vehicle running expenses

– Insurance

– Printing and stationary

– Heat and light

– Telephone and postage

9.

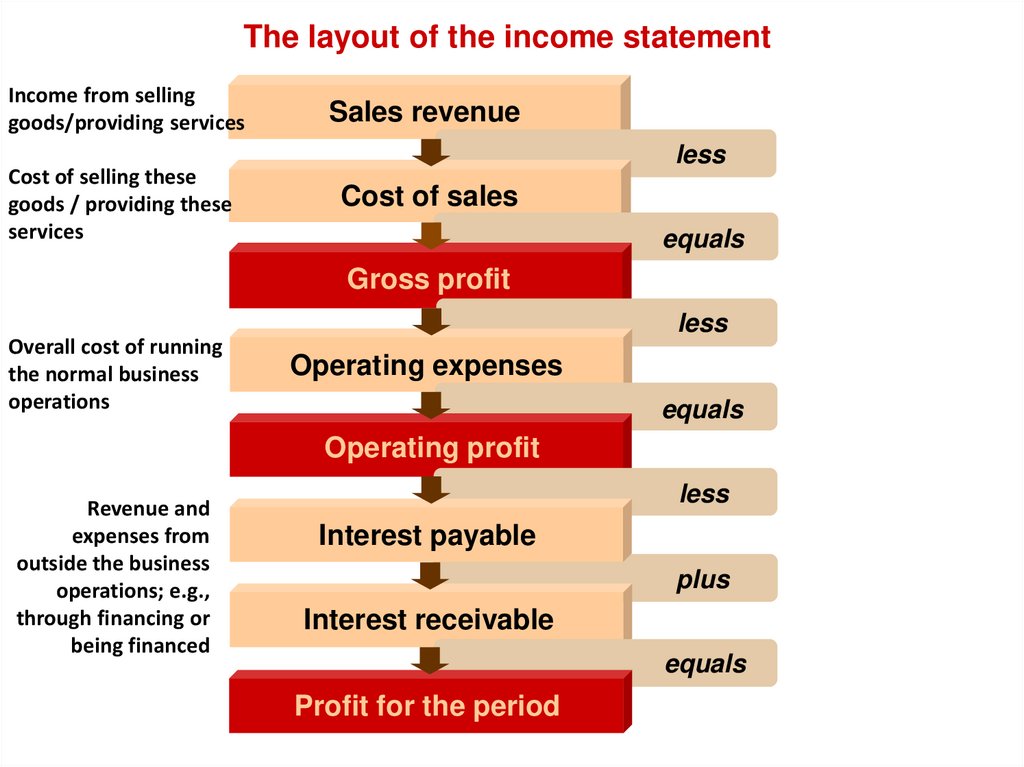

The layout of the income statementIncome from selling

goods/providing services

Cost of selling these

goods / providing these

services

Sales revenue

less

Cost of sales

equals

Gross profit

Overall cost of running

the normal business

operations

less

Operating expenses

equals

Operating profit

Revenue and

expenses from

outside the business

operations; e.g.,

through financing or

being financed

less

Interest payable

plus

Interest receivable

equals

Profit for the period

10.

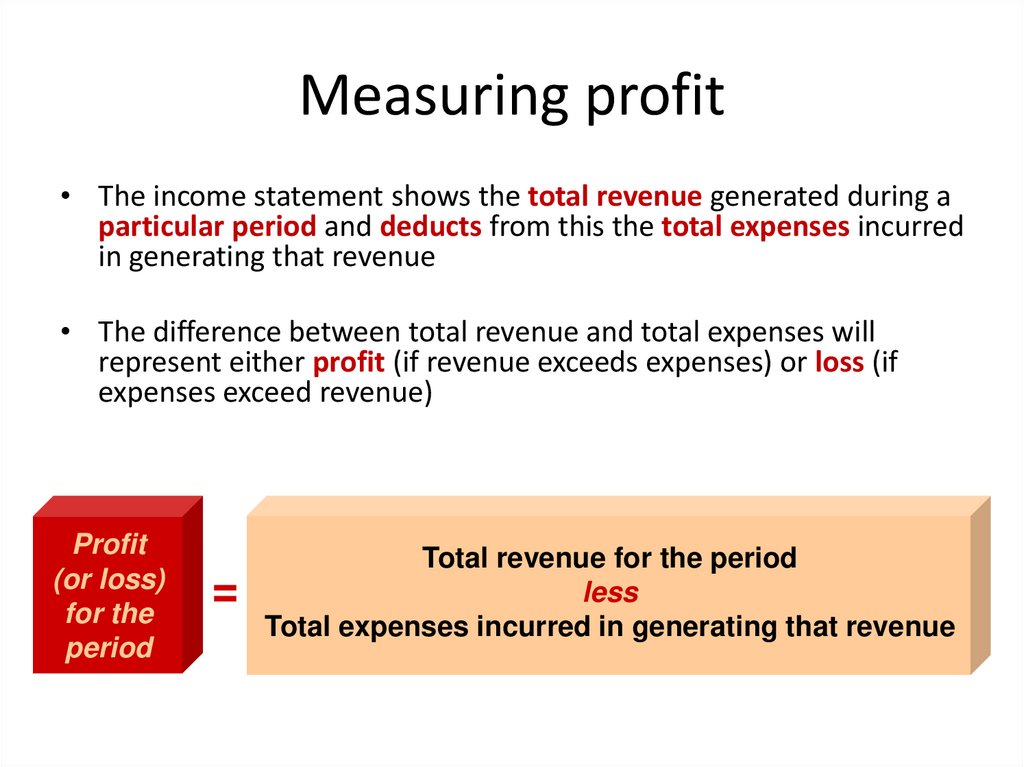

Measuring profit• The income statement shows the total revenue generated during a

particular period and deducts from this the total expenses incurred

in generating that revenue

• The difference between total revenue and total expenses will

represent either profit (if revenue exceeds expenses) or loss (if

expenses exceed revenue)

Profit

(or loss)

for the

period

=

Total revenue for the period

less

Total expenses incurred in generating that revenue

11.

Income statement layout• The layout will vary according to the type of

business to which it relates

• Let’s consider a retail business (a business that

buys goods in their complete state and resells

them)

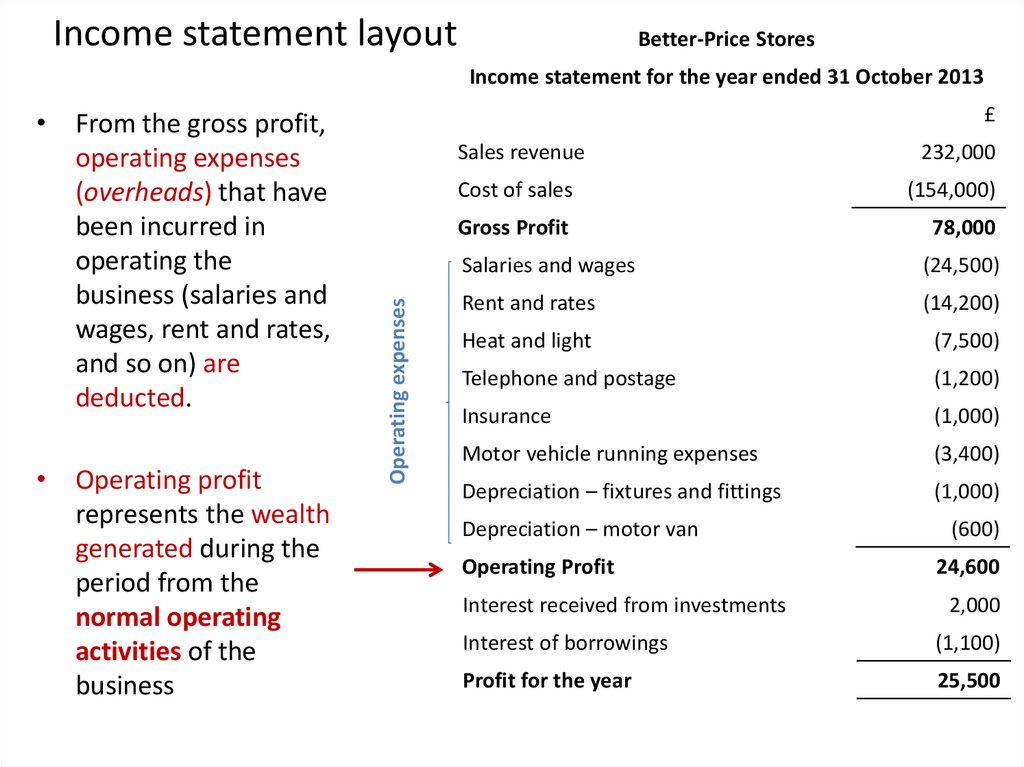

12.

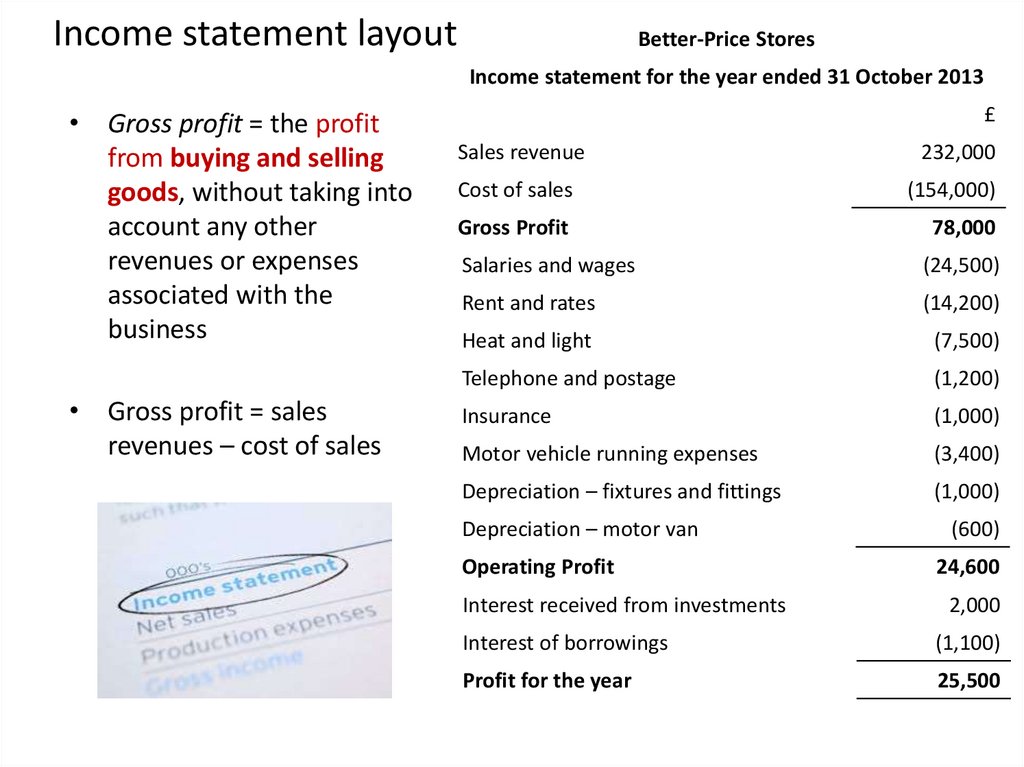

Income statement layoutBetter-Price Stores

Income statement for the year ended 31 October 2013

• Gross profit = the profit

from buying and selling

goods, without taking into

account any other

revenues or expenses

associated with the

business

• Gross profit = sales

revenues – cost of sales

£

Sales revenue

232,000

Cost of sales

(154,000)

Gross Profit

78,000

Salaries and wages

(24,500)

Rent and rates

(14,200)

Heat and light

(7,500)

Telephone and postage

(1,200)

Insurance

(1,000)

Motor vehicle running expenses

(3,400)

Depreciation – fixtures and fittings

(1,000)

Depreciation – motor van

(600)

Operating Profit

24,600

Interest received from investments

2,000

Interest of borrowings

(1,100)

Profit for the year

25,500

13.

Income statement layoutBetter-Price Stores

Income statement for the year ended 31 October 2013

• Operating profit

represents the wealth

generated during the

period from the

normal operating

activities of the

business

£

Operating expenses

• From the gross profit,

operating expenses

(overheads) that have

been incurred in

operating the

business (salaries and

wages, rent and rates,

and so on) are

deducted.

Sales revenue

232,000

Cost of sales

(154,000)

Gross Profit

78,000

Salaries and wages

(24,500)

Rent and rates

(14,200)

Heat and light

(7,500)

Telephone and postage

(1,200)

Insurance

(1,000)

Motor vehicle running expenses

(3,400)

Depreciation – fixtures and fittings

(1,000)

Depreciation – motor van

(600)

Operating Profit

24,600

Interest received from investments

2,000

Interest of borrowings

(1,100)

Profit for the year

25,500

14.

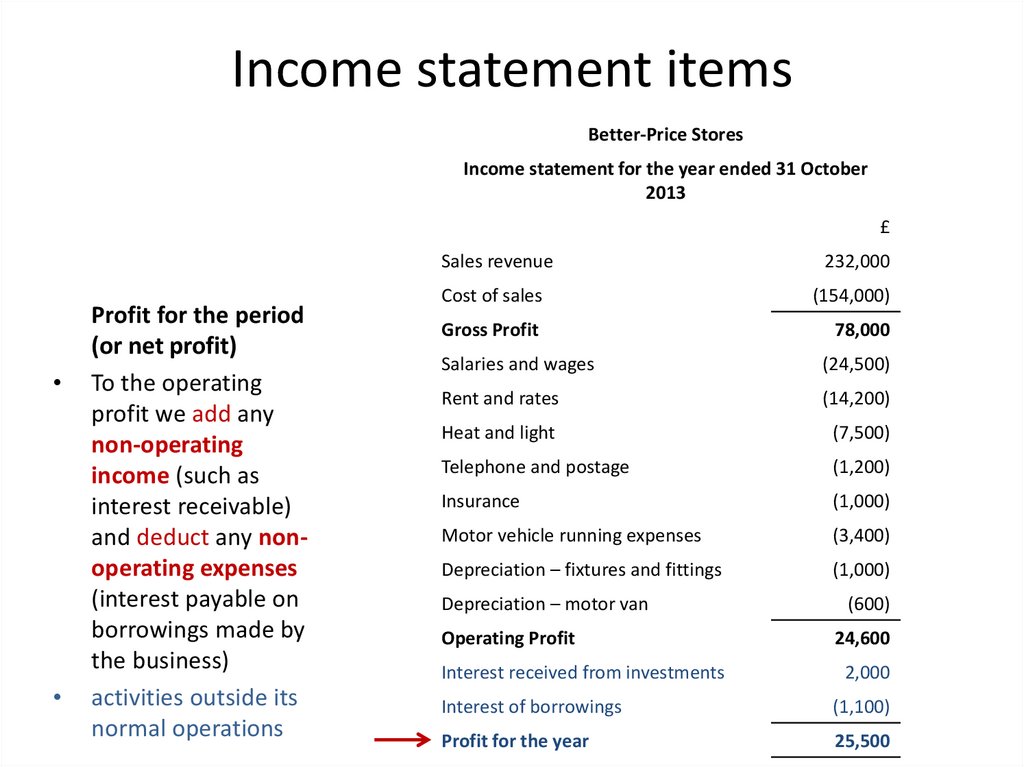

Income statement itemsBetter-Price Stores

Income statement for the year ended 31 October

2013

£

Profit for the period

(or net profit)

To the operating

profit we add any

non-operating

income (such as

interest receivable)

and deduct any nonoperating expenses

(interest payable on

borrowings made by

the business)

activities outside its

normal operations

Sales revenue

232,000

Cost of sales

(154,000)

Gross Profit

78,000

Salaries and wages

(24,500)

Rent and rates

(14,200)

Heat and light

(7,500)

Telephone and postage

(1,200)

Insurance

(1,000)

Motor vehicle running expenses

(3,400)

Depreciation – fixtures and fittings

(1,000)

Depreciation – motor van

(600)

Operating Profit

24,600

Interest received from investments

2,000

Interest of borrowings

(1,100)

Profit for the year

25,500

15.

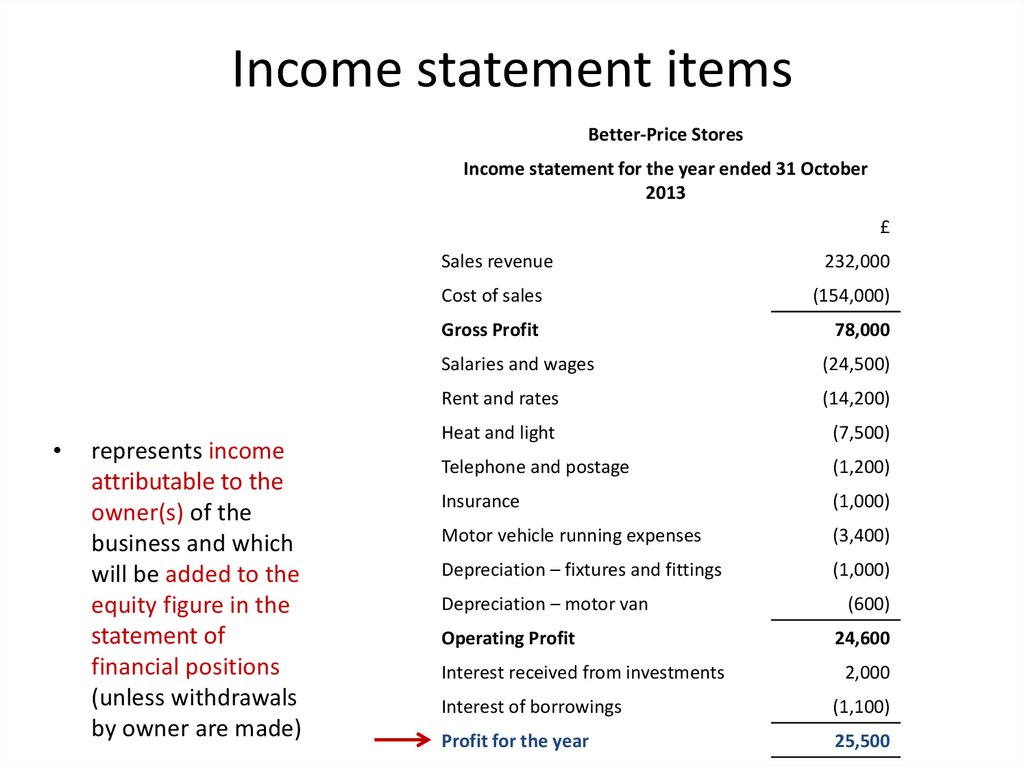

Income statement itemsBetter-Price Stores

Income statement for the year ended 31 October

2013

£

represents income

attributable to the

owner(s) of the

business and which

will be added to the

equity figure in the

statement of

financial positions

(unless withdrawals

by owner are made)

Sales revenue

232,000

Cost of sales

(154,000)

Gross Profit

78,000

Salaries and wages

(24,500)

Rent and rates

(14,200)

Heat and light

(7,500)

Telephone and postage

(1,200)

Insurance

(1,000)

Motor vehicle running expenses

(3,400)

Depreciation – fixtures and fittings

(1,000)

Depreciation – motor van

(600)

Operating Profit

24,600

Interest received from investments

2,000

Interest of borrowings

(1,100)

Profit for the year

25,500

16.

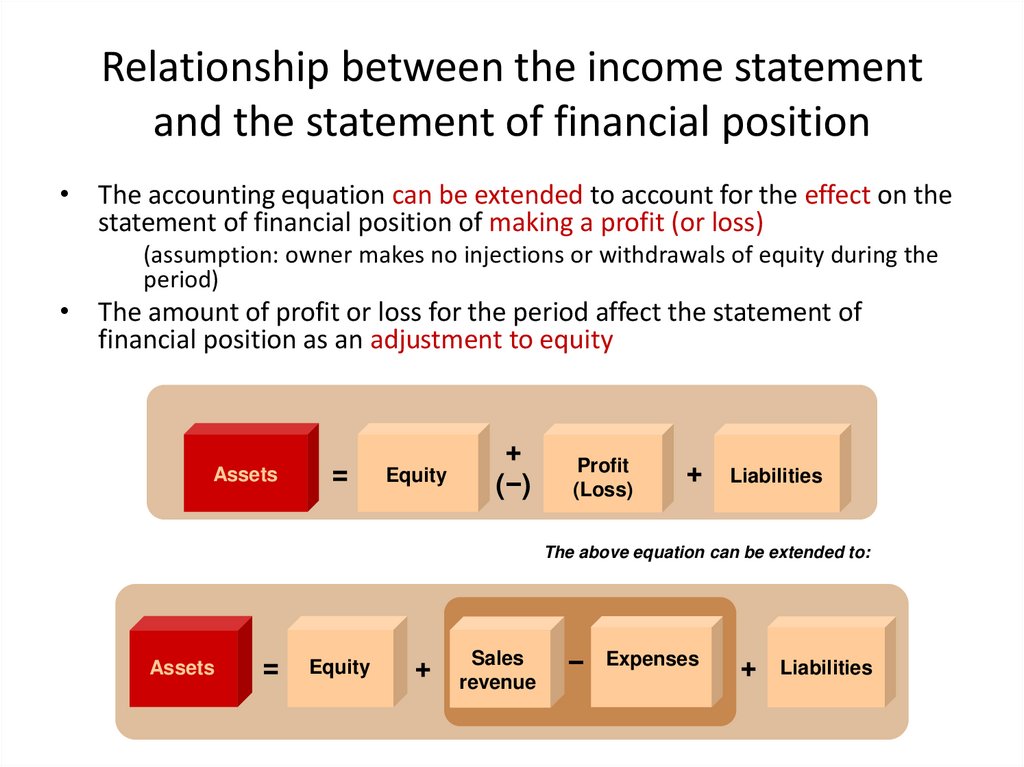

Relationship between the income statementand the statement of financial position

• The accounting equation can be extended to account for the effect on the

statement of financial position of making a profit (or loss)

(assumption: owner makes no injections or withdrawals of equity during the

period)

• The amount of profit or loss for the period affect the statement of

financial position as an adjustment to equity

Assets

=

Equity

+

(−)

Profit

(Loss)

+

Liabilities

The above equation can be extended to:

Assets

=

Equity

+

Sales

revenue

−

Expenses

+

Liabilities

17.

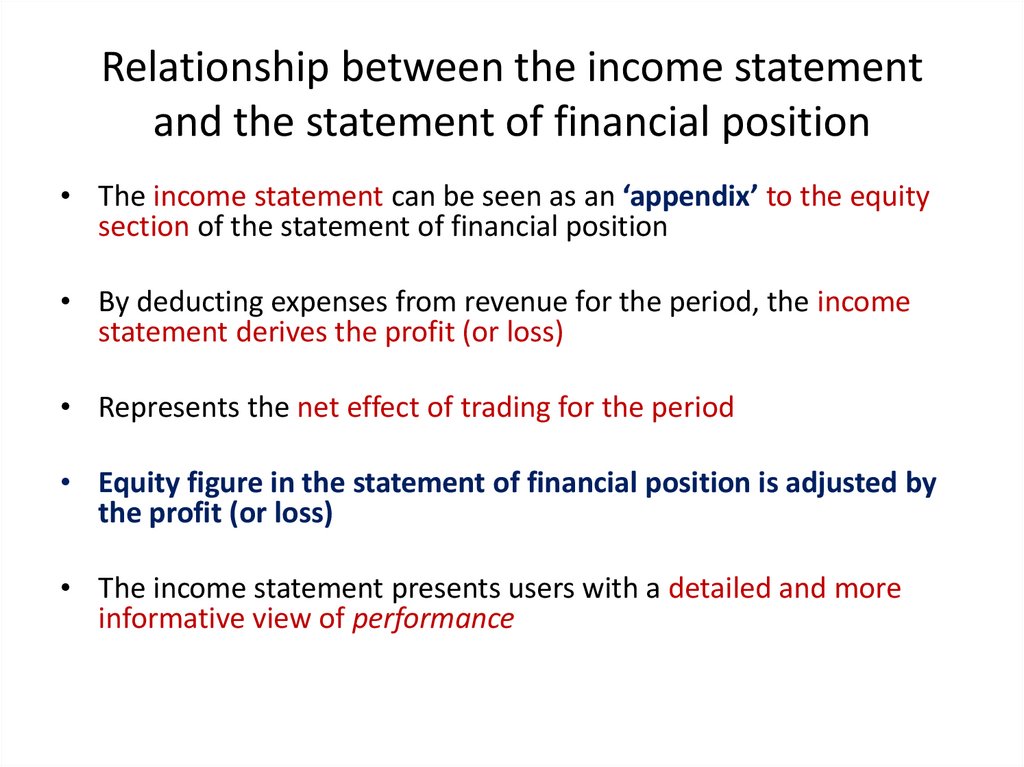

Relationship between the income statementand the statement of financial position

• The income statement can be seen as an ‘appendix’ to the equity

section of the statement of financial position

• By deducting expenses from revenue for the period, the income

statement derives the profit (or loss)

• Represents the net effect of trading for the period

• Equity figure in the statement of financial position is adjusted by

the profit (or loss)

• The income statement presents users with a detailed and more

informative view of performance

18.

Cost of sales£3,500

£2,500

Opening

inventories

£4,000

Purchases of

inventories

during period

£5,000

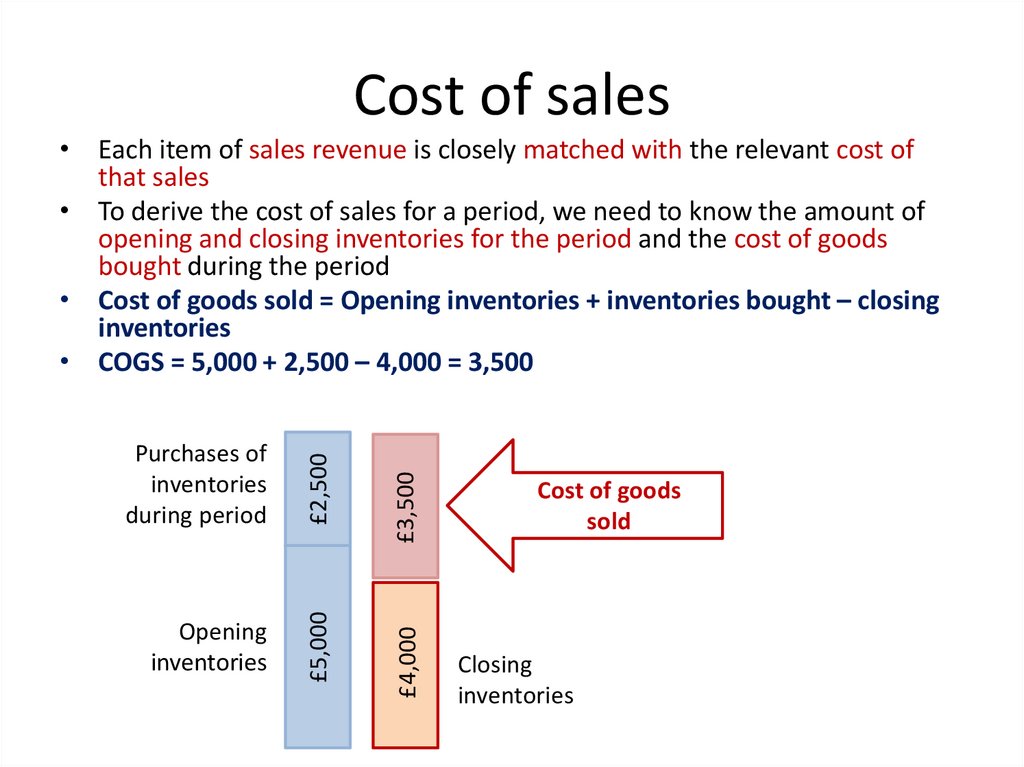

• Each item of sales revenue is closely matched with the relevant cost of

that sales

• To derive the cost of sales for a period, we need to know the amount of

opening and closing inventories for the period and the cost of goods

bought during the period

• Cost of goods sold = Opening inventories + inventories bought – closing

inventories

• COGS = 5,000 + 2,500 – 4,000 = 3,500

Cost of goods

sold

Closing

inventories

19.

Example: Better-PriceStores

Inventories

Closing

Opening

inventories

inventories

bought

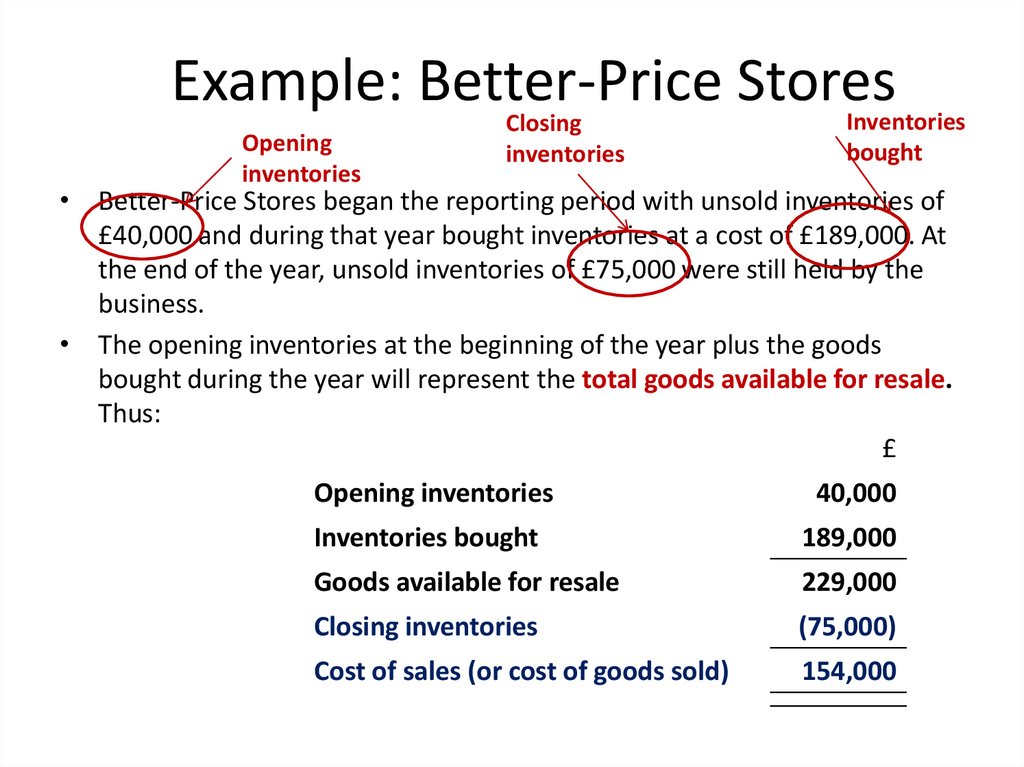

• Better-Price Stores began the reporting period with unsold inventories of

£40,000 and during that year bought inventories at a cost of £189,000. At

the end of the year, unsold inventories of £75,000 were still held by the

business.

• The opening inventories at the beginning of the year plus the goods

bought during the year will represent the total goods available for resale.

Thus:

£

Opening inventories

40,000

Inventories bought

189,000

Goods available for resale

229,000

Closing inventories

(75,000)

Cost of sales (or cost of goods sold)

154,000

20.

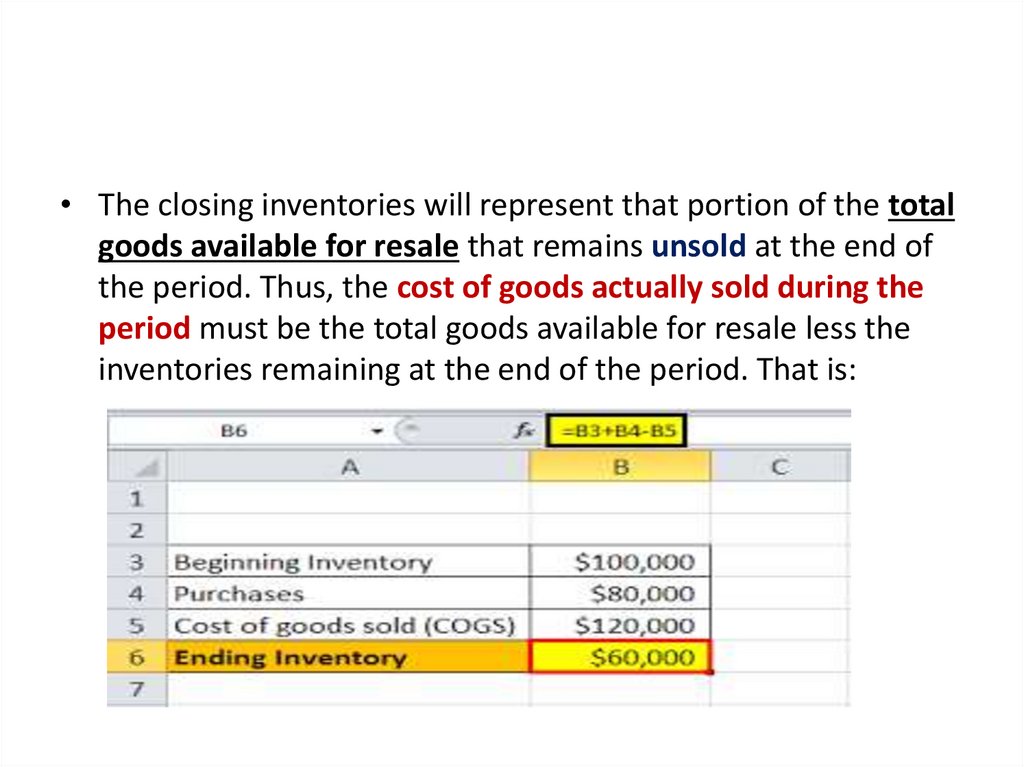

• The closing inventories will represent that portion of the totalgoods available for resale that remains unsold at the end of

the period. Thus, the cost of goods actually sold during the

period must be the total goods available for resale less the

inventories remaining at the end of the period. That is:

21.

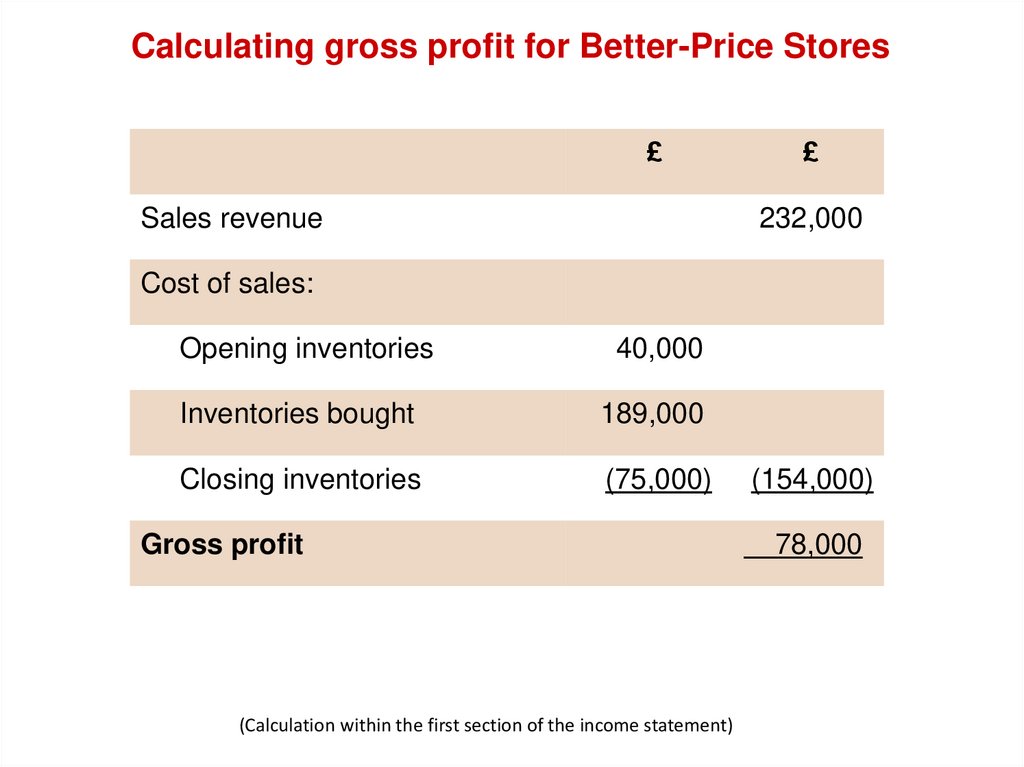

Calculating gross profit for Better-Price Stores£

Sales revenue

£

232,000

Cost of sales:

Opening inventories

40,000

Inventories bought

189,000

Closing inventories

(75,000)

Gross profit

(Calculation within the first section of the income statement)

(154,000)

78,000

22.

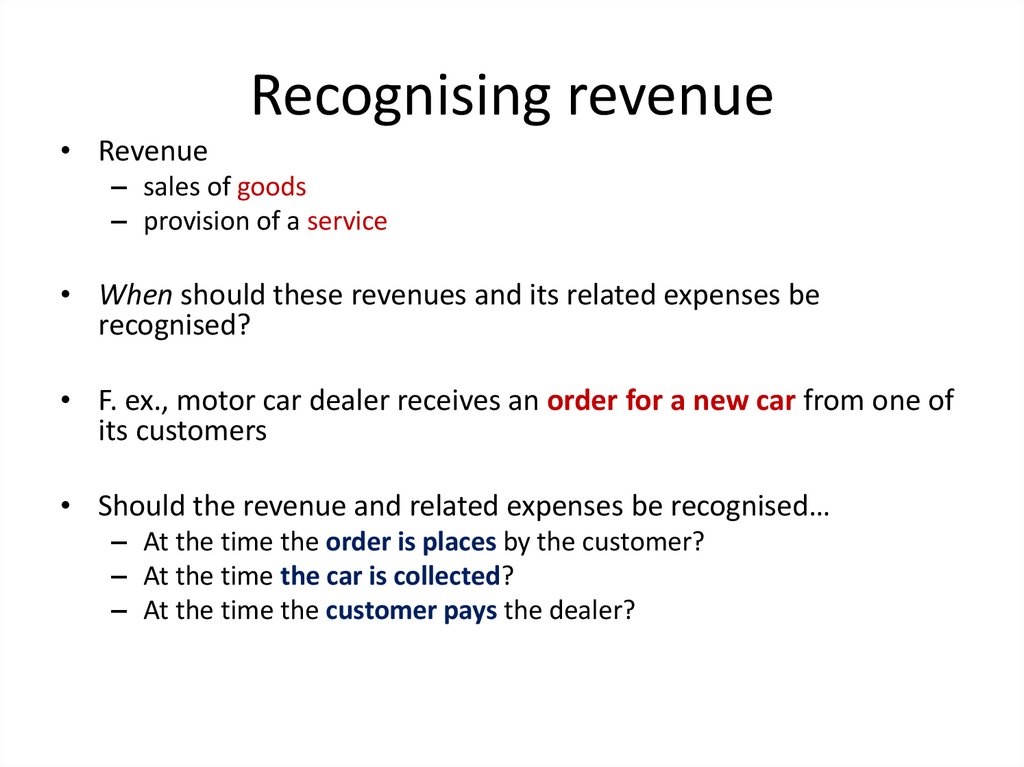

Recognising revenue• Revenue

– sales of goods

– provision of a service

• When should these revenues and its related expenses be

recognised?

• F. ex., motor car dealer receives an order for a new car from one of

its customers

• Should the revenue and related expenses be recognised…

– At the time the order is places by the customer?

– At the time the car is collected?

– At the time the customer pays the dealer?

23.

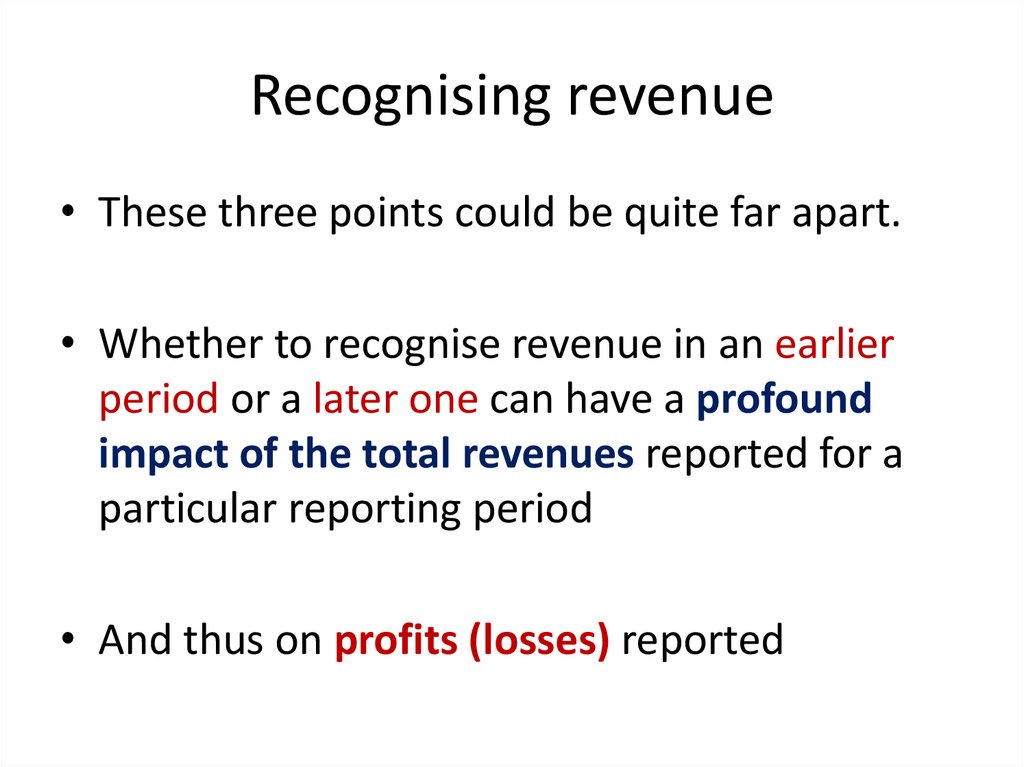

Recognising revenue• These three points could be quite far apart.

• Whether to recognise revenue in an earlier

period or a later one can have a profound

impact of the total revenues reported for a

particular reporting period

• And thus on profits (losses) reported

24.

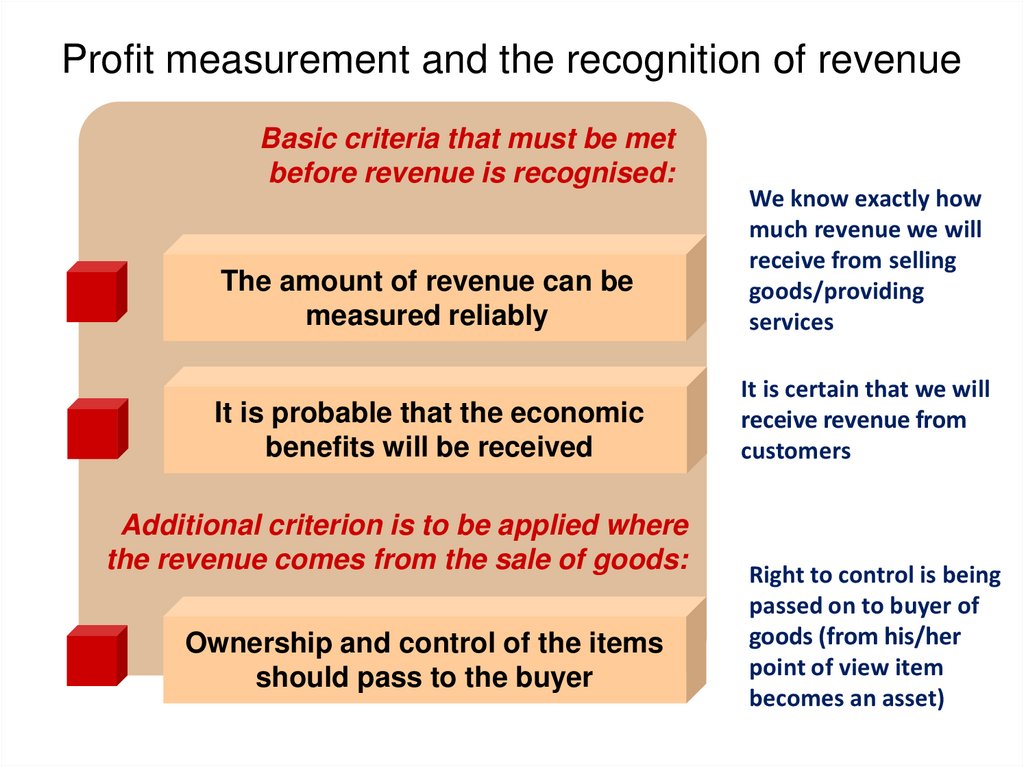

Profit measurement and the recognition of revenueBasic criteria that must be met

before revenue is recognised:

The amount of revenue can be

measured reliably

We know exactly how

much revenue we will

receive from selling

goods/providing

services

It is probable that the economic

benefits will be received

It is certain that we will

receive revenue from

customers

Additional criterion is to be applied where

the revenue comes from the sale of goods:

Ownership and control of the items

should pass to the buyer

Right to control is being

passed on to buyer of

goods (from his/her

point of view item

becomes an asset)

25.

Recognising revenue• Problems arise when revenues and its

expenses stretch over more than one

reporting period

– Revenues from long-contracts

– Revenues from services

26.

Recognising revenue from long-termcontracts

• Contracts can last for more than one reporting period

• If the business waits until the contract is completely

fulfilled before recognising revenue, the income statement

could give a misleading picture of the wealth generated in

the various reporting periods covered by the contract

• Example: construction contract to build a new factory over

three years

– It is possible to recognise revenue before that factory is

completed, provided that the building work can be broken down

into a number of stages and each stage can be measured

reliably

27.

Example: construction contractsStage 1: clearing and levelling the land and putting in the

foundations

Stage 2: building the walls

Stage 3: putting on the roof

Stage 4: putting in the windows and completing all the interior

work

• Each stage can be awarded a separate price with the total

for all the stages being equal to the total contract price for

the factory

• Builder can recognise the price for each completed stage as

revenue and bill the customer accordingly

28.

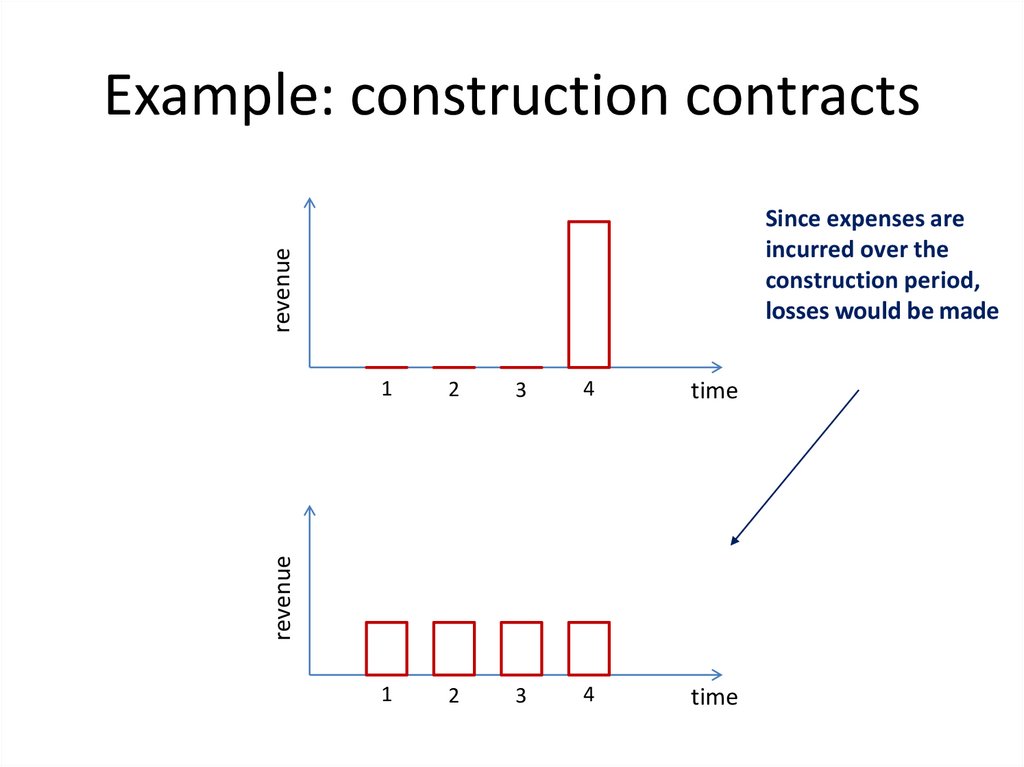

Example: construction contractsrevenue

Since expenses are

incurred over the

construction period,

losses would be made

2

3

4

time

1

2

3

4

time

revenue

1

29.

Recognising revenue from services• Same approach as that used in the construction

contract

• Example: introduction of a new computer system for a

government, which take several years to complete

– Broken down into stages, and each stage can be measured

reliably

• Continuous services

– Benefits from providing the service are usually assumed to

flow evenly over time and so revenue is recognised evenly

over the subscription period

30.

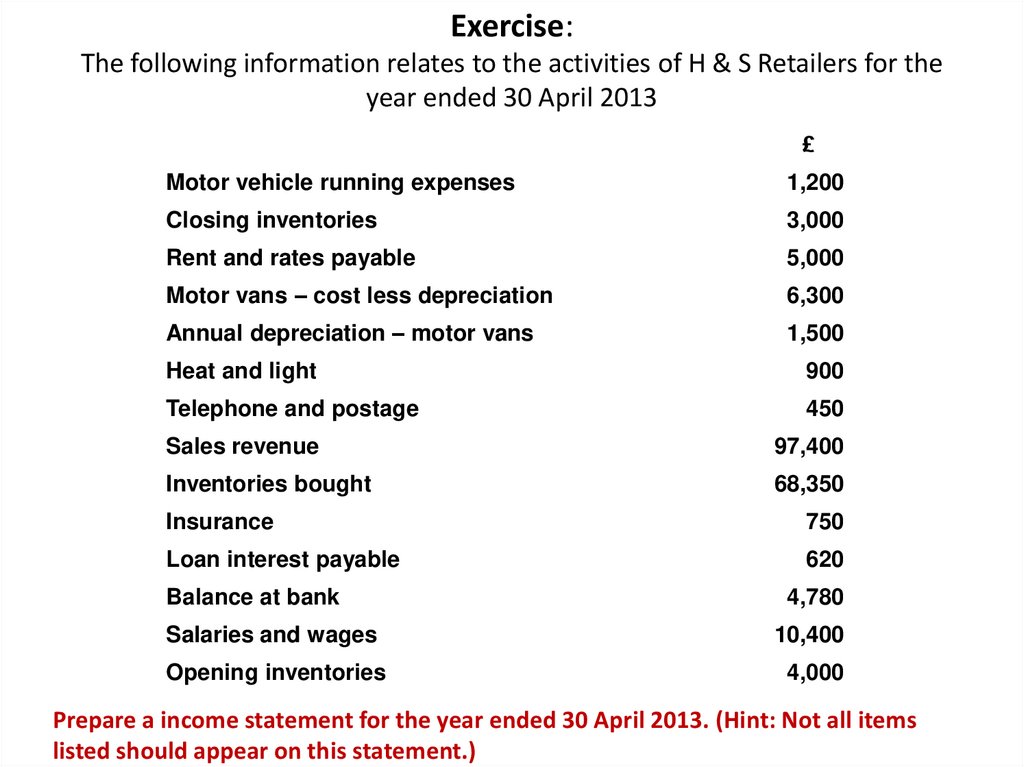

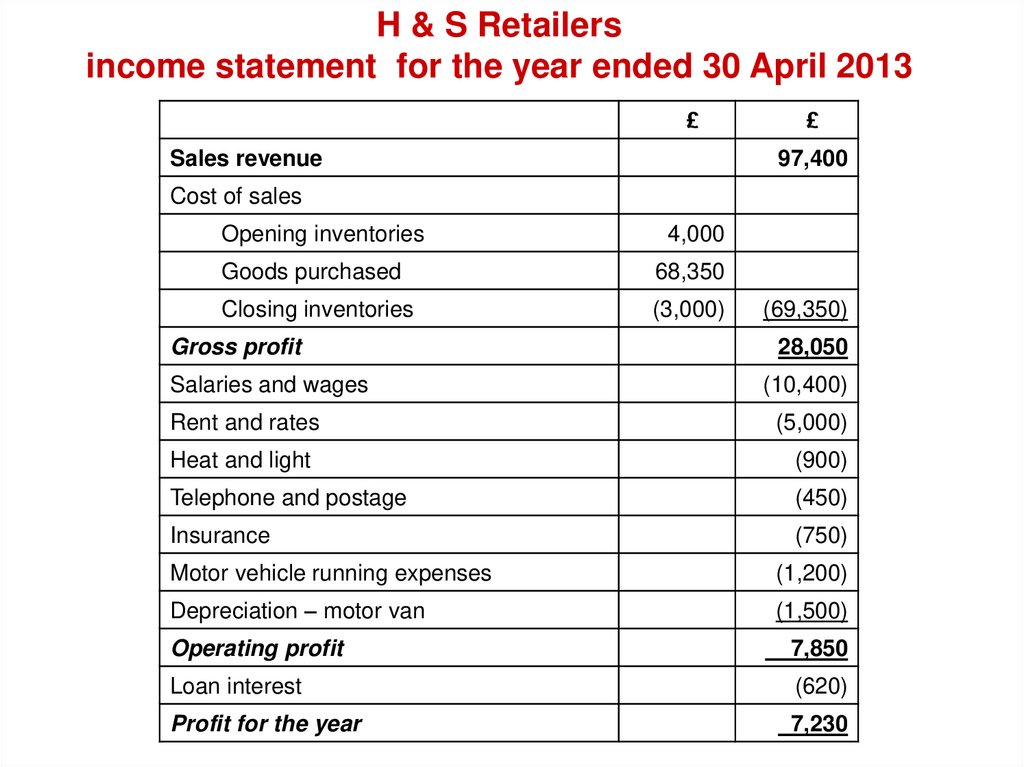

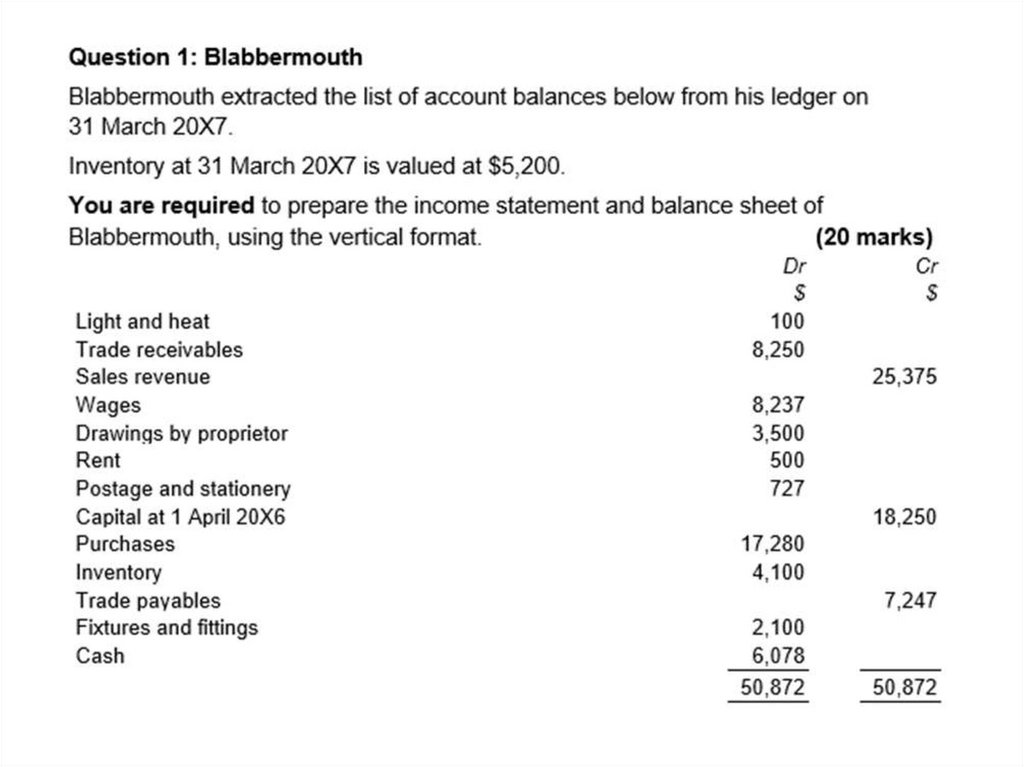

Exercise:The following information relates to the activities of H & S Retailers for the

year ended 30 April 2013

£

Motor vehicle running expenses

1,200

Closing inventories

3,000

Rent and rates payable

5,000

Motor vans – cost less depreciation

6,300

Annual depreciation – motor vans

1,500

Heat and light

900

Telephone and postage

450

Sales revenue

97,400

Inventories bought

68,350

Insurance

750

Loan interest payable

620

Balance at bank

4,780

Salaries and wages

10,400

Opening inventories

4,000

Prepare a income statement for the year ended 30 April 2013. (Hint: Not all items

listed should appear on this statement.)

31.

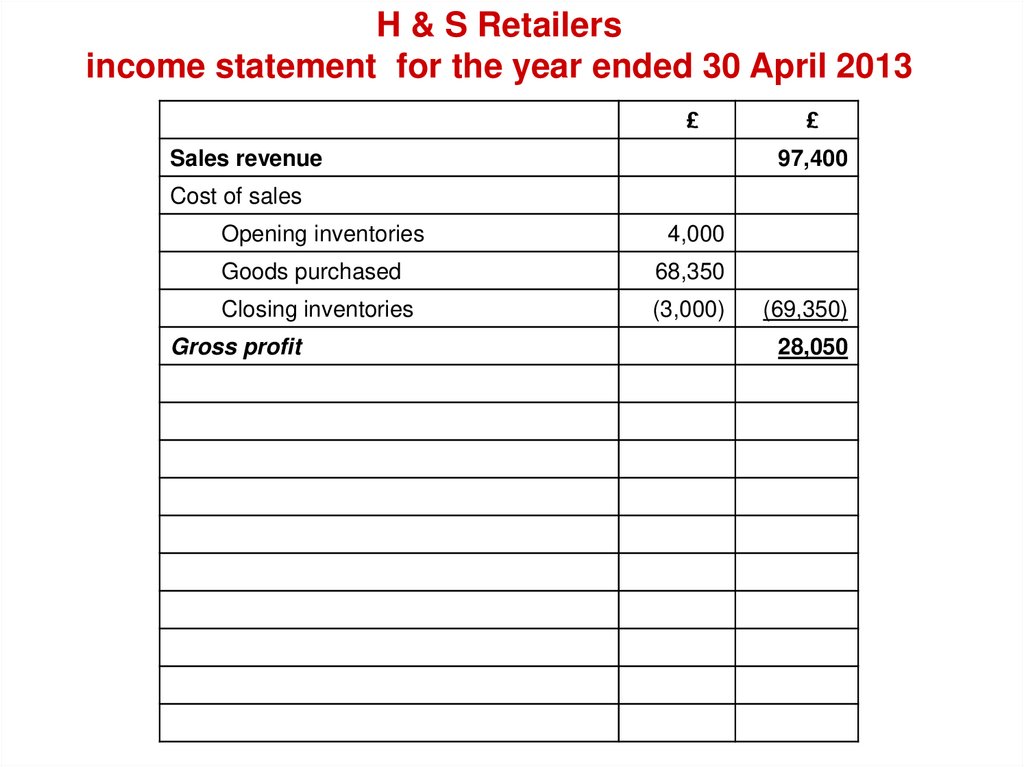

H & S Retailersincome statement for the year ended 30 April 2013

£

£

32.

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

33.

H & S Retailersincome statement for the year ended 30 April 2013

£

£

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

(69,350)

34.

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

Gross profit

(69,350)

28,050

35.

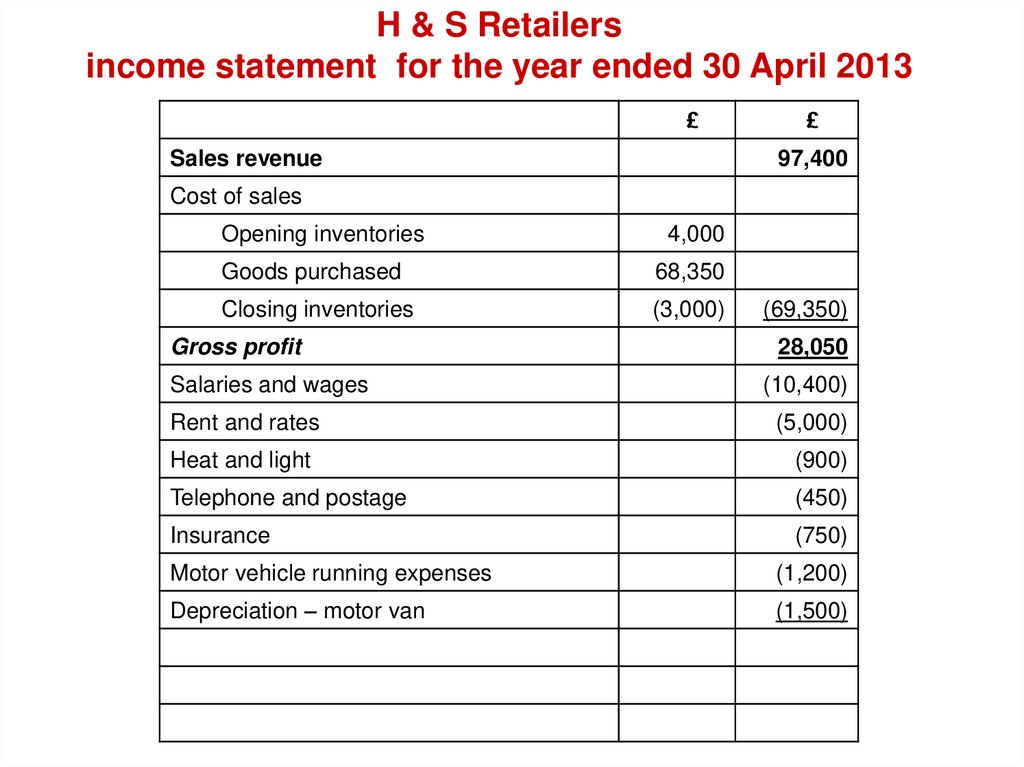

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

(69,350)

Gross profit

28,050

Salaries and wages

(10,400)

Rent and rates

(5,000)

Heat and light

(900)

Telephone and postage

(450)

Insurance

(750)

Motor vehicle running expenses

(1,200)

Depreciation – motor van

(1,500)

36.

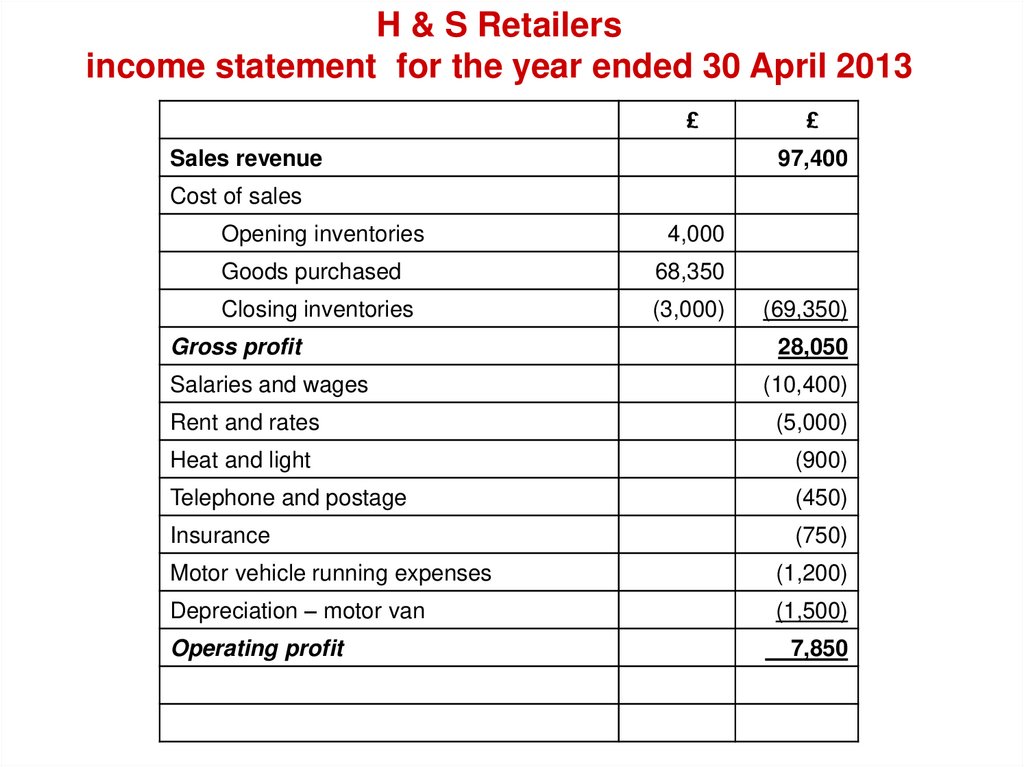

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

(69,350)

Gross profit

28,050

Salaries and wages

(10,400)

Rent and rates

(5,000)

Heat and light

(900)

Telephone and postage

(450)

Insurance

(750)

Motor vehicle running expenses

(1,200)

Depreciation – motor van

(1,500)

Operating profit

7,850

37.

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

(69,350)

Gross profit

28,050

Salaries and wages

(10,400)

Rent and rates

(5,000)

Heat and light

(900)

Telephone and postage

(450)

Insurance

(750)

Motor vehicle running expenses

(1,200)

Depreciation – motor van

(1,500)

Operating profit

7,850

Loan interest

(620)

38.

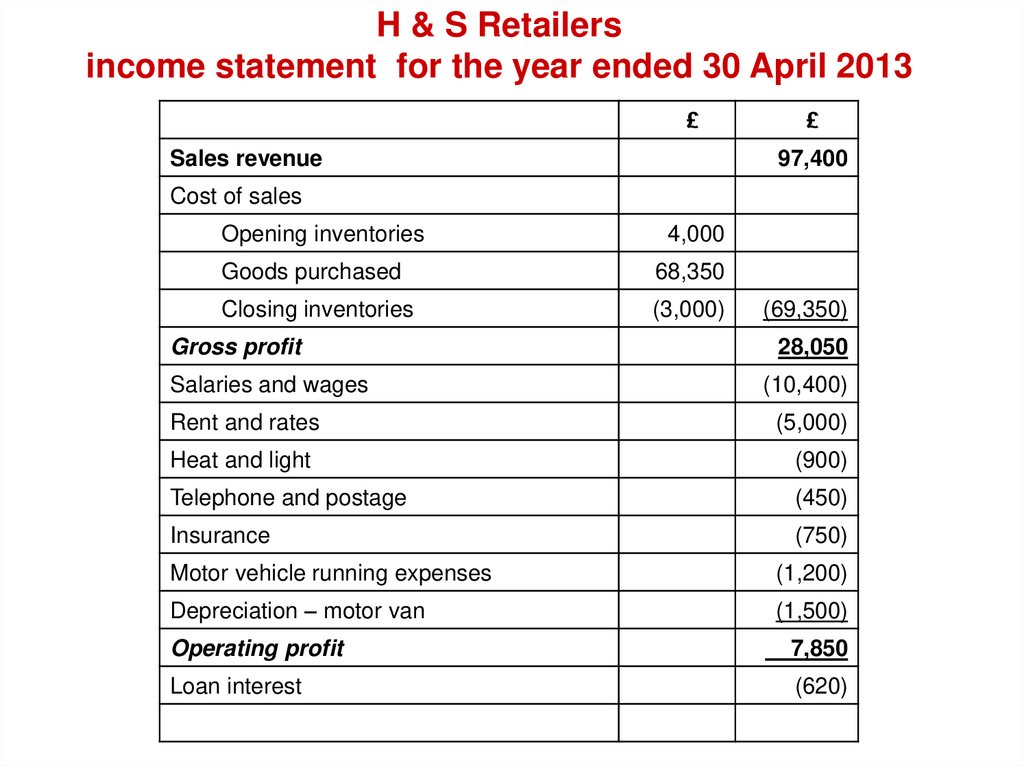

H & S Retailersincome statement for the year ended 30 April 2013

£

Sales revenue

£

97,400

Cost of sales

Opening inventories

4,000

Goods purchased

68,350

Closing inventories

(3,000)

(69,350)

Gross profit

28,050

Salaries and wages

(10,400)

Rent and rates

(5,000)

Heat and light

(900)

Telephone and postage

(450)

Insurance

(750)

Motor vehicle running expenses

(1,200)

Depreciation – motor van

(1,500)

Operating profit

7,850

Loan interest

(620)

Profit for the year

7,230

39.

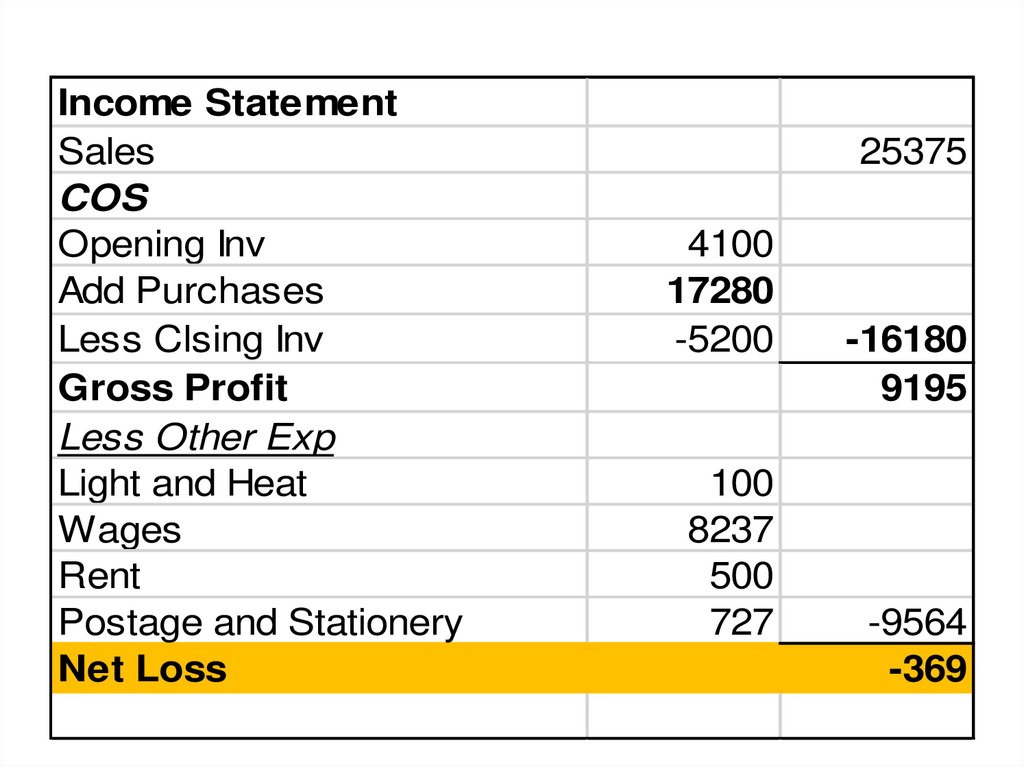

40.

Income StatementSales

COS

Opening Inv

Add Purchases

Less Clsing Inv

Gross Profit

Less Other Exp

Light and Heat

Wages

Rent

Postage and Stationery

Net Loss

25375

4100

17280

-5200

100

8237

500

727

-16180

9195

-9564

-369

41.

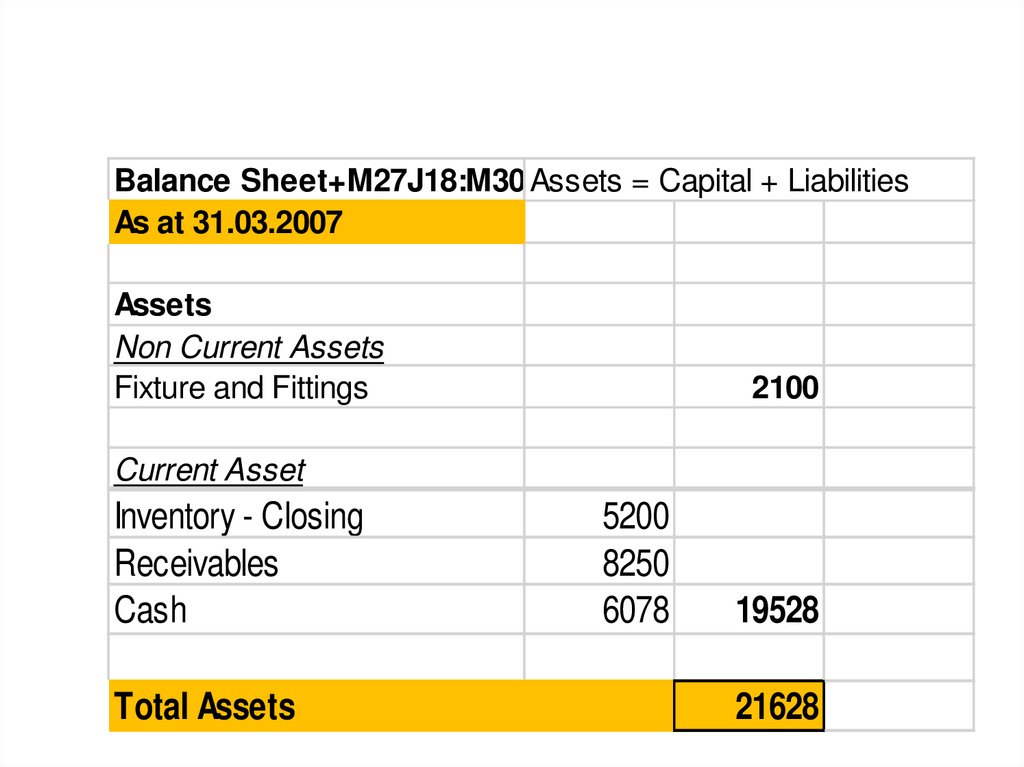

Balance Sheet+M27J18:M30 Assets = Capital + LiabilitiesAs at 31.03.2007

Assets

Non Current Assets

Fixture and Fittings

2100

Current Asset

Inventory - Closing

Receivables

Cash

Total Assets

5200

8250

6078

19528

21628

42.

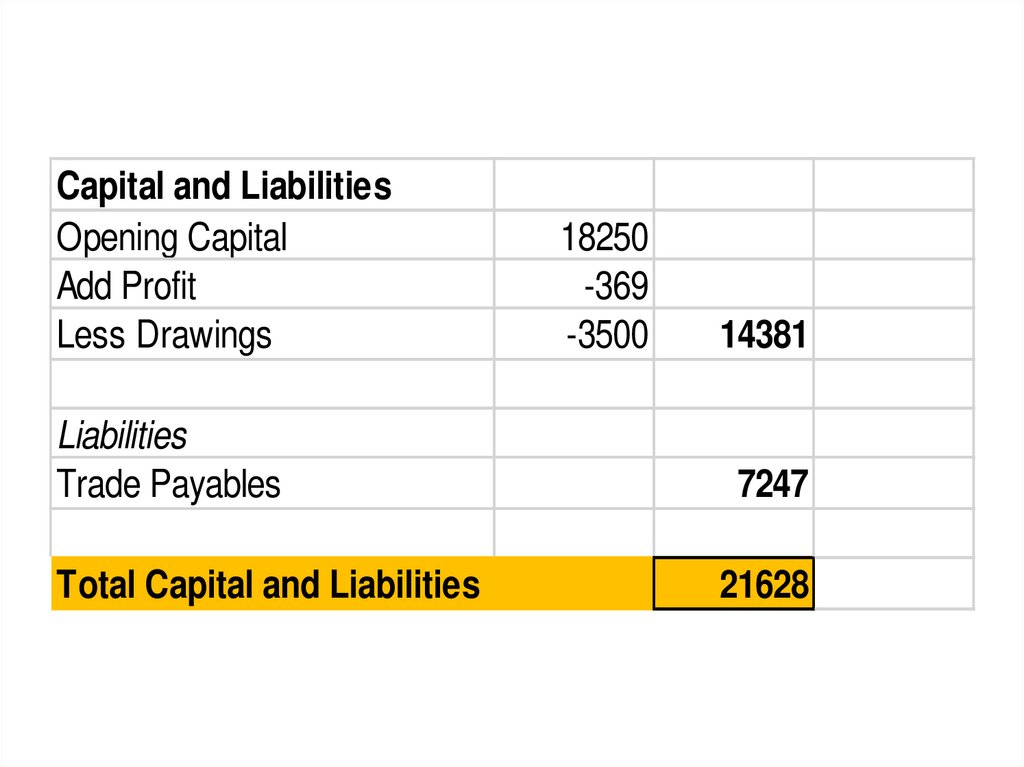

Capital and LiabilitiesOpening Capital

Add Profit

Less Drawings

18250

-369

-3500

14381

Liabilities

Trade Payables

7247

Total Capital and Liabilities

21628

43.

Exercise44.

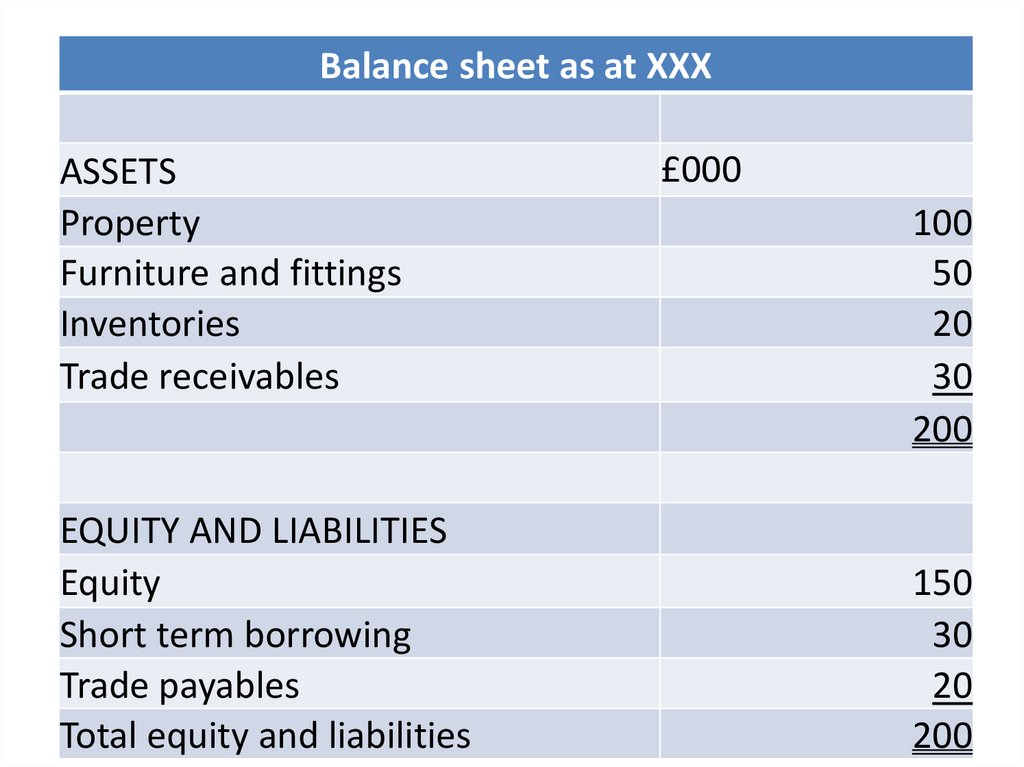

Balance sheet as at XXXASSETS

Property

Furniture and fittings

Inventories

Trade receivables

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

£000

100

50

20

30

200

150

30

20

200

45.

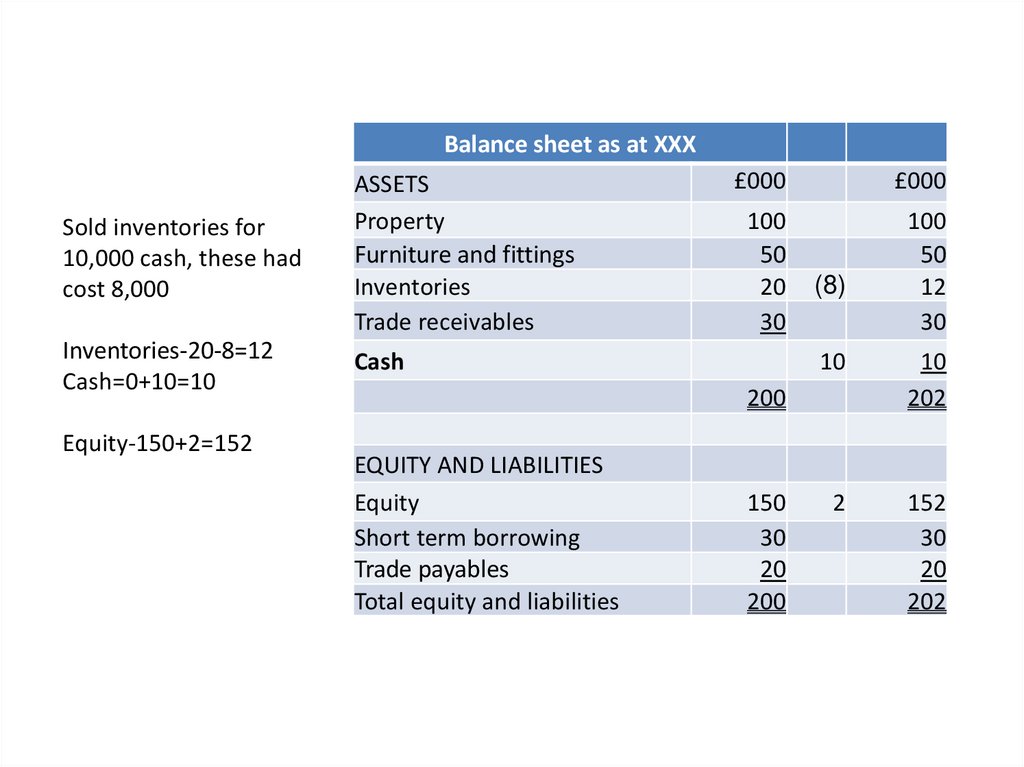

Balance sheet as at XXXSold inventories for

10,000 cash, these had

cost 8,000

ASSETS

Property

Furniture and fittings

Inventories

Trade receivables

Inventories-20-8=12

Cash=0+10=10

Cash

Equity-150+2=152

£000

£000

100

50

20

30

100

50

12

30

(8)

10

10

202

2

152

30

20

202

200

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

150

30

20

200

46.

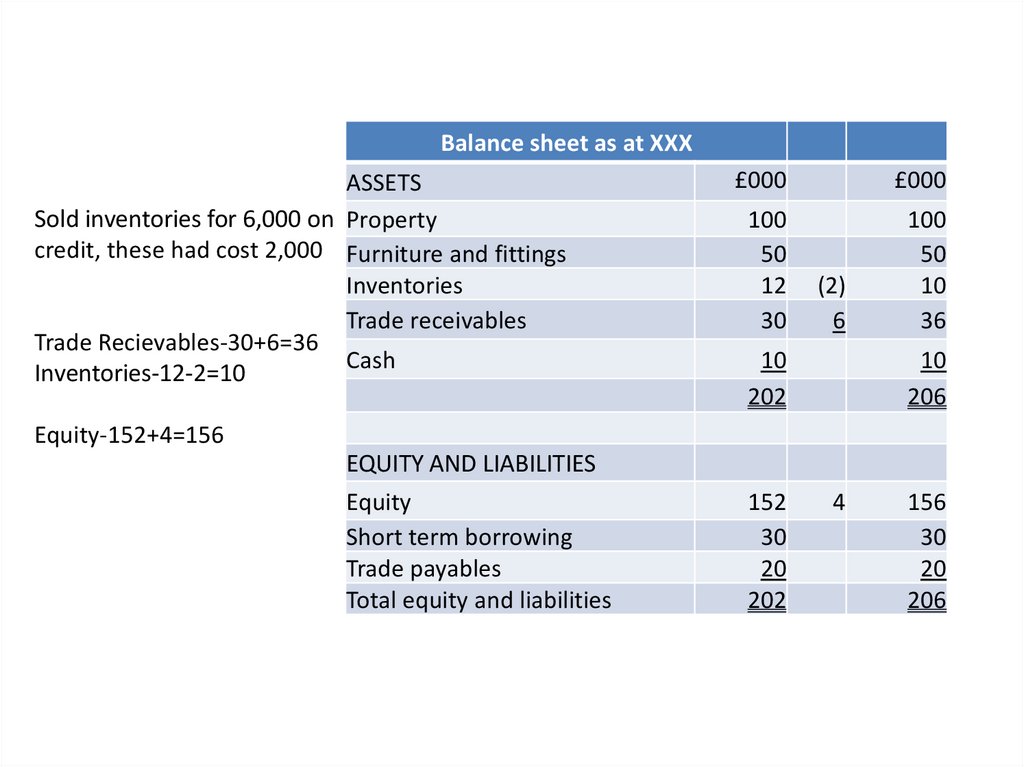

Balance sheet as at XXXASSETS

Sold inventories for 6,000 on Property

credit, these had cost 2,000 Furniture and fittings

Inventories

Trade receivables

Trade Recievables-30+6=36

Cash

Inventories-12-2=10

£000

£000

100

50

12

30

100

50

10

36

(2)

6

10

202

10

206

Equity-152+4=156

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

152

30

20

202

4

156

30

20

206

47.

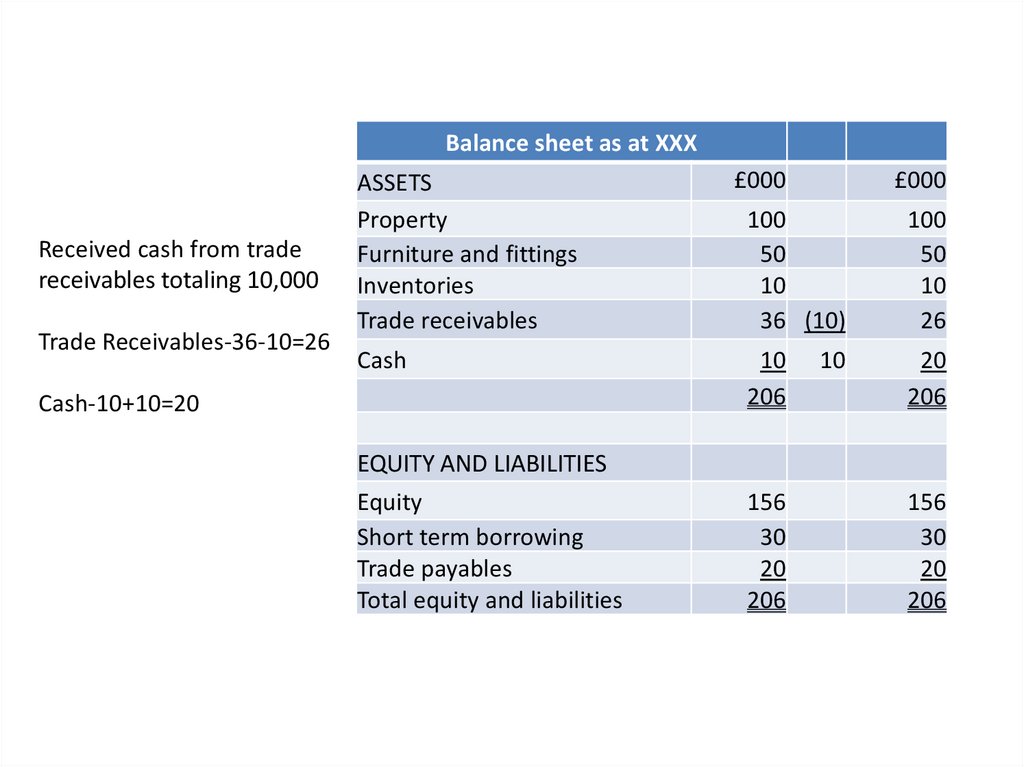

Balance sheet as at XXXReceived cash from trade

receivables totaling 10,000

Trade Receivables-36-10=26

ASSETS

Property

Furniture and fittings

Inventories

Trade receivables

£000

£000

100

50

10

36 (10)

100

50

10

26

Cash

10

206

20

206

Cash-10+10=20

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

156

30

20

206

10

156

30

20

206

48.

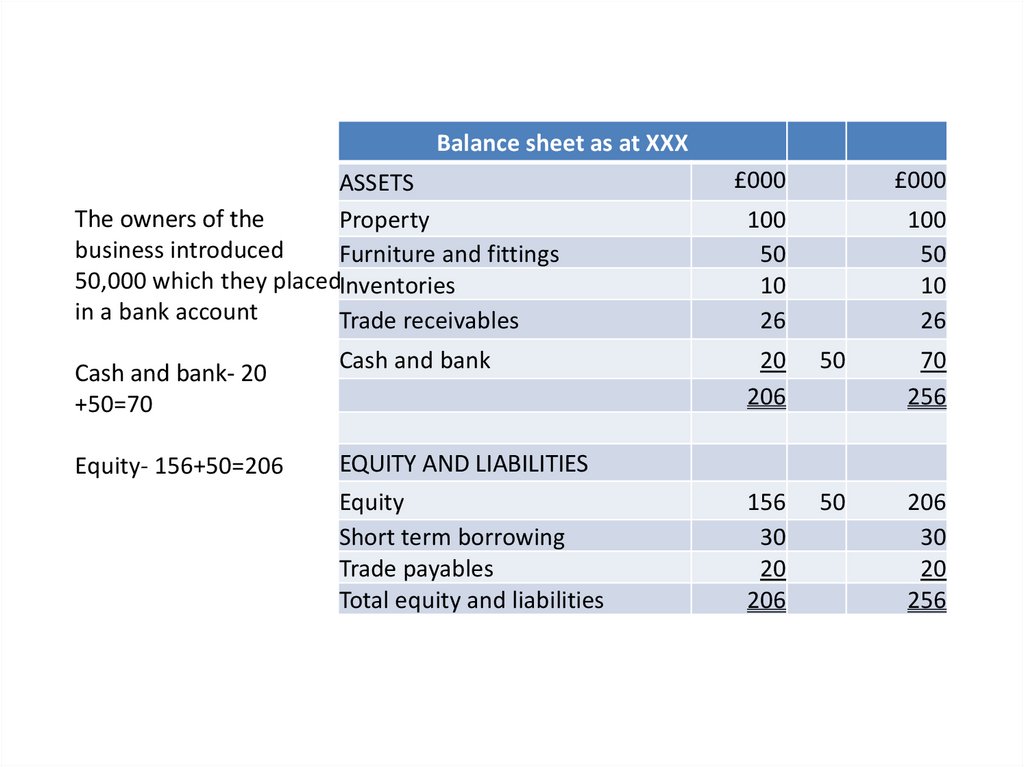

Balance sheet as at XXXASSETS

The owners of the

Property

business introduced

Furniture and fittings

50,000 which they placedInventories

in a bank account

Trade receivables

Cash and bank- 20

+50=70

Equity- 156+50=206

Cash and bank

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

£000

£000

100

50

10

26

100

50

10

26

20

206

50

70

256

156

30

20

206

50

206

30

20

256

49.

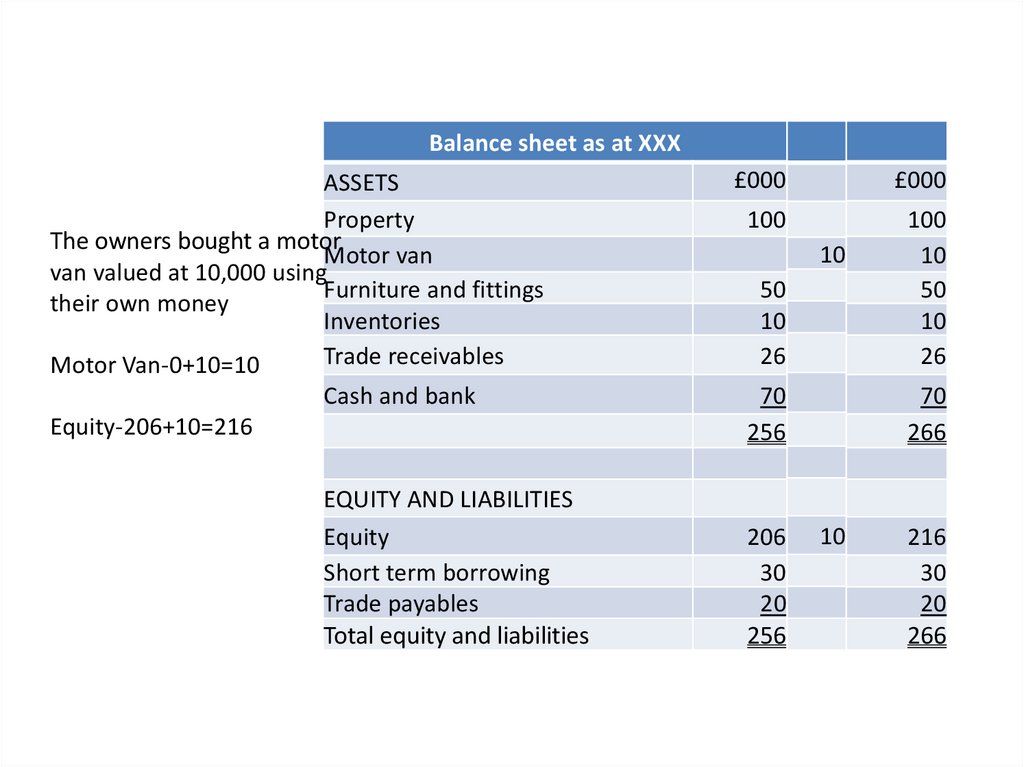

Balance sheet as at XXXASSETS

Property

The owners bought a motor

Motor van

van valued at 10,000 using

Furniture and fittings

their own money

Inventories

Trade receivables

Motor Van-0+10=10

Cash and bank

Equity-206+10=216

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

£000

£000

100

50

10

26

100

10

50

10

26

70

256

70

266

10

206

30

20

256

10

216

30

20

266

50.

Balance sheet as at XXXASSETS

Property

Bought inventories on credit Motor van

Furniture and fittings

for 14,000

Inventories

Trade receivables

Inventories-10+14=24

Trade Payables- 20+14=34

Cash and bank

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

£000

£000

100

10

50

10

26

100

10

50

24

26

14

70

266

70

280

216

30

20

266

216

30

34

280

14

51.

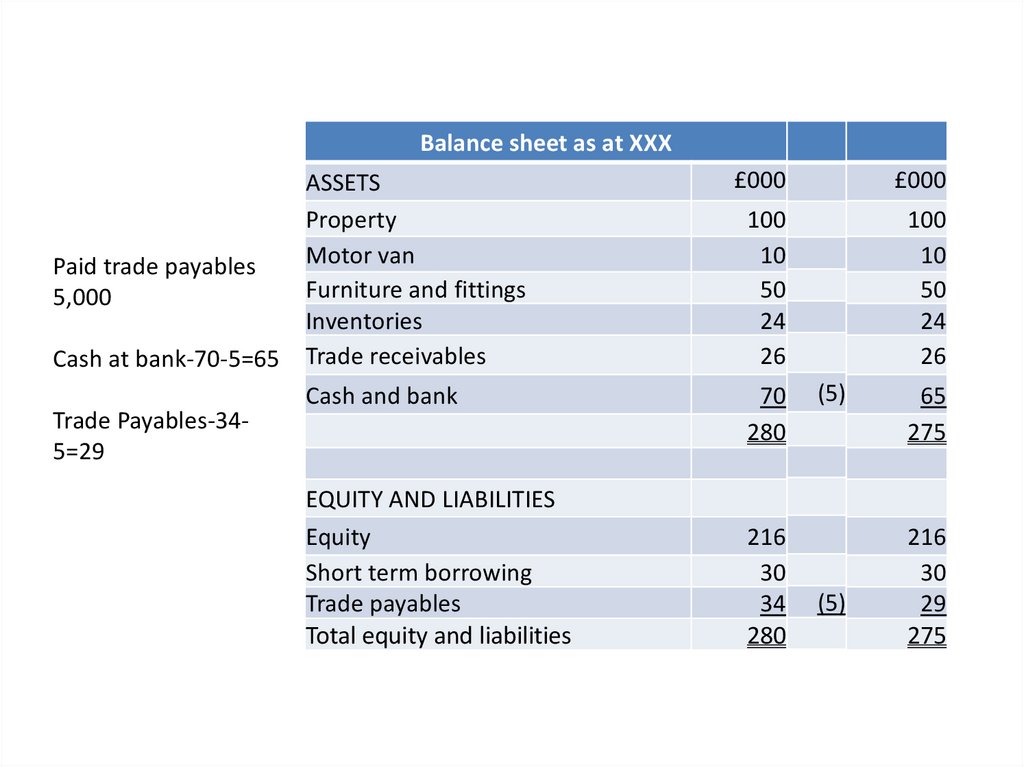

Balance sheet as at XXXPaid trade payables

5,000

Cash at bank-70-5=65

Trade Payables-345=29

ASSETS

Property

Motor van

Furniture and fittings

Inventories

Trade receivables

£000

£000

100

10

50

24

26

100

10

50

24

26

Cash and bank

70

280

EQUITY AND LIABILITIES

Equity

Short term borrowing

Trade payables

Total equity and liabilities

216

30

34

280

(5)

(5)

65

275

216

30

29

275

52.

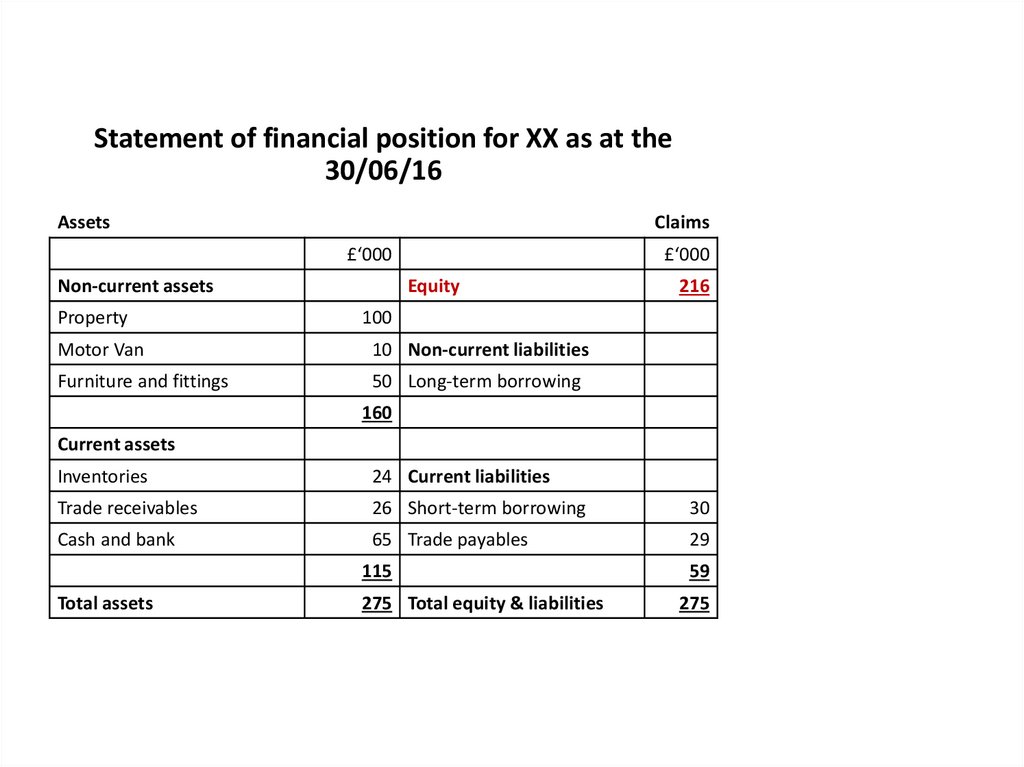

Statement of financial position for XX as at the30/06/16

Assets

Claims

£‘000

Non-current assets

£‘000

Equity

Property

100

Motor Van

10 Non-current liabilities

Furniture and fittings

50 Long-term borrowing

216

160

Current assets

Inventories

24 Current liabilities

Trade receivables

26 Short-term borrowing

30

Cash and bank

65 Trade payables

29

115

59

275 Total equity & liabilities

275

Total assets