economics

economics law

lawSimilar presentations:

")

Ryanair & Aer Lingus

1.

Ryanair & Aer LingusMerger Case

Evstafyev Dmitriy

Orlov Konstantin

Stefanov Kirill

Ponomarev Sergey

2.

AGENDASUMMARY

BACKGROUND INFORMATION ON THE FIRMS AND MARKET

BRIEF OVERVIEW OF THE ENTRY DETERRENCE AND EFFICIENCY GAINS MODELS

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

APPEALS OF BOTH PARTIES

SECOND AND THIRD MERGER ATTEMPTS

THE EVOLUTION OF THE MARKET AFTER DECISION

3.

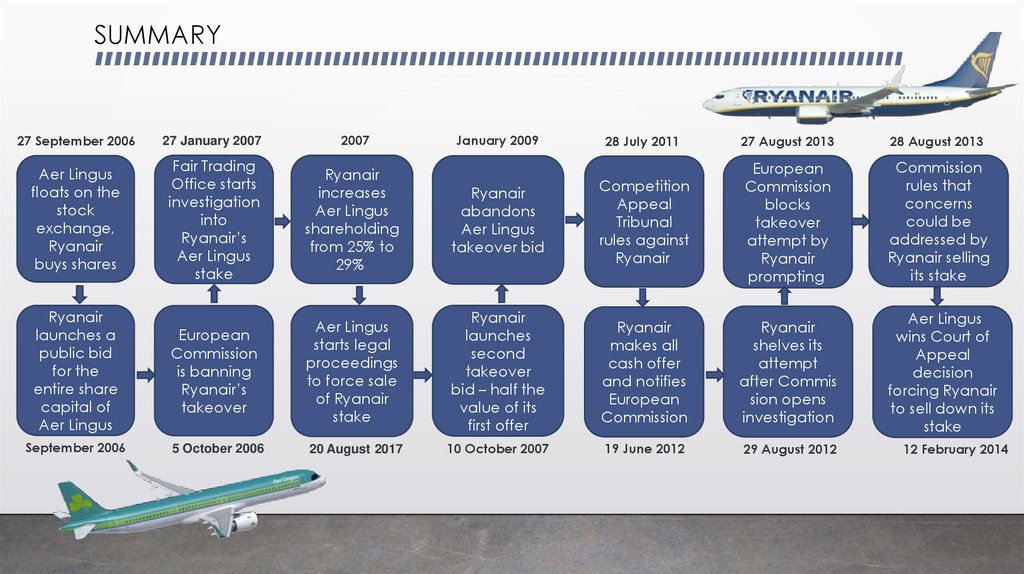

SUMMARY27 September 2006

27 January 2007

2007

Aer Lingus

floats on the

stock

exchange,

Ryanair

buys shares

Fair Trading

Office starts

investigation

into

Ryanair’s

Aer Lingus

stake

Ryanair

increases

Aer Lingus

shareholding

from 25% to

29%

European

Commission

is banning

Ryanair’s

takeover

Aer Lingus

starts legal

proceedings

to force sale

of Ryanair

stake

5 October 2006

20 August 2017

Ryanair

launches a

public bid

for the

entire share

capital of

Aer Lingus

September 2006

January 2009

28 July 2011

27 August 2013

28 August 2013

Ryanair

abandons

Aer Lingus

takeover bid

Competition

Appeal

Tribunal

rules against

Ryanair

European

Commission

blocks

takeover

attempt by

Ryanair

prompting

Commission

rules that

concerns

could be

addressed by

Ryanair selling

its stake

Ryanair

launches

second

takeover

bid – half the

value of its

first offer

Ryanair

makes all

cash offer

and notifies

European

Commission

Ryanair

shelves its

attempt

after Commis

sion opens

investigation

Aer Lingus

wins Court of

Appeal

decision

forcing Ryanair

to sell down its

stake

10 October 2007

19 June 2012

29 August 2012

12 February 2014

4.

BACKGROUND INFORMATION ON THE FIRMSIreland‘s old ”flag carrier“

3 bases (Dublin, Cork and Shannon)

Operated mostly a short-haul network on

70 routes between Ireland and the UK

Fleet of 28 aircraft in 2006

Publicly limited company

Privatized by the Irish Government in 2006

Europe‘s largest low frills carrier

51 bases (Dublin, Brussels South, Milan

Bergamo and Stansted etc.)

More than 400 destinations in 40

countries

Fleet of 120 aircraft in 2006

Publicly listed

5.

BACKGROUND INFORMATION ON THE MARKETActual Competition: Market Shares of

Passengers from and to Dublin

Combined market shares of

Ryanair and Aer Lingus

increased from 80% in 2007 to

87% in 2012

6.

BACKGROUND INFORMATION ON THE MARKETIrish airports are hard to penetrate for

new competitors

The Irish market is a small peripheral

market with limited growth

Aer Lingus and Ryanair have a strong

base

newcomers would face substantial sunk

costs for marketing, promotion, brand

recognition

EasyJet has tried and failed

Several companies (e.g. BA) have left

Dublin

7.

BRIEF OVERVIEW OF THE RELEVANT THEORYBecause the main arguments of Ryanair was about

efficiency by reducing cost and competition

(especially increasing it by possibility of entry) we will

consider models on this themes.

8.

BRIEF OVERVIEW OF THE RELEVANT THEORYEntry deterrence

Model of entry deterrence from Fudenberg and Tirole (1984):

The model is developed into three stages:

1)incumbent decides about its strategic investments (in our case

capacities and frequencies of flies, commitment for price) to

prevent enter.

2)potential rival firm makes its choice whether entering the market

or not

3)if the rival has entered, firms compete in quantities.

The game is solved by backward induction.

Note that Ryanair is the largest (and most profitable) European "lowfrills" carrier with a clear price-aggressive airline profile and it invest a

lot to prevent entry new firms.

9.

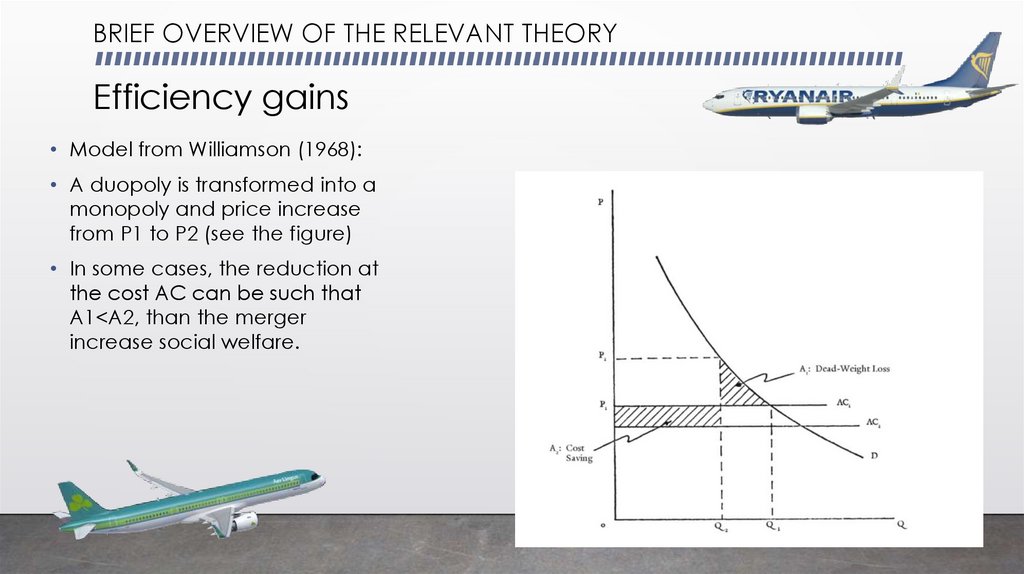

BRIEF OVERVIEW OF THE RELEVANT THEORYEfficiency gains

• Model from Williamson (1968):

• A duopoly is transformed into a

monopoly and price increase

from P1 to P2 (see the figure)

• In some cases, the reduction at

the cost AC can be such that

A1<A2, than the merger

increase social welfare.

10. Competition and efficiency

BRIEF OVERVIEW OF THE RELEVANT THEORYCompetition and efficiency

Model from Dusoet al. (2007):

Main idea – we can measure gain in efficiency from merger (that is cost reduction) by competitors’ stock

price reaction at the date of the merger announcement.

This can be easily find from figure:

CS-consumer surplus, П is profit: m for merge,

c for competitors, e is cost reduction.

Giulia Sargenti at “Ryanair and Aer Lingus

Merger Cases” measured that price reaction in first

days is insignificant, that means that efficiency

gain is insignificant small. (The cost reduction was one of the main argument of Ryanair)

11.

THE FIRST MERGER ATTEMPT AND TRIAL PROCESSRyanair arguments and commitments

• The effectivity would rise:

Operational cost savings due to the Economy of scale effect

Better management of Ryanair

The application of Ryanair’s successful low-cost structure to Aer Lingus

• Consumer would benefit:

The transition of raised effectivity to lower tariffs

Low-coster structure of the new firm implies lower prices

• Possible commitments of the new firm:

Aer Lingus’ operations on 43 overlapping routes get transferred to Flybe

Some landing slots are delegated to IAG/British Airways on routes from

London to Dublin, Shannon and Cork

Flybe and IAG/British Airways commit to operate the routes for three years

12.

THE FIRST MERGER ATTEMPT AND TRIAL PROCESSAer Lingus objections

• On the Ryanair’s post-merger cost reductions evaluation:

Some efficiency improvement measures can be done with current

management and are planned already

The proposed measures can only be achieved through an adaptation of

Ryanair’s low-coster business model

• On the consequences for consumers:

The formed firm would lack incentives to pass the efficiencies onto

consumers due to increased market power on many routes

Time- and quality- preferring travelers on many routes would be forced to

use Ryanair low-quality service in the absence of other options

13.

THE FIRST MERGER ATTEMPT AND TRIAL PROCESSEuropean Commission disapproval

• Evaluations validity concerns:

Cost reduction evaluations don’t measure any post-merger market effects

Higher effectivity of Ryanair evidence omits quality of service measurement

• Synergetic effect concerns:

Aer Lingus argues that it’s cost-efficient with their current business model and is planning further

effectivity-improvement measures

The low-cost model of Ryanair is specific and cannot be easily imposed on another airline company

• Consumers benefits concerns:

Absence of high-quality service on the routes under the merged firm monopoly

Lower competition and merged firm monopoly on 35 routes means higher prices

• Commitments concerns:

The proposed measures are not sufficient to neglect the anti-competitive effect

Uncertainty about the continuation of commitments after the 3-year period

The measures could take much time and effort to be executed

14.

APPEALS OF BOTH PARTIESBoth companies appeal against Commission decisions in General Court

Aer Lingus appeal the renouncement of

Commission from ordering the Ryanair to divest

its part of Aer Lingus’s shares

Arguments:

Court’s answer:

The Article 8(4) of the Ryanair is nonMerger regulation

controlling minority

The negative effect of

shareholder

the decision on

Ryanair hasn’t control

competition

share

Ryanair’s

Ryanair can’t seriously

shareholding (even

influence on a

minority) could lead

company with a

to a control over Art

current part of shares

Lingus

Ryanair appeal the prohibition of the merger

Arguments:

Court’s answer:

The Commission pay

The Commission made

attention only to

careful analysis

market shares

The weights of gathered

“Selectively” used

information could be

information from

weighted by

investigation

Commission

The qualitive and

Partly persuasive

quantitative analysis

evidence always could

sometimes indicated

be accessory arguments

in different directions The remedies had

Rejecting of remedies

unclear formulations

(because they were

made late)

15.

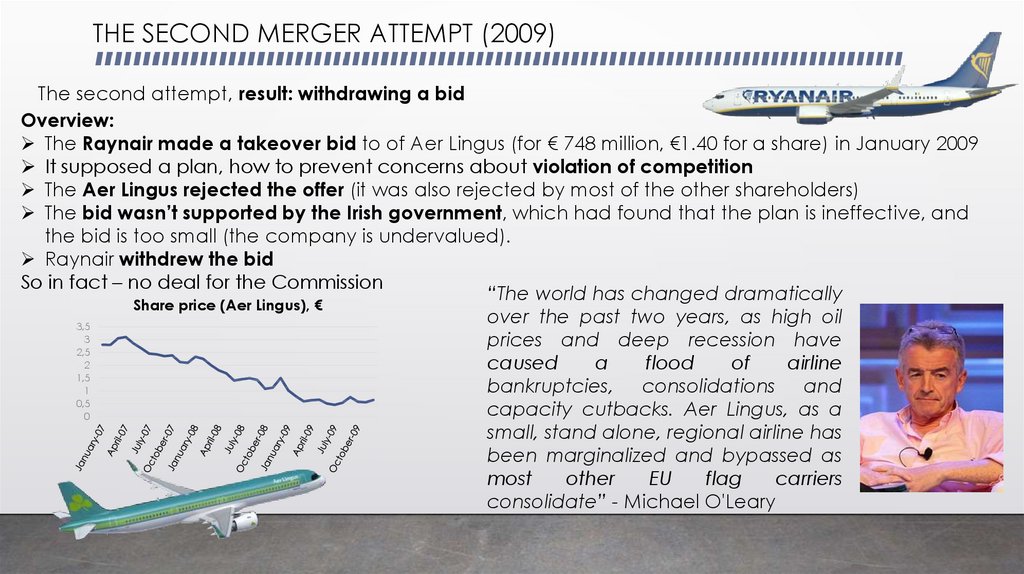

THE SECOND MERGER ATTEMPT (2009)The second attempt, result: withdrawing a bid

Overview:

The Raynair made a takeover bid to of Aer Lingus (for € 748 million, €1.40 for a share) in January 2009

It supposed a plan, how to prevent concerns about violation of competition

The Aer Lingus rejected the offer (it was also rejected by most of the other shareholders)

The bid wasn’t supported by the Irish government, which had found that the plan is ineffective, and

the bid is too small (the company is undervalued).

Raynair withdrew the bid

So in fact – no deal for the Commission

“The world has changed dramatically

Share price (Aer Lingus), €

over the past two years, as high oil

3,5

3

prices and deep recession have

2,5

2

caused

a

flood

of

airline

1,5

bankruptcies, consolidations and

1

0,5

capacity cutbacks. Aer Lingus, as a

0

small, stand alone, regional airline has

been marginalized and bypassed as

most

other

EU

flag

carriers

consolidate” - Michael O'Leary

16.

THE THIRD MERGER ATTEMPT (2012-2013)The third attempt of the takeover, result: prohibition

1) Overview:

At 19.06.2012 the Raynair made another bid to

takeover the Aer Lingus (for € 748 million, at

€1.30 per share)

2) Argument of the Commission:

The Aer Lingus rejected the offer again

The arguments of the Commission qualitatively were

Raynair notified the European Commission

the same from the case one, but after a new

about the takeover

investigation quantitively become even stronger:

The commission prohibited the takeover. Why?

Increased of the combined market shares of

Raynair and Aer Lingues (from 80% in 2007 to 87%

3) Remedies proposed by Ryanair:

in 2012) for short-haul flights from Dublin

Transferring of Aer Lingus’ operations on overlap

Increased number of overlap routes with high

routes to Flybe

market’s share of the possible merged company

The cession of the slots at London airports for IAG

(from 35 in 2007 to 46 in 2012)

However, Commission’s investigation

High barriers of entering on the relevant market

had demonstrated, that these remedies

would be inefficient

4) Conclusion:

The takeover will harm consumers and decrease

competition, the fares will increase

17.

THE EVOLUTION OF THE MARKET AFTER DECISION18.

THANKS FOR YOUR ATTENTION!ANY QUESTIONS?

19.

REFFERENCES• “Yes, we can (prohibit) – The Ryanair/Aer Lingus merger before the Court” - Oliver Koch1 (Forthcoming

in Competition Policy Newsletter 2010-3)

• Press Releases of the three cases from European Commission:

http://ec.europa.eu/competition/elojade/isef/index.cfm?fuseaction=dsp_result&policy_area_id=2&ca

se_title=%20AER%20LINGUS

• https://dial.uclouvain.be/memoire/ucl/en/object/thesis%3A11481/datastream/PDF_01/view

• Timeline of cases: https://www.telegraph.co.uk/finance/newsbysector/transport/11408325/TimelineRyanair-vs-Aer-Lingus-the-decade-long-battle-of-the-Irish-airlines.html

• The history of Aer Lingus: https://en.wikipedia.org/wiki/Aer_Lingus