management

managementSimilar presentations:

")

")

")

")

Performance management. Target costing. (Topic 1)

1. Performance management

Topic 1Target costing

Reference: Chapter 2b

2.

ACCA exam referencesTopic list

Syllabus

reference

1. What is target costing

A2 (a)

2. Implementing target costing

A2 (a)

3. Deriving a target cost

A2 (a)

4. Closing a target cost gap

A2 (c)

5. Target costing in services industries

A2 (b)

Exam guide

Target costing may be examined in Section A multiple choice questions or it may form a

part of a Section B mini case study question where a calculation of a target cost may be

required, followed by a multiple choice question on the theory of target costing.

3.

1. What is target costing?Target costing involves setting a target cost for a product, having identified a target selling

price and a required profit margin. The target cost equals the target selling price minus the

required profit.

Target cost = Selling price – Required profit

or

Target cost = Selling price × (1 – required profit margin)

Selling price – determined mainly by outside factors and cannot be manipulated in

competitive environment.

Required profit margin – is that minimal level of return required by the owners of a

business.

Target costing focuses on getting the expected cost of a product down to a target cost

amount.

Estimated cost

of a product

Should be reduced to

Target cost for

a product

4.

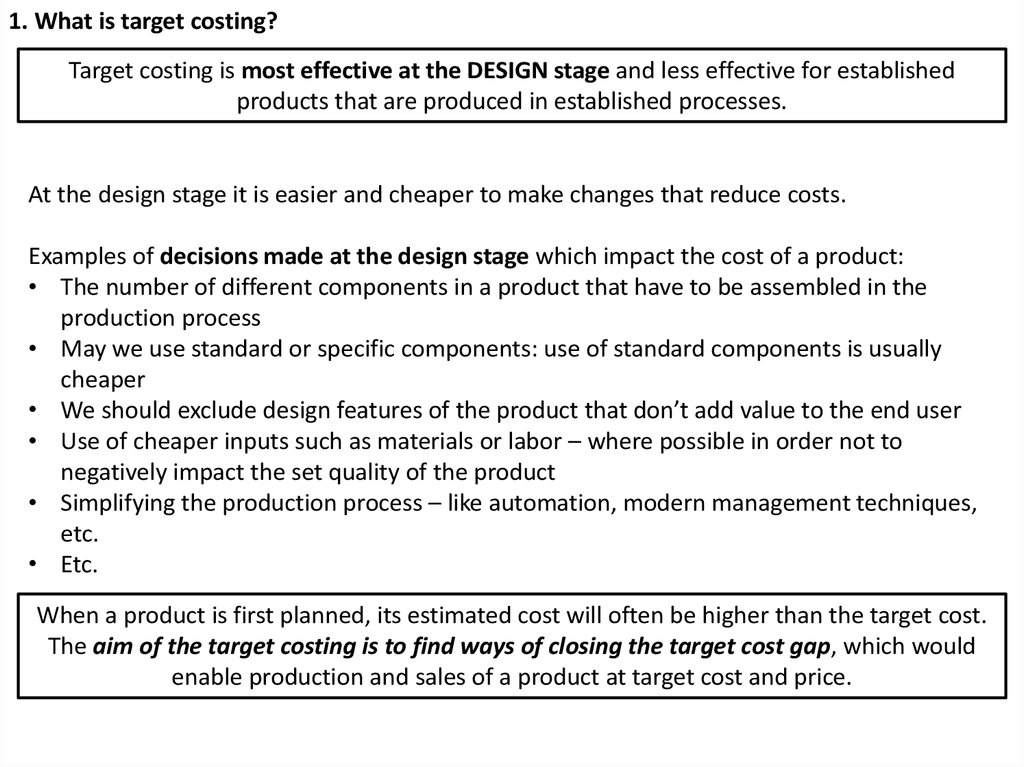

1. What is target costing?Target costing is most effective at the DESIGN stage and less effective for established

products that are produced in established processes.

At the design stage it is easier and cheaper to make changes that reduce costs.

Examples of decisions made at the design stage which impact the cost of a product:

• The number of different components in a product that have to be assembled in the

production process

• May we use standard or specific components: use of standard components is usually

cheaper

• We should exclude design features of the product that don’t add value to the end user

• Use of cheaper inputs such as materials or labor – where possible in order not to

negatively impact the set quality of the product

• Simplifying the production process – like automation, modern management techniques,

etc.

• Etc.

When a product is first planned, its estimated cost will often be higher than the target cost.

The aim of the target costing is to find ways of closing the target cost gap, which would

enable production and sales of a product at target cost and price.

5.

2. Implementing target costingStep 1

• Determine a product specification of which an adequate volume of sales is expected

• Infer a target selling price at which the company will be able to sell the product successfully

Step 2 and achieve a desired market share

• Identify the required profit from the product, may be based on required profit margin or

Step 3 return on investment

Step 4

• Calculate: Target cost = Target selling price – Target profit

• Determine an estimated cost of the product, based on the initial design specification and

Step 5 current cost levels

Step 6

• Calculate Target cost gap = Estimated cost – Target cost

• Make efforts to close the gap. More likely to be successful if efforts are made to “design out”

Step 7 costs prior to production, rather than to “control out” costs after “live” production has started

Usually target cost is based on target selling price per unit, however it may

also be based on the expected volume of sales

6.

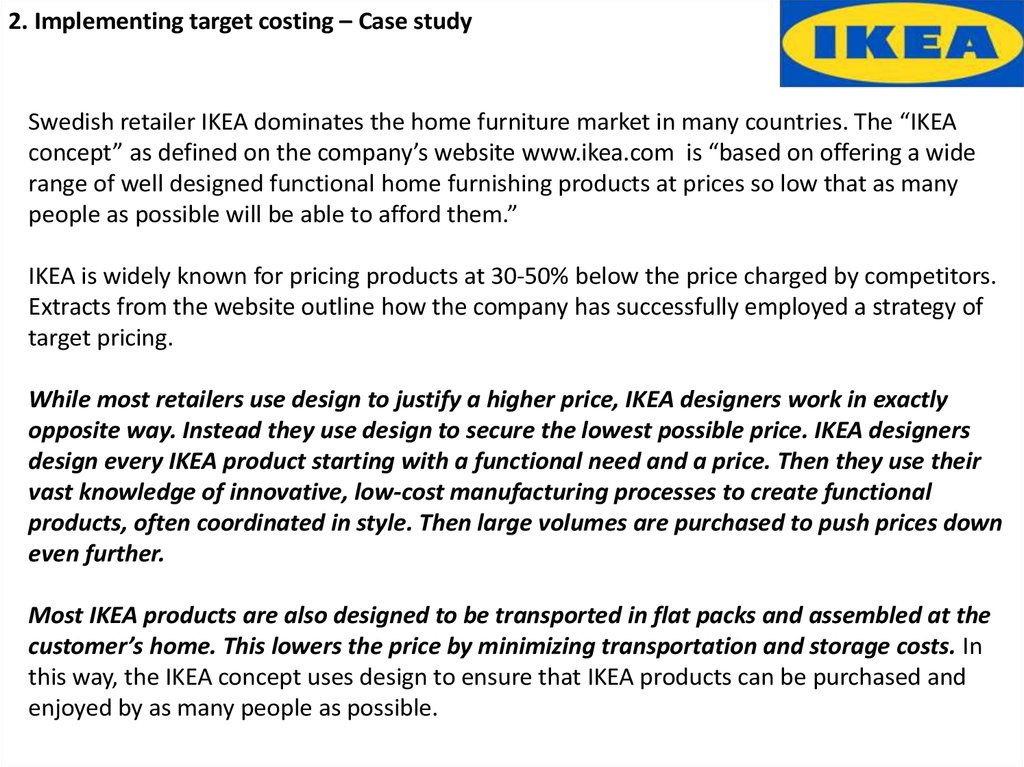

2. Implementing target costing – Case studySwedish retailer IKEA dominates the home furniture market in many countries. The “IKEA

concept” as defined on the company’s website www.ikea.com is “based on offering a wide

range of well designed functional home furnishing products at prices so low that as many

people as possible will be able to afford them.”

IKEA is widely known for pricing products at 30-50% below the price charged by competitors.

Extracts from the website outline how the company has successfully employed a strategy of

target pricing.

While most retailers use design to justify a higher price, IKEA designers work in exactly

opposite way. Instead they use design to secure the lowest possible price. IKEA designers

design every IKEA product starting with a functional need and a price. Then they use their

vast knowledge of innovative, low-cost manufacturing processes to create functional

products, often coordinated in style. Then large volumes are purchased to push prices down

even further.

Most IKEA products are also designed to be transported in flat packs and assembled at the

customer’s home. This lowers the price by minimizing transportation and storage costs. In

this way, the IKEA concept uses design to ensure that IKEA products can be purchased and

enjoyed by as many people as possible.

7.

3. Deriving a target costExample 1:

A car manufacturer wants to calculate a target cost for a new car, the price of which will

be set at $17’950. The company requires an 8% profit margin on sales.

Required:

What is target cost?

Solution:

Profit required = 8% × $17’950 = $1’436

Target cost = $(17’950 – 1’436) = $16’514 or = $17’950 × (1-0.08) = 16’514

8.

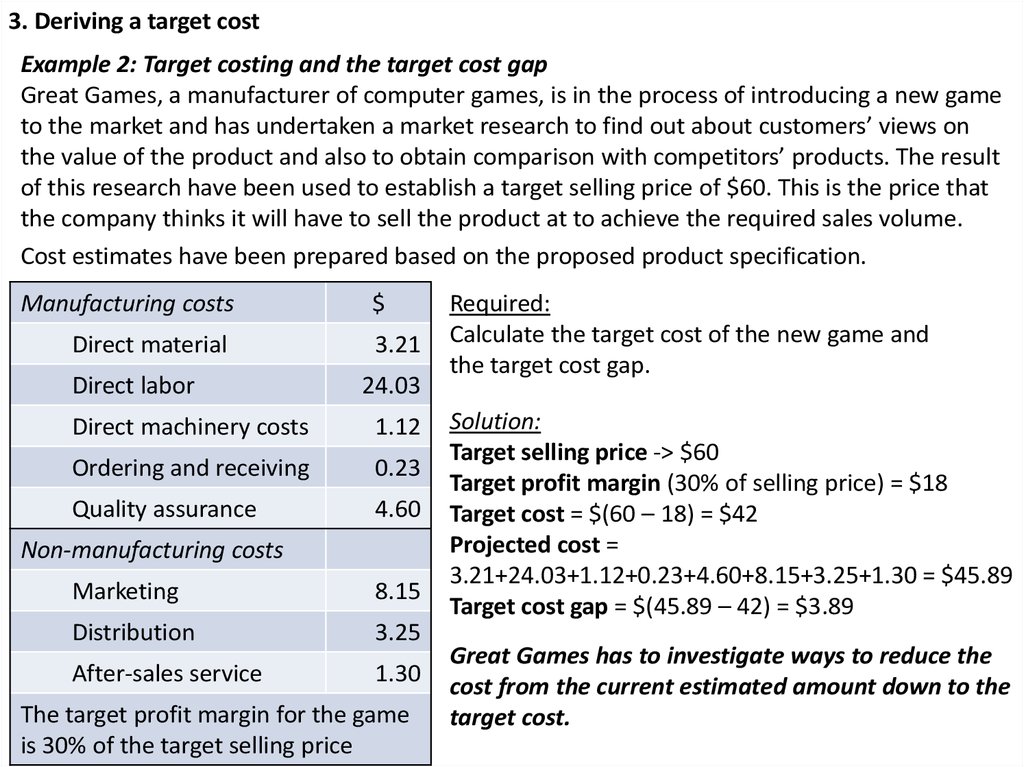

3. Deriving a target costExample 2: Target costing and the target cost gap

Great Games, a manufacturer of computer games, is in the process of introducing a new game

to the market and has undertaken a market research to find out about customers’ views on

the value of the product and also to obtain comparison with competitors’ products. The result

of this research have been used to establish a target selling price of $60. This is the price that

the company thinks it will have to sell the product at to achieve the required sales volume.

Cost estimates have been prepared based on the proposed product specification.

Manufacturing costs

Direct material

Direct labor

$

3.21

24.03

Direct machinery costs

1.12

Ordering and receiving

0.23

Quality assurance

4.60

Non-manufacturing costs

Marketing

8.15

Distribution

3.25

After-sales service

1.30

The target profit margin for the game

is 30% of the target selling price

Required:

Calculate the target cost of the new game and

the target cost gap.

Solution:

Target selling price -> $60

Target profit margin (30% of selling price) = $18

Target cost = $(60 – 18) = $42

Projected cost =

3.21+24.03+1.12+0.23+4.60+8.15+3.25+1.30 = $45.89

Target cost gap = $(45.89 – 42) = $3.89

Great Games has to investigate ways to reduce the

cost from the current estimated amount down to the

target cost.

9.

4. Closing a target cost gap• Increasing the price will not close the cost gap.

• What to do?

• Split the target cost into broad cost categories

• such as development, marketing, manufacturing

• Manufacturing target cost per unit is split up across the different

functional areas of the product.

• Product is designed so that each functional product area can be made within

the target cost.

• If the target cost gap cannot be fully eliminated in a particular product

area:

a. Target for other areas are reduced

b. Product is redesigned

c. Product is rejected

• Product should be developed in an atmosphere of continuous improvement

using value engineering techniques and close collaboration with suppliers to

a. enhance the product (in terms of service, quality, durability, etc.) and

b. reduce costs.

10.

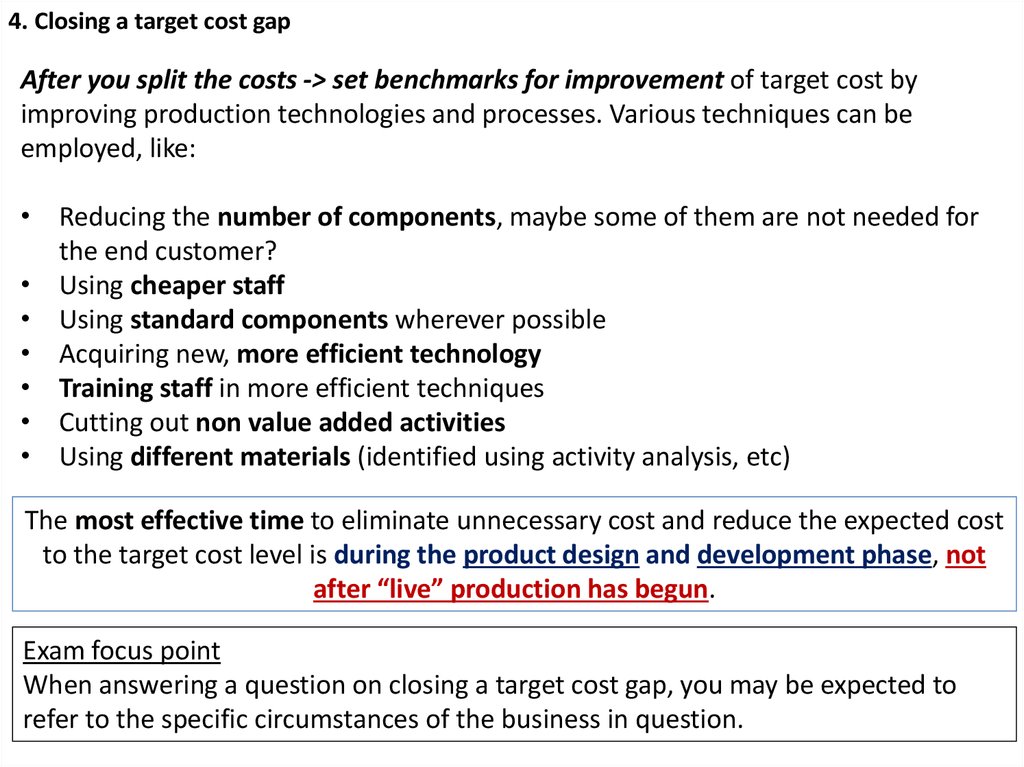

4. Closing a target cost gapAfter you split the costs -> set benchmarks for improvement of target cost by

improving production technologies and processes. Various techniques can be

employed, like:

• Reducing the number of components, maybe some of them are not needed for

the end customer?

• Using cheaper staff

• Using standard components wherever possible

• Acquiring new, more efficient technology

• Training staff in more efficient techniques

• Cutting out non value added activities

• Using different materials (identified using activity analysis, etc)

The most effective time to eliminate unnecessary cost and reduce the expected cost

to the target cost level is during the product design and development phase, not

after “live” production has begun.

Exam focus point

When answering a question on closing a target cost gap, you may be expected to

refer to the specific circumstances of the business in question.

11.

5. Target costing in service industriesExamples of service businesses:

a. Mass service eg banking, transportation (rail, air), mass entertainment

b. Either/or eg fast food, teaching, hotels and holidays, psychoterapy

c. Personal service eg financial advisory, car maintenance, audit

Five major characteristics of services that distinguish services from products:

• Intangibility (of what is provided to and valued by individual customers)

• Inseparability/Simultaneity (production and consumption of the service coincide)

• Perishability (the inability to store the service)

• Heterogeneity (variability in the standard of performance of the provision of the service)

• No transfer of ownership

12.

5. Target costing in service industriesRemind that: a target cost for a product is a cost for an item whose design and make-up is

specified in exact detail in a product specification. A target cost is a cost for this detailed

specification.

Services are much more difficult to specify exactly due to the following characteristics:

1. Intangibility.

• and target price

• what exactly does a customer receive – and thus ->

• what exactly every particular customer is paying for? ->

• What should be the benchmark target price for this service?

• and cost of materials

• the major cost in the service industry is salaries. Bought-in materials are usually

low when compared to salaries. It is very difficult to reduce the cost of salaries.

2. Variability/homogeneity

• A service can differ every time it is provided, and standard service may not exist.

• Ex: repairing a motor car, providing an audit, pulling out a tooth are never

exactly the same each time.

• When services are variable, it is possible to calculate an estimated average cost,

but this is not specific and so not ideal for target costing.