law

lawSimilar presentations:

")

")

Immunities and privileges of diplomatic agents. Part 2

1.

IMMUNITIES ANDPRIVILEGES OF

DIPLOMATIC AGENTS

Part 2

24 October 2018

2.

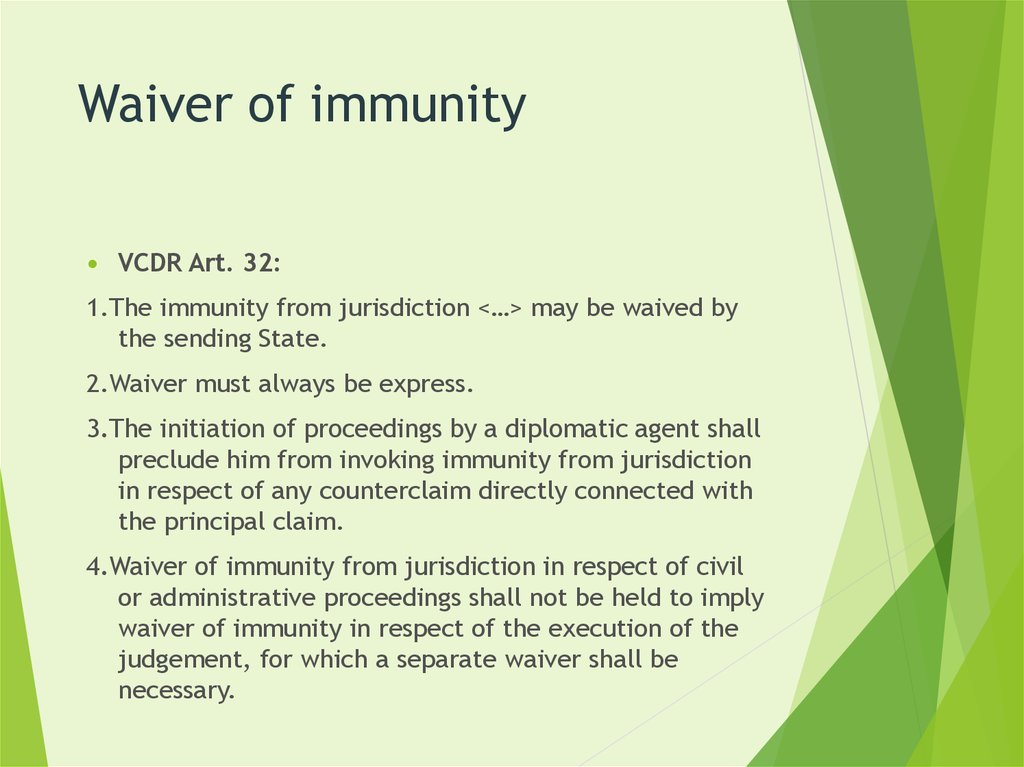

Waiver of immunityVCDR Art. 32:

1.The immunity from jurisdiction <…> may be waived by

the sending State.

2.Waiver must always be express.

3.The initiation of proceedings by a diplomatic agent shall

preclude him from invoking immunity from jurisdiction

in respect of any counterclaim directly connected with

the principal claim.

4.Waiver of immunity from jurisdiction in respect of civil

or administrative proceedings shall not be held to imply

waiver of immunity in respect of the execution of the

judgement, for which a separate waiver shall be

necessary.

3.

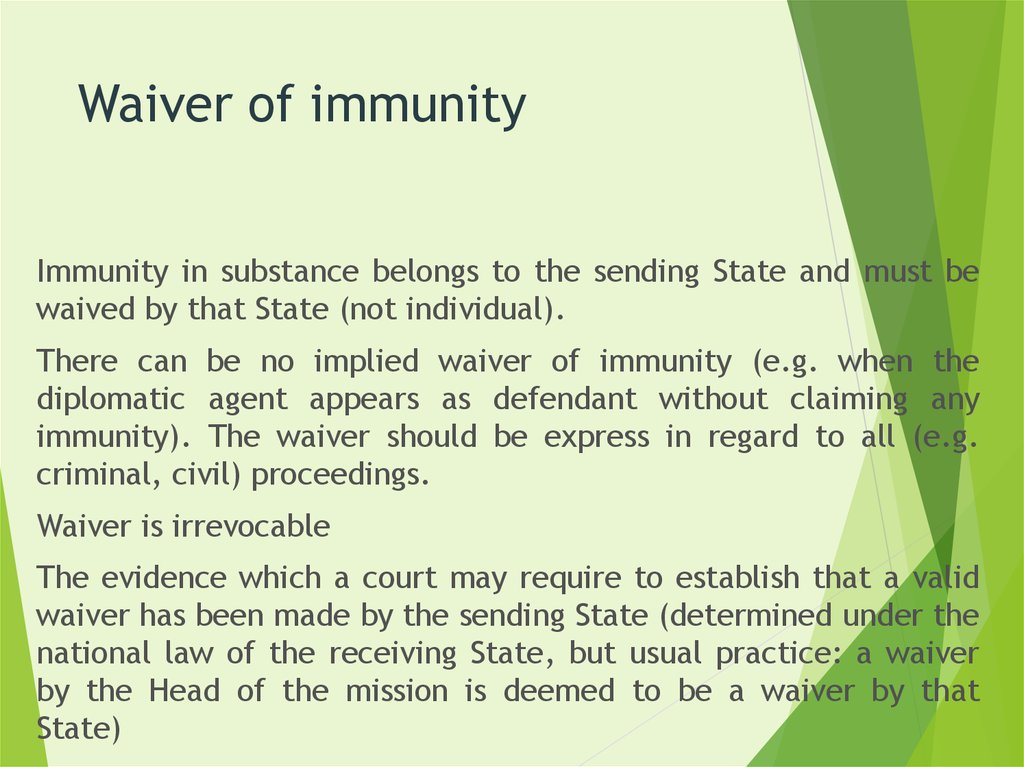

Waiver of immunityImmunity in substance belongs to the sending State and must be

waived by that State (not individual).

There can be no implied waiver of immunity (e.g. when the

diplomatic agent appears as defendant without claiming any

immunity). The waiver should be express in regard to all (e.g.

criminal, civil) proceedings.

Waiver is irrevocable

The evidence which a court may require to establish that a valid

waiver has been made by the sending State (determined under the

national law of the receiving State, but usual practice: a waiver

by the Head of the mission is deemed to be a waiver by that

State)

4.

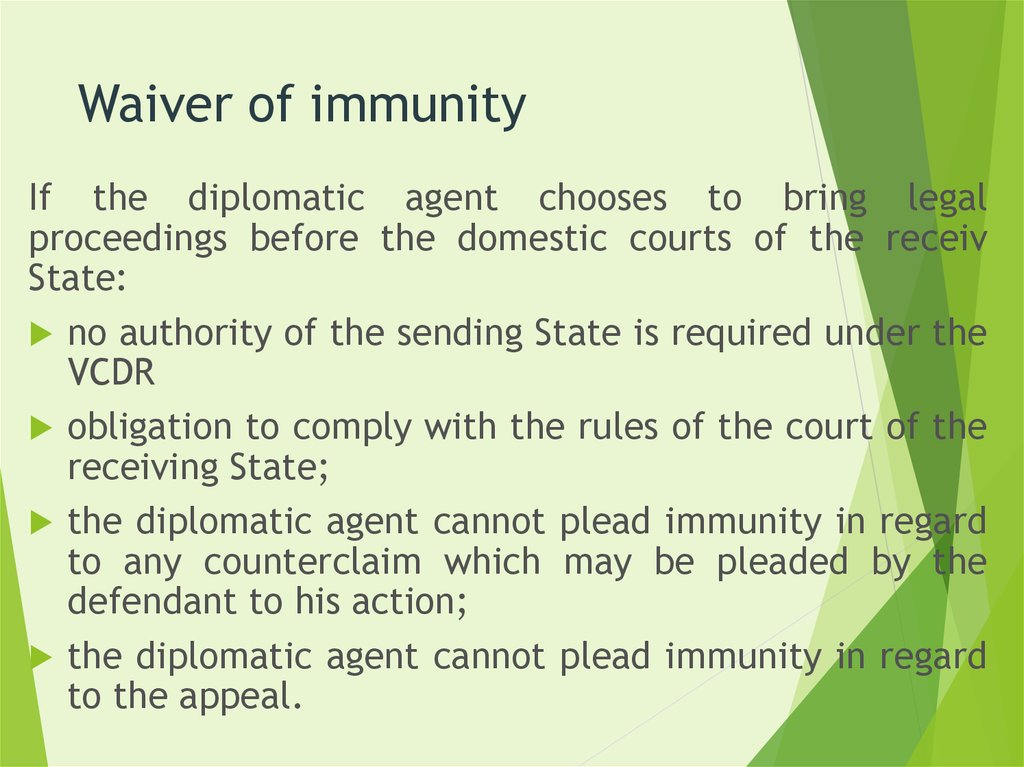

Waiver of immunityIf the diplomatic agent chooses to bring legal

proceedings before the domestic courts of the receiv

State:

no authority of the sending State is required under the

VCDR

obligation to comply with the rules of the court of the

receiving State;

the diplomatic agent cannot plead immunity in regard

to any counterclaim which may be pleaded by the

defendant to his action;

the diplomatic agent cannot plead immunity in regard

to the appeal.

5.

Waiver of immunitythe execution of a judgment requires a separate waiver

by the sending State (Art 32.4 of the VCDR). The

implication of the text is that in respect of criminal

proceedings no separate waiver in respect of execution

of any penalty is necessary, thus waiver of immunity in a

criminal case cannot be confined to the proceedings to

determine guilt

6.

If a person wants to sue adiplomat...

3 options:

1. try to institute proceedings before the

courts of the diplomat's home State;

2. lay the matter before the ambassador of

the sending State hoping to have his

assistance in obtaining a settlement;

3. lay the matter before his own

government, usually before the ministry

of foreign affairs, and ask them to

intervene.

7.

Commencement andtermination of immunities

VCDR Article 39

1.Every person entitled to privileges and immunities shall enjoy them

from the moment he enters the territory of the receiving State on

proceeding to take up his post or, if already in its territory, from the

moment when his appointment is notified to the Ministry for

Foreign Affairs or such other ministry as may be agreed.

2.When the functions of a person enjoying privileges and immunities

have come to an end, such privileges and immunities shall normally

cease at the moment when he leaves the country, or on expiry of

a reasonable period in which to do so, but shall subsist until that

time, even in case of armed conflict. However, with respect to acts

performed by such a person in the exercise of his functions as a

member of the mission, immunity shall continue to subsist.

<...>

8.

4. Commencement andtermination of immunities

(cont’d)

Termination: immunities subsist until:

1. the diplomatic agent leaves the country on

termination of his mission, or for a reasonable

period to enable him to do so.

What constitutes a “reasonable period”? Some states

define under domestic law, some prefer a flexible

approach; usually 1-30 days for the persona non

grata or 1-6 months to normal cases

2. the receiving State may extend a longer 'reasonable

period' to members of the family of the diplomat

expelled on short notice or in the case of death of the

diplomat.

3. No termination of immunity for official acts.

9.

2. Privileges of a diplomatic agentPrivileges granted for the diplomatic agents:

exemption from taxation,

exemption from customs duties and baggage inspection,

exemption from social security obligations,

exemption from personal and public services,

special treatment under the laws of the receiving State

regarding the acquisition of nationality

the right to freedom of movement

special privileges under the law of the receiving State in the

absence of international obligation

10.

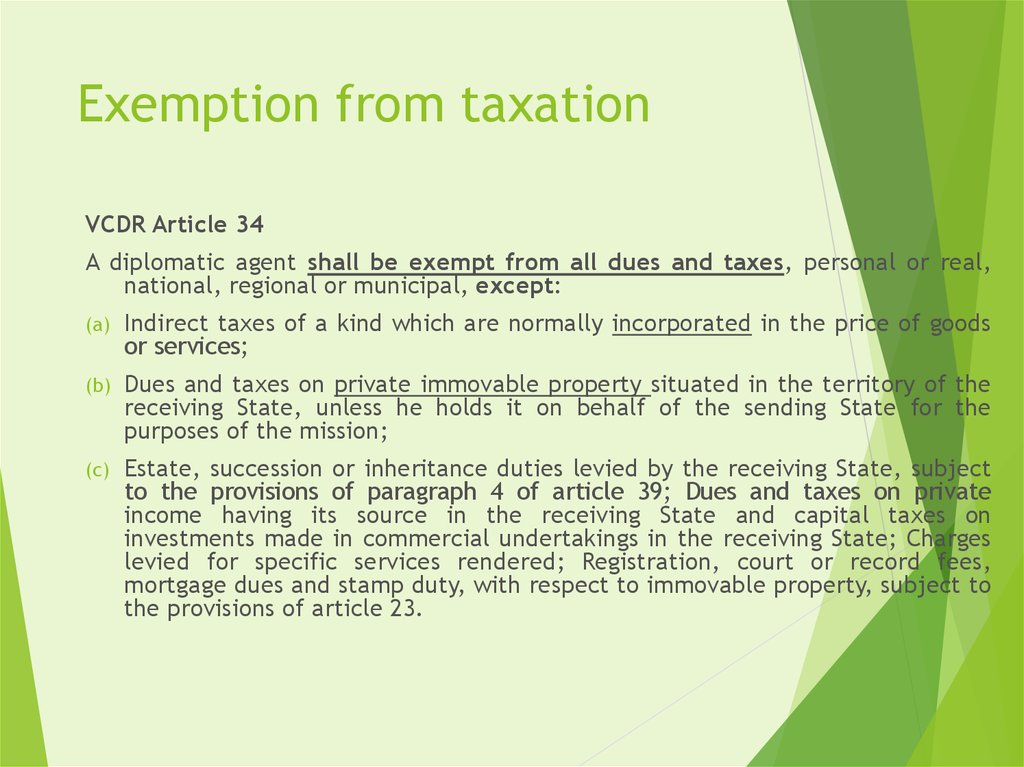

Exemption from taxationVCDR Article 34

A diplomatic agent shall be exempt from all dues and taxes, personal or real,

national, regional or municipal, except:

(a)

Indirect taxes of a kind which are normally incorporated in the price of goods

or services;

(b)

Dues and taxes on private immovable property situated in the territory of the

receiving State, unless he holds it on behalf of the sending State for the

purposes of the mission;

(c)

Estate, succession or inheritance duties levied by the receiving State, subject

to the provisions of paragraph 4 of article 39; Dues and taxes on private

income having its source in the receiving State and capital taxes on

investments made in commercial undertakings in the receiving State; Charges

levied for specific services rendered; Registration, court or record fees,

mortgage dues and stamp duty, with respect to immovable property, subject to

the provisions of article 23.

11.

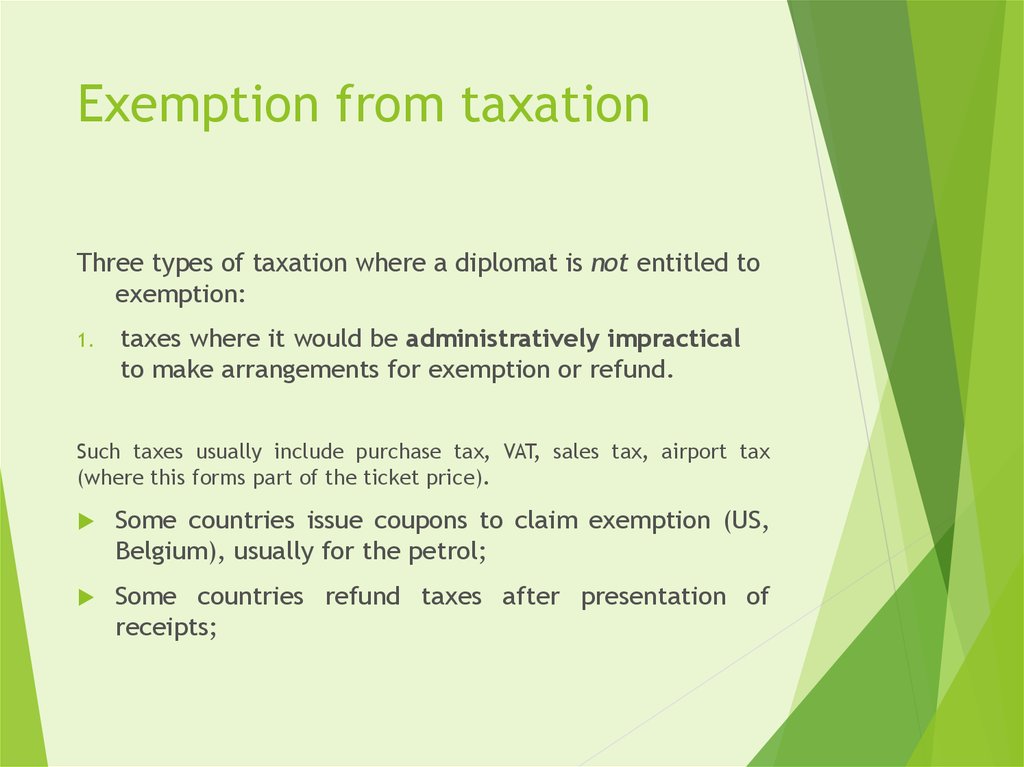

Exemption from taxationThree types of taxation where a diplomat is not entitled to

exemption:

1.

taxes where it would be administratively impractical

to make arrangements for exemption or refund.

Such taxes usually include purchase tax, VAT, sales tax, airport tax

(where this forms part of the ticket price).

Some countries issue coupons to claim exemption (US,

Belgium), usually for the petrol;

Some countries refund taxes after presentation of

receipts;

12.

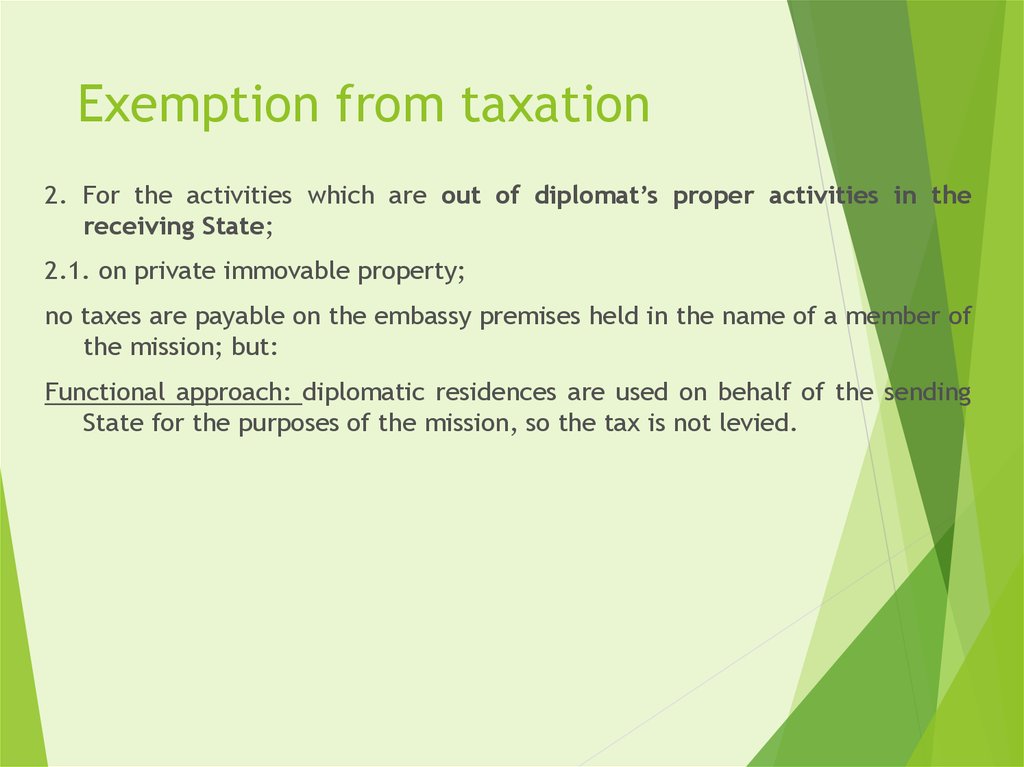

Exemption from taxation2. For the activities which are out of diplomat’s proper activities in the

receiving State;

2.1. on private immovable property;

no taxes are payable on the embassy premises held in the name of a member of

the mission; but:

Functional approach: diplomatic residences are used on behalf of the sending

State for the purposes of the mission, so the tax is not levied.

13.

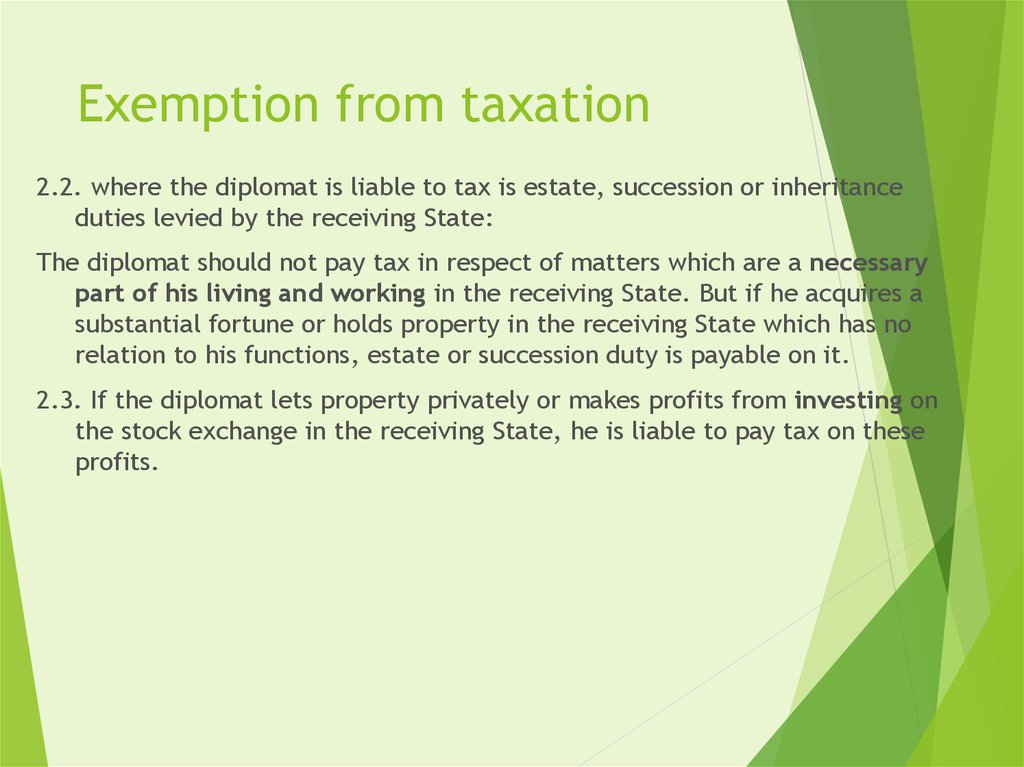

Exemption from taxation2.2. where the diplomat is liable to tax is estate, succession or inheritance

duties levied by the receiving State:

The diplomat should not pay tax in respect of matters which are a necessary

part of his living and working in the receiving State. But if he acquires a

substantial fortune or holds property in the receiving State which has no

relation to his functions, estate or succession duty is payable on it.

2.3. If the diplomat lets property privately or makes profits from investing on

the stock exchange in the receiving State, he is liable to pay tax on these

profits.

14.

Exemption from taxation3. charges for services (analogy with mission’s duty to pay taxes on specific

services):

3.1. The diplomat is obliged to pay road or bridge tolls and other similar

taxes related with his residence.

3.2. registration, court or record fees, mortgage dues and stamp duty, with

respect to immovable property - imposed to cover the administrative cost

of providing the service of registration of immovable property

15.

Exemption from customs dutiesand baggage inspection

VCDR Article 36

1. The receiving State shall, in accordance with such laws and regulations as it may adopt,

permit entry of and grant exemption from all customs duties, taxes, and related charges

other than charges for storage, cartage and similar services, on:

(a) Articles for the official use of the mission;

(b) Articles for the personal use of a diplomatic agent or members of his family forming part

of his household, including articles intended for his establishment.

2. The personal baggage of a diplomatic agent shall be exempt from inspection, unless

there are serious grounds for presuming that it contains articles not covered by the

exemptions mentioned in paragraph 1 of this article, or articles the import or export of

which is prohibited by the law or controlled by the quarantine regulations of the receiving

State. Such inspection shall be conducted only in the presence of the diplomatic agent or

of his authorized representative.

16.

Exemption from customs dutiesand baggage inspection

the exemption is to be granted in accordance with the laws and

regulations of the receiving State;

If regulations are imposed in bad faith or so restrictive as essentially to

obstruct the exercise of the right to duty-free imports, they may be

challenged by sending states.

17.

Exemption from social securityobligations

VCDR Art. 33

1.Subject to the provisions of paragraph 3 of this article, a diplomatic

agent shall with respect to services rendered for the sending State

be exempt from social security provisions which may be in force in

the receiving State.

<...>

4.The exemption provided for in paragraphs 1 and 2 of this article shall

not preclude voluntary participation in the social security system of

the receiving State provided that such participation is permitted by

that State.

5.The provisions of this article shall not affect bilateral or multilateral

agreements concerning social security concluded previously and shall

not prevent the conclusion of such agreements in the future.

18.

Exemption from personal andpublic services

VCDR Art. 35:

The receiving State shall exempt diplomatic agents from all personal services, from all public

service of any kind whatsoever, and from military obligations such as those connected with military

contributions.

Exemption from compulsory services – civic duties:

jury service;

military service;

military obligations such as requisition and billeting,

duties to assist in public emergencies such as floods or forest fires..

19.

Duties of diplomatic agentsSee VCDR Art. 41:

1.Without prejudice to their privileges and immunities, it is the duty of all persons

enjoying such privileges and immunities to respect the laws and regulations of

the receiving State. They also have a duty not to interfere in the internal

affairs of that State.

2.All official business with the receiving State entrusted to the mission by the

sending State shall be conducted with or through the Ministry for Foreign Affairs

of the receiving State or such other ministry as may be agreed.<..>

1. duty to respect the laws and regulations of the receiving State: applicable to official as well as

the private activities of diplomats:

1.1. Obligation to observe local motor traffic regulations, insurance, keep technical standards for

the car maintenance..

1.2. Obligation not to perform consular functions if the permit of the receiving state is required;

etc.

20.

Duties of diplomatic agents2. duty not to interfere in the internal affairs of the receiving State:

2.1. avoid public statements or actions which would be construed as supporting

one candidate or party;

3. To inform the ministry of foreign affairs on all aspects of relations between

sending and receiving States.

4. Other duties (VCDR Art. 42 - commercial activities etc.)

21.

Reading materialsDENZA, E. Diplomatic Law: Commentary on the Vienna Convention

on Diplomatic Relations, Oxford: Oxford University Press, 4th

edition, 2016, p. 213-364; p. 386-388;

United States Diplomatic and Consular Staff in Tehran (United

States of America v. Iran), ICJ, judgment of 24 May 1980:

(judgment

full

text:

http://www.icjcij.org/docket/files/64/6291.pdf; summary of the judgment:

http://www.icj-cij.org/docket/files/64/6293.pdf

Armed Activities on the Territory of the Congo (Democratic

Republic of the Congo v. Uganda), ICJ, Judgment of 19 December

2005:

(judgment

full

text:

http://www.icjcij.org/docket/files/116/10455.pdf, summary of the judgment:

http://www.icj-cij.org/docket/files/116/10457.pdf

Certain Questions of Mutual Assistance in Criminal Matters

(Djibouti v. France), ICJ, judgment of 4 June 2008 (judgment

full text: http://www.icj-cij.org/docket/files/136/14550.pdf;

summary

of

the

judgment:

http://www.icjcij.org/docket/files/136/14572.pdf

22.

Reading materialsArrest Warrant of 11 April 2000 (Democratic Republic of the Congo v.

Belgium), ICJ, Judgment of 14 February 2002: (judgment full text:

http://www.icj-cij.org/docket/files/121/8126.pdf; summary of the

judgment: http://www.icj-cij.org/docket/files/121/13743.pdf)