finance

financeSimilar presentations:

")

Problems and Countermeasures in Financial Accounting of Publicly Financed Institutions

1. Problems and Countermeasures in Financial Accounting of Publicly Financed Institutions

Guo LongchaoMaster's Thesis Defense – Belarus State

Economic University, 2025

z

Problems and

Countermeasures in

Financial Accounting of

Publicly Financed

Institutions

2.

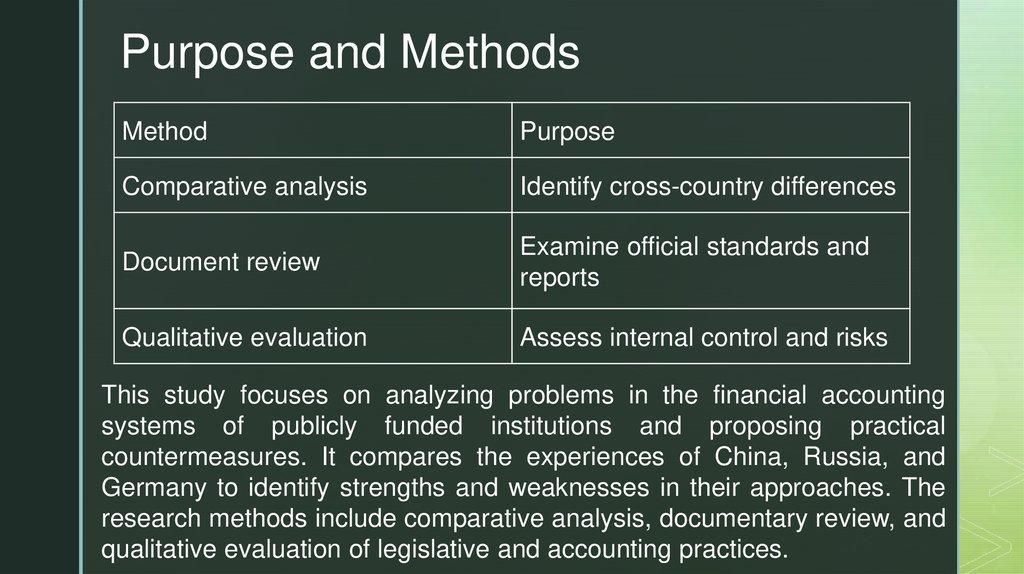

Purpose and MethodsMethod

Purpose

Comparative analysis

Identify cross-country differences

Document review

Examine official standards and

reports

Qualitative evaluation

Assess internal control and risks

This study focuses on analyzing problems in the financial accounting

systems of publicly funded institutions and proposing practical

countermeasures. It compares the experiences of China, Russia, and

Germany to identify strengths and weaknesses in their approaches. The

research methods include comparative analysis, documentary review, and

qualitative evaluation of legislative and accounting practices.

3.

The Role of Public Sector AccountingFinancial accounting in publicly funded institutions

ensures transparency, accountability, and effective

use of budgetary resources.

Unlike commercial entities, these institutions are

responsible not to shareholders, but to the public.

Their accounting must comply with strict legal and

regulatory frameworks to guarantee the proper use

of funds.

4.

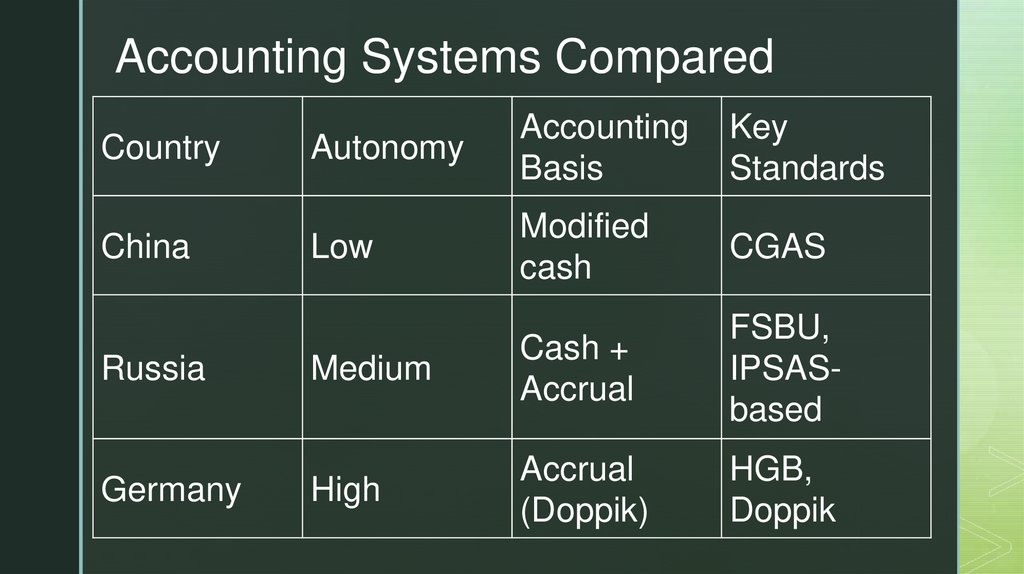

Accounting Systems ComparedCountry

China

Russia

Germany

Autonomy

Accounting

Basis

Key

Standards

Low

Modified

cash

CGAS

Medium

Cash +

Accrual

FSBU,

IPSASbased

High

Accrual

(Doppik)

HGB,

Doppik

5.

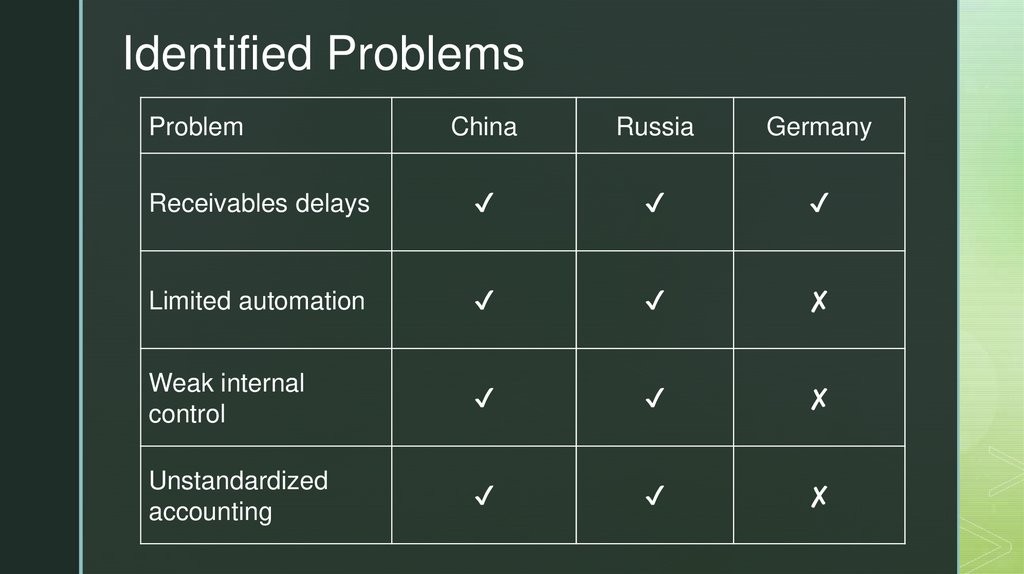

Identified ProblemsProblem

China

Russia

Germany

Receivables delays

✔

✔

✔

Limited automation

✔

✔

✘

Weak internal

control

✔

✔

✘

Unstandardized

accounting

✔

✔

✘

6.

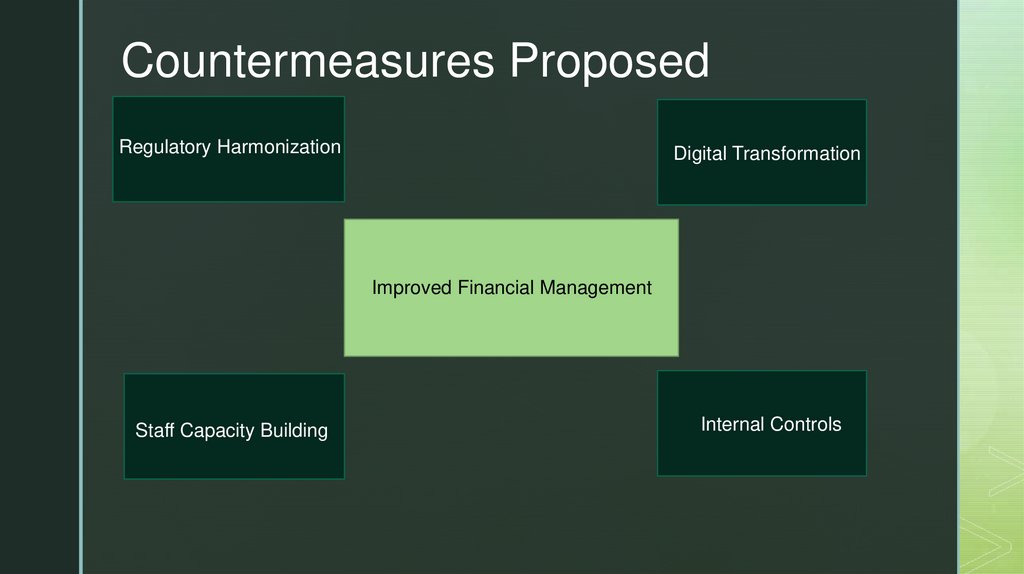

Countermeasures ProposedRegulatory Harmonization

Digital Transformation

Improved Financial Management

Staff Capacity Building

Internal Controls

7.

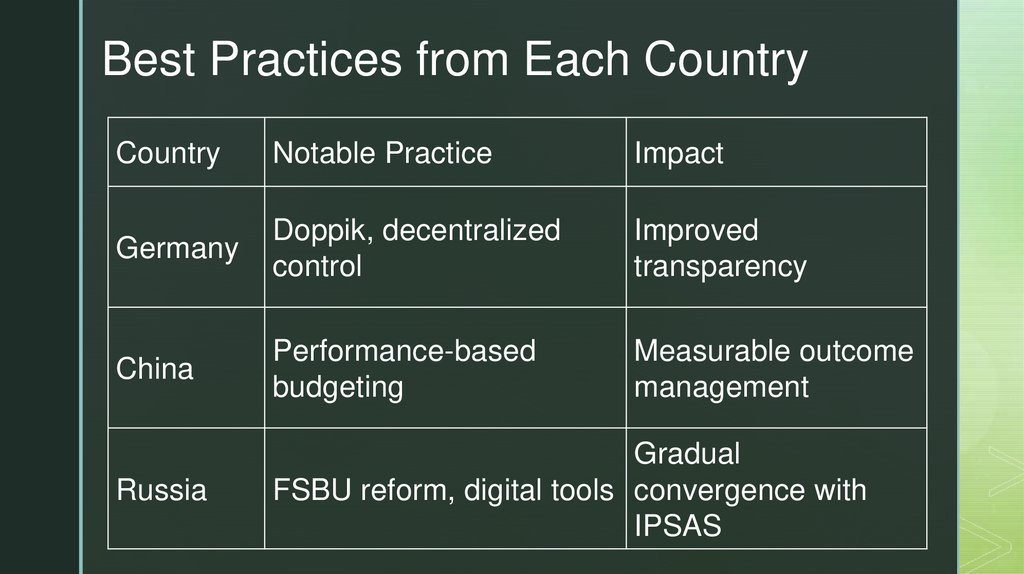

Best Practices from Each CountryCountry

Notable Practice

Impact

Germany

Doppik, decentralized

control

Improved

transparency

China

Performance-based

budgeting

Measurable outcome

management

Russia

Gradual

FSBU reform, digital tools convergence with

IPSAS