marketing

marketingSimilar presentations:

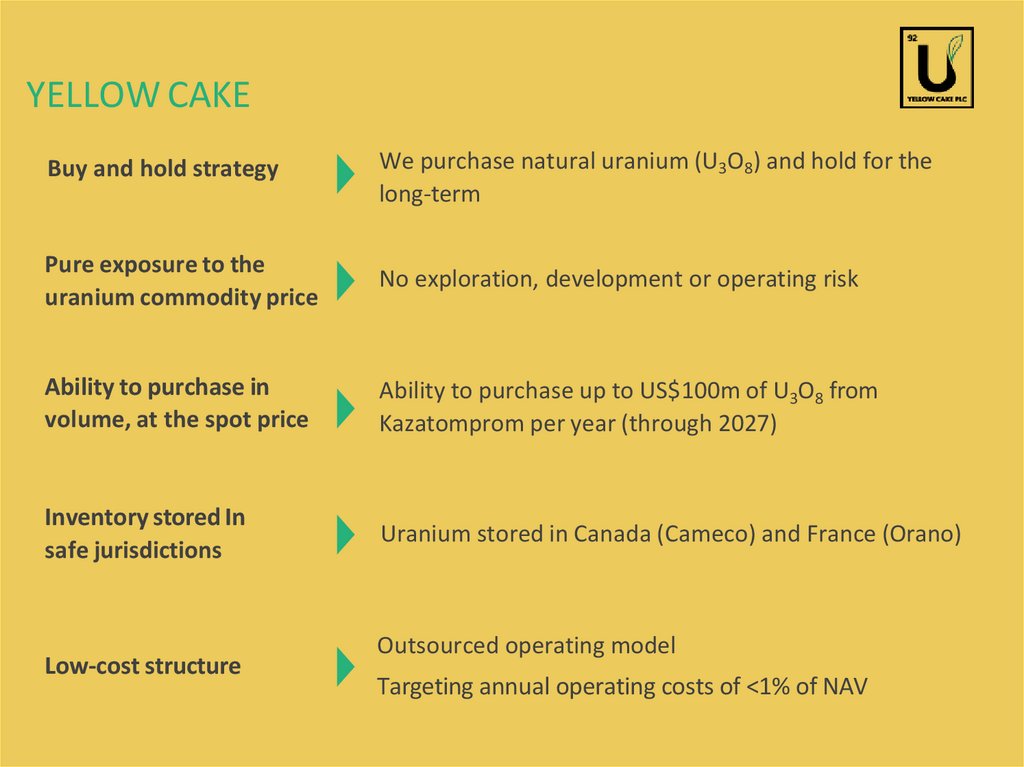

Yellow Cake Buy and hold strategy

1.

JuneZakhvatov Viktor

Peshkov Arthur

Dankina Irina

2.

YELLOW CAKEBuy and hold strategy

We purchase natural uranium (U3O8) and hold for the

long-term

Pure exposure to the

uranium commodity price

No exploration, development or operating risk

Ability to purchase in

volume, at the spot price

Ability to purchase up to US$100m of U3O8 from

Kazatomprom per year (through 2027)

Inventory stored In

safe jurisdictions

Uranium stored in Canada (Cameco) and France (Orano)

Low-cost structure

Outsourced operating model

Targeting annual operating costs of <1% of NAV

3.

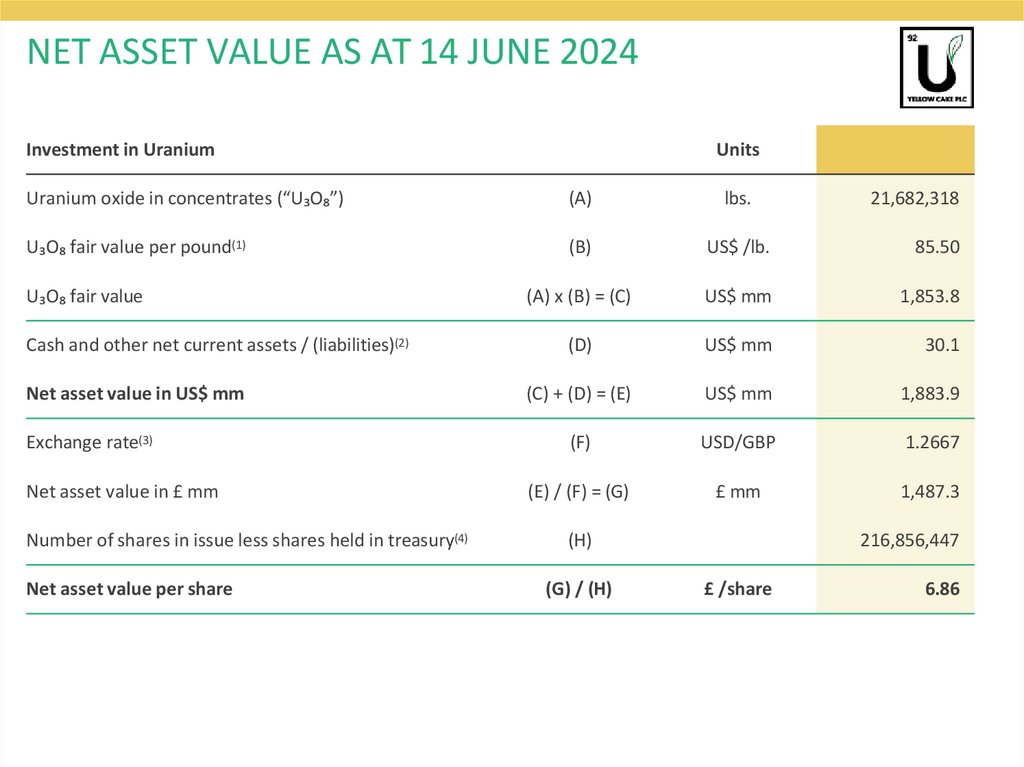

NET ASSET VALUE AS AT 14 JUNE 2024Investment in Uranium

Units

Uranium oxide in concentrates (“U₃O₈”)

(A)

lbs.

U₃O₈ fair value per pound(1)

(B)

US$ /lb.

85.50

(A) x (B) = (C)

US$ mm

1,853.8

(D)

US$ mm

30.1

(C) + (D) = (E)

US$ mm

1,883.9

(F)

USD/GBP

1.2667

(E) / (F) = (G)

£ mm

1,487.3

U₃O₈ fair value

Cash and other net current assets / (liabilities)(2)

Net asset value in US$ mm

Exchange rate(3)

Net asset value in £ mm

Number of shares in issue less shares held in treasury(4)

Net asset value per share

(H)

(G) / (H)

21,682,318

216,856,447

£ /share

6.86

4.

YELLOW CAKE CORPORATE SUMMARYCorporate overview

GBP share price and uranium price L12M(1,3)

NAV per share(2)

£6.86

Market cap (mm)(1)

£1,278.4

Shares outstanding less those held

in treasury (mm)

216.9

Shares held in treasury (mm)(2)

4.6

52 week high

£7.45

52 week low

£3.98

120

10.00

9.00

100

8.00

7.00

80

6.00

60

5.00

4.00

40

3.00

2.00

20

1.00

Analyst coverage and rating

Buy

Jun 23 Jul 23 Aug 23 Sep 23 Oct 23 Nov 23 Dec 23 Jan 24 Feb 24 Mar 24 Apr 24 May 24

Uranium Spot Price

Buy

Yellow Cake Share Price

Blue chip shareholder register

Buy

Buy

Hold

MMCAP Fund

JD Squared

-

Yellow Cake Share Price (£)

£5.90

Uranium Spot Price (US$/lb.)

Last share price(1)

5.

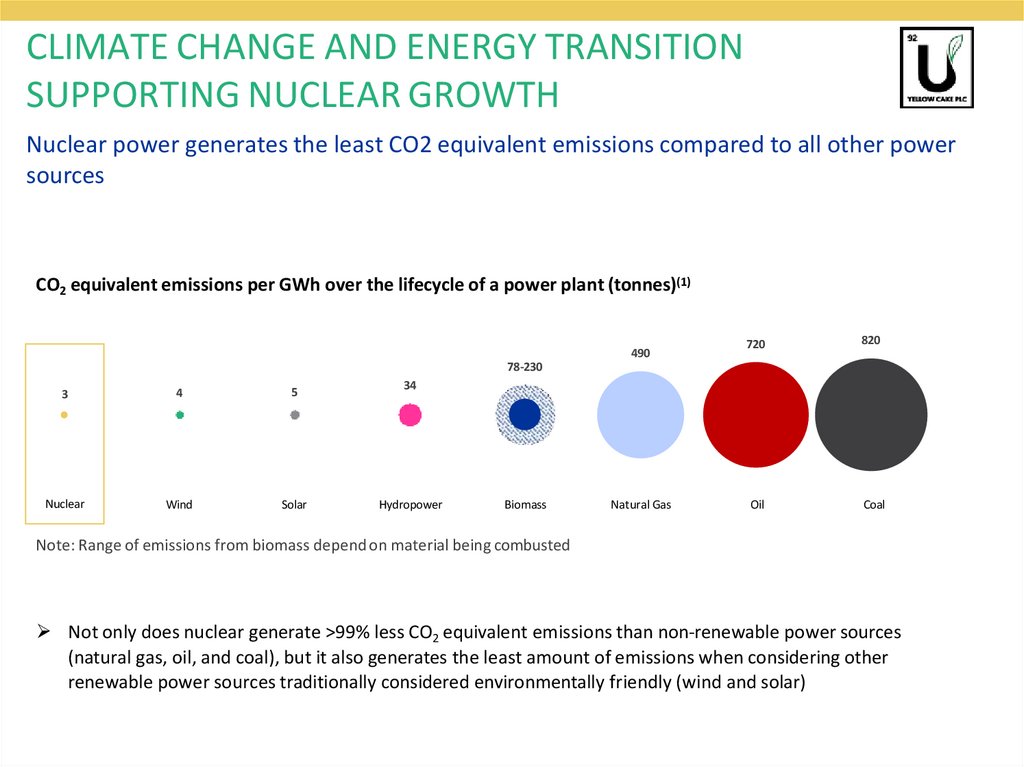

CLIMATE CHANGE AND ENERGY TRANSITIONSUPPORTING NUCLEAR GROWTH

Nuclear power generates the least CO2 equivalent emissions compared to all other power

sources

CO2 equivalent emissions per GWh over the lifecycle of a power plant (tonnes)(1)

490

720

820

Oil

Coal

78-230

3

4

5

Nuclear

Wind

Solar

34

Hydropower

Biomass

Natural Gas

Note: Range of emissions from biomass depend on material being combusted

Not only does nuclear generate >99% less CO2 equivalent emissions than non-renewable power sources

(natural gas, oil, and coal), but it also generates the least amount of emissions when considering other

renewable power sources traditionally considered environmentally friendly (wind and solar)

6.

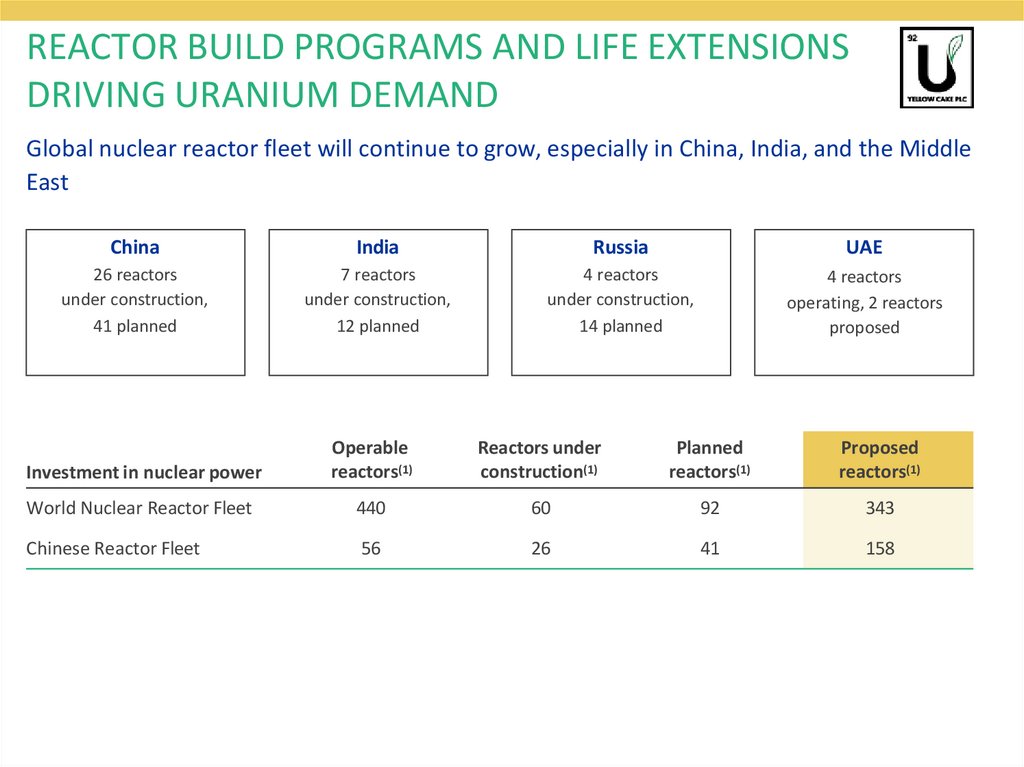

REACTOR BUILD PROGRAMS AND LIFE EXTENSIONSDRIVING URANIUM DEMAND

Global nuclear reactor fleet will continue to grow, especially in China, India, and the Middle

East

China

India

Russia

UAE

26 reactors

under construction,

41 planned

7 reactors

under construction,

12 planned

4 reactors

under construction,

14 planned

4 reactors

operating, 2 reactors

proposed

Investment in nuclear power

Operable

reactors(1)

Reactors under

construction(1)

Planned

reactors(1)

Proposed

reactors(1)

World Nuclear Reactor Fleet

440

60

92

343

Chinese Reactor Fleet

56

26

41

158

7.

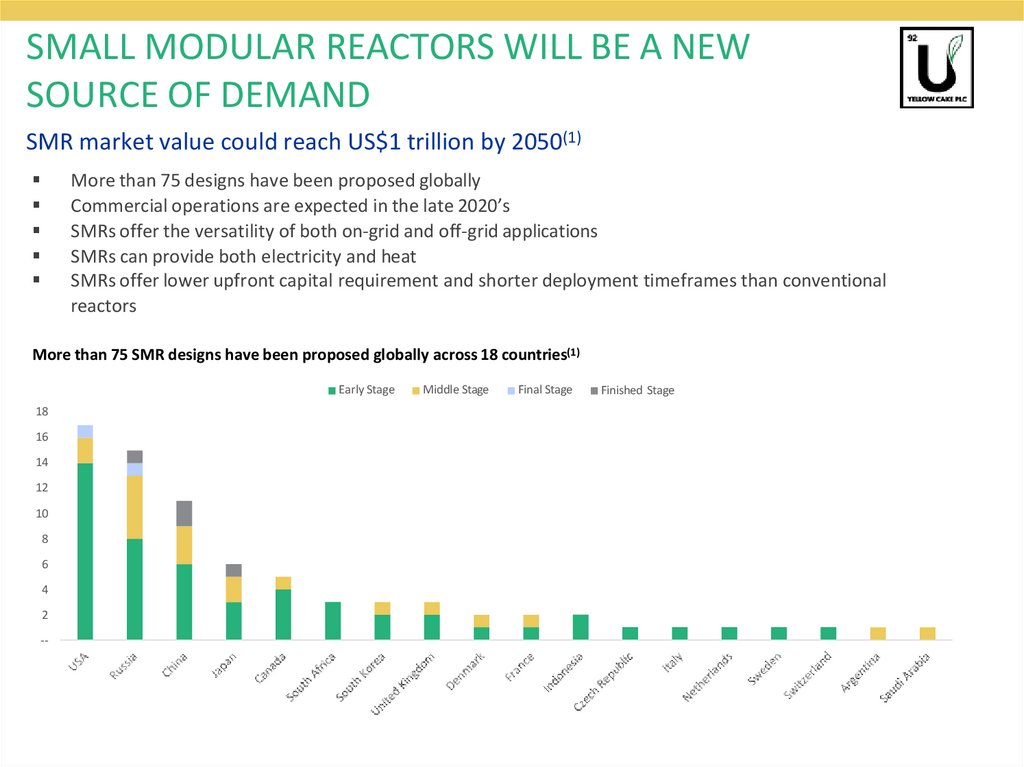

SMALL MODULAR REACTORS WILL BE A NEWSOURCE OF DEMAND

SMR market value could reach US$1 trillion by 2050(1)

More than 75 designs have been proposed globally

Commercial operations are expected in the late 2020’s

SMRs offer the versatility of both on-grid and off-grid applications

SMRs can provide both electricity and heat

SMRs offer lower upfront capital requirement and shorter deployment timeframes than conventional

reactors

More than 75 SMR designs have been proposed globally across 18 countries(1)

Early Stage

18

16

14

12

10

8

6

4

2

--

Middle Stage

Final Stage

Finished Stage

8.

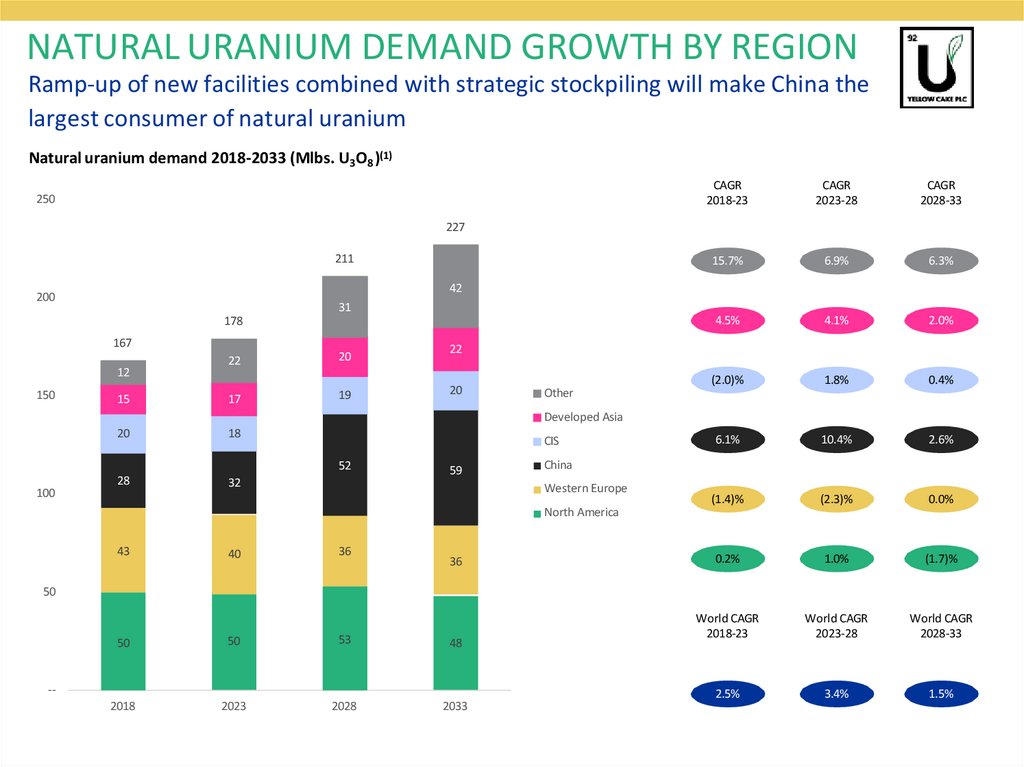

NATURAL URANIUM DEMAND GROWTH BY REGIONRamp-up of new facilities combined with strategic stockpiling will make China the

largest consumer of natural uranium

Natural uranium demand 2018-2033 (Mlbs. U3O8 )(1)

250

CAGR

2018-23

CAGR

2023-28

CAGR

2028-33

15.7%

6.9%

6.3%

4.5%

4.1%

2.0%

(2.0)%

1.8%

0.4%

6.1%

10.4%

2.6%

(1.4)%

(2.3)%

0.0%

0.2%

1.0%

(1.7)%

World CAGR

2018-23

World CAGR

2023-28

World CAGR

2028-33

2.5%

3.4%

1.5%

227

211

42

200

31

178

167

22

20

15

17

19

20

18

28

32

12

150

22

20

Other

Developed Asia

CIS

52

100

59

China

Western Europe

North America

43

40

36

36

50

50

50

53

48

2018

2023

2028

2033

--

9.

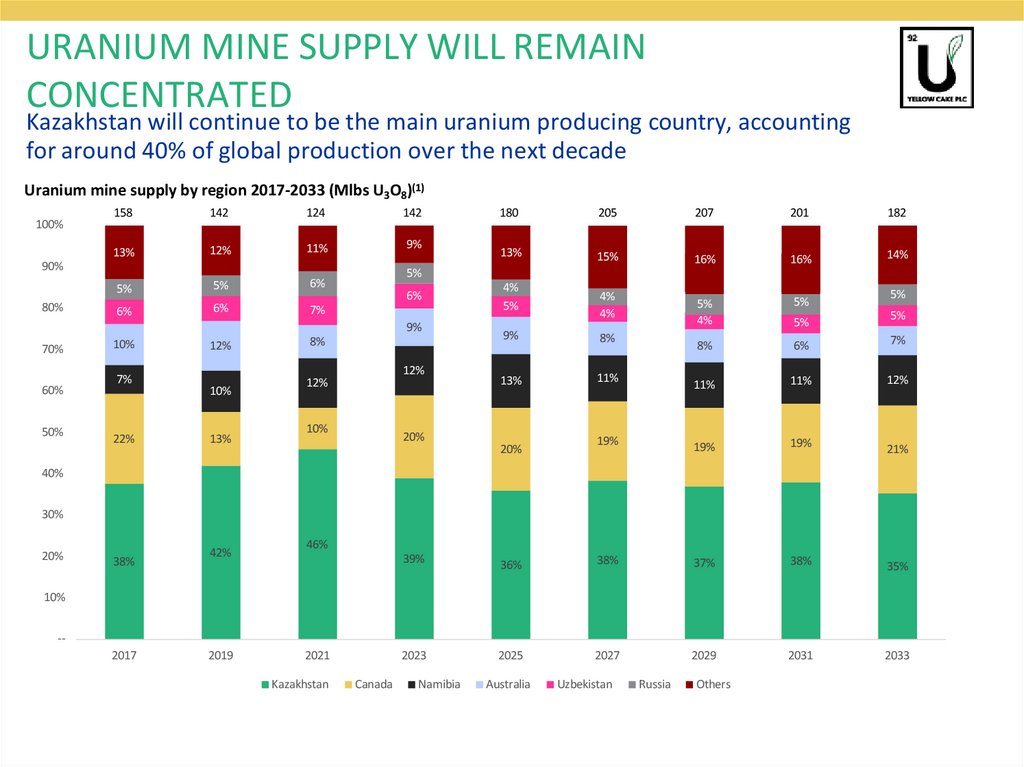

URANIUM MINE SUPPLY WILL REMAINCONCENTRATED

Kazakhstan will continue to be the main uranium producing country, accounting

for around 40% of global production over the next decade

Uranium mine supply by region 2017-2033 (Mlbs U3O8)(1)

100%

158

142

124

142

13%

12%

11%

9%

90%

80%

5%

5%

6%

6%

6%

7%

60%

50%

10%

7%

22%

12%

10%

13%

205

207

201

182

13%

15%

16%

16%

14%

5%

4%

5%

8%

6%

7%

11%

11%

12%

19%

19%

19%

21%

5%

6%

9%

70%

180

8%

12%

12%

10%

20%

4%

5%

4%

4%

9%

8%

13%

11%

20%

5%

5%

5%

40%

30%

20%

38%

42%

46%

39%

36%

38%

37%

38%

35%

2023

2025

2027

2029

2031

2033

Australia

Uzbekistan

10%

-2017

2019

2021

Kazakhstan

Canada

Namibia

Russia

Others

10.

YELLOW CAKE IS WELL POSITIONED TO BENEFITFROM CURRENT MARKET TRENDS

Nuclear energy provides low emission power generation that is critical to decarbonisation

Globally, demand for uranium is increasing due to aggressive nuclear plant build programs, reactor

life extensions, and small modular reactor developments

Western countries have been dependent on Russian uranium, conversion, and enrichment

historically but are now shifting away towards ex-Russian supply

Term contracting activity increased significantly in 2023 and is likely to remain at an elevated level

There is a growing uranium supply deficit as producing mines enter their “end of life”, secondary

supply declines, and excess inventory has been drawn down

Having secured 21.7Mlbs. in U3O8 inventory and benefitting from an ongoing framework

agreement with Kazatomprom that provides access to US$100m in further material per year,

Yellow Cake is well positioned to benefit from market tailwinds