finance

financeSimilar presentations:

")

The Money Markets Assoc. Prof

1.

BUS 362 Financial Institutions andMarkets

Week 6: Financial Markets:The Money Markets

Assoc. Prof. Hülya Hazar

Faculty of Economics and Administrative Sciences, Department of

Business Administration

hulyahazar@aydin.edu.tr

1

2.

Financial Institutions and Markets1. The Efficient Market Hypothesis

2. The Money Markets Defined

3. The Purpose of Money Markets

4. Money Market Instruments

5. Who Participates in Money Markets?

6. Comparing Money Market Securities

ue.aydin.edu.tr

2

3.

Financial Institutions and MarketsThe efficient markets hypothesis:

• The efficient market hypothesis views the expectations as

equal to optimal forecasts using all available information.

• Assuming the market is in equilibrium, expected returns

equal required returns.

• A security’s price fully reflects all available information in an

efficient market.

• In an efficient market, all abnormal profit opportunities will be

eliminated.

ue.aydin.edu.tr

3

4.

Financial Institutions and MarketsFavorable evidence on efficient market hypothesis:

• Investment analysts and mutual funds don't beat

the market.

• Stock prices reflect publicly available information

• Stock prices and exchange rates close to random walk

(future behavior is independent of past history)

• Technical analysis does not outperform market

ue.aydin.edu.tr

4

5.

Financial Institutions and MarketsUnfavorable evidence on efficient market hypothesis:

• Small-firm effect: small firms have abnormally high returns

• January effect: high returns in January

• Market overreaction: stock prices may overreact to news announcements

and that the pricing errors are corrected only slowly

• Excessive volatility: the stock market displays excessive volatility

(fluctuations in stock prices are greater than is warranted by fluctuations in their

fundamental value)

• Mean reversion: stocks with low returns today tend to have high returns in

the future

• New information is not always immediately incorporated into

stock prices

ue.aydin.edu.tr

5

6.

Financial Institutions and MarketsThe money market:

• Money (currency) is not actually traded in the money

markets.

• The securities in the money market are short term with high

liquidity; therefore, they are close to being money.

• Securities have characteristics:

• Usually sold in large denominations ($1,000,000 or more)

• Low default risk

• Mature in one year or less from their issue date, although

most mature in less than 120 days

ue.aydin.edu.tr

6

7.

Financial Institutions and MarketsThe purpose of money markets:

• Investors in money market: Provides a place for

warehousing surplus funds for short periods of time

• Borrowers from money market provide low-cost source of

temporary funds

• Corporations and government use these markets because

the timing of cash inflows and outflows are not well

synchronized.

• Money markets provide a way to solve these cash-timing

problems.

ue.aydin.edu.tr

7

8.

Financial Institutions and MarketsMoney market instruments:

• Treasury Bills

• State Funds

• Repurchase Agreements

• Negotiable Certificates of Deposit

• Commercial Paper

• Banker’s Acceptance

• Eurodollars

ue.aydin.edu.tr

8

9.

Financial Institutions and MarketsMoney market instruments:

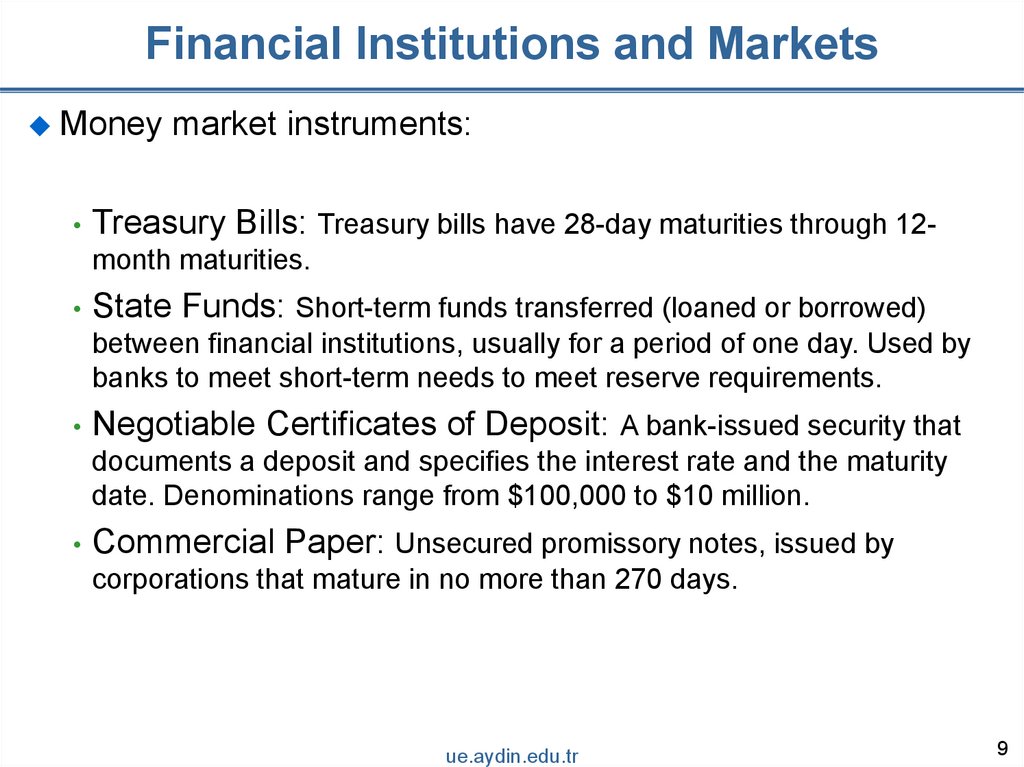

• Treasury Bills: Treasury bills have 28-day maturities through 12-

month maturities.

• State Funds: Short-term funds transferred (loaned or borrowed)

between financial institutions, usually for a period of one day. Used by

banks to meet short-term needs to meet reserve requirements.

• Negotiable Certificates of Deposit: A bank-issued security that

documents a deposit and specifies the interest rate and the maturity

date. Denominations range from $100,000 to $10 million.

• Commercial Paper: Unsecured promissory notes, issued by

corporations that mature in no more than 270 days.

ue.aydin.edu.tr

9

10.

Financial Institutions and MarketsMoney market instruments:

• Repurchase Agreements (repos): A form of short-term borrowing

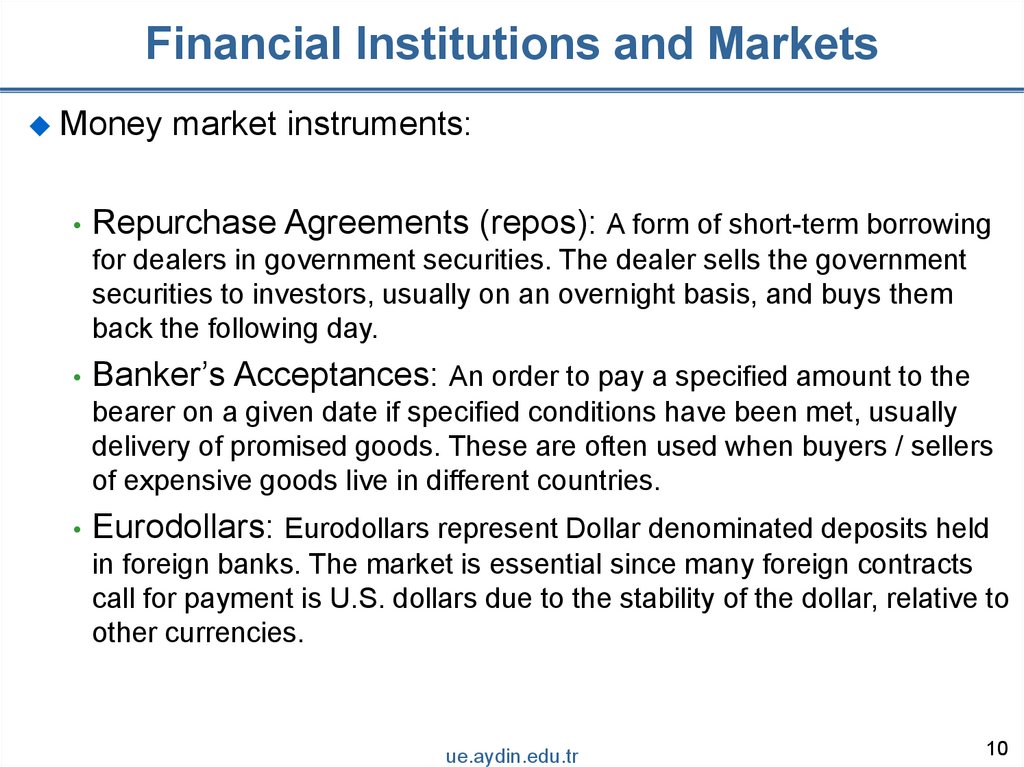

for dealers in government securities. The dealer sells the government

securities to investors, usually on an overnight basis, and buys them

back the following day.

• Banker’s Acceptances: An order to pay a specified amount to the

bearer on a given date if specified conditions have been met, usually

delivery of promised goods. These are often used when buyers / sellers

of expensive goods live in different countries.

• Eurodollars: Eurodollars represent Dollar denominated deposits held

in foreign banks. The market is essential since many foreign contracts

call for payment is U.S. dollars due to the stability of the dollar, relative to

other currencies.

ue.aydin.edu.tr

10

11.

Financial Institutions and MarketsWho participates in money markets?

• Treasury

• Commercial banks

• Businesses

• Individuals (through banks)

ue.aydin.edu.tr

11

12.

Financial Institutions and MarketsComparing money market securities:

• Issuers range from the government to banks to large

corporations

• Mature in as little as 1 day to as long as 1 year

• The secondary market liquidity varies substantially

ue.aydin.edu.tr

12

13.

Subjects Covered1. The Efficient Market Hypothesis

2. The Money Markets Defined

3. The Purpose of Money Markets

4. Money Market Instruments

5. Who Participates in Money Markets?

6. Comparing Money Market Securities

ue.aydin.edu.tr

13

14.

ReferencesReadings:

Chapters 6 and 11

Reference Book:

Mishkin, Frederic S. Financial Markets and Institutions. Eighth Edition.

UK: Pearson, 2016.

ue.aydin.edu.tr

14

15.

Financial Institutions and MarketsSee you next week…

ue.aydin.edu.tr

15