finance

financeSimilar presentations:

Free movement of capital. Formation of a monetary union and a banking

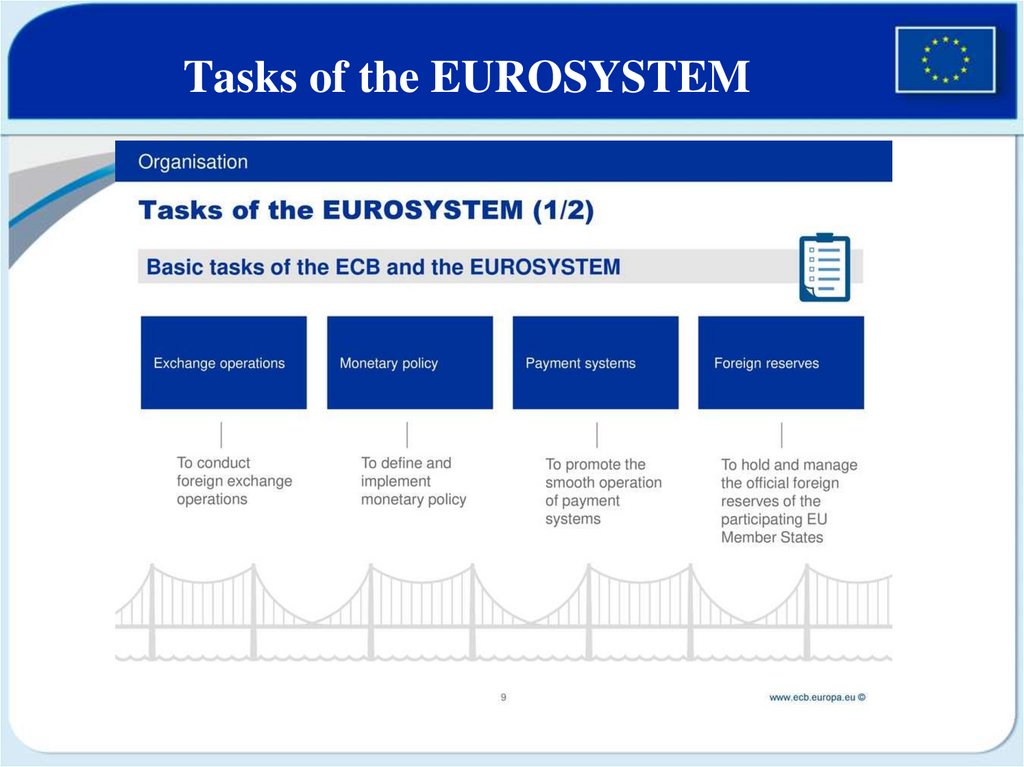

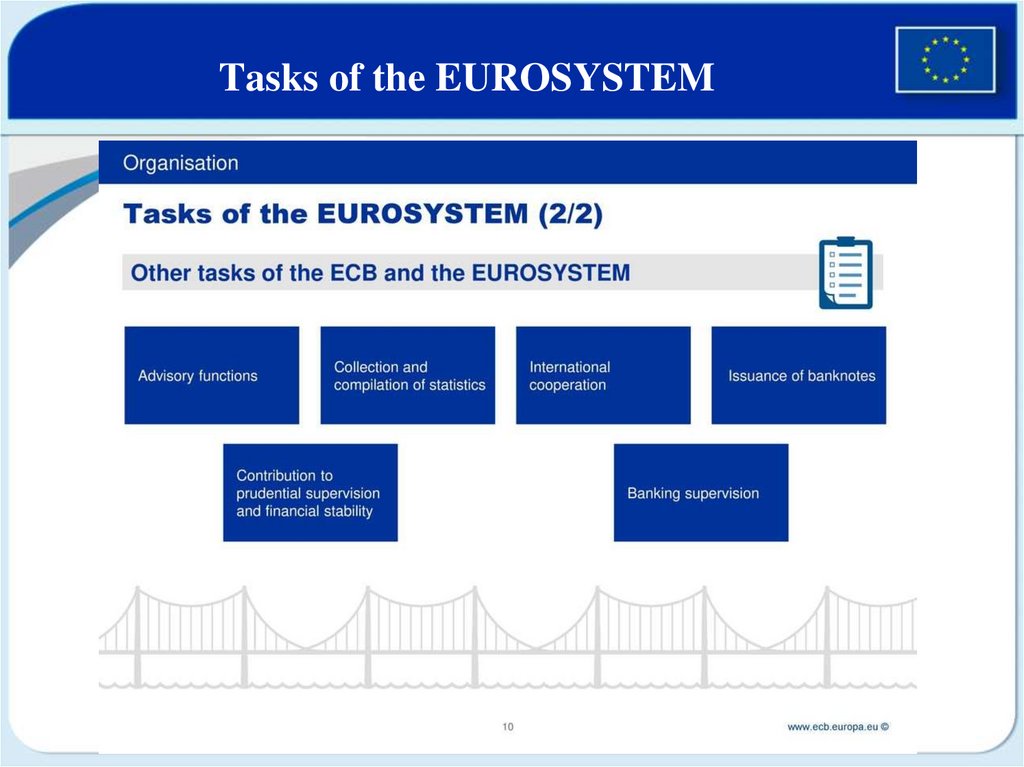

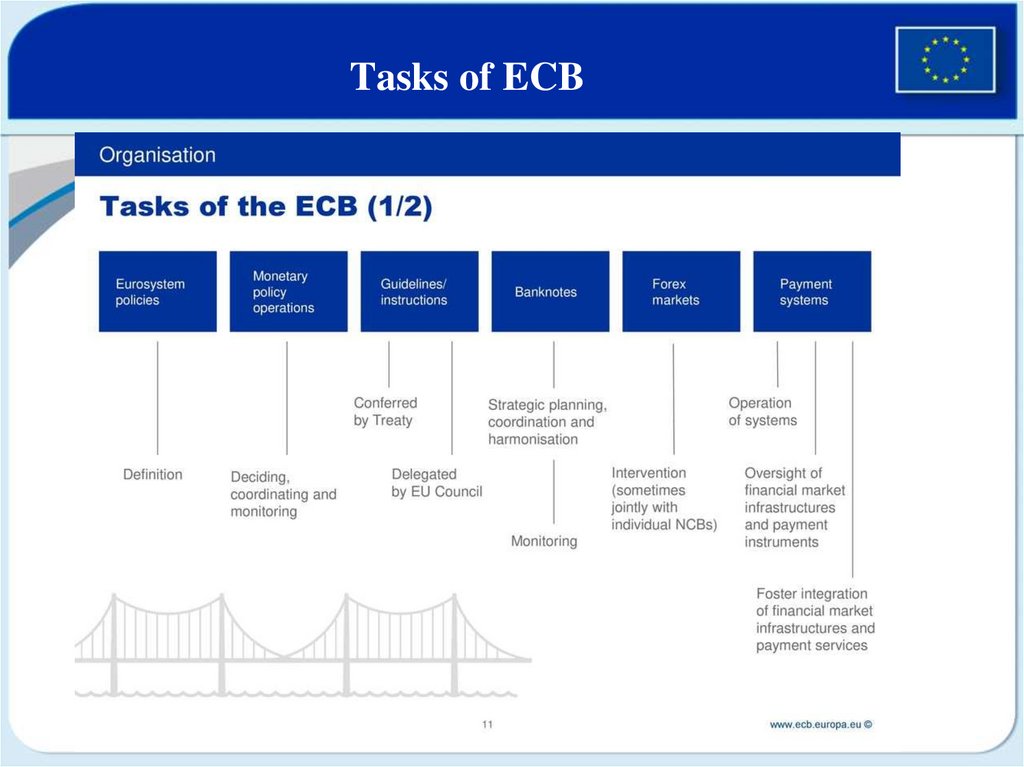

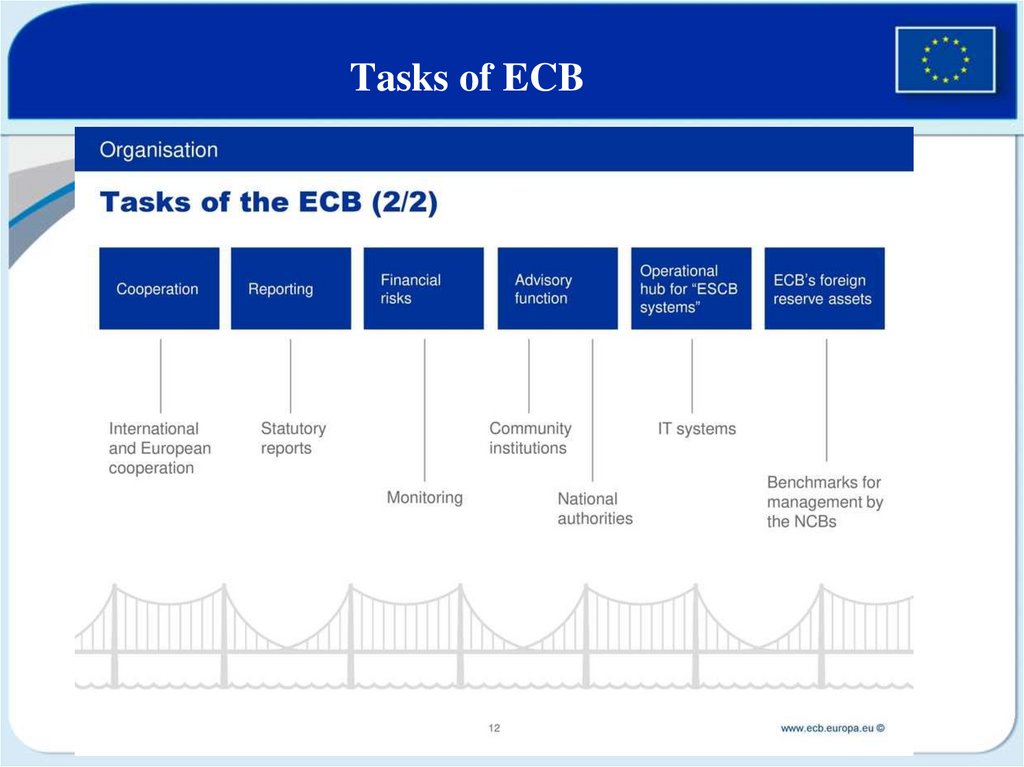

1.

TOPIC 11. FREE MOVEMENT OF CAPITAL. FORMATIONOF A MONETARY UNION AND A BANKING UNION

1. The concept of «capital», «free movement of

capital». Legal exceptions to the freedom of

movement of capital.

2. The concept of a monetary union. The legal

regime of the single currency, the euro area.

3. The EU banking system: structure, sources of

legal regulation

2.

1. The concept of «capital», «free movement of capital». Legalexceptions to the freedom of movement of capital

Free movement of capital is at the heart of the

Single Market and is one of its four freedoms.

Together with free movement of goods, persons and

services it enables integrated, open, competitive and

efficient European financial markets and services

Legal basis

Articles 63 to 66 of the Treaty on the Functioning of the

European Union (TFEU).

3.

Free movement of capitalFree movement of capital is enshrined in the Treaty of Maastricht.

With the entry into force of this treaty in 1994 all restrictions on

capital movements and payments across borders were prohibited.

The aim of liberalisation is to enable integrated, open, and

efficient European financial markets.

For European citizens, free movement of capital means the

ability to carry out many transactions, such as

opening bank accounts abroad

buying shares in non-domestic companies

investing where the best return is

purchasing real estate in another country

For companies, it means being able to

invest in, and own, other European companies

raise money where it is cheapest

4.

DefinitionThe treaty on the functioning of the EU does not define the

term «movements of capital». In the absence of a definition, the

Court of Justice of the European Union has held that the definitions

in the nomenclature annexed to Directive 88/361/EEC can be used

to define that term.

According to these definitions, cross-border capital

movements include:

foreign direct investments (FDI)

real estate investments or purchases

securities investments (e.g. in shares, bonds, bills, unit trusts)

granting of loans and credit

other operations with financial institutions, including personal

capital operations such as dowries, legacies, endowments, etc.

5.

Legal frameworkAmongst the fundamental freedoms that underpin the EU single market (free

movement of people, goods, services and capital), the free movement of capital is

the most recent. It became a directly applicable treaty freedom only with the

Maastricht treaty.

The legal framework for the free movement of capital includes

treaty provisions

protocols and declarations

transitional measures granted by the acts of accession to new member countries

Article 63 of the Treaty on the functioning of the EU prohibits all

restrictions on capital movements and payments not only within the EU, but

also between EU countries and countries outside the EU.

However, further provisions in the treaty stipulate a number of exceptions to the

principle of free movement of capital, in particular to prevent problems related to

taxation, prudential supervision of financial institutions, public policy and security.

The Court of Justice of the European Union (CJEU) has the final say in

interpreting treaty provisions, and there is extensive case law in this area.

6.

Exceptions and justified restrictionsExceptions are largely confined to capital movements related to

third countries (Article 64 of the TFEU).

In addition to the option for Member States of maintaining

restrictions on direct investment and other transactions which existed

on a given date, the Council may also, after consulting the European

Parliament, unanimously adopt measures which constitute a step

backwards in the liberalisation of capital movements with third

countries.

In addition, the Council and the European Parliament may adopt

legislative measures involving direct investment, establishment,

provision of financial services or the admission of securities to

capital markets.

Article 66 of the TFEU covers emergency measures vis-à-vis

third countries, limited to a period of six months.

7.

Exceptions and justified restrictionsThe only justified restrictions on capital movements in general,

including movements within the EU, are laid down in Article 65

of the TFEU.

These include:

(i) measures to prevent infringements of national law (namely for

taxation and prudential supervision of financial services);

(ii) procedures for the declaration of capital movements for

administrative or statistical purposes; and

(iii) measures justified on the grounds of public policy or public

security.

The latter was invoked during the European sovereign debt crisis,

when Cyprus (2013) and Greece (2015) were forced to introduce

capital controls in order to prevent an excessive outflow of capital.

Cyprus removed all of the remaining restrictions in 2015 and

Greece did so in 2019.

8.

Exceptions and justified restrictionsArticle 144 of the TFEU allows, within the framework of the

balance of payments assistance programmes, for protective

balance of payments measures where difficulties jeopardise the

functioning of the internal market or where a sudden crisis

occurs. This safeguard clause is only available to Member

States outside of the euro area.

Finally, Articles 75 and 215 of the TFEU provide for the

possibility of financial sanctions either to prevent and combat

terrorism or based on decisions adopted within the framework

of the common foreign and security policy.

9.

2. The concept of a monetary union. The legalregime of the single currency, the euro area

The Economic and Monetary Union (EMU)

is an umbrella term for the group of policies

aimed at converging the economies of member

states of the European Union at three stages.

The policies cover the 19 eurozone states, as

well as non-euro European Union states.

10.

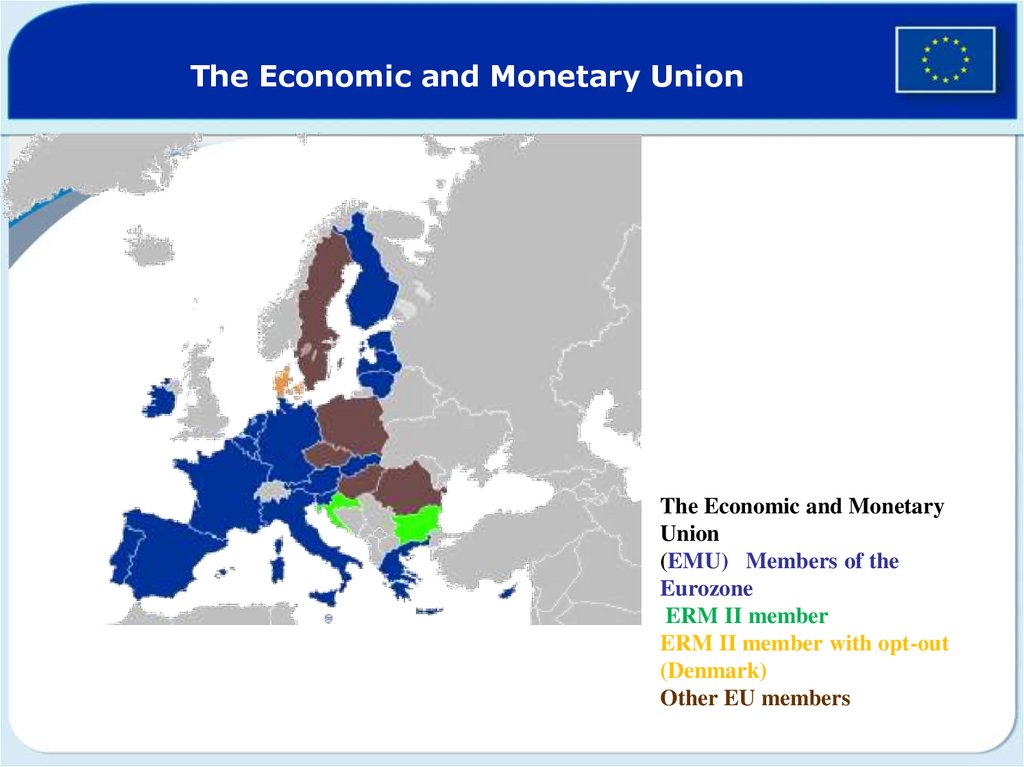

The Economic and Monetary UnionThe Economic and Monetary

Union

(EMU) Members of the

Eurozone

ERM II member

ERM II member with opt-out

(Denmark)

Other EU members

11.

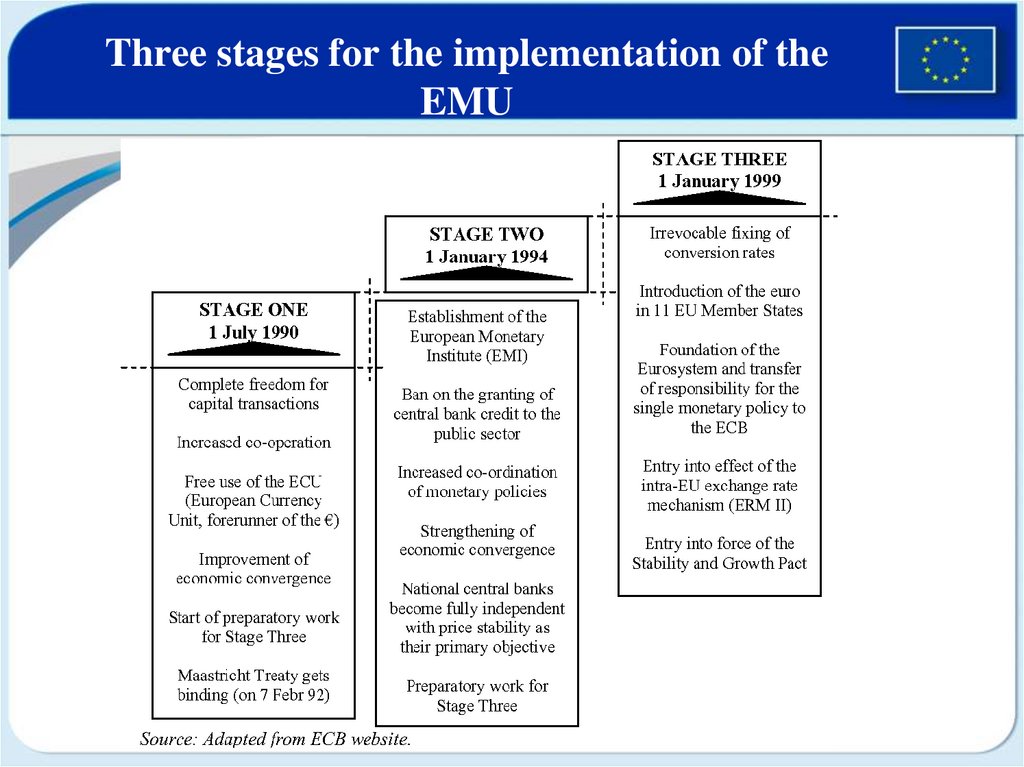

Three stages for the implementation of theEMU

12.

The three stages for the implementation of theEMU were the following:

Stage One: 1 July 1990 - 31 December 1993

On 1 July 1990, exchange controls are abolished, thus capital

movements are completely liberalised in the European Economic

Community.

The Treaty of Maastricht in 1992 establishes the completion of

the EMU as a formal objective and sets a number of economic

convergence criteria, concerning the inflation rate, public

finances, interest rates and exchange rate stability.

The treaty enters into force on 1 November 1993.

13.

Stages for the implementation of the EMUStage Two: 1 January 1994 - 31 December 1998

• The European Monetary Institute is established as the forerunner of the

European Central Bank, with the task of strengthening monetary cooperation

between the member states and their national banks, as well as supervising ECU

banknotes.

• On 16 December 1995, details such as the name of the new currency (the euro)

as well as the duration of the transition periods are decided.

• On 16–17 June 1997, the European Council decides at Amsterdam to adopt the

Stability and Growth Pact, designed to ensure budgetary discipline after creation

of the euro, and a new exchange rate mechanism (ERM II) is set up to provide

stability above the euro and the national currencies of countries that haven't yet

entered the eurozone.

• On 3 May 1998, at the European Council in Brussels, the 11 initial countries

that will participate in the third stage from 1 January 1999 are selected.

• On 1 June 1998, the European Central Bank (ECB) is created, and on 31

December 1998, the conversion rates between the 11 participating national

currencies and the euro are established.

14.

Stages for the implementation of the EMU• From the start of 1999, the euro is now a real currency, and a

single monetary policy is introduced under the authority of the ECB.

A three-year transition period begins before the introduction of actual

euro notes and coins, but legally the national currencies have already

ceased to exist.

• On 1 January 2001, Greece joins the third stage of the EMU.

• On 1 January 2002, the euro notes and coins are introduced.

• On 1 January 2007, Slovenia joins the third stage of the EMU.

• On 1 January 2008, Cyprus and Malta join the third stage of the

EMU.

• On 1 January 2009, Slovakia joins the third stage of the EMU.

• On 1 January 2011, Estonia joins the third stage of the EMU.

• On 1 January 2014, Latvia joins the third stage of the EMU.

• On 1 January 2015, Lithuania joins the third stage of the EMU.