english

englishSimilar presentations:

Today’s Agenda

1.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of Production Execution

4. Specific MU Business cases

5. Resources for further study

2.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of production Execution

4. Specific MU Business cases

5. Resources for further study

3.

What is MU?1) MU is the abbreviation for Material Utilisation

2) It is a Product Supply Measure to track the efficiency of

material usage in Manufacturing Plants*

3) It uses an IWS Approach to identify losses versus an Ideal

State.

4) MU can be reported as both Percent % and Monetary Value

5) MU is obtained directly out of SAP, via the ZD28 report

6) MU can be calculated at material level or any level of aggregation

7) MU is NOT an account or a cost center !

4.

What is MU?The MU Measure is obtained by comparing:

Value of materials

that should have

been used*:

98 $M

versus

Value of

materials

actually used :

100$M

MU% = 98% (Theoretical Usage* divided by Total Actual Usage)

MU Loss = 2 $M (Total Actual Usage less Theoretical Usage)

*The theoretical usage does not include the scrap factor!

5.

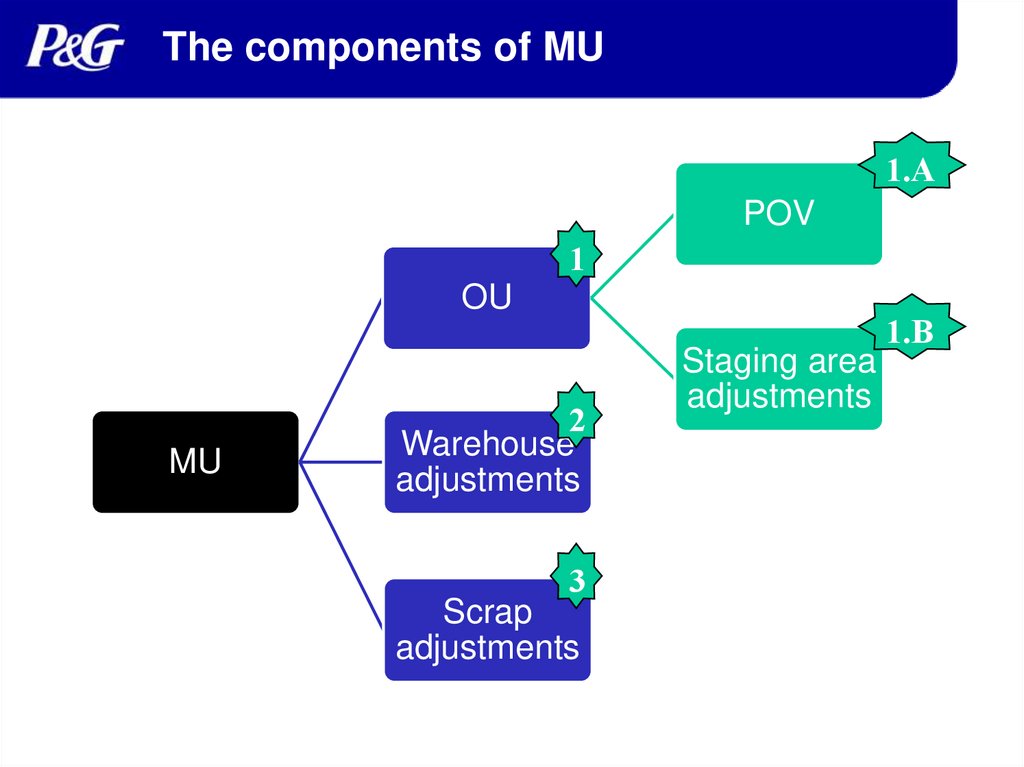

The components of MU1.A

POV

1

OU

MU

2

Warehouse

adjustments

3

Scrap

adjustments

Staging area

adjustments

1.B

6.

1. Definitions: OU• Operational Utilization is an analysis of POV

and staging area adjustments.

• This considers only materials with planned

and unplanned goods issues on the PO’s

which meet the selection criteria.

• Mathematically for a given material it is

calculated as follows:

Planned Usage w/o Scrap

Actual Production Usage + Staging Adjustments

• The plant total OU is weighted by price and

the ideal state is 100%

7.

1.A Process Order Variance (POV)• Process Order Variance is an analysis of net usage to PO’s

versus the planned usage. This considers only materials

with planned and unplanned goods issues on the PrO’s

which meet the selection criteria. The target is 0%.

• Mathematically it is represented as follows:

Quantity Variance w/o Scrap x 100

Planned Usage

• Quantity Variance = Actual Production Usage minus Planned Usage

• This is the only report that allows aggregation by Production

Line. Other reports do not since they include metrics not

linked to individual production lines in the system.

8.

1.B Staging Area Adjustment• Difference between the actual inventory

counted and the inventory quantity on record in

the system in the Staging Area

• Staging area = Small inventory quantities in

locations close to where production resources

will consume the material normally on or near

the production resources. A plant can have any

number of staging areas

• Production movement type: 931/932

9.

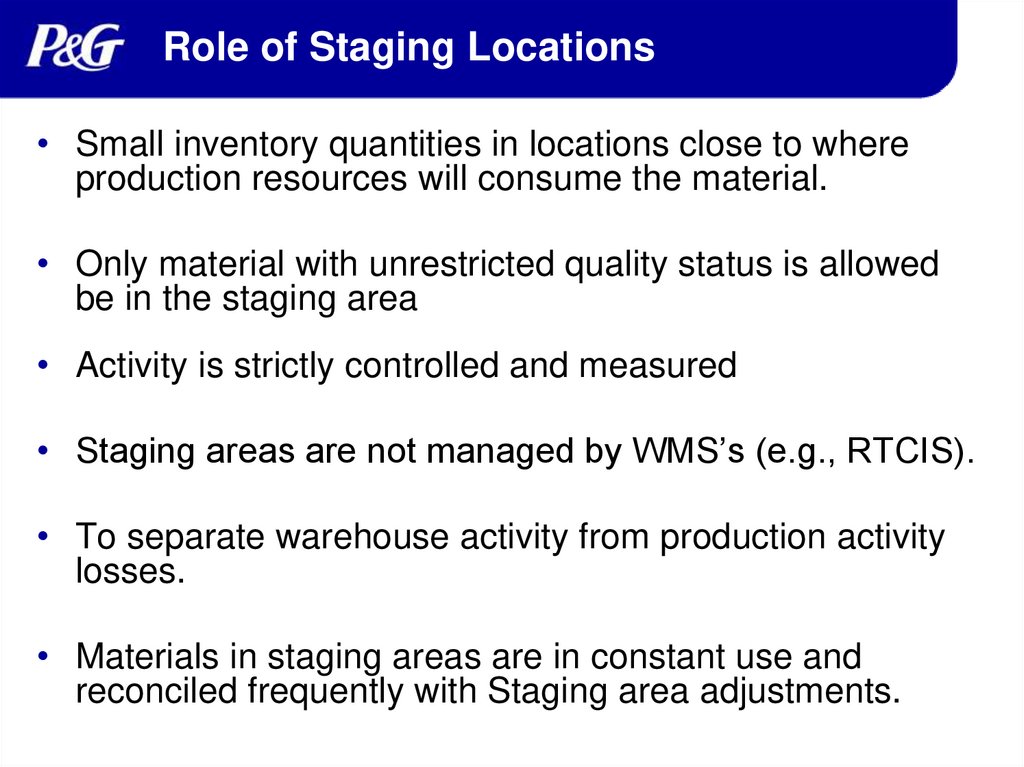

Role of Staging Locations• Small inventory quantities in locations close to where

production resources will consume the material.

• Only material with unrestricted quality status is allowed

be in the staging area

• Activity is strictly controlled and measured

• Staging areas are not managed by WMS’s (e.g., RTCIS).

• To separate warehouse activity from production activity

losses.

• Materials in staging areas are in constant use and

reconciled frequently with Staging area adjustments.

10.

2. Warehouse Adjustment• Difference between the actual inventory counted and

the inventory quantity on record in the system prior to

reaching the Staging Area.

• Warehouse adjustments can be done for any type of

materials (RPM, intermediates or FP)

• Only active materials are taken into account

• Part of GMC/GLC, shows under the inventory variance

GL account

• Production movement type: 700 series

11.

Role of Warehouse Storage Locations• Warehouse is the location where materials are received

and stored until they are needed for production, shipment

or scrap so materials could be in any quality status

• Store large amounts of inventory

• Normally physically separated from production resources

• All activity strictly controlled and measured

• Accurate balance at any time. Warehouse areas are

reconciled as needed (min 1x/month) with Warehouse

adjustment movements (70X)

12.

3. Scrap Adjustment• Inventory adjustments for scrap of materials,

only for active materials

• Active materials = materials that have been

consumed or manufactured during the

period

• Part of TDC under IDE

• Production movement type: 55Xseries

13.

Knowledge checkCan we measure MU by production

asset (e.g. line level)?

14.

Knowledge checkWhat can cause MU to be above 100% ?

15.

Knowledge checkCan a site reduce it’s reported MU loss

by increasing their scrap factors?

16.

What is MUV ?• MUV = The difference between the actuals

losses (expressed as OU) vs the scrap factors

included in the finance BOMs

• MUV is a financial variance used by the CCT to

prepare the materials forecast updates

• This measure is not used by PS and has no

practical value in understanding the plant losses. It

is only relevant in the RBU TDC forecasting

process.

17.

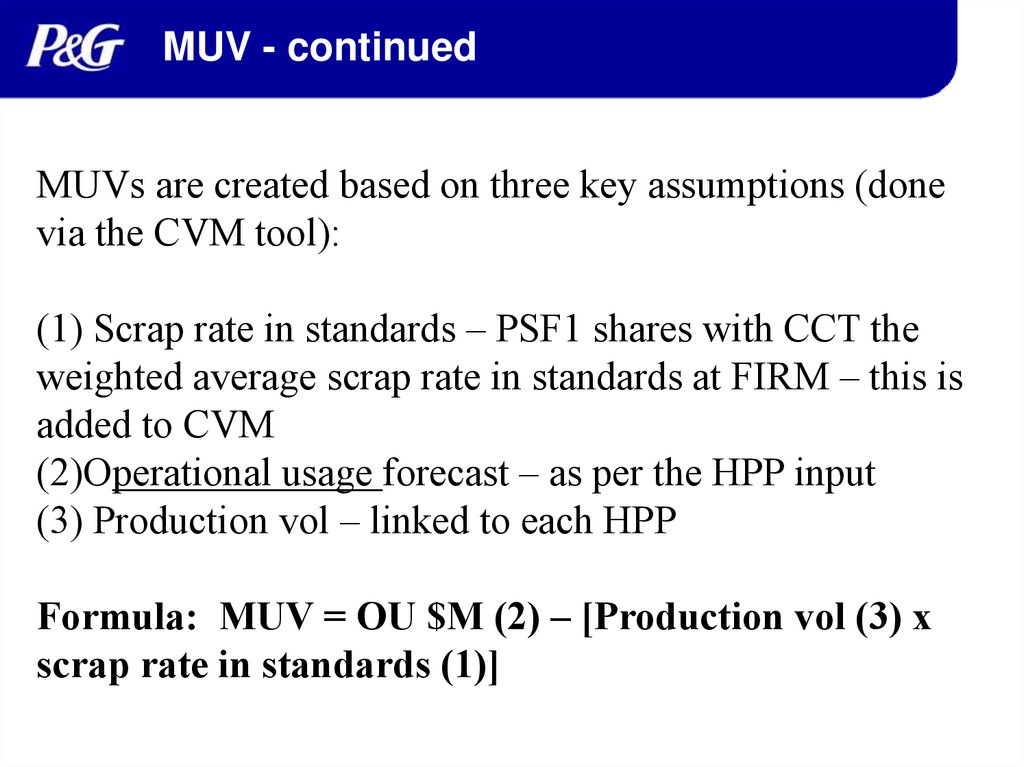

MUV - continuedMUVs are created based on three key assumptions (done

via the CVM tool):

(1) Scrap rate in standards – PSF1 shares with CCT the

weighted average scrap rate in standards at FIRM – this is

added to CVM

(2)Operational usage forecast – as per the HPP input

(3) Production vol – linked to each HPP

Formula: MUV = OU $M (2) – [Production vol (3) x

scrap rate in standards (1)]

18.

MU vs MUV – Simplified comparisonActual

usage

Actual

usage

vs.

vs.

Production

BOM

MU

Material

Utilization

Finance

BOM

MUV

Material Usage

Variance

MU = difference between Actual Usage vs. Production BOM (w/o

scrap) -> loss elimination tool

MU Variance = difference between OU vs. Finance BOM scrap

factor -> forecast tool

19.

MU accountingZD28 element

Accounting Entry

P&L impact

OU

(Process Order

Variance and

Staging Adjustment)

RPM and FP Staging/Variance

accounts

As per the VHP

GMC Adjustments

(warehouse

adjustment)

IDE Adjustments

(scrap adjustment)

(e.g. 58120100 Stg Area Var PM Std)

GMC Variance accounts

(e.g. 58510100 Inv Var RM Std

58520100 Inv Var PM Std )

IDE accounts

(e.g. 58710100 Disp St RM Std

58720100 Disp St PM Std )

Reconciled in MUV

June release*

(peg rate)

Reconciled in

GMC/GLC

As incurred

Reconciled in IDE

* Part of the GMC adjustment could be captured in the Peg Rate if forecasted at FIRM

20.

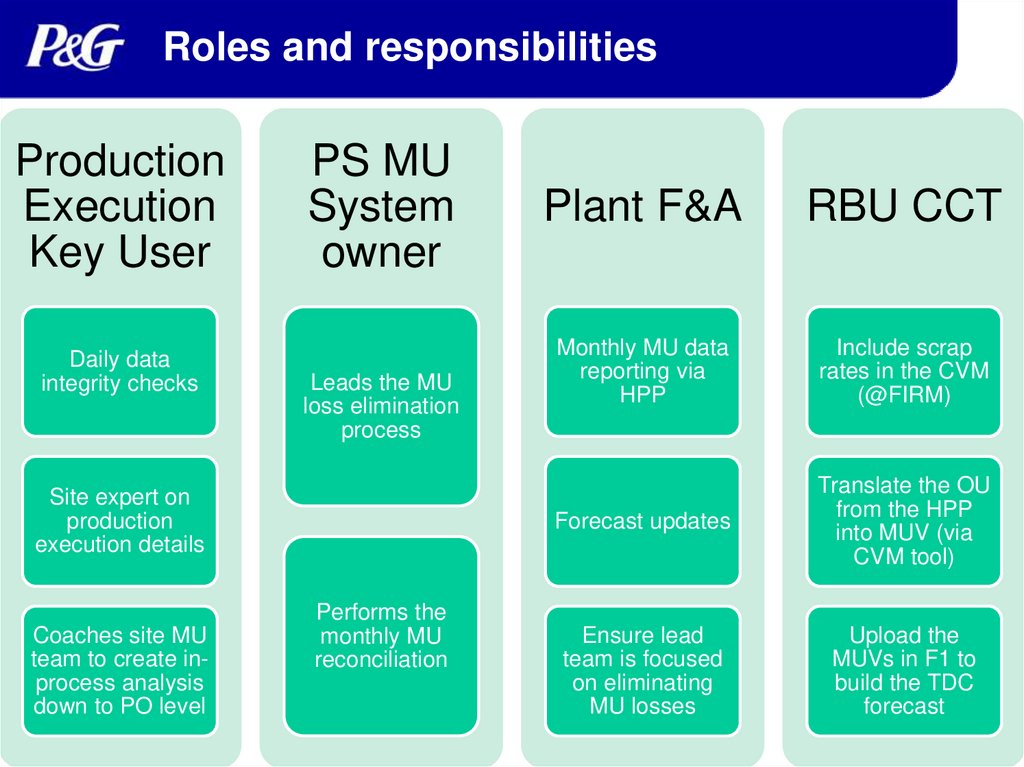

Roles and responsibilitiesProduction

Execution

Key User

Daily data

integrity checks

PS MU

System

owner

Leads the MU

loss elimination

process

Site expert on

production

execution details

Coaches site MU

team to create inprocess analysis

down to PO level

Performs the

monthly MU

reconciliation

Plant F&A

RBU CCT

Monthly MU data

reporting via

HPP

Include scrap

rates in the CVM

(@FIRM)

Forecast updates

Translate the OU

from the HPP

into MUV (via

CVM tool)

Ensure lead

team is focused

on eliminating

MU losses

Upload the

MUVs in F1 to

build the TDC

forecast

21.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of production Execution

4. Specific MU Business cases

5. Resources for further study

22.

Set of 3 standard MU reportsPlant MU Report

Users: Plant-based teams, PLT, Plant

F&A, MU leader

Global Category Dashboard

Users: GBU/RBU PS and PS F&A

23.

How to use MU reportsMU performance of the Plant

Preliminary diagnosis

Origin groups, Materials driving top losses;

Enable x-plant/category benchmarking

Basis for HPP – Plant Cost Forecast

It does NOT enable full Loss Analysis and

Elimination actions

PS will continue to use additional systems (Prophicy) and

processes (on-the-floor studies and measurements)

24.

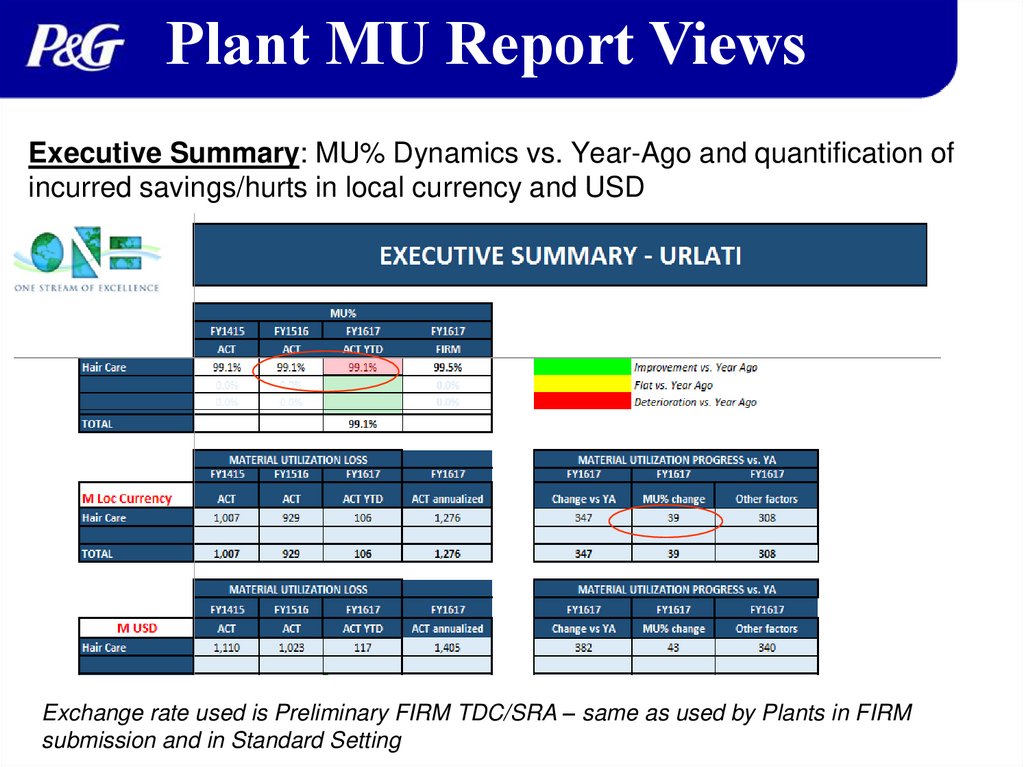

Plant MU Report ViewsExecutive Summary: MU% Dynamics vs. Year-Ago and quantification of

incurred savings/hurts in local currency and USD

Exchange rate used is Preliminary FIRM TDC/SRA – same as used by Plants in FIRM

submission and in Standard Setting

25.

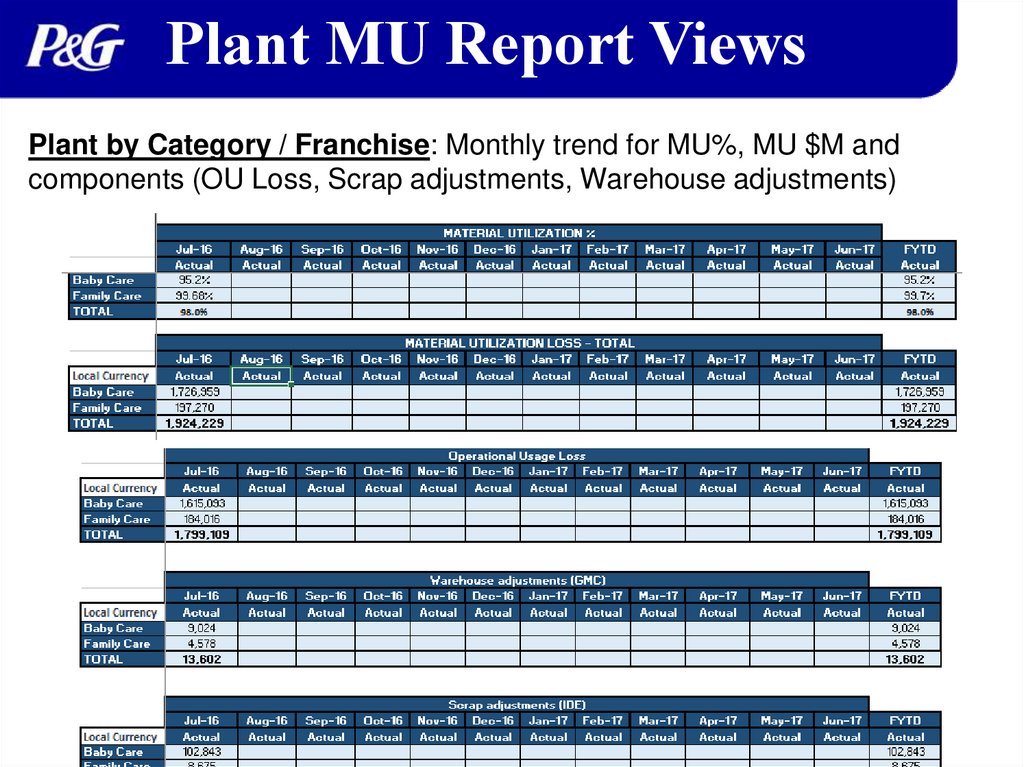

Plant MU Report ViewsPlant by Category / Franchise: Monthly trend for MU%, MU $M and

components (OU Loss, Scrap adjustments, Warehouse adjustments)

26.

Plant MU Report ViewsOrigin Group: Summarized MU (and components) monthly progression by

key groupings of materials (SAP origin groups) at plant level

27.

Plant MU Report ViewsMU Output: The material line item database (ZD28) on which the entire

report is built. It can be used for other pivots/summaries as need by the plant

(i.e. Top 5 losses, Staging Area analysis)

28.

Category/region MU DashboardCategory / Region MU Dashboard is targeted for high level reviews

(GBU view across global plants, or regional GTM reviews)

Similarly to Plant Reports, the

Regional Scorecard shows MU%

Dynamics vs. Year-Ago and

quantification of incurred

savings/hurts in USD

29.

Category/Region MU DashboardContains monthly progression for Key Measures (MU% and MU loss $) as

well as OU loss $M progression useful for unplanned variance proofing

Contains capability for benchmarking at origin group level

30.

Where to find the reportsMaking OPT teamspace:

https://pgone.sharepoint.com/sites/shcmakingopt/SitePages/MaterialUtilization.aspx

31.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of production Execution

4. Specific MU Business cases

5. Resources for further study

32.

Key terms: Bill of Materials (BOM)• Data initiates in the Formula Card and Pack Standards (both

created and approved by R&D)

• From these, SIP creates Bill of Materials

• From the BOM, SIP creates POML

• The final POML may vary from the standards in that it may

include test materials, reblend materials, alternate A v.

alternate B, etc…

• Ultimately, it is the list of materials needed to produce finish

products or intermediates

• It may include raw, pack, intermediates and finished goods

• It is the POML expected material usages compared to site

actuals that generate MU results

33.

Key terms: Scrap Factor• Planned, additional quantity of material that has to be added

to base formula in order to cover material losses in

production process

– 2 ways to set-up scrap factors: in BOM or in Material Master

– Incurred in the end to end production area

• Usually based on historical material usage

• Used as a planning tool to ensure enough materials are

available for production at the time needed

• It is not possible to have a negative scrap factor, i.e., a gain.

Gains reflect inaccurate planning or data integrity issues and

should be corrected – not planned for.

• Scrap factors represent known losses which should be

planned for but also have loss elimination action

plans/forecasts when right for the business. Often business

will create scrap factor tolerances to identify which losses to

target.

34.

Key terms: Scrap in Bill Of Material35.

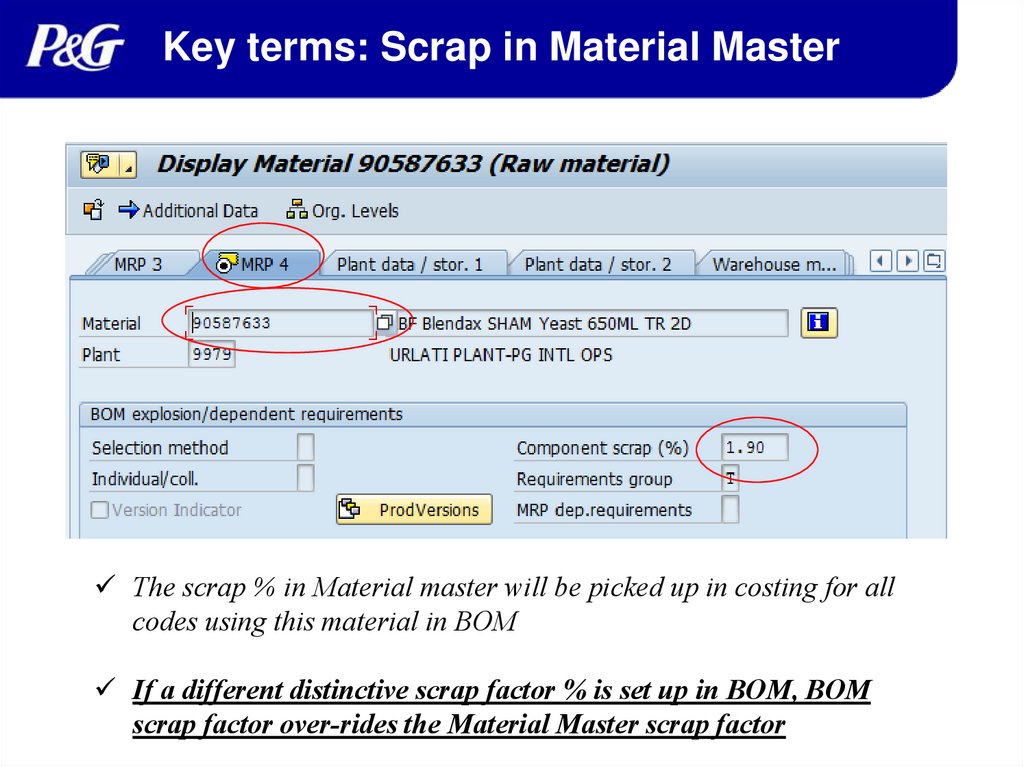

Key terms: Scrap in Material MasterThe scrap % in Material master will be picked up in costing for all

codes using this material in BOM

If a different distinctive scrap factor % is set up in BOM, BOM

scrap factor over-rides the Material Master scrap factor

36.

Key terms: PROCESS ORDERInstrument in SAP created by Planning to confirm what is to be

produced at a point in time*, on which operating line/machine

Before production:

PO contain all materials

required to make a

product

Planned Usage

During and after

production:

Charge any material

consumed against the PO

Actual Usage

SAP is able to compare Actual Usage versus Planned

Usage for any product on any day for any line/machine.

A PO serves as a cost collector for all cost of production –

includes both materials and labor costs. (material + Labour)

A PO can represent a production run that can take any where

from a few minutes to a couple of days

37.

Key terms: Standard Cost• Pre-determined during the annual Product Supply budgeting process

• Constant for the entire fiscal year (set in March-April for the year ahead)

• Every material has a standard cost

• This cost is used to assign value for all transactions for the material.

• Standard costs are tracked in the currency rate of the manufacturing

company. Any conversions made in the MU report will use:

– in SAP ZD28 the previous day’s exchange rate;

– in PSF1 monthly report “Preliminary FIRM TDC and SRAP exchange rate”,

i.e., it is fixed for the year

• The MU report uses the standard cost of a given material at the

time the report is run *

* Key watch-out when pulling data for June!

38.

Material Physical FlowWarehouse

Material

Receipt

WHSE (TANK)

Component Materials

not managed by WMS

Cost/

SIP

WHSE

Component Materials

managed by WMS

ULF

Finished

Cases

Line Staging Areas (no

WMS)

Common Line

Staging Area (no WMS)

Production Line

(Resource)

(Process Order)

or

Intermediate

WHSE

Produced

Materials

managed by

WMS

39.

Material Goods IssuingWarehouse

Material

Receipt

WHSE (TANK)

Component Materials

not managed by WMS

Cost/

SIP

WHSE

Component Materials

managed by WMS

ULF

Finished

Cases

Line Staging Areas (no

WMS)

Common Line

Staging Area (no WMS)

Production Line

(Resource)

(Process Order)

or

Intermediate

WHSE

Produced

Materials

managed by

WMS

40.

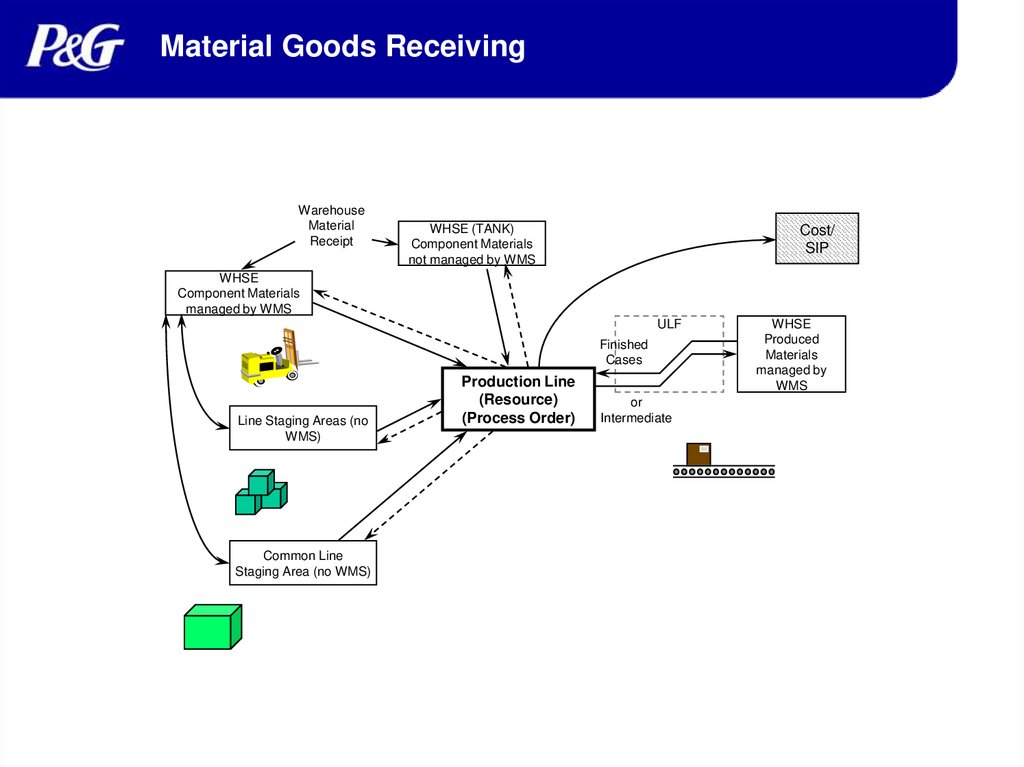

Material Goods ReceivingWarehouse

Material

Receipt

WHSE (TANK)

Component Materials

not managed by WMS

Cost/

SIP

WHSE

Component Materials

managed by WMS

ULF

Finished

Cases

Line Staging Areas (no

WMS)

Common Line

Staging Area (no WMS)

Production Line

(Resource)

(Process Order)

or

Intermediate

WHSE

Produced

Materials

managed by

WMS

41.

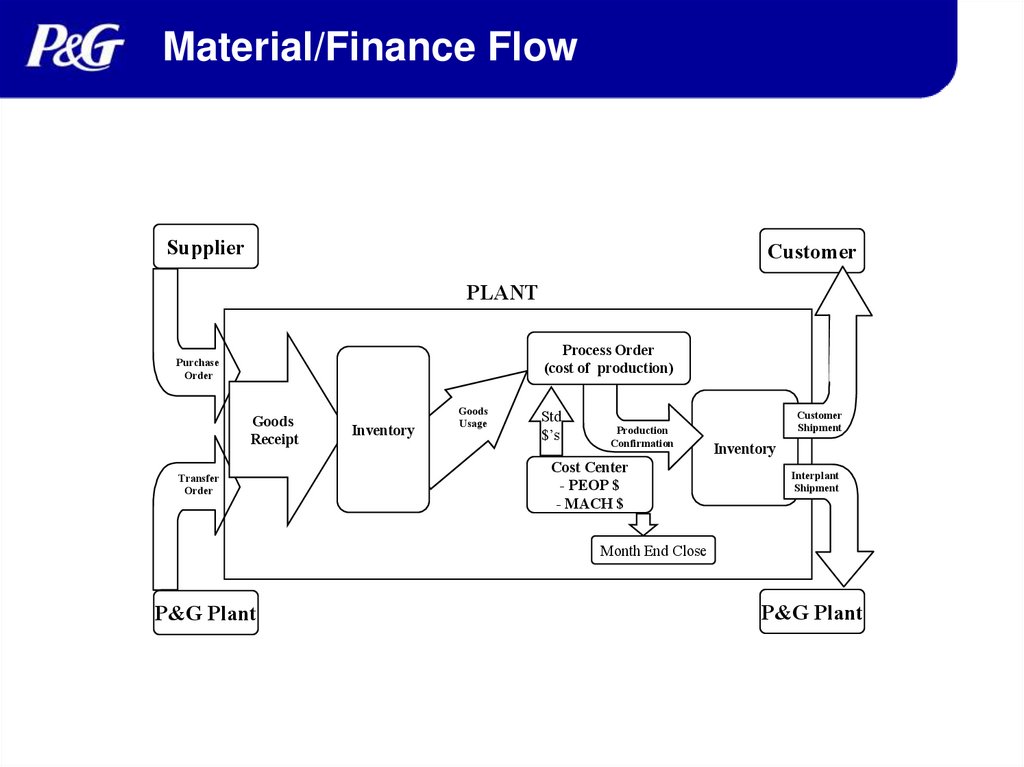

Material/Finance FlowSupplier

Customer

PLANT

Process Order

(cost of production)

Purchase

Order

Goods

Receipt

Transfer

Order

Inventory

Goods

Usage

Std

$’s

Production

Confirmation

Cost Center

- PEOP $

- MACH $

Customer

Shipment

Inventory

Interplant

Shipment

Month End Close

P&G Plant

P&G Plant

42.

Material/Finance FlowProcess Order

Variance

Supplier

PLANT

Process Order

(cost of production)

Purchase

Order

Goods

Receipt

Transfer

Order

P&G Plant

Inventory

Goods

Usage

Std

$’s

Production

Confirmation

Cost Center

- PEOP $

- MACH $

43.

Material/Finance FlowOrder Variance

- Prod Ord Var

- Prod Activ Var

Supplier

PLANT

Process Order

(cost of production)

Purchase

Order

Goods

Receipt

Transfer

Order

P&G Plant

Inventory

Goods

Usage

Std

$’s

Production

Confirmation

Cost Center

- PEOP $

- MACH $

Staging

Area

Variance

44.

Material/Finance FlowSupplier

Customer

PLANT

Process Order

(cost of production)

Purchase

Order

Goods

Receipt

Transfer

Order

Inventory

Goods

Usage

Std

$’s

Production

Confirmation

Cost Center

- PEOP $

- MACH $

Customer

Shipment

Inventory

Interplant

Shipment

Month End Close

P&G Plant

Warehouse Var.

P&G Plant

45.

The Variances Considered in MUProcess Order

Variance

Supplier

Customer

PLANT

Process Order

(cost of production)

Purchase

Order

Goods

Receipt

Transfer

Order

Inventory

Goods

Usage

Std

$’s

Confirmation

Cost Center

- PEOP $

- MACH $

Customer

Shipment

Inventory

Interplant

Shipment

Month End Close

Staging

Area

Variance

P&G Plant

P&G Plant

Warehouse

Variation/Scrap

46.

Q&A• In which period does the MU loss

from a PO show in the MU report ?

47.

Q&A• Which materials should not be part of

the MU report ?

– ROH

– HALBS

– Finish products

– FERT

48.

Q&A• Can a plant that is not producing

anything at the moment show a MU

loss?

49.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of production Execution

4. Specific MU Business cases

5. Resources for further study

50.

Staging area and warehouse adjustments• Who does it– counts are done by P&G or 3rd Parties but posting

differences are only P&G (stock controllers)

• On what frequency – for non-IRA cycle count materials/locations, at

least monthly but could be higher depending on business need. For

IRA cycle count materials/locations, at least annually driven by the

number of materials/locations.

• When is the movement booked – immediately

• What is the approval process – authorizations (by PS

management) are required after the fact for adjustments > $15M.

Sites may define lower thresholds. The authorization implies root

cause analysis but the details of the process is left to the business.

• What’s the role of plant finance – monthly oversight of the

inventory adjustments posted in the plant. F&A should be part of the

concurrence process for large adjustments. The rules need to be

documented in the Decision authority of the site.

51.

Production scrap factor updates• Who does it ? – the MU System Owner or delegate owns the process. It

is communicated via POSS (owned by the Site Ops SPOC) to the PSC.

The master data in SAP is entered by SIP.

• On what frequency ? – at least annually but business needs should

drive higher frequency. This should be criteria based.

• What is the approval process ? – the site SNP team owns the

approval process (which includes Finance)

• Finance BOMs - For Material costing, scrap factors are frozen, part of

calculation, at the specific costing time of the material (can be part of

standard setting for existing materials, or initial standard costing for new

materials)

• What are the implications of updating the production scrap factor ?

– this generates a difference between the current production scrap factor

and the scrap factor originally used for costing generating MUV

(specifically planned variances).

52.

POs amended after month end• Process orders should not be adjusted in previous

periods after the period is closed

• Unlocking the period creates financial risk and often the

complexity of correcting a process order is not fully

understood by those performing this task leading to

increased errors not less

• In practice this can sometimes happen and there are no

SAP restrictions to prevent this

• The implication of making changes to closed periods is

that your actual MU results for those months will

change. As the PSF1 reports do not re-run the data for

older periods, these adjustments will pass unseen in

your actuals

53.

Formula cards with ranges• In certain business cases, the formula cards do not give exact quantities

per product, but rather indicate a range

• Planning will then have to indicate in the BOM a fixed point from within

that range and the MU calculation will be done against that value

• In this case, MU is only a measure for planning accuracy and not a true

loss measurement

• To determine the real loss, the site will have to consider additional factors

such as:

– Can the BOM target be moved to the target lowest usage successfully

demonstrated in the BU?

– Benchmark the BOMs between sites

– Understand the technology limitations that drive us to run above the lowest

point demonstrated

54.

Accounting for Pre-production• Pre-production costs = plant costs incurred in the

start-up of a new asset. These are costs that would

not be chargeable to an Appropriation (>500$M

capital spending) or Construction A.E (<500$M).

• The standard work process for this is to GI materials

used to cost centers (GMC pre-production if

Appropriation level or MOE if AE level). Implications:

– 100% of the cost of materials used in preproduction will

be expensed and show up in PCC

– There is no impact to the site MU, as the full cost ends

up in a cost center

55.

Accounting for EOs• EOs can be used for products in the first 2 stages of the

product development cycle :

– Product Making & Product Testing

– Development Completion

• EOs require the use of 2 specific tools :

1. PIDV process orders (only used in these cases)

2. UNBW materials and finished products

– Specific codes intended for material tracking but with 0 financial value

– Products and component material codes that are not yet qualified for

production

– At GR the value of received material will be posted (expensed ) to the

Cost Center defined in the PO and not to inventory – hence 0 inv value

• When EOs are executed this way there is no MU impact (as

the materials have no value in SAP)

– More detailed guidance on the EO process is available here ->

56.

ReblendDefinition: Source material is treated as a component material.

The source material will be issued to a process order to document

consumption (261 movements).

There are three ways this can be managed. Frequency of

occurrence, material supply work processes and Quality

requirements will dictate the choice:

• A unique Production Version (with a BOM containing the

reblend material) is created for re-blending.

• The Process/Planned Order’s material list is modified by SIP

to contain the reblend material prior to the Order being

released.

• The source material is goods issued to the process order

without modifying the production version or material list.

57.

The Impact on MU of Reblend• The impact on MU will vary depending on a number of

factors: planning, costing and actual execution

Process order set-up

Impact on MU

Unplanned reblend material costed at the

value of the output production (FP)

0 MU impact for the total process order

BUT creates MU variances by material

Unplanned reblend material costed

below/over the value of the output

production (FP)

MU help/hurt is generated on the

process order AND MU variances by

material

Planned reblend costed at the value of the 0 MU impact for the total process order

material it replaces and the BOM

AND 0 MU impact by material

quantities are adjusted accordingly

• Key take-away: the distorting effect on MU of reblend can be

avoided by proper planning

• Resources for further study:

58.

MU and the IWS progressionIn the current IWS phase progression only looks at 2

criteria:

1. The site MU is within 98-102% MU AND

2. That there is a $ loss limit established with action plan

(MU is not classified as a ‘go /no-go criteria’)

Potential directions for future changes to the MU

integration into IWS:

1. $M loss improvement goal

2. Tighter MU% ranges in each phase

3. YoY progress in MU reduction (similar to Plant cost Net

Savings)

59.

Production-Warehouse CSAProduction-Warehouse CSA has Inventory Usage Variance as a Key Attribute

test. The test descriptions are:

1. Does the site perform and document root cause analysis for all inventory

usage variances twice per month at minimum?

2. Does the variance analysis include all process order types (including

experimental orders)?

3. Are corrective actions implemented and monitored to prevent recurrence of

significant inventory usage variances?

4. Does the site conduct a review of top materials incurring significant inventory

usage variances (both losses and gains)?

5. Do the inventory usage variances incurred in SAP match with the offline

variance reports presented to management?

6. Is the Material Utilization reported monthly for all materials consumed in

production?

7. Does the site review the Material Utilization for the consigned materials and

reconcile it with the supplier's records?

60.

Today’s Agenda1. MU Key Concepts

2. The standard MU reports

3. Basic of production Execution

4. Specific MU Business cases

5. Resources for further study

61.

The Global MU BC team• Global MU contacts:

• Regional MU team:

– NA:

– LA:

– EU:

– IMEA:

– APAC EM:

– APAC FM:

– GC: