management

managementSimilar presentations:

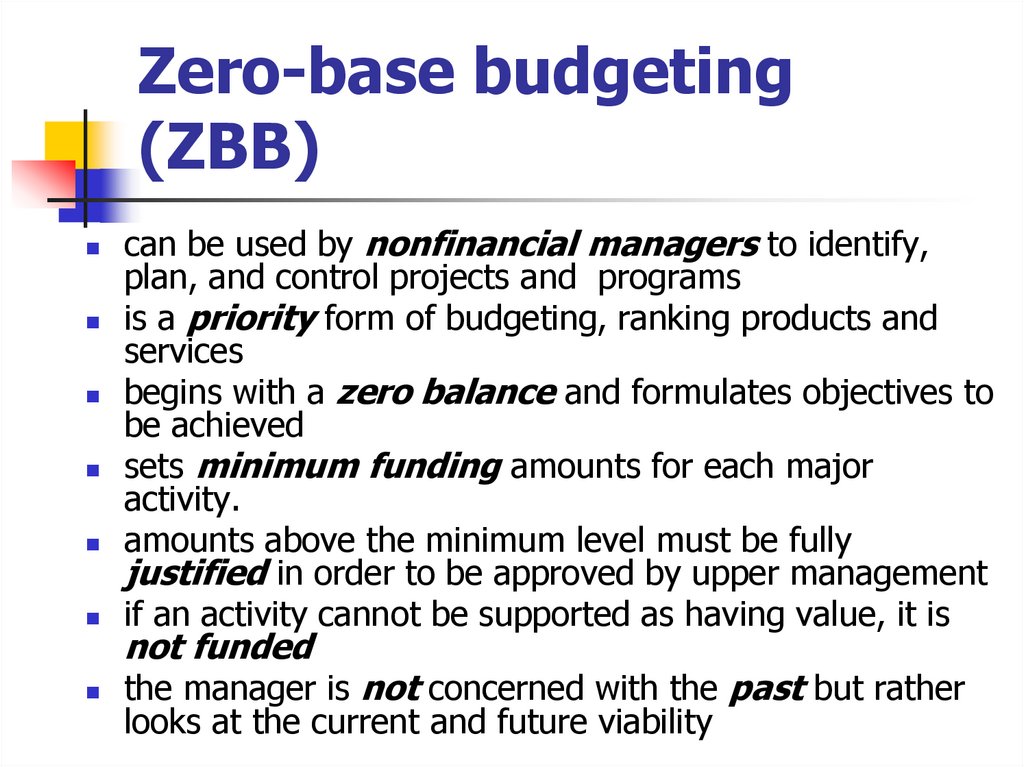

")

")

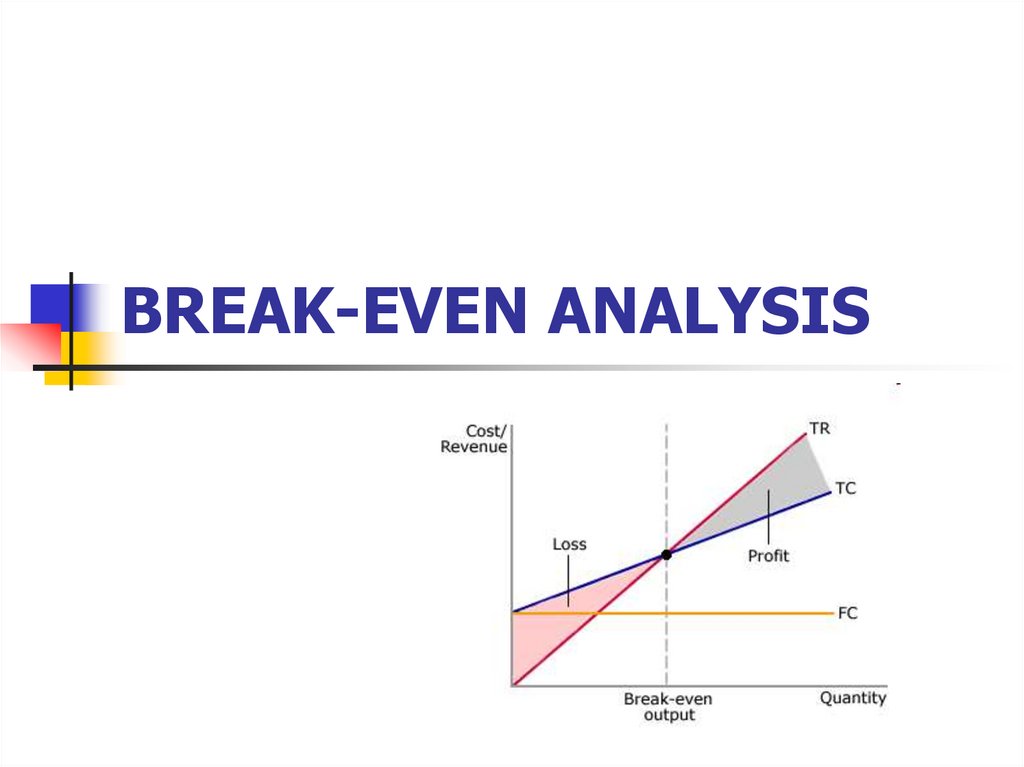

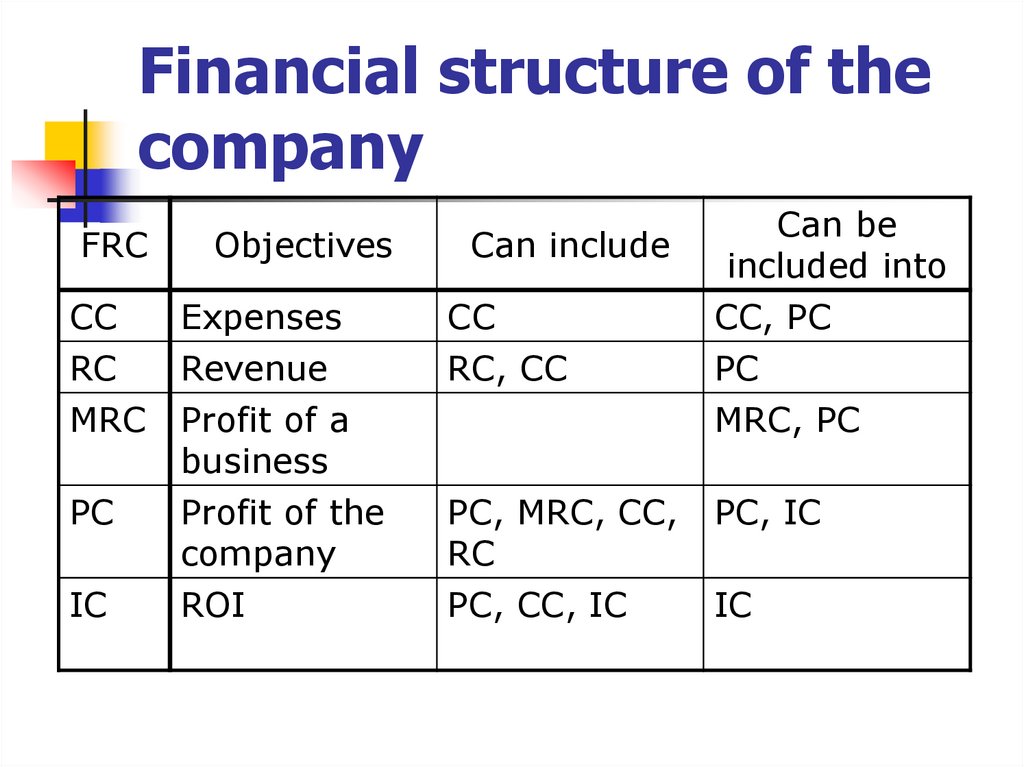

Management Accounting

1.

MANAGEMENT ACCOUNTINGMaria E. Gogolukhina, PhD

2.

INTRODUCTION3.

Management accountingManagement accounting is the

application of professional skills and

knowledge in the preparation of

financial and accounting information in

a manner in which it will assist the

internal management in the formulation

of policies, planning, and control of the

operations of the firm.

4.

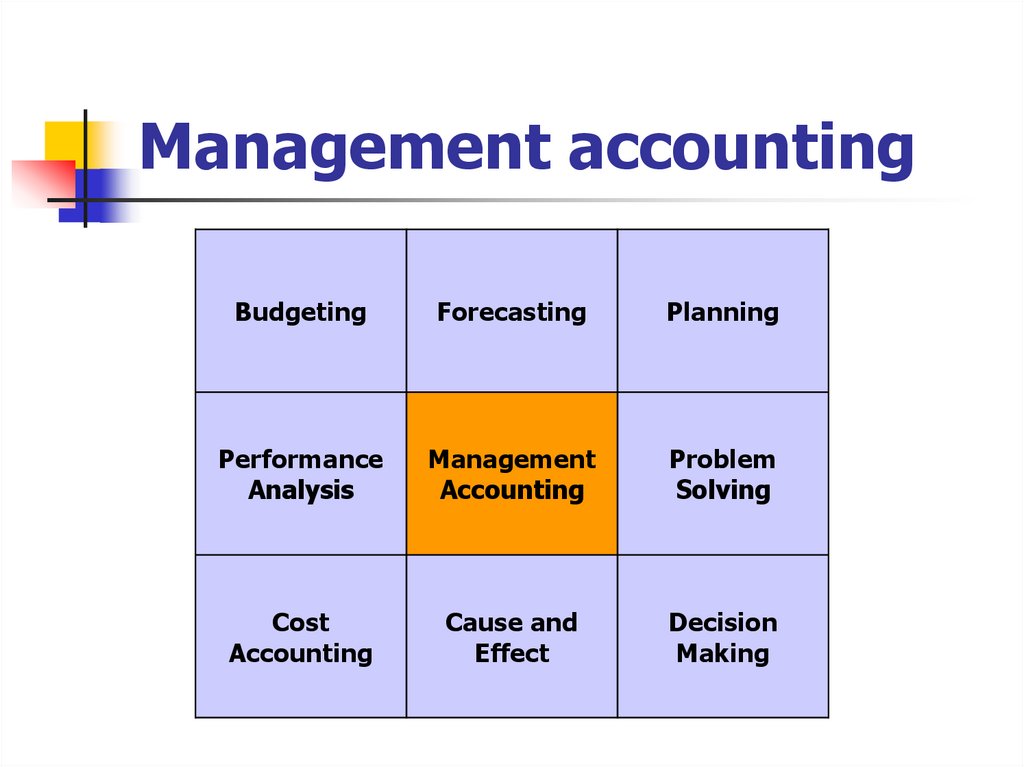

Management accountingBudgeting

Forecasting

Planning

Performance

Analysis

Management

Accounting

Problem

Solving

Cost

Accounting

Cause and

Effect

Decision

Making

5.

Management accountingThe purpose is

to assist management in running the

business the way to achieve the

business objectives

6.

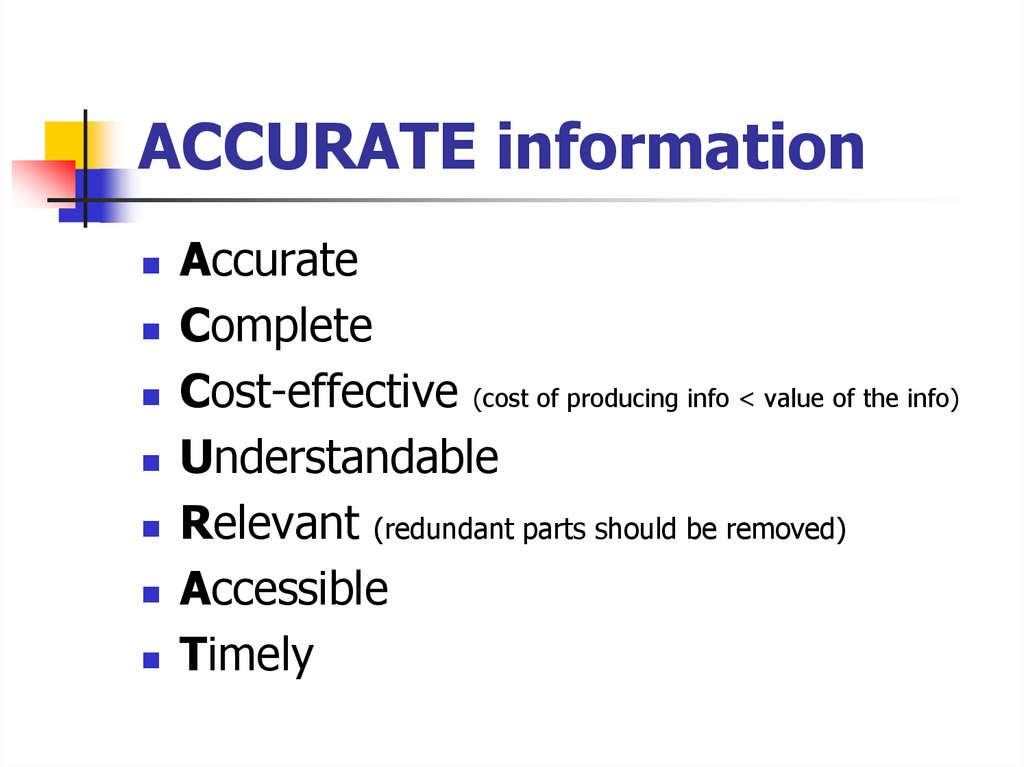

ACCURATE informationAccurate

Complete

Cost-effective (cost of producing info < value of the info)

Understandable

Relevant (redundant parts should be removed)

Accessible

Timely

7.

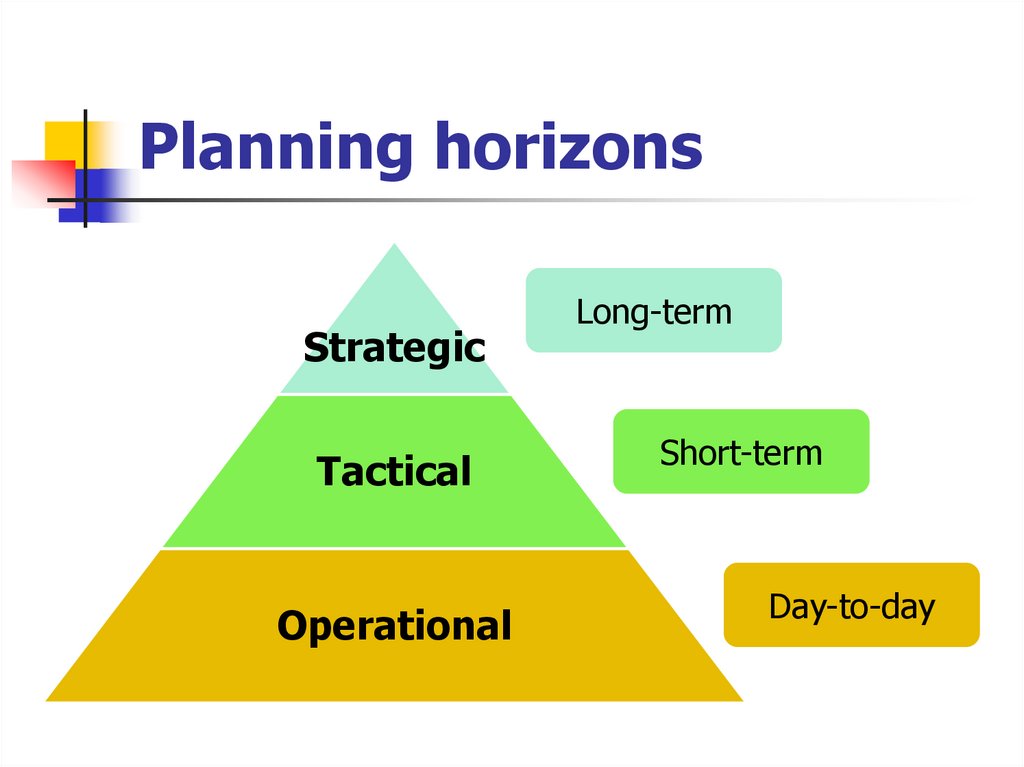

Planning horizonsStrategic

Tactical

Operational

Long-term

Short-term

Day-to-day

8.

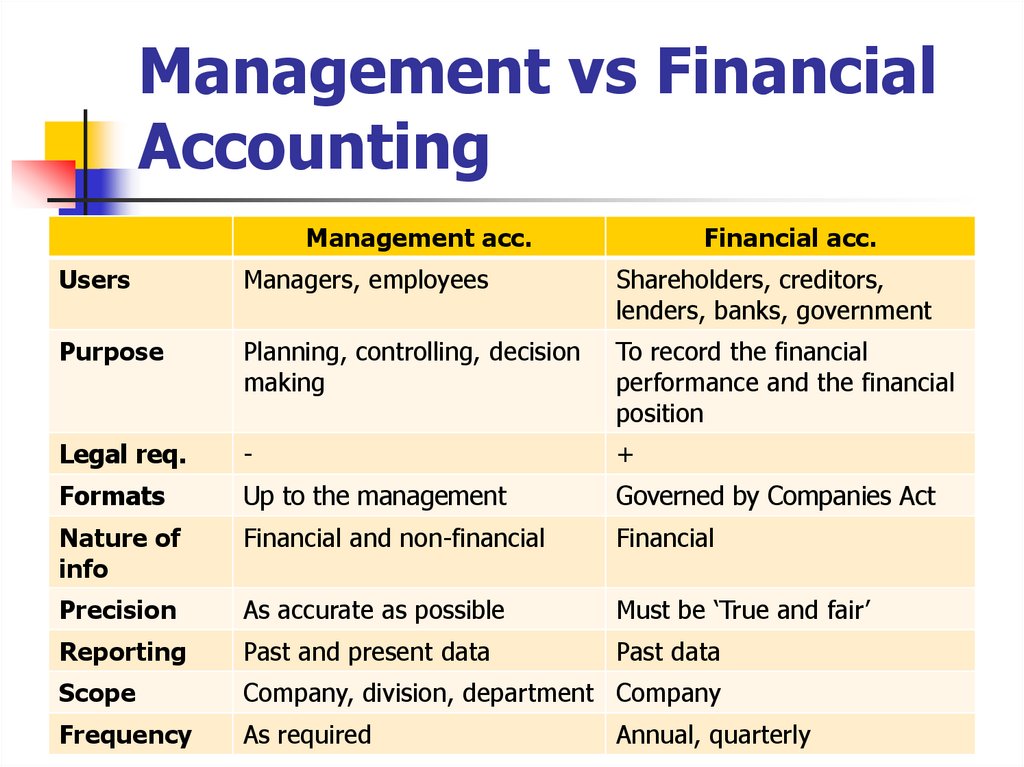

Management vs FinancialAccounting

Management acc.

Financial acc.

Users

Managers, employees

Shareholders, creditors,

lenders, banks, government

Purpose

Planning, controlling, decision

making

To record the financial

performance and the financial

position

Legal req.

-

+

Formats

Up to the management

Governed by Companies Act

Nature of

info

Financial and non-financial

Financial

Precision

As accurate as possible

Must be ‘True and fair’

Reporting

Past and present data

Past data

Scope

Company, division, department Company

Frequency

As required

Annual, quarterly

9.

COST MANAGEMENT10.

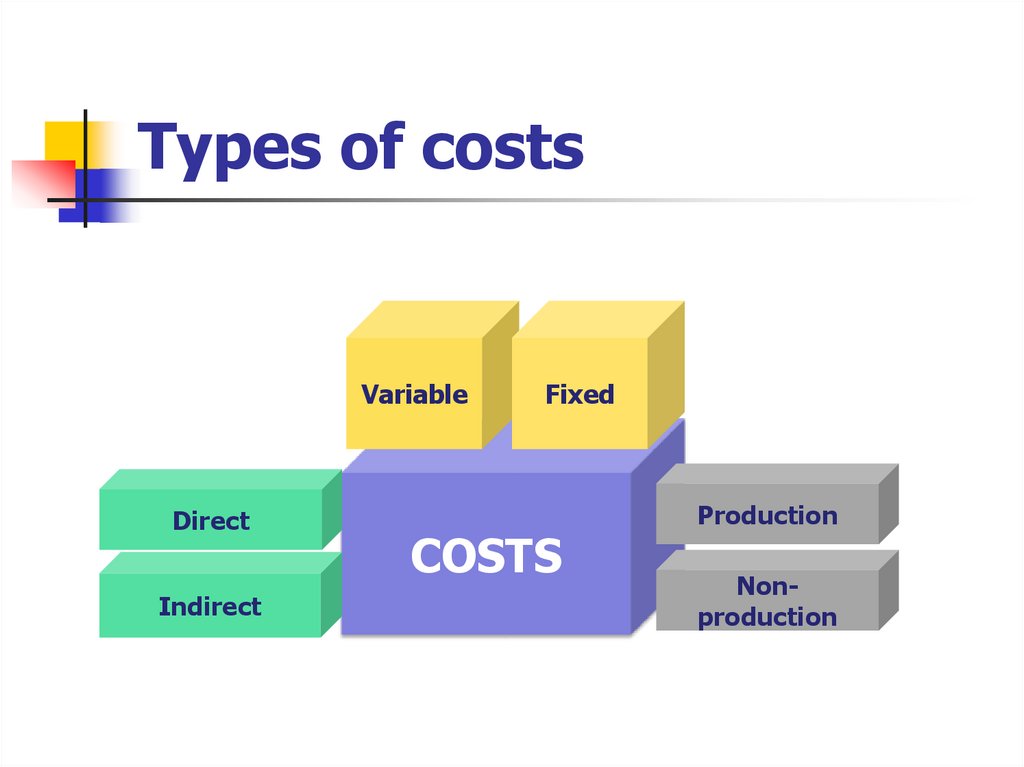

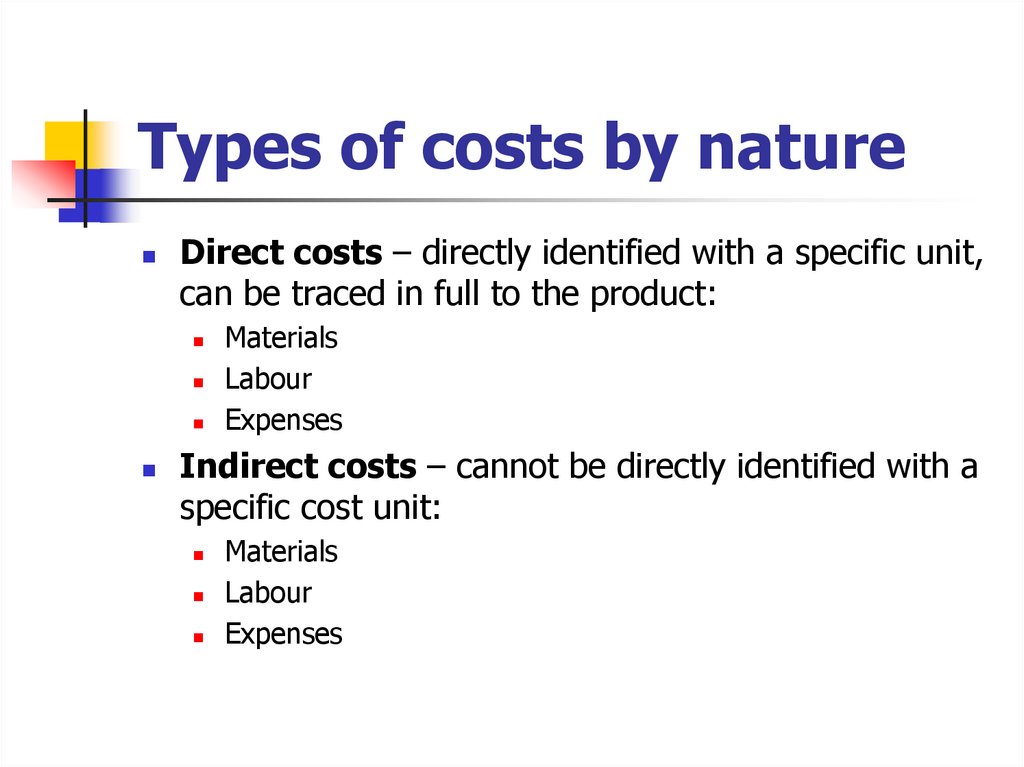

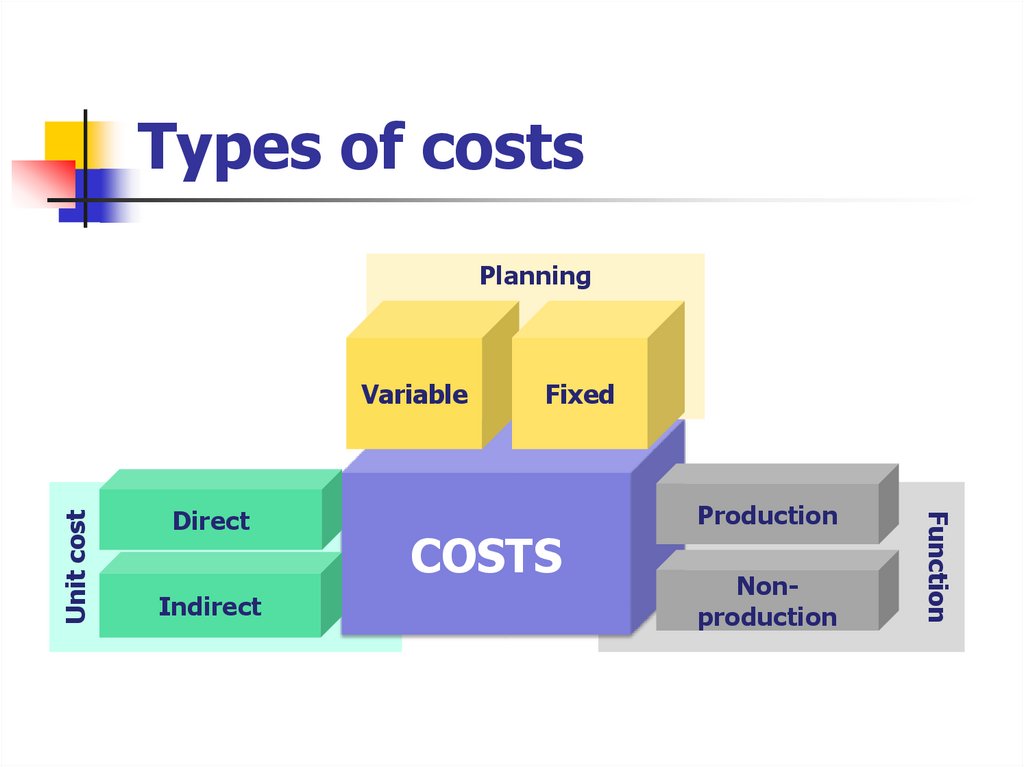

Types of costsVariable

Direct

Indirect

Fixed

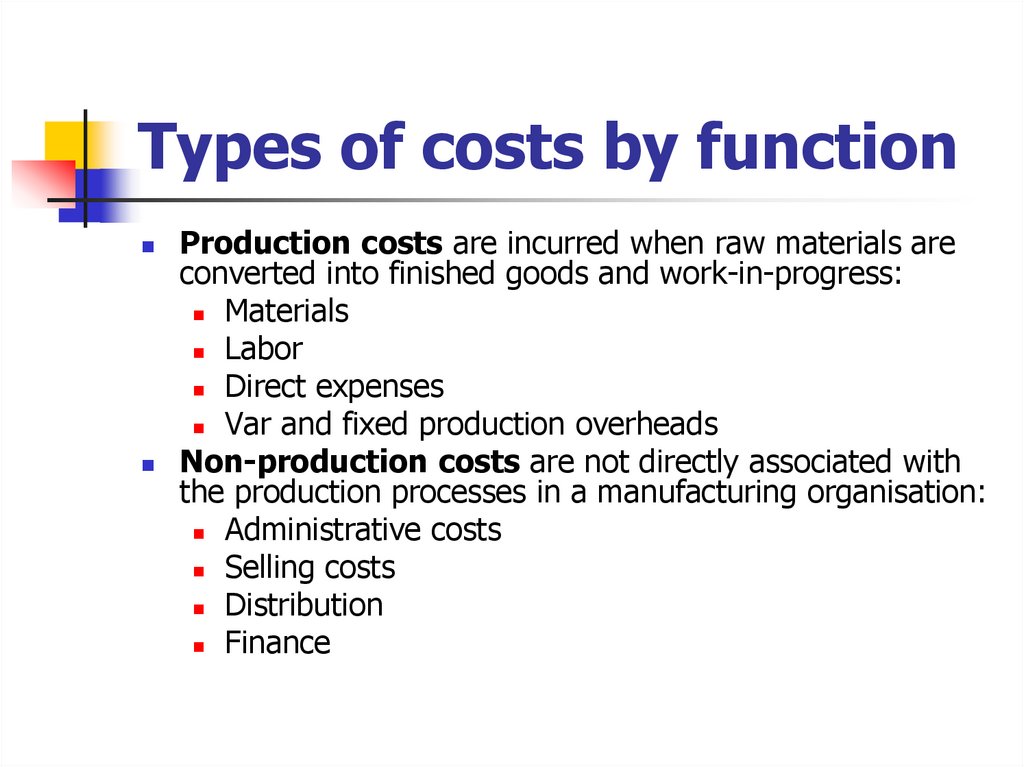

COSTS

Production

Nonproduction

11.

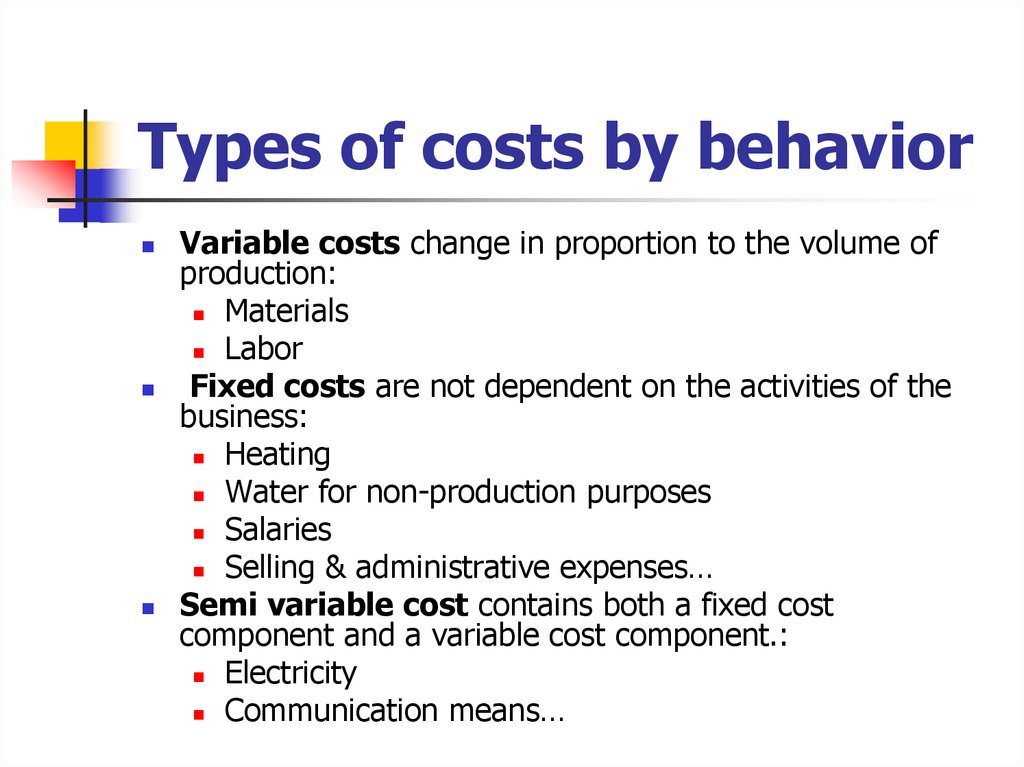

Types of costs by behaviorVariable costs change in proportion to the volume of

production:

Materials

Labor

Fixed costs are not dependent on the activities of the

business:

Heating

Water for non-production purposes

Salaries

Selling & administrative expenses…

Semi variable cost contains both a fixed cost

component and a variable cost component.:

Electricity

Communication means…

12.

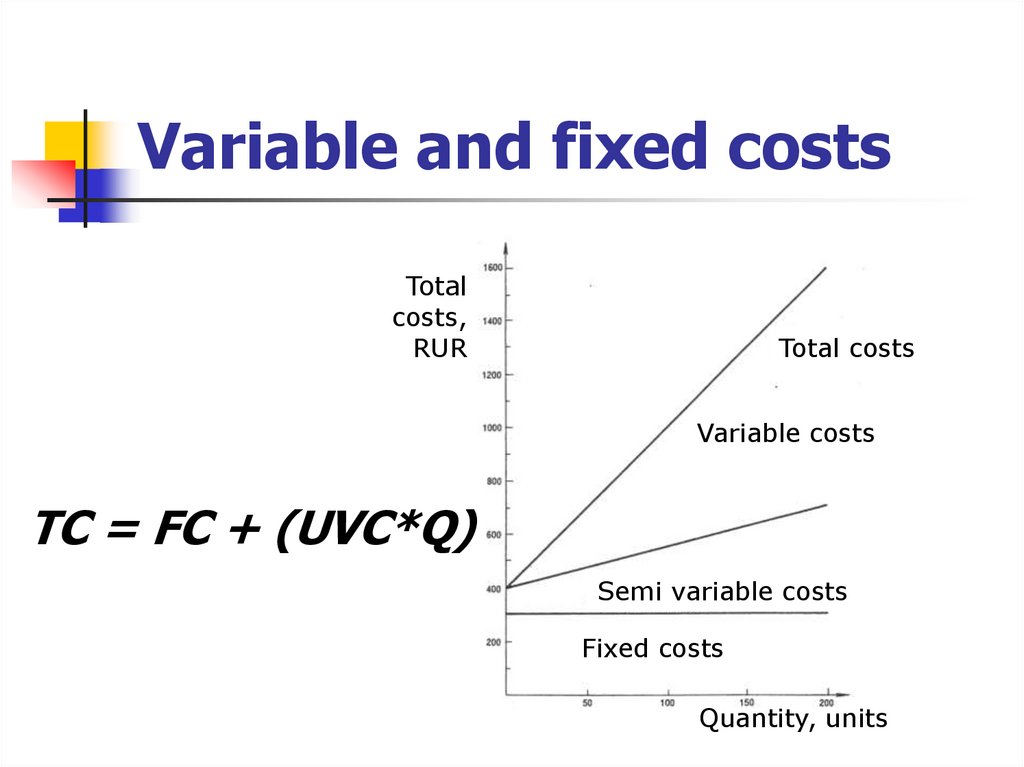

Variable and fixed costsTotal

costs,

RUR

Total costs

Variable costs

TC = FC + (UVC*Q)

Semi variable costs

Fixed costs

Quantity, units

13.

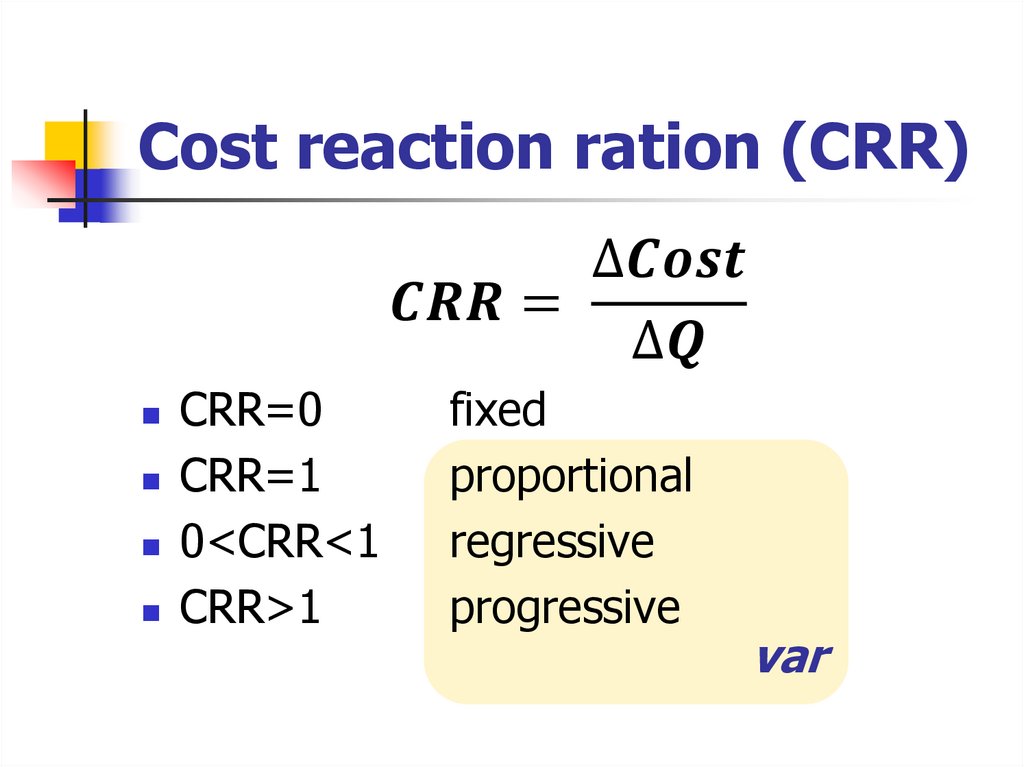

Cost reaction ration (CRR)∆