Address labor shortage through reforms to boost productivity Message 2) Address fiscal risks associated with aging (pension, health & long care)")

economics

economics english

englishSimilar presentations:

")

")

Russia economic. Report november 2007

1. Russia Economic Report November 2007

2. Main Messages

Robust growth supported by high energy prices, large capital inflows, rising

domestic demand and prudent macroeconomic management

Short-term challenges:

–

–

–

–

Control inflation

Limit rapid real exchange rate appreciation

Manage large capital flows

Maintain prudent fiscal policy

Medium-term challenges:

–

–

–

–

Sustain productivity growth

Close the infrastructure gap

Boost private investment

Promote economic diversification

2

3.

I. Recent EconomicDevelopments

3

4. Rapid Output Growth Driven by Booming Domestic Demand

Contributions to GDP Growth, in %GDP growth, %

12

9

8

7

6

5

4

3

2

1

0

10

8

6

4

2

0

-2

-4

-6

H1-2006

2001

2002

2003

2004

2005

2006

2007-9M

Final consumption

H1-2007

Capital formation

Net exports

• Economic growth remains robust. Having grown by 7.9 percent in 1H-2007, Russia

is likely to post full-year GDP growth of over 7 percent

• Output growth was driven by rising domestic demand, in particular, buoyant

household consumption (9.8 percent growth in 1H-2007) and business investment

(21 percent growth in 1H-2007)

• Negative contribution of net exports to GDP growth is explained by rapid import

growth and weak export performance, affected by the real appreciation of the ruble

4

5. Non-Tradable Sectors Continued to Boom

Output Growth by Sectors, 2006-2007Transport

Retail trade

9M-2007

Construction

9M- 2006

Electricity, gas, water

2006

Manufacturing

Extraction of mineral resources

Agriculture

Base industries and sectors

-5

0

5

10

15

20

25

• Sectors servicing domestic demand continued to boom in 9M-2007: construction

(23.5 percent) and retail trade (15 percent)

• Manufacturing also grew at healthy 10 percent in 9M-2007, driven by the steady

performance of a few sectors (machines and equipment, electro- technical, and

transportation equipment)

5

6. Manufacturing Growth: Strong But Tapering Off

Quarterly growth in Russia Manufacturing(relative to the same period of the previous year)

18.0

16.0

14.0

12.0

10.0

y = -0.1776x + 9.7795

8.0

6.0

4.0

2.0

0.0

IQ

2003

II Q

2003

III Q

2003

IV Q

2003

IQ

2004

II Q

2004

III Q

2004

IV Q

2004

IQ

2005

Manufacturing growth rate, %, y-o-y

II Q

2005

III Q

2005

IV Q

2005

IQ

2006

II Q

2006

III Q

2006

IV Q

2006

IQ

2007

II Q

2007

III Q

2007

Linear (Manufacturing growth rate, %, y-o-y)

•While still strong, manufacturing growth is decelerating. The impressive growth

posted in early 2007 was driven by temporary factors (warm winter, low output level in

Q1-2006 and unusually high investment demand in machine-building sectors)

6

7. The downward trend in manufacturing might be associated with the erosion in competitiveness in non-fuel, non-metal tradable sectors

Unit Labor Costs in ManufacturingManufacturing ULC index (US dollars), 2002 = 100

220

Russia

200

180

160

140

120

100

80

2002

2003

Russia

Slovak Republic

2004

Czech Republic

Euro Area

2005

Hungary

United States

2006

Poland

Parts of manufacturing that service domestic demand with limited competition

from imports may continue to thrive in Russia’s booming domestic market

But the real appreciation of the ruble, without commensurate increases in

productivity, drives up unit labor costs, hindering competitiveness in tradable

sectors (outside resources and metals)

7

8. Russia continues to experience an investment boom

Capital investment growth, % to previous year2007*

2006

2005

2004

2003

2002

2001

2000

22

20

18

16

14

12

10

8

6

4

2

0

•The aggregate fixed capital investment grew by 21.2 percent in 9-M of 2007

(from 11.8 percent growth in the same period in 2006)

•While capital investments decelerated in September 2007 they still posted

double-digit growth rates (16.1 percent, relative to the same month in 2006)

8

9. Despite Investment Boom, Domestic and Foreign Investments Went to A Few Sectors

Total Fixed Capital Investment by SectorForeign Direct Investment by Sector

H1-2006

(% of total)

3.7

19.5

18.7

3.2

H1-2007

(% of total)

4.7

20.4

17.5

3.2

Coke and oil products

1.9

1.6

Machine building

0.8

1.1

Transportation devices

Chemical products

Other non-metal mineral products

Metallurgy and metal products

0.9

2.3

1.3

5.3

1.1

1.9

1.4

4.1

6.3

3.6

2.8

25.7

4

4.5

11.1

6.9

2.9

2.9

23.3

4

4.5

12

Agriculture, hunting, forestry

Extraction of mineral resources

Manufacturing

Food & tobacco

Electricity, gas, water

Construction

Retail Trade,Wholesale Trade, Repair

Transport and communication

Railways

Communication

Real estate

2006

% total

H1-2007

% total

Agriculture, hunting, forestry

1.4

0.6

Extraction of mineral resources

Manufacturing

33.1

70.6

19

11.1

Electricity, gas and water

0.4

0.2

2

2.9

Retail & wholesale Trade, Repair

6.1

4.1

Hotels and restaurants

Transport and communication

Finance

0.2

2.8

11

0.1

1

4

Real estate

23.5

5.2

Construction

• Resource sectors and Non-Tradable Sectors (retail and construction) remain the

favorite direction for domestic and foreign investments.

• In Manufacturing, most investments went to the food and metal sectors

9

10. Inflation is Rising, Driven by Food Prices and Monetary Factors

CPI inflation, %Core CPI Inflation, %

PPI inflation, %

M2 growth, %

10M-2006

10M-2007

7.5

9.3

6.5

15.2 *

28.0*

8.9

17.0*

27.8*

*Data for 9 months. Source: CBR

• Inflation increased since April 2007 to reach 9.3 percent over 10M-2007 (compared to

7.5 percent in the same period of 2006)

• Most likely, end-of-year inflation will reach 11 percent (Dec/Dec)

10

11. Food prices increased, but prices of non-tradable goods and services also increased…

17.0015.00

13.00

11.00

9.00

7.00

5.00

3.00

Jan - Feb - Mar - Apr - May - June July - Aug - Sept Oct - Nov - Dec - Jan - Feb - Mar - Apr - May - June July - Aug - Sept

2006 2006 2006 2006 2006

2006 2006

2006 2006 2006 2007 2007 2007 2007 2007

2007 2007

2006

2006

2007

2007

CPI, p-o-p, %

Food CPI, p-o-p, %

Changes in prices of the main components of the CPI

weight in CPI

Meat products

Milk and milk products

Bread and bakery products

Fruit and vegetables

Alcohol

Clothing

Footwear

Construction materials

Housing utility services

Transportation services

Communication services

Education services

10.28

2.68

2.23

3.83

6.63

5.27

2.55

2.07

8.83

3.26

3.19

2.5

Price change (end period)

10M-2007

10M-2006

6.4

22.7

21.3

9.0

6.0

6.0

5.9

15.0

13.5

8.2

10.7

14.2

4.5

5.8

9.0

3.7

8.3

5.9

5.4

9.9

17.1

11.3

1.9

14.4

11

12. Keeping inflation in check is becoming increasingly difficult with large capital inflows

Accumulation of Foreign Reserves and the Stabilization Fund500000

450000

400000

350000

300000

250000

200000

150000

100000

50000

0

01.01.05

01.04.05

01.07.05

01.10.05

01.01.06

01.04.06

01.07.06

Gross foreign reserves, mln USD

01.10.06

01.01.07

01.04.07

01.07.07

01.10.07

Stabilization fund, mln USD

•Unlike oil revenues, capital inflows are not absorbed by the Stabilization Fund, driving

rapid money expansion and exerting upward pressures on the ruble.

• Given the limited monetary instruments for sterilization, one policy response would be

gradually allowing more rapid nominal appreciation of the ruble.

•The pace of nominal appreciation this year was slower than in 2006. The rubble

appreciated by 6 percent against the USD in nominal terms in 10M-2007 (compared to 7

percent in 2006).

12

13. BoP continued recording surpluses: weaker C/A was more than offset by stronger Capital Account

•Balance of Payments (USD billions)Current Account Balance

Trade Balance

Capital and Financial

Account

Errors and Omissions

Change in Reserves

2004

2005

2006

9M2006

9M2007*

58.6

85.8

83.8

118.4

94.5

139.2

79.7

111.2

57.1

94.1

-6.3

-13.6

11.9

-5.1

59.5

-7.1

45.2

-8.8

61.5

1.1

107.5

1.5

76.2

-10.2

106.4

• The surge in capital inflows pushed the BoP surplus to record highs, becoming an

important source of foreign reserve accumulation (gross foreign reserves: 447bn)

• Large capital inflows reflected acceleration in foreign borrowing by state

corporations and the banking sector. Net capital inflows to the private sector

amounted to 56.8 bn in 9M-2007 (compared to 26.3 bn in the same period last year)

• Russia has weathered well the global financial turmoil. By October 2007 Russia

received a net inflow of capital of about 10 bn

Total net capital inflows to the private sector

Net capital inflows to the banking sector

Net capital inflows to the non-banking sector

2006

9M-2006

9M-2007

Q3-2007

40.1

27.5

12.6

26.3

15.7

10.6

56.8

37.6

19.2

-9.4

0.7

-10.1

13

14. Fiscal surpluses continue, but recently fiscal policy has become more accommodative

Three year budget planFederal budget

surplus reached 7.1

percent of GDP (9M2007 )

Revenues

Expenditures

Of which:

General state management w/o

interest expenditure

National defense

National security, law enforcement

National economy

Housing and communal Services

Education

Culture, mass media

Health and sport

Social policy

Interbudgetary transfers

Transfers to extrabudgetary funds

Total non-interest expenditure

Interest payment

Oil and Gas Transfer

2007 Budget

Law

(approved)

Federal

Budget with

amendment

2007

22.3

17.5

2.1

2.6

2.1

1.6

0.2

0.9

0.2

0.7

0.7

2.5

3.4

17

0.5

2008

2009

2010

23.19

19

18.8

18.1

20.35

18.8

18.8

18.1

3.0 (0.7)*

2.6

2.1

2.3 (0.6)*

0.9 (0.7)*

0.9

0.2

0.9

0.9

2.8

3.3

19.9

0.5

2.1

2.7

2.2

2.1

1.9

2.7

2.3

2

1.8

2.7

2.2

1.2

0.9

0.2

0.6

0.8

2.6

3.8

18.2

0.5

6.1

0.8

0.2

0.6

0.9

2.3

3.8

18.2

0.5

5.3

0.8

0.2

0.6

1

2

4.1

17.5

0.6

4.5

(..)* capitalization of development institutions: Bank for Development, Russian Nanotechnology Corporation,

Investment Fund, Fund for Housing reform support

• The approved 3-year budget entails fiscal relaxation (that might reduce the budget surplus to 0.2 % of

GDP by 2008). Recent revisions to the 2007 federal budget entail additional fiscal easing (that would

reduce the budget surplus to 2.8 percent by end 2007).

• The bulk of the planned increase in public expenditures goes to infrastructure and social spending

with a view of boosting growth.

• Two cautionary notes:

(i) raising public investments might not be enough to achieve a sustained impact on economic

growth. Keeping up private investments and improving the efficiency of investments will be as

important;

(ii) the pace of fiscal policy needs to be studied carefully to avoid exacerbating tensions in the

14

macro mix (additional fiscal stimulus might increase pressures for ruble appreciation)

15. Prospects

• Growth is likely to remain robust. With energy prices setto remain high, booming domestic demand will continue to

translate into strong growth in services and manufacturing

• However, growth might slowdown if medium-term

challenges are not addressed….

– Sustain Productivity Growth (which can also help alleviating

pressures from the real appreciation of the exchange rate)

– Promote Economic Diversification

– Boost Private Investment

15

16.

II. Productivity Growthin Russia

16

17. Russia has experienced a productivity surge, propelling economic growth

Total factor productivity growth (5.8 percent) drove GDP growth (6.5 percent) over (1999-2005)Real income per capita (constant $2000,PPP) rose from $5,964 in 1998 to $9,650 in 2005

GDP Index (1989=100): Russia, ECA, and EU-10

Sources of Growth: Russia and Comparators (1999-2005)

Contributions of K, L, and TFP Growth to Aggregate Growth

140

130

9

EU10

120

110

7

ECA

100

5

(%)

TFPGr

3

90

LgrCont

80

KgrCont

70

RUSSIA

60

1

50

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

EU10

1992

Industrial

1991

China

1990

RUSSIA

1989

40

-1

But capital and labor

accumulation played little

role in total output growth

17

18. What are the drivers of the productivity surge?

• Capacity utilization• Sectoral shifts

• Firm dynamics

18

19. Higher capacity utilization explains part of the productivity surge

• Utilization of excess capacity yields ‘easy’ productivity gains in a growth rebound after a deep recession• But higher capacity utilization only explains part of the productivity surge

Sources of Grow th in Russia: 1999-2005

Im pact of Adjustm ent for Capacity Utilization

8

(%)

6

TFP

4

L

2

K

0

No Adjustm ent for

Cap. Util.

Adjusting for

Capacity Utilization

Even after adjusting for capacity utilization,

TFP growth still accounts for 4.15

percent of total GDP growth (of 6.5

percent)

19

20. The productivity surge is also explained by major sectoral shifts in the economy

A substantial reallocation of resources toward servicesLabor Productivity Growth, 1999-2004

Sectoral Shares in Russia

Agriculture

Industry

Services

within

8%

100%

reallocation

7%

90%

80%

6%

70%

5%

60%

4%

50%

3%

40%

2%

30%

1%

20%

0%

10%

- 1%

0%

1990

2005

1990

Total Value Added

2003

Total Employment

- 2%

RUSSIA

EU15

EU10

Efficiency gains ‘within sectors’ had more impact on total

productivity growth than cross-sector shifts

Labor productivity over 1999-2004 grew by :

4.4 percent in agriculture,

4.7 percent in industry and

6.4 percent in services

20

21. Firm dynamics

Productivity growth came mostly from efficiency gainswithin firms -but reallocation & net entry also mattered

Sources of Productivity Growth in Russian Manufacturing

Contribution rates (in % )

Within

Net entry

Reallocation

25

20

15

10

5

0

1998-2001

2001-2004

Highest Productivity

Growth in ICT sectors

RUSSIA: Decomposition for Manufacturing, Contributions to Aggregate

Productivity Growth 2001-2004

80

Within

70

Reallocation

Net Entry

60

40

30

20

10

0

-10

NACE Industry Code

Furniture

Other Transport

Motor Vehicles

Precision Tools

Elec. Mach.

Electronics

Machinery

Fabricated Metal

Basic Metals

Minerals

Rubber/Plastics

Chemicals

Printing

Paper

Wood

Leather

Garments

Textiles

-30

Food

-20

MANU

Growth Rate (%)

50

22

22. Productivity growth came mostly from efficiency gains within firms -but reallocation & net entry also mattered

Firm turnover plays a smaller role than inother advanced economies

In advanced market economies 5-20 percent of firms enter and exit the market every year.

In Russia, only about 5 percent of firms were created or destroyed during the last decade

60

50

40

30

20

10

0

UK

USA

Canada

Mexico

Korea

Firm Entry rates

Taiwan

Slovenia

Hungary

RUSSIA

Firm Exit rates

•Private entrants are less productive than state-owned peers (suggesting barriers to entry and exit)

• Entrants do not promote productivity of incumbents (suggesting weak market competition)

Labor Productivity - Pooled Manufacturing

Incumbent Prod Growth

Russia

Five-Year Differencing, Real Gross Output

Country and Industry Time Averages

150

100

50

0

-40

-20

0

-50

20

Incumbents' Productivity Growth

1.5

Correlation Coefficient: 0.5800***

1.0

0.5

40

60

80

100

0.0

-0.5

-1.0

-100

Net Entry Contribution

-0.5

0.0

0.5

Net Entry Productivity Growth

Note: Excluding Brazil and Venezuela. Outliers Excluded.

1.0

1.5

23

23. Firm turnover plays a smaller role than in other advanced economies

Challenges AheadIn spite of the productivity surge, Russia’s income per capita remains low (at 28

percent of EU-15 average)

Rapid productivity gains were ‘easy’ to achieve in the first years of the growth

rebound

But now with the economy growing close to potential, sustaining productivity

gains will be more difficult.

Capital and labor accumulation must play a greater role

Economic diversification including higher export sophistication also needs to

be promoted…

Share of Medium and High Tech Products in Total Exports (%)

1995-1998

40

% of Discovery in Total Exports, 1995-2005

1.2

1999-2005

1.0

35

30

0.8

25

0.6

20

15

0.4

10

0.2

5

0.0

0

RUSSIA

EU-10

RUSSIA

EU-10

Source: Bank staff calculations; UN-Comtrade, 2007

24

24. Challenges Ahead

Sustaining Productivity Growth Calls For Policy Reformsthat Accelerate Reallocation of Resources towards More

Efficient Uses

Russia has most to gain from policy catch-up

Impact of Policy Improvements on Productivity Growth:

Catching Up with the Median Industrial Country

5

(in percentages)

4

3

2

1

0

-1

RUSSIA

Education

Financial Development

ECA

Trade Openness

Institutional Quality

EU-10

Infrastructure Stock

Infrastructure Quality

25

25. Sustaining Productivity Growth Calls For Policy Reforms that Accelerate Reallocation of Resources towards More Efficient Uses

III.From Red to Gray:

The Third Transition of

Aging Population in Russia

26

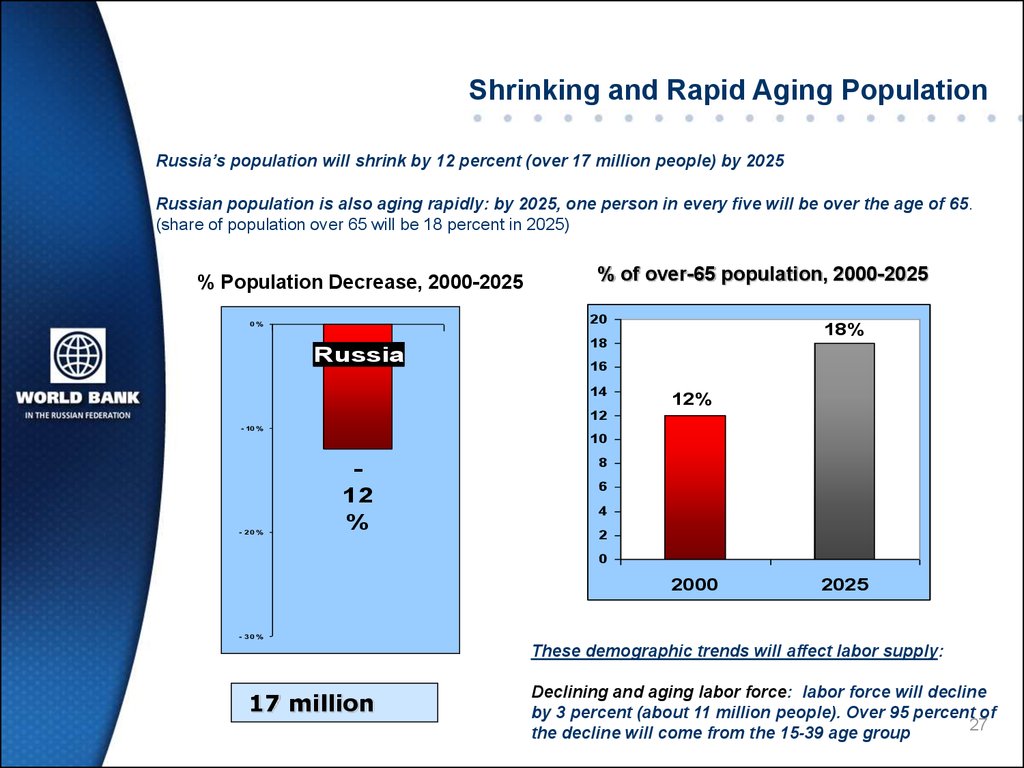

26.

Shrinking and Rapid Aging PopulationRussia’s population will shrink by 12 percent (over 17 million people) by 2025

Russian population is also aging rapidly: by 2025, one person in every five will be over the age of 65.

(share of population over 65 will be 18 percent in 2025)

% Population Decrease, 2000-2025

% of over-65 population, 2000-2025

20

0%

Russia

18%

18

16

14

12%

12

- 10 %

10

- 20%

12

%

8

6

4

2

0

2000

2025

- 30%

These demographic trends will affect labor supply:

17 million

Declining and aging labor force: labor force will decline

by 3 percent (about 11 million people). Over 95 percent of

27

the decline will come from the 15-39 age group

27. Shrinking and Rapid Aging Population

But growing older does not have to mean growing slowerAging is not a stop sign for growth:

Message 1) Address labor shortage through reforms to boost productivity

Message 2) Address fiscal risks associated with aging (pension, health & long care)

Russia, Growth decomposition, 1998-2005

10%

32%

58%

Share of growth due to higher:

Labor productivity

Employment rates

Working-age population

28

28. Aging is not a stop sign for growth: Message 1) Address labor shortage through reforms to boost productivity Message 2) Address fiscal risks associated with aging (pension, health & long care)

Thank you for your attention29