business

businessSimilar presentations:

Valuation of Business

1.

Valuation ofBusiness

NVC-TW10

Alisher Ismailov

2.

Agenda• Buying and existing business

• Due diligence before purchasing

• Business Valuation & Its methods

• Determining the Business Value of your

business

3.

Buying anexisting

business

• It is less risky than starting from scratch because facilities,

employees, and customers will likely be in place.

• To acquire a business with ongoing operations and

established relationships with loyal customers and

reliable suppliers

• The business has established trade credit, which is crucial

because relationships with suppliers and others take a

long time to develop.

• It is easier to own a business if the entrepreneur has

limited business experience, especially if the owner stays

on for a time to help with the transition.

• To begin a business more quickly than starting from

scratch

• To obtain an established business at a price below what a

new business or franchise would cost

4.

What toLook For

in a

Business

• A business that had a broad scope that would

insulate it from market downturns.

• A business with existing customers and vendors

• A low-tech business with high growth

• A market that was not so large as to encourage

significant players but not so small that the

company couldn’t grow.

• Available float from suppliers; in other words,

leeway in paying vendors.

• Manageable seasonality

• Cost cutting potential

5.

Investigatingand

Evaluating

Available

Businesses

Due Diligence

• The exercise of prudence, such as

would be expected of a reasonable

person, in the careful evaluation of a

business opportunity

Relying on Professionals

• Accountants

• Attorneys

• Other experienced business owners

6.

Find OutWhy the

Business Is

For Sale

• Owner’s stated reasons for selling the business

• Poor health or illness in the family

• Wants to retire while he can still enjoy life

• Desires to relocate to a different section of

the country

• Has accepted a position working for another

company

• Wants to start a new business in a different

industry

• Has to sell the business to generate funds to

settle a divorce, lawsuit, etc.

• Beware of sellers who may have priced the business

at more than its worth or who have “cooked the

books” to make the business appear to be more

attractive than it really is.

7.

Thepotential

reasons

could be

Larger companies are squeezing the firm out of the market

Key employees have been leaving

The industry is very mature and there aren’t any new ways or

places to grow

Competitors’ products (or services) are superior

The business has developed a negative reputation in the

community

The firm is facing a pending lawsuit

The business is just not profitable

The physical facilities are old or obsolete and in need of major

renovation/repairs

8.

Examiningthe

Financial

Data

Review financial statements and tax returns for the

past five years.

Recognize that financial data can be misleading.

Assets overvalued

Expenses under-stated

Income over-stated

Unrecorded debts

Adjust asset valuations to reflect the true state of the

business.

9.

BusinessValuation

• Business valuation is the process of determining

the economic value of a company or

organisation. The valuation provides an

estimate of what the business is worth and is

usually done by professional appraisers,

accountants, or investment bankers.

10.

Why to doBusiness

valuation

• Business valuation is important for various reasons,

including:

1. Mergers and Acquisitions: A company may want to

buy another business, and business valuation helps

determine the target company’s value.

2. Sale of the Business: A business owner may want

to sell their business, and business valuation can

help determine a fair asking price.

3. Financing: Business valuation is essential when

raising capital from investors or getting a loan from

a bank.

4. Tax Purposes: The value of a business is essential

for estate and gift taxes, and business valuation

provides a fair value for tax purposes.

5. Litigation: Business valuation is essential in legal

proceedings, such as shareholder disputes, divorce

proceedings, and bankruptcy.

11.

Businessvaluation

Methods

• Market Approach: This approach determines

the value of a business by comparing it to

similar businesses that have sold recently.

• Income Approach: This approach determines

the value of a business based on its current and

projected income stream.

• Asset Approach: This approach determines the

value of a business based on its assets and

liabilities.

12.

TheMarket

Approach

The market approach is a business valuation method that determines the value of a

business by comparing it to similar businesses that have sold recently. The market

approach is based on the assumption that similar businesses in the same industry will

have similar valuations.

The steps in the market approach for business valuation include:

• Identify Comparable Transactions: The first step is to identify comparable

transactions or businesses that have sold recently in the same industry. These

transactions should be similar in size, location, industry, and other relevant

factors.

• Adjust for Differences: Once the comparable transactions have been identified,

adjustments are made for any differences between the subject business and the

comparable transactions. For example, if the comparable transaction had a higher

growth rate or a better location, an adjustment would be made to account for

these differences.

• Determine Valuation Multiples: After making the necessary adjustments,

valuation multiples are determined based on comparable transactions. These

multiples are ratios that compare the price of the business to a financial metric

such as revenue, EBITDA, or net income.

• Apply Multiples to Subject Business: The next step is to apply the valuation

multiples to the subject business. For example, if the average valuation multiple

for the comparable transactions was three times the revenue, and the subject

business had revenue of $1 million, the estimated value would be $3 million.

• Consider Additional Factors: Finally, additional factors such as the current market

conditions, growth potential, and industry trends should be considered to ensure

that the valuation is reasonable and accurate.

13.

MarketApproach

Example

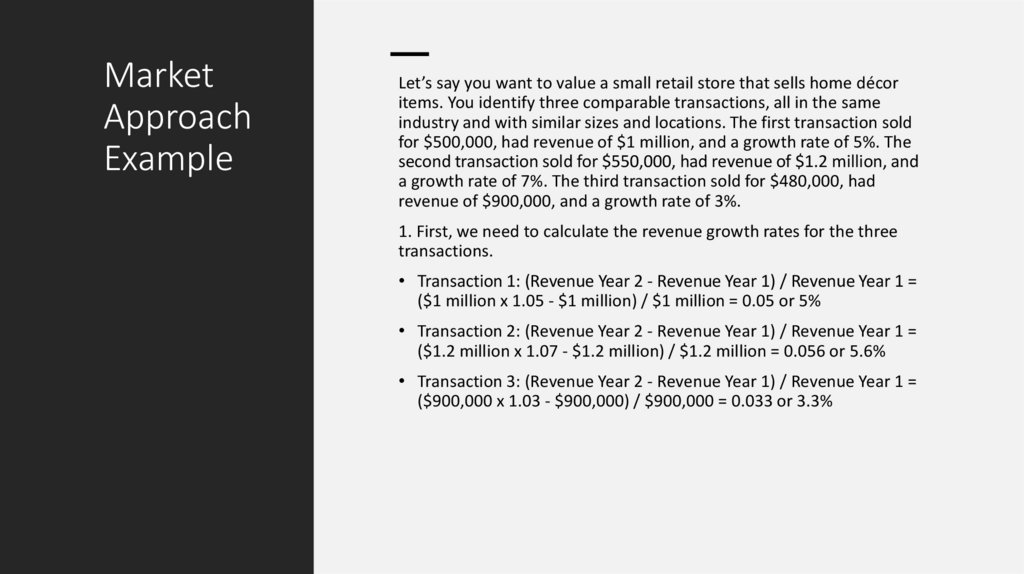

Let’s say you want to value a small retail store that sells home décor

items. You identify three comparable transactions, all in the same

industry and with similar sizes and locations. The first transaction sold

for $500,000, had revenue of $1 million, and a growth rate of 5%. The

second transaction sold for $550,000, had revenue of $1.2 million, and

a growth rate of 7%. The third transaction sold for $480,000, had

revenue of $900,000, and a growth rate of 3%.

1. First, we need to calculate the revenue growth rates for the three

transactions.

• Transaction 1: (Revenue Year 2 - Revenue Year 1) / Revenue Year 1 =

($1 million x 1.05 - $1 million) / $1 million = 0.05 or 5%

• Transaction 2: (Revenue Year 2 - Revenue Year 1) / Revenue Year 1 =

($1.2 million x 1.07 - $1.2 million) / $1.2 million = 0.056 or 5.6%

• Transaction 3: (Revenue Year 2 - Revenue Year 1) / Revenue Year 1 =

($900,000 x 1.03 - $900,000) / $900,000 = 0.033 or 3.3%

14.

MarketApproach

Example

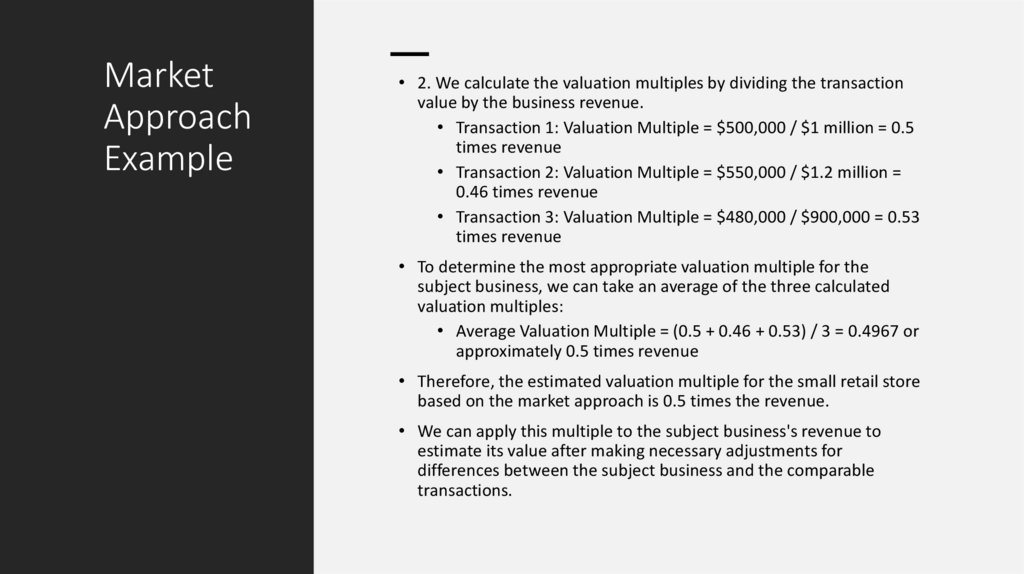

• 2. We calculate the valuation multiples by dividing the transaction

value by the business revenue.

• Transaction 1: Valuation Multiple = $500,000 / $1 million = 0.5

times revenue

• Transaction 2: Valuation Multiple = $550,000 / $1.2 million =

0.46 times revenue

• Transaction 3: Valuation Multiple = $480,000 / $900,000 = 0.53

times revenue

• To determine the most appropriate valuation multiple for the

subject business, we can take an average of the three calculated

valuation multiples:

• Average Valuation Multiple = (0.5 + 0.46 + 0.53) / 3 = 0.4967 or

approximately 0.5 times revenue

• Therefore, the estimated valuation multiple for the small retail store

based on the market approach is 0.5 times the revenue.

• We can apply this multiple to the subject business's revenue to

estimate its value after making necessary adjustments for

differences between the subject business and the comparable

transactions.

15.

IncomeApproach

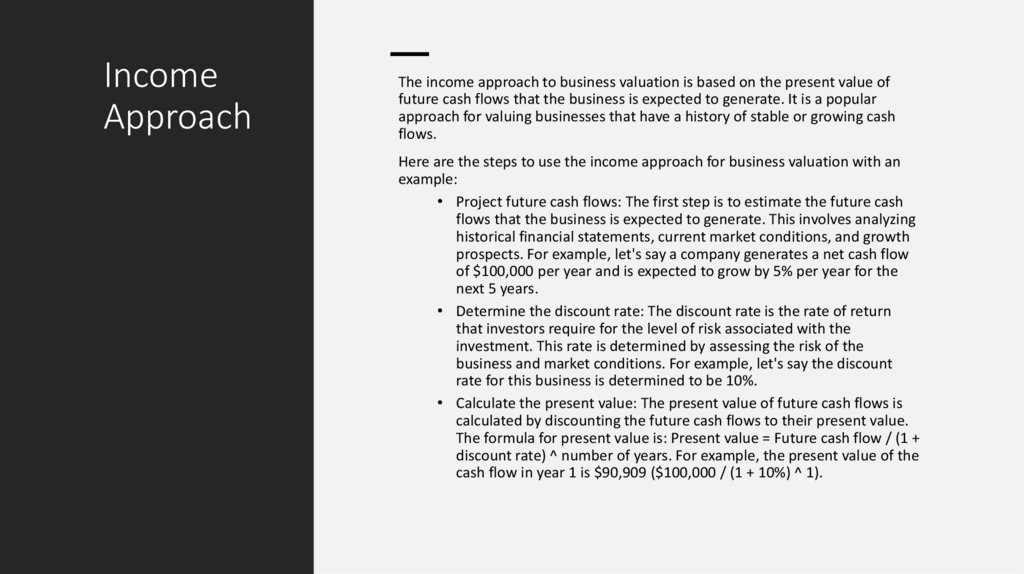

The income approach to business valuation is based on the present value of

future cash flows that the business is expected to generate. It is a popular

approach for valuing businesses that have a history of stable or growing cash

flows.

Here are the steps to use the income approach for business valuation with an

example:

• Project future cash flows: The first step is to estimate the future cash

flows that the business is expected to generate. This involves analyzing

historical financial statements, current market conditions, and growth

prospects. For example, let's say a company generates a net cash flow

of $100,000 per year and is expected to grow by 5% per year for the

next 5 years.

• Determine the discount rate: The discount rate is the rate of return

that investors require for the level of risk associated with the

investment. This rate is determined by assessing the risk of the

business and market conditions. For example, let's say the discount

rate for this business is determined to be 10%.

• Calculate the present value: The present value of future cash flows is

calculated by discounting the future cash flows to their present value.

The formula for present value is: Present value = Future cash flow / (1 +

discount rate) ^ number of years. For example, the present value of the

cash flow in year 1 is $90,909 ($100,000 / (1 + 10%) ^ 1).

16.

IncomeApproach

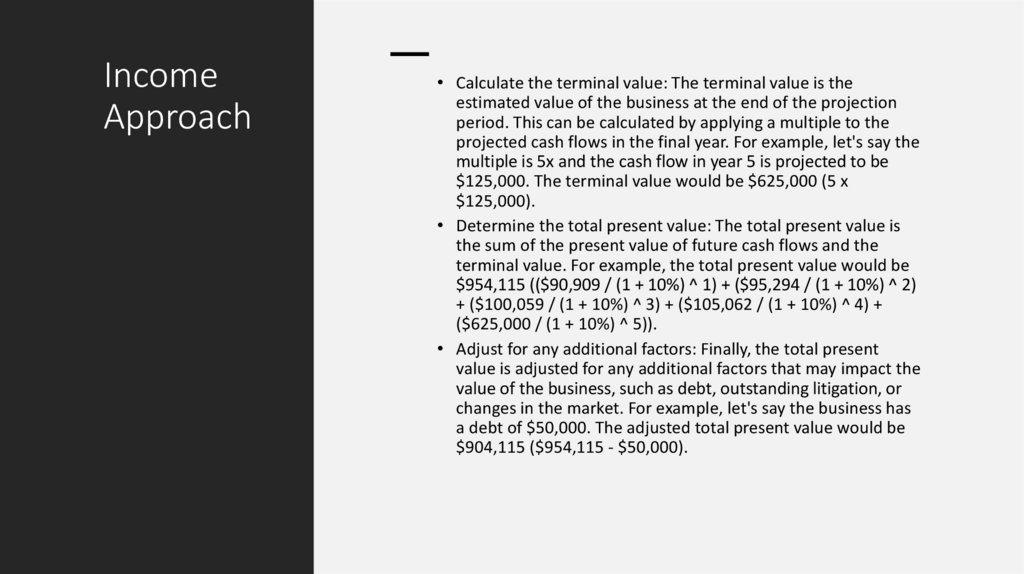

• Calculate the terminal value: The terminal value is the

estimated value of the business at the end of the projection

period. This can be calculated by applying a multiple to the

projected cash flows in the final year. For example, let's say the

multiple is 5x and the cash flow in year 5 is projected to be

$125,000. The terminal value would be $625,000 (5 x

$125,000).

• Determine the total present value: The total present value is

the sum of the present value of future cash flows and the

terminal value. For example, the total present value would be

$954,115 (($90,909 / (1 + 10%) ^ 1) + ($95,294 / (1 + 10%) ^ 2)

+ ($100,059 / (1 + 10%) ^ 3) + ($105,062 / (1 + 10%) ^ 4) +

($625,000 / (1 + 10%) ^ 5)).

• Adjust for any additional factors: Finally, the total present

value is adjusted for any additional factors that may impact the

value of the business, such as debt, outstanding litigation, or

changes in the market. For example, let's say the business has

a debt of $50,000. The adjusted total present value would be

$904,115 ($954,115 - $50,000).

17.

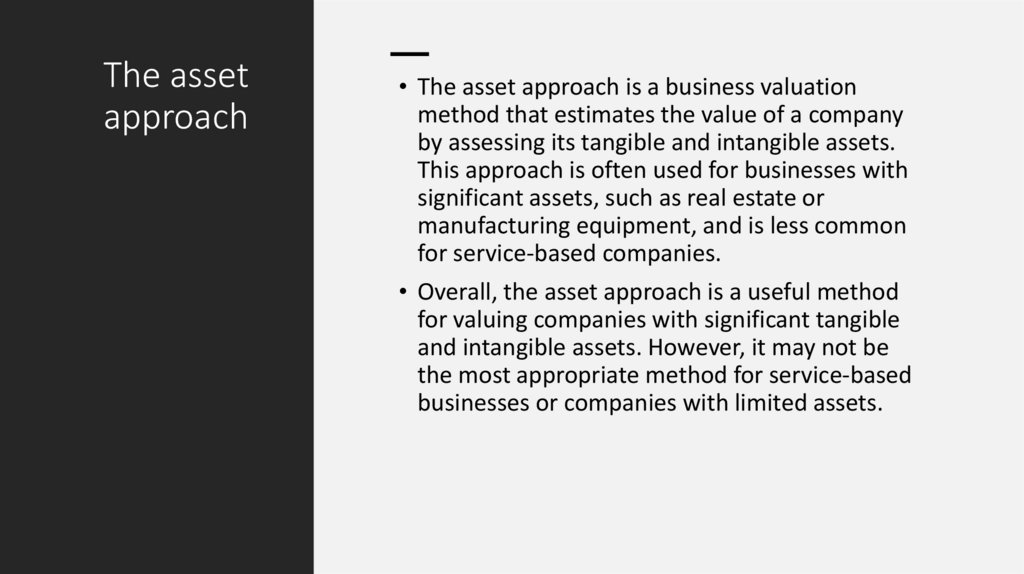

The assetapproach

• The asset approach is a business valuation

method that estimates the value of a company

by assessing its tangible and intangible assets.

This approach is often used for businesses with

significant assets, such as real estate or

manufacturing equipment, and is less common

for service-based companies.

• Overall, the asset approach is a useful method

for valuing companies with significant tangible

and intangible assets. However, it may not be

the most appropriate method for service-based

businesses or companies with limited assets.

18.

The assetapproach

steps

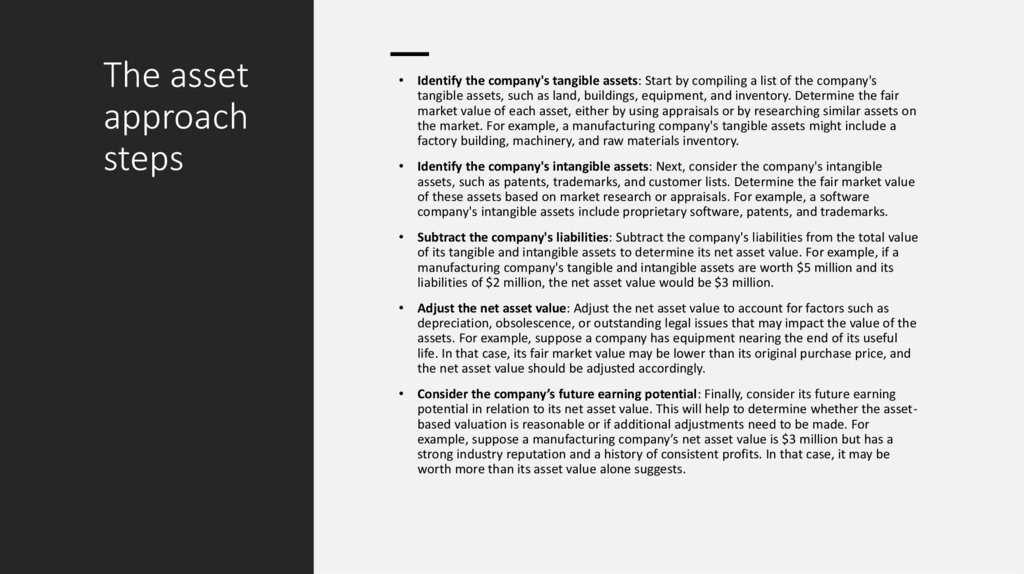

Identify the company's tangible assets: Start by compiling a list of the company's

tangible assets, such as land, buildings, equipment, and inventory. Determine the fair

market value of each asset, either by using appraisals or by researching similar assets on

the market. For example, a manufacturing company's tangible assets might include a

factory building, machinery, and raw materials inventory.

Identify the company's intangible assets: Next, consider the company's intangible

assets, such as patents, trademarks, and customer lists. Determine the fair market value

of these assets based on market research or appraisals. For example, a software

company's intangible assets include proprietary software, patents, and trademarks.

Subtract the company's liabilities: Subtract the company's liabilities from the total value

of its tangible and intangible assets to determine its net asset value. For example, if a

manufacturing company's tangible and intangible assets are worth $5 million and its

liabilities of $2 million, the net asset value would be $3 million.

Adjust the net asset value: Adjust the net asset value to account for factors such as

depreciation, obsolescence, or outstanding legal issues that may impact the value of the

assets. For example, suppose a company has equipment nearing the end of its useful

life. In that case, its fair market value may be lower than its original purchase price, and

the net asset value should be adjusted accordingly.

Consider the company’s future earning potential: Finally, consider its future earning

potential in relation to its net asset value. This will help to determine whether the assetbased valuation is reasonable or if additional adjustments need to be made. For

example, suppose a manufacturing company’s net asset value is $3 million but has a

strong industry reputation and a history of consistent profits. In that case, it may be

worth more than its asset value alone suggests.

19.

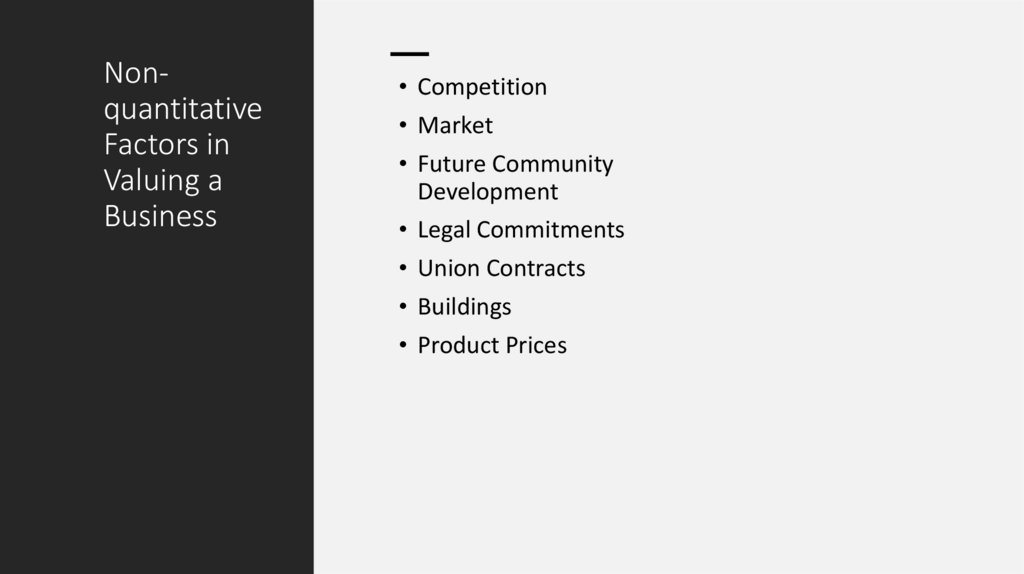

NonquantitativeFactors in

Valuing a

Business

• Competition

• Market

• Future Community

Development

• Legal Commitments

• Union Contracts

• Buildings

• Product Prices

20.

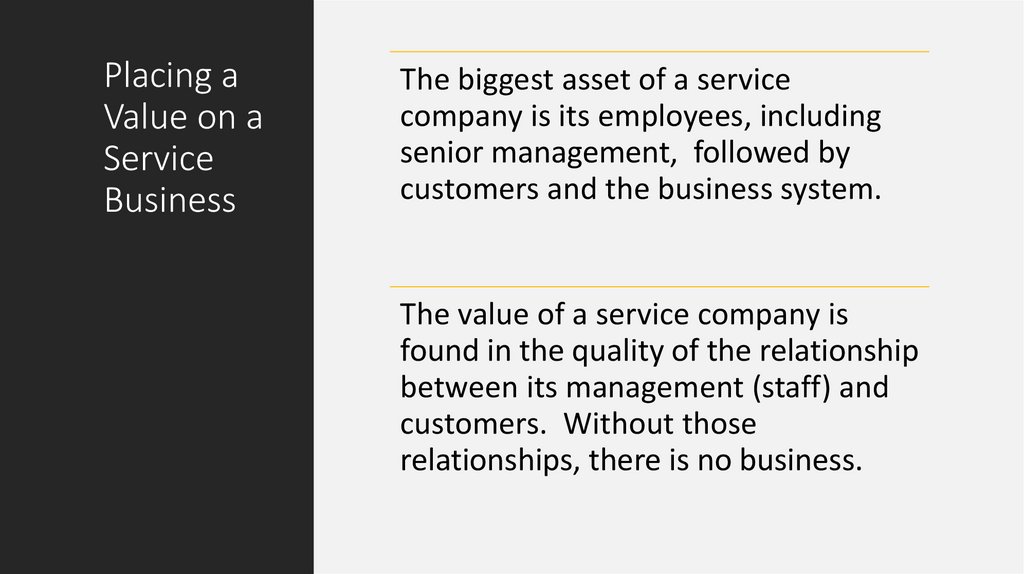

Placing aValue on a

Service

Business

The biggest asset of a service

company is its employees, including

senior management, followed by

customers and the business system.

The value of a service company is

found in the quality of the relationship

between its management (staff) and

customers. Without those

relationships, there is no business.

21.

PossibleConditions

on the

Purchase

of a

Service

Business

The owner must stay on as an employee

for two years, an employee for one year,

and a consultant for two more.

Any loss of an account or a large

customer in place at the sale’s closing

will reduce the payout by some defined

amount.

One-third of the total purchase price will

be paid at closing. The remainder will be

paid in equal payments over three years.

22.

Calculateyour

business

worth

• Go to https://www.bizex.net/business-valuation-tool or scan the

QR Code

• Give details of your business from your financial forecasts

• Give determinants of multiple of earnings and select your risk

factors

• Get your business value and compare it with its valuation by assets